Blockchain entered public consciousness through dramatic headlines—surging cryptocurrency markets, sudden crashes, and stories of early adopters becoming overnight millionaires or losing fortunes. These narratives shaped perceptions long before people understood the underlying technology. Despite years of development, mature enterprise deployments, and improved regulatory guidance, inaccurate assumptions continue to dominate discussions. Many business leaders still approach blockchain with expectations shaped by hype cycles rather than grounded analysis. This confusion influences investment decisions, public policy, and even academic research. It has become clear that separating fact from fiction is essential for anyone evaluating blockchain’s real role in the digital economy.

Much of the misunderstanding stems from the technology’s rapid evolution. What was true during blockchain’s early years is often outdated today, but older beliefs remain influential. Some people still think blockchains are only for cryptocurrency. Others believe blockchains solve every trust-related problem. Both assumptions oversimplify the diverse landscape of distributed ledger technologies. Because blockchain spans finance, supply chains, identity systems, data security, and digital assets, misconceptions can easily distort how individuals and institutions evaluate its potential. Clearing these myths helps organizations make better decisions and avoid misguided investments based on outdated or exaggerated claims.

Hype, Headlines and Half-truths

Public narratives about blockchain evolved through cycles of excitement and skepticism. Early coverage positioned it as a revolutionary force set to disrupt every industry. Then came backlash—stories about hacks, speculative bubbles, and regulatory crackdowns. These extremes created an environment where nuance rarely survived. As a result, half-truths gained traction, whether glorifying blockchain as a universal solution or condemning it as inherently flawed.

This dynamic shaped corporate boardrooms as well. Decision-makers often encountered conflicting reports: glowing case studies from technology vendors on one side, and cautious regulatory statements on the other. Without clear standards or benchmarks, the gap between expectations and reality widened. Headlines exaggerated technological limitations or capabilities, blurring the line between reasonable assessment and myth-making. Today, those leftover narratives still impact blockchain strategy across industries.

Why these Blockchain Misconceptions Matter for Business and Policy

Misunderstandings about blockchain are not trivial—they shape significant decisions. If leaders assume blockchain is too slow or energy-intensive, they may avoid solutions that actually address pressing operational challenges. Conversely, if they believe blockchain removes the need for governance or oversight, projects can fail from unrealistic assumptions. Policymakers face similar dilemmas. Some fear that blockchain automatically enables criminal activity, while others assume it cannot be regulated at all. These misconceptions slow the establishment of responsible frameworks that support innovation while protecting consumers.

Correcting these myths helps businesses identify where blockchain provides tangible value. Instead of chasing trends or avoiding innovation out of fear, organizations can approach blockchain as a practical tool—neither miraculous nor dangerous, but one piece of a broader digital infrastructure strategy. Understanding blockchain’s real strengths and weaknesses enables more effective risk management, smoother deployment, and more meaningful experimentation.

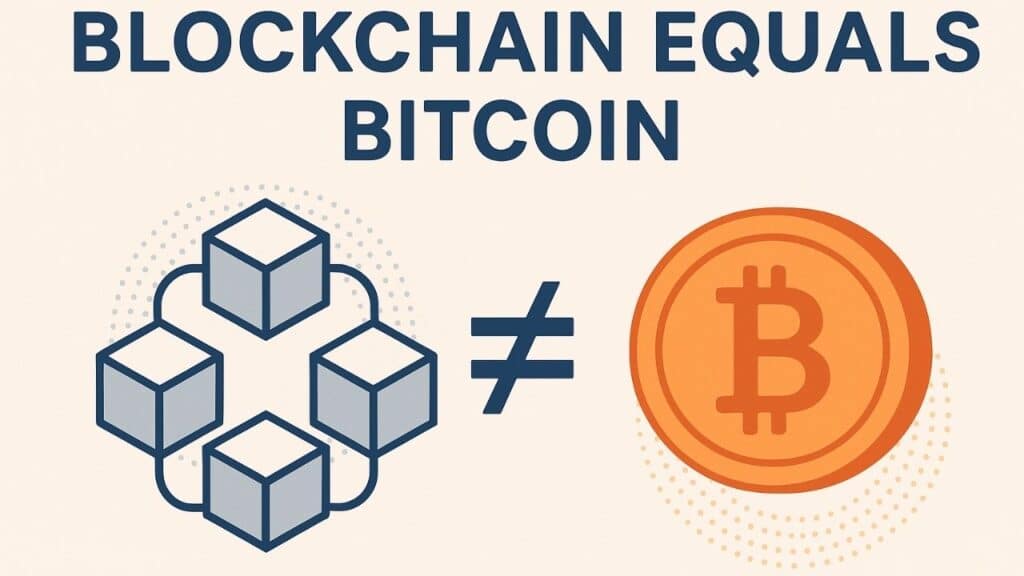

Myth 1 – “Blockchain Equals Bitcoin”

One of the most entrenched blockchain myths is the belief that blockchain and Bitcoin are interchangeable. This misconception persists because Bitcoin was the first mainstream application of blockchain, and for many, it defined the entire category. In reality, blockchain is a broader technology that underpins a wide range of applications—including but not limited to cryptocurrencies. Yet, the association remains strong due to years of media coverage that lumped the two together, reinforcing the notion that blockchain exists solely to support digital currency transactions.

How this myth started

During Bitcoin’s early rise, the term “blockchain” rarely appeared in public conversation. News stories focused primarily on Bitcoin’s price movements, speculation, and volatility. The infrastructure enabling it remained in the background. As people learned about blockchain through this limited lens, they began equating the ledger with the currency. That early framing stuck, especially because Bitcoin’s success overshadowed other potential uses of distributed ledger technology. Even technologists initially used “Bitcoin” as shorthand for the entire idea, reinforcing the misconception.

What blockchain actually is

Blockchain is a distributed ledger designed to record and secure data across multiple nodes without central authority. Bitcoin happens to run on one type of blockchain, but many blockchains bear little resemblance to the Bitcoin network. Some are public and decentralized, while others are private and controlled by organizations. Businesses adopt blockchain for reasons far beyond currency—such as transparency, auditability, automation through smart contracts, and secure data sharing. Once separated from Bitcoin’s public narrative, blockchain emerges as a flexible framework applicable across industries.

Myth 2 – “Blockchain Is Just Another Database in the Cloud”

Another persistent blockchain misconception is the belief that it functions like a traditional database. This misunderstanding often appears in early-stage business discussions where decision-makers assume blockchain offers little beyond what existing cloud systems already provide. However, blockchain introduces structural differences that make it suitable for very specific types of workflows—particularly those involving trust boundaries, multi-party coordination, and shared recordkeeping.

Databases vs distributed ledgers

Traditional databases rely on central administration. A single organization controls how records are stored, who can edit them, and how errors are corrected. This model works well when trust is concentrated in one place. Blockchains, by contrast, intentionally distribute authority. All participants maintain synchronized copies of the ledger, and changes require consensus rather than unilateral action. This structure makes tampering difficult, because no single entity can modify records without detection. The goal is not to replace databases, but to solve challenges that centralized systems cannot easily address.

When a blockchain structure really adds value

Blockchain delivers value when multiple parties need shared, tamper-resistant data. For example, global supply chain participants may not trust a single company to host the definitive record of product movement. Financial institutions collaborating on trade finance require auditability that spans borders and systems. Healthcare organizations sharing patient data may need transparent rules for access and verification. In such cases, blockchain’s distributed nature provides protections and coordination mechanisms that conventional databases cannot offer. Blockchain becomes an infrastructure for trusted collaboration—not merely another data repository.

Myth 3 – “Blockchain Is Anonymous and Perfect for Criminals”

Popular imagination often links blockchains with illicit transactions. This belief stems from early news stories about darknet markets that used cryptocurrency as a payment method. The idea spread quickly: if blockchain transactions are encrypted and borderless, criminals can operate unseen. Yet this myth oversimplifies how blockchain works. Most blockchains create transparent, traceable records that remain visible forever, which in many cases makes investigations easier, not harder.

Pseudonymity vs real anonymity

Blockchain addresses do not contain personal information, but every transaction is recorded publicly. This pseudonymity means individuals can hide behind addresses temporarily, but once an address becomes associated with a real identity—whether through an exchange, a merchant, or forensic analysis—every past and future transaction becomes traceable. Law enforcement agencies have become highly skilled at linking transactions to criminal networks. Far from offering perfect anonymity, public blockchains function like permanent financial ledgers.

Why law enforcement increasingly uses blockchains

Investigative agencies have embraced blockchain analytics because of the transparency inherent in many networks. Even sophisticated criminal operations leave digital footprints that analysts can follow across wallets, platforms, and chain hops. This level of visibility is rarely possible in traditional financial systems, where private bank ledgers remain inaccessible without legal action. While criminals may attempt to use blockchain, it is not uniquely suited for illegal activity—and in many cases, it exposes them to greater risk of detection.

Myth 4 – “Blockchain Is Completely Secure and Unhackable”

At the opposite extreme is the idea that blockchain provides perfect security. Advocates sometimes describe distributed ledgers as “tamper-proof” or “unhackable,” implying that the technology guarantees safety. This myth, while flattering, creates unrealistic expectations and can lead to poorly designed projects. Blockchain strengthens certain elements of data security, but it does not eliminate vulnerability. Many blockchain-related incidents stem from errors outside the core protocol.

Where the real attack surface sits

Blockchains themselves rarely fail due to cryptographic weaknesses. Instead, attackers target surrounding infrastructure: smart contracts with flawed logic, poorly secured wallets, exchanges with weak authentication, or governance mechanisms that concentrate control. These vulnerabilities create real risks for users and organizations. When a smart contract contains a bug, the blockchain faithfully executes the flawed code, resulting in irreversible losses. The ledger’s strength preserves both intended and unintended outcomes.

Governance, code and human error

No technology is free from human error. Blockchain magnifies the consequences of mistakes because changes are harder to reverse. The immutability that prevents tampering also prevents easy fixes. Developers must approach blockchain development with rigorous testing, audits, and formal verification. Even governance models require careful planning. Smaller networks may face risks of coordinated attacks, while decentralized systems can struggle with decision-making during crises. Understanding these limitations prevents organizations from treating blockchain as a cure-all for security.

Myth 5 – “Everything on Blockchain Is Public, So Privacy Is Dead”

Another common misunderstanding assumes that all blockchain activity is publicly visible and therefore dangerous for sensitive data. This myth stems from the nature of early public blockchains, where every transaction appears on a global ledger. However, blockchain technology now encompasses a wide range of architectures, including systems designed specifically to protect privacy and confidentiality.

Public, private and permissioned chains

Not all blockchains operate like Bitcoin. Organizations frequently deploy permissioned or consortium blockchains, where participants must be verified and access is controlled. These networks allow varying degrees of visibility so that sensitive information is accessible only to authorized parties. Public transparency is not a requirement for all blockchains; it is merely one design choice. This flexibility allows industries such as healthcare and finance to adopt blockchain without sacrificing confidentiality.

Techniques that protect sensitive data

Modern cryptographic tools enable privacy-preserving blockchain applications. Zero-knowledge proofs allow parties to verify information without revealing underlying data. Off-chain storage systems keep confidential records secure while anchoring integrity checks on-chain. Selective disclosure techniques empower individuals to share specific attributes without exposing full identities. These innovations reflect a simple truth: blockchain does not eliminate privacy—it evolves the way privacy is managed.

Myth 6 – “Blockchain Is Always Slow and Can’t Scale”

A widespread belief about blockchain is that it cannot handle large-scale operations or high transaction volumes. This assumption originally came from early public networks that prioritized decentralization over speed. Years ago, Bitcoin’s throughput hovered around single-digit transactions per second, and Ethereum often struggled during peak activity. These limitations were real, but over time they became exaggerated into a blanket narrative that “blockchain is slow,” even as technology rapidly evolved. Many modern blockchain systems now operate at speeds comparable to mainstream financial platforms, and others continue to push performance boundaries.

Early limits vs current performance

First-generation blockchains faced clear bottlenecks, but the industry responded with architectural improvements. New consensus algorithms, better networking layers, and more efficient data structures have drastically improved throughput. Enterprise-focused blockchains routinely achieve thousands of transactions per second because they operate in controlled environments where validator nodes are known and optimized. Even some public networks now offer transaction speeds suitable for real-time applications. The misconception that all blockchains share the same performance profile overlooks how diverse the ecosystem has become.

Layer-2, sidechains and enterprise architectures

Scaling solutions now exist at multiple layers. Sidechains, rollups, and state channels allow vast amounts of activity to be processed outside the main ledger, settling only essential data on-chain. This approach reduces congestion while preserving security guarantees. Layer-2 technologies have transformed blockchain performance, enabling markets, games, micropayments, and enterprise workflows to function at scale. In corporate environments, permissioned chains deliver even greater throughput because the system does not need to defend against unknown participants. The result is a landscape where scalability depends on design choices—not an inherent flaw of blockchain itself.

Myth 7 – “Blockchain Always Wastes Huge Amounts of Energy”

Environmental concerns shaped public opinion during the rise of Bitcoin mining, and for good reason: proof-of-work systems require substantial computational resources. However, this narrative quickly turned into a sweeping myth that all blockchain technology is energy-intensive. In reality, energy consumption varies dramatically depending on the consensus mechanism and network structure. Many blockchains consume no more energy than a conventional database server, and some run on infrastructure already used for other enterprise systems.

Proof of Work vs Proof of Stake and beyond

Proof-of-work relies on competitive mining, which drives energy usage upward. But it is only one model. Proof-of-stake and proof-of-authority mechanisms operate with minimal power requirements because they do not involve computational racing. As a result, most modern blockchains use these energy-efficient systems. Enterprise deployments, consortium chains, and government platforms almost universally avoid proof-of-work, opting for consensus structures that align with sustainability goals. The blockchain ecosystem has moved far beyond the model that created early environmental criticism.

How design choices change the footprint

Energy consumption is ultimately a governance decision. A blockchain designed around resource-intensive mining will consume more power, while one designed around stake-based or permissioned validation remains lightweight. Organizations adopting blockchain evaluate energy impact alongside security requirements, performance needs, and regulatory expectations. As sustainability becomes increasingly important, developers continue optimizing systems with energy-efficient designs. The idea that blockchain inherently wastes electricity is a dated assumption, not a conclusion supported by modern deployments.

Myth 8 – “Blockchain Is Only Useful for Finance”

Because blockchain rose to prominence through cryptocurrencies, many people still assume its value lies exclusively within financial services. Finance certainly remains a major domain, but industries far beyond banking and trading now use blockchains for transparency, authenticity, coordination, and automation. This broader adoption challenges the notion that blockchain is relevant only for digital money or investment platforms.

Supply chains, health records and identity

Supply chain transparency is one of the most mature blockchain applications. Retailers, logistics providers, and manufacturers use distributed ledgers to track goods from origin to destination. This approach improves traceability, reduces fraud, and allows consumers to verify product authenticity. Healthcare institutions experiment with blockchain to protect patient data, streamline clinical trials, and coordinate research without compromising privacy. Governments test blockchain-based identity systems to improve service delivery, reduce administrative friction, and provide citizens with secure digital credentials. These examples illustrate a growing landscape of real-world uses that extend far beyond financial transactions.

Where pilots are turning into production

For years, blockchain projects existed mostly as proofs of concept. Today, many quietly operate in production environments, embedded into larger technologies. Shipping consortia employ blockchains to coordinate documentation. Agribusiness companies use them to track crops and verify sustainability claims. Intellectual property platforms employ blockchain for rights management, ensuring creators receive proper attribution. While not always headline-worthy, these operational systems reflect blockchain’s maturing role as a foundational digital tool. Finance was the gateway, but it is no longer the boundary.

Myth 9 – “All Blockchains Are the Same”

A common misunderstanding treats every blockchain as identical. This myth arises because people often generalize from one well-known platform—usually Bitcoin or Ethereum—and assume the same characteristics apply everywhere. In truth, blockchain is a category that includes numerous architectures, governance structures, and performance capabilities. Using a single definition for all blockchains obscures how different they can be in practice.

Public, private, consortium and hybrid models

Blockchains fall into several structural categories. Public blockchains allow anyone to participate, offering decentralization but requiring careful design to prevent abuse. Private blockchains restrict access to one organization, providing control and efficiency. Consortium blockchains operate under shared governance, balancing trust among multiple partners. Hybrid models combine public anchoring with private data layers to achieve both transparency and confidentiality. Each type serves distinct purposes and offers unique trade-offs, which is why understanding these differences is essential when selecting a solution.

Trade-offs leaders actually need to weigh

Choosing the right blockchain framework depends on governance, risk tolerance, data sensitivity, and long-term strategy. Leaders must evaluate who participates, how decisions are made, how upgrades occur, and how disputes are resolved. Some applications prioritize decentralization, while others focus on compliance or scalability. Treating all blockchains as interchangeable leads to poor planning and disappointing outcomes. Recognizing the diversity within blockchain technology enables organizations to match the correct structure to their specific goals.

Myth 10 – “Smart Contracts Are Automatically Legal Contracts”

The term “smart contract” can be misleading. It suggests that these digital agreements are legally binding by default, when in reality they are simply programs that execute predefined conditions on a blockchain. While smart contracts enable automation and reduce the need for intermediaries, they do not inherently carry legal standing unless integrated with formal legal frameworks. This misunderstanding can create confusion in enterprises seeking to use blockchain for contractual workflows.

Code, law and the gap between them

Smart contracts automate processes, but they rarely capture the nuance of legal obligations. Code enforces strict logic, whereas legal contracts include interpretations, rights, remedies, and jurisdictional requirements. A smart contract may transfer tokens or update records, but it cannot address all contingencies that a traditional contract covers. Moreover, bugs or unintended logic can lead to outcomes that contradict the intentions of the parties involved. Understanding this gap is essential for responsible deployment.

How regulators and courts are catching up

Legal systems have begun acknowledging blockchain-based agreements, but recognition varies widely. Some jurisdictions permit digital signatures and blockchain records as evidence. Others explore regulatory sandboxes where automated agreements can be tested. However, widespread legal equivalence between smart contracts and formal contracts remains limited. Organizations must complement smart contract functionality with traditional legal documentation to ensure enforceability. The myth that smart contracts override legal systems oversimplifies a complex and evolving landscape.

Myth 11 – “Blockchain Is Beyond Regulation—or Will Be Banned Completely”

Two contradictory blockchain myths frequently appear side by side. One claims blockchain cannot be regulated, while the other predicts governments will ban it outright. Both misconceptions stem from early uncertainty about how decentralized systems fit into existing regulatory models. Over the past several years, however, regulatory frameworks have evolved significantly, and neither extreme scenario reflects current reality.

How regulators already shape the market

Regulators worldwide now oversee aspects of digital asset markets, blockchain infrastructure providers, stablecoin issuers, custodial services, and tokenized security platforms. These frameworks may vary by region but share common goals: consumer protection, anti-money-laundering enforcement, and financial stability. Blockchain-based businesses routinely operate under licensing regimes, compliance requirements, and reporting obligations. Far from being immune to regulation, the blockchain industry increasingly collaborates with regulators to establish consistent standards.

Why compliance, not avoidance, is the real trend

A complete ban on blockchain is unlikely because the technology aligns with broader digital transformation goals, such as improving transparency and reducing friction in multi-party systems. Rather than suppress blockchain, governments aim to regulate its use responsibly. Businesses adopting blockchain now treat compliance as an integrated part of system design. This shift signals a maturing ecosystem where innovation and regulation coexist. The belief that blockchain is ungovernable or destined for prohibition ignores the significant progress already made.

Myth 12 – “Blockchain Will Fix Every Business Problem”

The final myth may be the most pervasive: that blockchain is a universal solution capable of solving any operational, security, or trust-related challenge. This misconception emerged from early hype, where presenters described blockchain as transformative for everything from voting systems to food delivery. The reality is far more measured. Blockchain is powerful in certain contexts, but it is not suitable for every problem.

When blockchain makes sense—and when it doesn’t

Blockchain shines when multiple parties need shared, verifiable data without relying on a single central authority. It is valuable when auditability, provenance, or tamper-resistance are critical. However, many business challenges require faster performance, simpler workflows, or centralized oversight—areas where traditional databases excel. If trust already exists among participants, blockchain may add unnecessary complexity. Successful deployments begin with understanding the specific problem rather than trying to fit blockchain into every scenario.

Questions to ask before launching a blockchain project

Organizations evaluating blockchain should consider several key questions:

- What problem requires a shared source of truth?

- Who are the stakeholders, and do they trust one another?

- Would stronger data governance achieve the same result more efficiently?

- How will the system be maintained, upgraded, and governed?

- What regulatory considerations apply to the data and participants?

These questions help determine whether blockchain is a strategic asset or a technological distraction. Real value emerges when blockchain’s strengths match the needs of the problem—clarity, transparency, coordination—not when it is applied indiscriminately.

Moving Beyond Blockchain Myths You Should Stop Believing

What a realistic roadmap looks like for leaders

Understanding the truth behind these blockchain myths enables leaders to make informed decisions. Rather than viewing blockchain as a disruptive force that will replace existing infrastructure overnight, organizations increasingly see it as a complementary layer that enhances transparency, security, and shared governance. A practical roadmap focuses on incremental adoption: identifying specific use cases, testing assumptions through controlled pilots, and integrating blockchain where it offers measurable benefits. This steady approach yields more sustainable results than chasing sensational narratives.

Why nuance now beats maximalism

The blockchain ecosystem has matured, moving beyond simplistic narratives of either radical transformation or imminent failure. Today’s successful deployments reflect a balanced understanding of possibilities and limitations. Nuance allows organizations to recognize where blockchain fits, where it does not, and how it interacts with existing systems. The myths outlined throughout this article continue to influence public perception, but informed decision-making requires moving past exaggeration. With realistic expectations, blockchain becomes a valuable tool—neither a miracle nor a menace, but a practical technology shaping the next phase of digital infrastructure.

Final Thoughts

Blockchain continues to evolve beyond the early hype, and understanding its reality requires moving past outdated assumptions. These myths shaped public perception for years, often overshadowing the meaningful progress happening across industries. When we strip away exaggeration—both positive and negative—a clearer picture emerges.

Blockchain is neither a universal remedy nor a passing trend, but a sophisticated tool with specific strengths. Its value depends on thoughtful design, clear governance, and alignment with real-world needs. By challenging long-held misconceptions, leaders can approach blockchain with grounded expectations and make better strategic choices. The future of blockchain will be built not on myths, but on careful evaluation and practical implementation.