The era of theoretical pilots is over. As 2026 dawns, the global monetary system is no longer just digitizing; it is splitting into two distinct, competing operating systems. With China’s mBridge now processing billions in non-dollar trade and the US formally outsourcing its digital currency strategy to the private sector via the 2025 GENIUS Act, the “neutrality” of money is officially dead. At the heart of this fracture lies Digital Sovereignty in AI Governance, as states embed monetary control into algorithmic infrastructures that determine who can transact, at what cost, and under whose rules.

- Digital sovereignty is moving AI governance from “ethics talk” to enforceable levers like market access, cloud procurement, chip supply, and grid capacity.

- 2026 is a tipping point because major EU obligations begin applying, while the US rewires export controls and China hardens security-first oversight.

- The real contest is shifting from “who has the best model” to “who controls the inputs,” especially compute, data, energy, and standards.

- Firms face a new operating reality: one product, many rulebooks, and growing pressure to localize infrastructure and compliance.

- Countries without compute and energy capacity risk becoming rule-takers, even if they write ambitious AI laws.

- What comes next is likely not one global AI constitution, but competing governance blocs that partially interoperate through standards and safety testing.

Why Digital Sovereignty Has Become AI Governance?

Digital sovereignty used to be a European-sounding phrase that many executives filed under privacy and compliance. In 2026, it has become a shared global instinct, even among countries that disagree on almost everything else. The reason is simple. AI is no longer only software. It is an infrastructure race. And infrastructure is where sovereignty lives.

Three forces pushed governments toward this moment.

First, AI has expanded the definition of “critical infrastructure.” Cloud platforms, hyperscale data centers, and chip supply chains now sit in the same political category as ports, pipelines, and power plants. When a country depends on a foreign jurisdiction for its most important compute, its economic security becomes a policy variable controlled elsewhere. That is not an abstract fear. It shows up when export controls change, when cross-border data rules tighten, or when global cloud outages disrupt essential services.

Second, AI has raised the cost of dependence. Earlier waves of digital globalization allowed countries to “import innovation” at low marginal cost. With frontier AI, the marginal cost is not low. Training and running advanced models demands massive compute, specialized chips, and electricity. When those inputs are scarce, the market does what it always does. It concentrates power in a few firms and a few geographies. Governments respond the same way they respond to any concentrated strategic dependency: they regulate, subsidize, localize, and bargain.

Third, AI has multiplied the political risks of digital systems. The governance debate is no longer only about privacy. It is also about labor displacement, disinformation at scale, cyber risk, and algorithmic decision-making in sensitive areas like credit, hiring, policing, border control, and healthcare. Even governments that want rapid innovation still need a story about legitimacy. Digital sovereignty is often the story they choose because it signals control and accountability, even when the details differ.

This is why 2026 feels like an inflection year. The global AI conversation is shifting from “what should AI do” to “who gets to decide what AI is allowed to do.” The moment a government ties AI permissions to market access, cloud procurement, chip supply, or energy approvals, governance stops being a guideline and becomes an operating constraint.

Here is the practical timeline logic that is shaping planning calendars, budgets, and product roadmaps.

| Time Window | What Changes In Practice | Why It Matters For Sovereignty |

| 2024–2025 | More principles, more safety summits, and early-phase legal rollouts begin | Countries test soft coordination while building hard levers |

| 2025 | Export control frameworks shift and alliances are tested | Compute access becomes geopolitical bargaining |

| 2026 | EU obligations expand and enforcement readiness becomes real | “Comply or segment” becomes a board-level decision |

| 2026–2027 | Grid and energy politics intensify around data centers | Electricity becomes a limiting factor for national AI ambitions |

| 2028–2030 | Interoperability battles accelerate around evaluation and standards | The world risks “competing compliance regimes” with partial bridges |

The deeper point is that digital sovereignty is not one policy. It is a bundle of policies that aim to answer one question: how can a state regain agency in a digital economy that increasingly runs on AI? Different governments will answer that question differently. But the direction of travel is converging. Control over AI is being built into the infrastructure layer, not just written into law.

How The EU, US, And China Are Hardening Their AI Governance Models?

The fastest way to understand global AI governance in 2026 is to see it as three competing templates.

Europe’s template is rules-first, rights-first, and market-shaping. The United States’ template is innovation-first, security-first, and alliance-managed. China’s template is security-first, state-supervised, and stability-centered. These are generalizations, but they explain why “global AI governance” is increasingly a negotiation between systems rather than a single system.

Europe’s leverage comes from the size and regulatory coherence of its market. It is trying to turn AI into a governed product category, not a wild-west feature layer. That is why its framework is risk-based and why it invests in enforcement architecture. The key thing about the EU model is the calendar. When regulators publish a phased timeline, they create a planning horizon that companies cannot ignore. That horizon forces firms to build compliance capability, risk classification, documentation, transparency workflows, and monitoring capacity as part of product development.

In US policy, the language often centers on leadership and strategic competition. The governance posture is increasingly tied to “trusted partner” thinking, especially around chips and advanced compute. Export controls and guidance are not side issues in this model. They are governance instruments. They decide who can scale advanced AI, where it can be trained, and which ecosystems become default. That means the US approach can look less like a single AI law and more like a coordinated toolkit that includes export controls, procurement, safety institutes, and sector rules.

China’s approach is built for administrative control and security review. Its generative AI measures illustrate how AI governance can be wired into licensing-like obligations, content duties, and security assessments, especially for services seen as influencing public opinion or social mobilization. This model creates a different kind of predictability. It is not always transparent to outside observers, but it is structured around state supervision and alignment with national objectives.

One reason the three templates matter is that they encourage different corporate behaviors.

- In the EU model, firms invest in documentation, audit readiness, risk management, and product transparency.

- In the US model, firms invest in scale, security partnerships, and ecosystem alignment, while tracking export control and supply chain exposure.

- In the China model, firms invest in content control, data governance, administrative filings, and local operational structures.

This is where sovereignty becomes a global market force. A multinational AI company cannot build one “neutral” product and expect it to fit everywhere. It either builds a global baseline that satisfies the strictest regime, or it builds regional variants. The more AI becomes embedded into high-stakes services, the more likely firms are to choose variants, because local rules can be fundamentally different, not just stricter.

The competition between templates also shapes diplomacy. When governments talk about “safe and trustworthy AI,” they often agree on the words. But they disagree on who enforces them, what counts as harm, how transparency should work, and what trade-offs are acceptable between safety and innovation. These disagreements are not temporary misunderstandings. They reflect political systems, security doctrines, and economic strategies.

| Governance Template | Primary Goal | Core Enforcement Lever | Typical Corporate Response |

| EU | Protect rights and harmonize the market | Legal obligations, enforcement timelines, penalties | Compliance-by-design, audit trails, risk classification |

| US | Maintain leadership and secure strategic tech | Export controls, alliances, procurement, safety coordination | Ecosystem strategy, supply chain hardening, rapid scaling |

| China | Maintain security and social stability | Security assessment, administrative oversight, content duties | Local governance layers, filings, controlled deployment |

The real story is not that one template will “win.” The more likely outcome is coexistence, with friction. That friction will reshape where models are trained, how products launch, how startups scale, and which countries capture value.

The Infrastructure Layer: Data, Compute, Chips, Cloud, And Energy As Sovereignty Tools

If laws are the visible layer of AI governance, infrastructure is the force multiplier. In 2026, the most consequential AI decisions are increasingly being made in five places: data rules, compute availability, chip flows, cloud procurement, and electricity policy. These levers are not new. What is new is that AI ties them together into one system.

Data sovereignty is the foundation. Training data, fine-tuning data, logs, feedback loops, and evaluation datasets all move across borders in the normal course of modern AI development. When governments restrict that movement, or require local storage, they change the economics of AI. Large firms can build regional data centers and compliance stacks. Smaller firms struggle. And the “default” becomes regional products that learn from regional data, which can widen performance gaps and create uneven safety outcomes.

This is where data localization trends matter. When dozens of countries adopt localization measures, the result is not a single barrier. It is a layered maze. Firms must decide what data stays local, what can flow, what can be used for training, what must be deleted, and what needs consent. The compliance burden becomes a structural advantage for incumbents.

Compute sovereignty is the second layer. Countries are learning that AI leadership without compute capacity is fragile. That is why governments are funding compute pools, subsidizing cloud credits, and building public-private partnerships to democratize access to GPUs for startups and researchers. The logic is partly economic and partly political. If domestic innovators cannot access compute at reasonable cost, the country’s policy ambitions become hollow. It becomes dependent on foreign platforms not only for technology, but for the pace of innovation.

Chip sovereignty is the third layer, and it is the most overtly geopolitical. Export controls, licensing rules, and supply chain restrictions turn chip access into a strategic throttle. Even small shifts in thresholds or permitted shipments can alter which actors can train advanced models at scale. For businesses, this creates a new kind of risk. It is not only about price volatility. It is about sudden policy reclassification that can disrupt product plans and investment cycles.

Cloud sovereignty is the fourth layer. Governments increasingly treat cloud procurement as governance. If public agencies, critical infrastructure providers, and regulated sectors are required to use “trusted” or “sovereign” cloud arrangements, cloud providers must redesign where data is stored, how encryption keys are managed, how access is audited, and which legal jurisdictions can touch sensitive workloads. This changes the competitive landscape. It also pushes cloud firms toward local partnerships, local subsidiaries, and region-specific operational controls.

Energy sovereignty is the fifth layer, and it may become the dominant constraint faster than many policymakers expected. AI does not only consume compute. It consumes electricity and water for cooling, and it competes with households and industry on the same grid. As a result, AI governance is now colliding with energy politics.

Recent US reporting highlights how data center growth is already becoming a political flashpoint, with proposals to shift more power system costs onto large data center operators and to accelerate new generation capacity. This matters because it reveals a new enforcement route that is not a tech law at all. It is an infrastructure rule: no power, no scaling. If a region requires self-supply, interruptible service, or long-term capacity contracts for large loads, it is effectively regulating AI growth through the grid.

The IEA’s projections add scale to this story. When global data center electricity demand is expected to more than double by 2030, and when AI-optimized data centers are projected to multiply their demand even faster, electricity becomes a strategic input, not a utility line item. That creates incentives for states to prioritize data centers in industrial planning, or to restrict them for affordability and reliability. Either choice is governance.

| Sovereignty Lever | What Governments Are Doing | The AI Governance Effect |

| Data rules | Localization, consent rules, cross-border restrictions | Splits training and operations into regional pipelines |

| Compute | Public compute pools, subsidized access, national AI missions | Reduces dependency on foreign clouds and labs |

| Chips | Export controls and supply chain security | Determines who can scale frontier systems |

| Cloud procurement | “Trusted cloud” requirements and public sector standards | Forces compliance via purchasing power |

| Energy | Load rules, interconnection reform, capacity market changes | Sets a hard ceiling on AI scaling speed |

The combined effect is a shift from “governance as policy” to “governance as constraints.” It also explains why sovereignty debates are intensifying. Whoever controls the constraints controls the playing field.

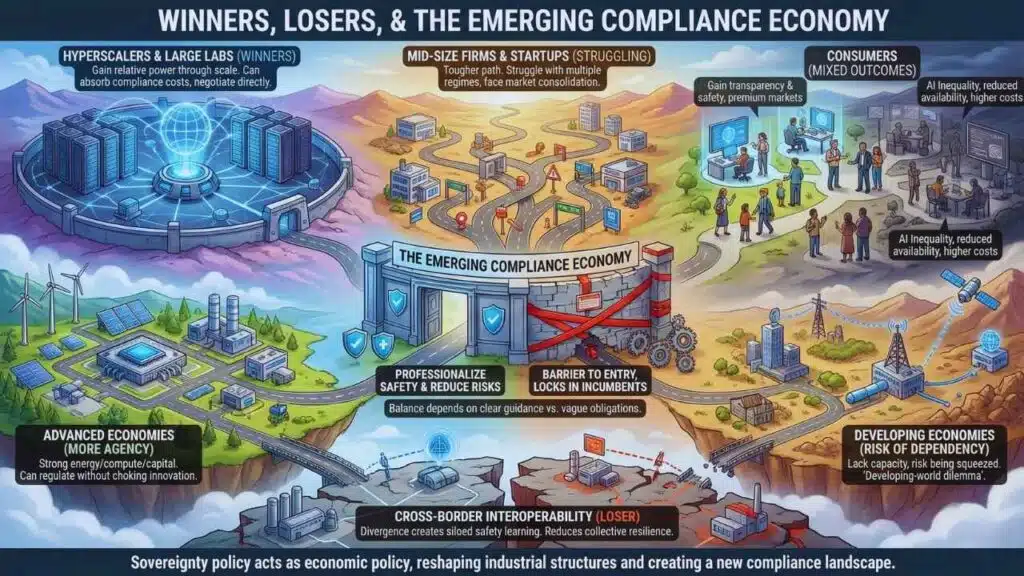

Winners, Losers, And The Emerging Compliance Economy

Digital sovereignty produces winners and losers, but not in a simple “countries vs companies” way. The more accurate picture is a reordering of advantages across different kinds of states and different kinds of firms.

Large AI labs and hyperscalers often gain relative power in a fragmented environment because they can absorb fixed compliance costs. They can hire legal teams, build safety evaluation units, localize infrastructure, and run parallel product variants. They can also negotiate directly with governments because they control scarce inputs like compute and specialized talent. In sovereignty-driven governance, bargaining power matters.

Mid-size software firms and startups face a tougher path. Many can comply with one regime, but struggle with five at once. They must decide where to launch, where to invest in localization, and whether to partner with larger clouds or labs. This is where sovereignty can unintentionally consolidate markets. When compliance becomes expensive, the market rewards scale.

Consumers gain in some ways and lose in others. Strong governance can improve transparency, reduce harmful deployments, and create clearer recourse. But fragmentation can also reduce product availability, slow feature rollouts, and increase costs. It can produce “AI inequality,” where premium markets get safer and more capable tools first, while others receive limited versions or delayed access.

Governments face their own winner-loser split. Countries with strong energy capacity, advanced chip access, and deep capital markets have more degrees of freedom. They can regulate without choking domestic innovation, because they can substitute with local capacity. Countries without those inputs risk being squeezed from both sides. They may adopt rules, but lack the enforcement capacity. Or they may avoid strong rules to attract investment, and become dumping grounds for riskier deployments.

The developing-world dilemma is especially important. Global statements often promise that AI should benefit all, but the infrastructure reality can deliver the opposite: concentration and dependency. If data localization spreads without corresponding local compute and skills investment, many countries may end up paying more for compliant services while capturing less economic value.

This is why we should treat sovereignty policy as an economic policy. It affects industrial structure. It shapes where jobs form, where R&D clusters emerge, and which firms become default providers. It also creates a new “compliance economy,” where standards consultants, auditors, safety evaluators, and governance tooling firms become essential parts of AI supply chains.

The compliance economy has two faces.

- It can professionalize AI safety and reduce irresponsible deployments.

- It can also become a barrier to entry that locks in incumbents.

The balance depends on implementation. If regulators provide clear guidance, harmonized standards, and predictable enforcement, compliance can become manageable. If they create vague obligations and inconsistent enforcement, compliance becomes a tax on innovation that only the largest players can pay.

| Stakeholder | Likely Gains | Likely Costs |

| Hyperscalers and large labs | Scale advantage, bargaining power, infrastructure leverage | Higher scrutiny, political risk, costly localization |

| Startups and mid-size firms | Opportunities in governance tooling and niche markets | Higher fixed compliance costs, slower expansion |

| Consumers | Better transparency and accountability in some markets | Feature fragmentation, higher prices, uneven access |

| Advanced economies with energy and compute | More policy agency, stronger domestic ecosystems | Domestic political backlash over energy and affordability |

| Developing economies without capacity | Potential investment and adoption gains | Risk of dependency and weak negotiating power |

The most overlooked “loser” category may be cross-border interoperability itself. When rules diverge, safety learning can become siloed. Incidents that should inform global best practices may remain regional. That reduces collective resilience.

What Happens Next In 2026–2030 And How To Watch The Real Signals

Predictions should be stated carefully because policy can change quickly. Still, there are clear signposts for what comes next, and they reveal where global AI governance is heading.

The first signal to watch is enforcement readiness in Europe as major obligations begin applying. Deadlines matter less than enforcement capacity. The key question is whether enforcement becomes consistent enough to shape global corporate behavior, or inconsistent enough to encourage selective compliance and legal arbitrage. If enforcement is predictable, many firms will adopt EU-grade governance processes globally. If enforcement is unpredictable, firms will segment products and manage risk by geography.

The second signal is the US export control “replacement rule” direction and how it is coordinated with allies. The US has already shown it is willing to change approach when it believes earlier frameworks would harm innovation or alliances. The replacement structure will likely clarify which countries are considered trusted partners, how controls apply to overseas chips, and how enforcement is handled. The outcome will shape global compute geography because it affects where advanced chips can flow at scale.

The third signal is how energy policy evolves into AI policy. The political logic is becoming clear: ratepayers do not want to subsidize hyperscale growth, and grid operators do not want reliability crises. That creates pressure for new rules around interconnections, capacity payments, curtailment obligations, and self-supply requirements for large loads. This is governance by infrastructure. It can slow AI scaling in certain regions and accelerate it in others, depending on how fast new generation and transmission are built.

The fourth signal is the rise of “evaluation diplomacy.” Instead of trying to negotiate one global AI law, governments may increasingly coordinate around safety testing methods, incident reporting formats, and shared scientific research on frontier risks. Networks of safety institutes and international guiding principles aim to reduce duplication and raise a common floor for safety practices. The risk is that evaluation becomes another sovereignty battlefield, with incompatible testing regimes and national security secrecy.

The fifth signal is what middle powers do with compute missions, procurement standards, and national model strategies. Some will try to build sovereign capacity through public-private compute pools and domestic foundational models. Others will focus on governance that attracts trusted investment, such as clearer procurement rules and transparent regulatory sandboxes. The success cases will likely be countries that align three things at once: compute access, data governance, and energy planning.

So what should readers and decision-makers watch in practice?

- Whether major AI firms announce regional product splits and “EU-first” governance builds.

- Whether new chip policy frameworks emphasize trusted partners and scalable compliance pathways.

- Whether grid operators and regulators begin requiring large-load self-supply or interruptible service as a norm.

- Whether international safety networks produce shared evaluation protocols that multiple governments adopt.

- Whether middle powers move from ambition to capacity by funding compute, talent, and datasets.

The long-term consequence is a world of partial interoperability. You will still see shared language about safe, secure, and trustworthy AI. You will also see competing rulebooks enforced through chips, cloud contracts, and grid approvals. In that environment, digital sovereignty in AI governance is not only a policy trend. It is the organizing principle of the AI decade.

If there is a hopeful interpretation, it is this: sovereignty does not have to mean isolation. It can mean building local capacity while still participating in global safety cooperation. The best-case outcome is “common floors with local ceilings,” where countries agree on baseline safety and rights protections, while keeping room for different social choices. The worst-case outcome is hardened blocs with minimal trust, where AI becomes another arena of economic coercion.

2026 is the year that will reveal which path is becoming dominant.