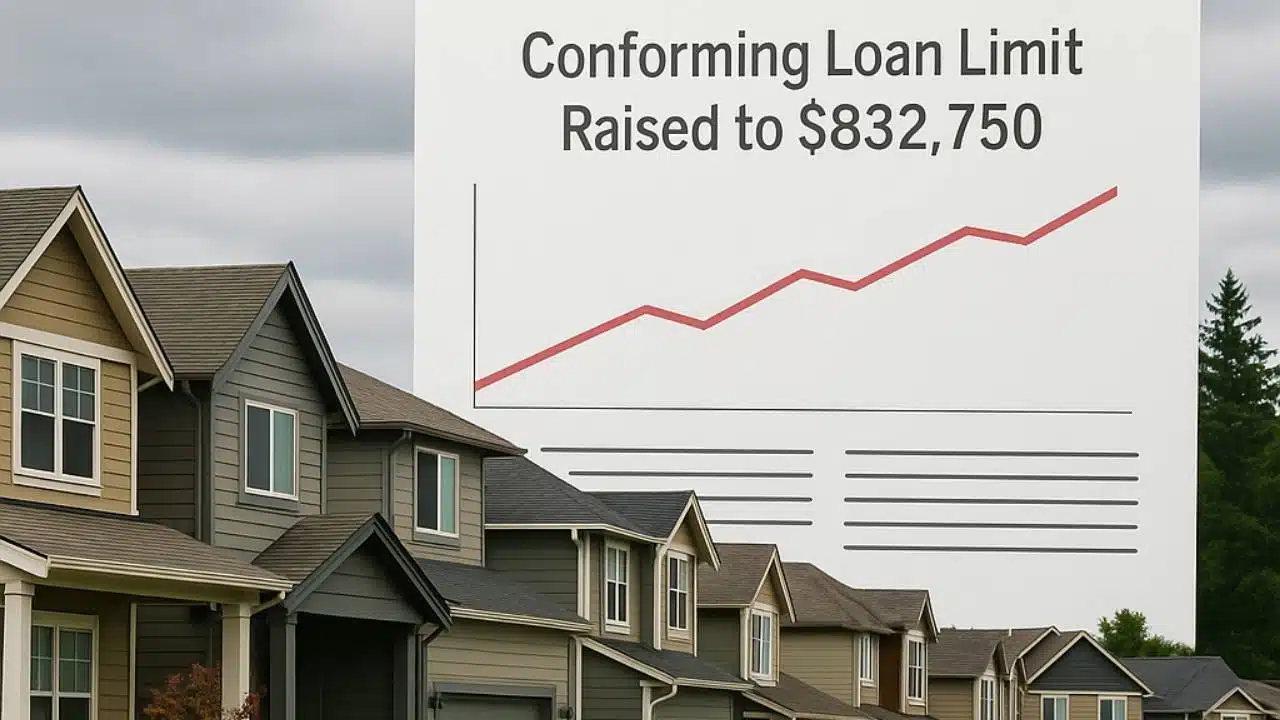

The Federal Housing Finance Agency (FHFA) has announced a significant update for homebuyers and lenders: beginning next year, the maximum size of most single-family mortgage loans that the government can guarantee will increase to $832,750. This new cap represents a 3.3% rise from the 2025 limit and reflects the continuing, although slower, rise in U.S. home prices across the country. The adjustment aims to ensure that conforming loans remain accessible to buyers in an environment where home values have been increasing steadily, even amid a broader housing market slowdown.

Conforming loans are mortgages that meet the guidelines set by the FHFA and are eligible to be bought or guaranteed by Fannie Mae and Freddie Mac, the two major government-sponsored enterprises that purchase loans from lenders. When they acquire these loans, they provide a guarantee to investors, reducing risk for lenders and helping stabilize the mortgage market. These loans often come with lower interest rates, simpler approval processes, and more predictable lending rules than jumbo loans, which exceed conforming loan limits. By raising the cap each year, the FHFA works to keep these benefits available to as many borrowers as possible in a changing real estate landscape.

The decision to raise the limit is closely tied to home-price trends. According to the agency’s House Price Index, U.S. home prices rose 3.3% from the July–September period of the previous year. While the pace of growth has slowed compared to past peaks, prices have continued to move upward. This increase, even if modest, means many homes now cost more than they did in previous years, so the loan limits must rise to prevent ordinary buyers from being pushed into more stringent jumbo-loan territory.

Although prices have been rising, the broader housing market has been experiencing a prolonged slump. Since 2022, home sales have fallen sharply due to the steep climb in mortgage rates from historically low levels reached during the pandemic. Last year, sales of previously occupied homes dropped to their lowest point in nearly three decades, a dramatic decline that highlighted the strain on affordability. Rising borrowing costs kept many potential buyers on the sidelines, while homeowners with ultra-low interest rates were reluctant to sell and take on new, higher-rate mortgages.

Throughout the first ten months of 2025, the market has continued to show weakness. Sales have been essentially flat compared to the same period in the previous year. However, some improvement emerged in the fall as mortgage rates receded from their earlier highs, dropping to their lowest levels in more than a year. This decline provided some relief for buyers, leading to a small uptick in purchasing activity — though not enough to fully revive the sluggish market.

The new national conforming loan limit of $832,750 applies to most counties across the United States, but there are exceptions for areas where home prices are significantly higher than the national average. In certain high-cost regions — such as parts of California, New York, and other metropolitan markets — the FHFA allows higher limits to ensure that buyers can still access conforming financing despite the typically steep property values in those areas. In counties where the median home value is more than double the national conforming limit, the ceiling for a single-family home loan rises accordingly. For example, beginning in 2026, the limit in high-priced counties, including Los Angeles County and New York County, will increase to $1,249,125, offering borrowers in those markets more flexibility in securing government-backed financing for properties that would otherwise require jumbo loans.

This annual adjustment helps prevent a disconnect between mortgage financing rules and real-world housing conditions. As prices grow — even at slower rates — loan limits must adjust to avoid excluding buyers from mainstream mortgage products. The new 2026 limits help to ensure that conforming loans remain a viable option for middle-income and upper-middle-income households who face higher home prices but still rely on traditional financing structures. It also helps maintain stability in the mortgage market, allowing lenders to continue offering competitive rates and terms as the agencies provide liquidity through their loan-purchase programs.

Overall, the FHFA’s decision reflects both the resilience and the challenges within the housing market. Prices continue their gradual rise due to limited inventory and high demand, yet sales remain weak because affordability constraints persist. The increase in the conforming loan limit aims to balance these pressures by giving buyers broader access to government-backed loans, particularly at a time when mortgage rates, though lower than their recent peaks, remain elevated compared to historic lows. As 2026 approaches, the new limits will shape both borrowing options and lending practices, influencing how buyers navigate a market that is still adjusting to the post-pandemic financial landscape.