In 2026, the era of “free banking” isn’t enough. The best digital banks don’t just waive fees—they actively pay you to use them. As inflation stabilizes but remains a concern for budget-conscious households, a new wave of “hybrid” neobanks has emerged. These platforms have moved beyond simple checking accounts to offer high-yield rewards traditionally reserved for elite credit cards. From earning stablecoins on your coffee runs to getting 6% back at your favorite sneaker store, the landscape of debit card rewards has evolved drastically.

Whether you are a travel nomad, a crypto-native user, or just someone looking to squeeze extra value out of their grocery budget, there is a neobank designed for your spending habits.

Below, Review the 7 best neobanks for cashback rewards in 2026, analyzing their earning potential, hidden caps, and ideal user profiles.

Top Neobank Rewards at a Glance

| Neobank | Best For | Core Reward Offer | Monthly Fee |

| 1. Upgrade | Overall Cash Value | Unlimited 1% + 2% on common expenses | $0 |

| 2. Revolut | Travelers | Up to 10% on stays; tiered card cashback | $0 – $55 |

| 3. SoFi | All-in-One | Points redeemable for cash/crypto + high APY | $0 |

| 4. Bleap | Web3 / Crypto | Flat 2% cashback in USDC | $0 |

| 5. Monzo | Budgeters | Rotating category cashback (up to 5%) | $0 – $15 |

| 6. Varo | Brand Shoppers | Up to 6% at partner brands (Nike, McD’s) | $0 |

| 7. Current | Gen Z / Gig Workers | Up to 7x points at participating merchants | $0 |

7 Best Neobanks for Cashback Rewards

Fine print to separate marketing hype from the actual money in your pocket, prioritizing “net value” over flashy but impossible-to-reach bonuses. The 2026 landscape is more diverse than ever, ranging from crypto-hybrid cards offering instant stablecoin payouts to established giants aggressively competing for your daily grocery spend. Whether you are a frequent traveler looking to offset flight costs or a budgeter wanting steady returns on utility bills, there is now a debit card engineered specifically for your financial lifestyle. Our rankings factor in monthly fees, spending caps, and redemption ease to ensure you truly come out ahead. Here is the definitive breakdown of the top contenders fighting for your deposits this year.

1. Upgrade Rewards Checking (Best for Unlimited 2% Cashback)

The “Set It and Forget It” Champion

Upgrade continues to dominate the US market in 2026 by offering a debit card that rivals entry-level credit cards. Unlike competitors that force you to activate rotating categories, Upgrade’s structure is refreshingly simple.

The Rewards Structure

- 2% Cashback: Earned on common everyday expenses, including convenience stores, drugstores, gas stations, restaurants, and monthly subscriptions (utilities, phone, streaming).

- 1% Cashback: Earned on all other debit card charges.

- The Catch: The 2% rate is capped at $500 in earned rewards per year. Once you hit that cap, those categories earn 1% for the remainder of the year.

Pros:

- No monthly fees or minimum balance requirements.

- The “common expenses” category covers the bulk of most households’ spending.

- Rewards are credited as cash, not obscure points.

Cons:

- To unlock the full 2% rate, you must maintain an active Rewards Checking account with direct deposit (usually $1,000/month minimum).

- The $500 cap on the 2% tier limits high spenders.

Ideal For: Users who want credit-card-like rewards without the risk of accumulating debt.

2. Revolut (Best for Travelers & Tiered Rewards)

The Global Nomad’s Wallet

Revolut has solidified its position as the go-to banking app for international travelers. In 2026, their “Ultra” and “Metal” plans offer some of the most aggressive cashback rates for users who spend globally.

The Rewards Structure

- Stays & Travel: Up to 10% instant cashback when booking accommodation through the Revolut Stays feature.

- Pro Accounts: Freelancers using Revolut Pro earn up to 1.2% cashback on all business spending.

- Card Spend: Metal and Ultra users earn cashback on card spend (variable rates depending on region, often up to 1% outside of Europe).

Pros:

- Massive value for frequent travelers (the 10% on hotels beats almost any travel credit card).

- includes built-in travel insurance and airport lounge access on higher tiers.

- Supports spending in 30+ currencies with excellent exchange rates.

Cons:

- The best rewards are locked behind monthly subscriptions (Metal is ~$17/mo; Ultra is ~$55/mo).

- Standard (free) accounts have very limited cashback potential.

Ideal For: Frequent flyers and freelancers who can offset the monthly fee with travel savings.

3. SoFi Checking & Savings (Best All-in-One Ecosystem)

The Financial Powerhouse

SoFi isn’t just a neobank; it’s a full-service financial ecosystem. While their direct debit cashback is lower than Upgrade’s, the total value proposition—including high-yield savings (APY) and sign-up bonuses—makes it a top contender in 2026.

The Rewards Structure

- SoFi Rewards Points: You earn points for various activities, such as logging in, monitoring your credit score, and spending on the debit card (offers vary by user profile).

- Redemption: Points can be redeemed at a rate of 1 cent per point into your checking account, towards a loan, or into a SoFi Invest account (crypto/stocks).

- Local Offers: Earn up to 15% cash back at local restaurants and shops when you pay with your SoFi card (requires activation in-app).

Pros:

- Industry-leading APY (often 3.50% – 4.50%) on savings balances with direct deposit.

- Seamless integration between spending, saving, and investing.

- Frequent “boosts” and sign-up bonuses ($50–$300).

Cons:

- Requires direct deposit to unlock the highest APY and overdraft coverage.

- The points system is more complex than a simple “cash back” auto-deposit.

Ideal For: High earners who want a primary bank that handles savings, investing, and spending in one dashboard.

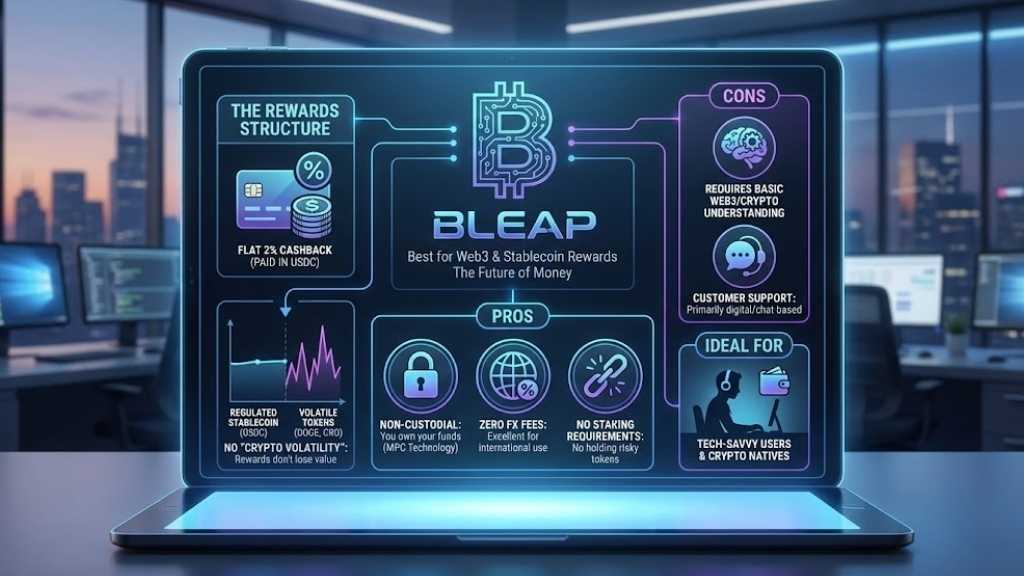

4. Bleap (Best for Web3 & Stablecoin Rewards)

The Future of Money

Bleap has emerged as the breakout star of 2026 for the crypto-curious demographic. It is a “hybrid” neobank that bridges the gap between a self-custody wallet and a Mastercard debit card.

The Rewards Structure

- Flat 2% Cashback: You earn 2% on all purchases, paid out in USDC (USD Coin).

- No “Crypto Volatility”: Unlike older crypto cards that paid rewards in volatile tokens like DOGE or CRO, Bleap pays in a regulated stablecoin, meaning your rewards don’t lose value if the market crashes.

Pros:

- Non-Custodial: You own your funds (MPC technology) until the moment you spend.

- Zero foreign transaction (FX) fees, making it excellent for international use.

- No staking requirements (you don’t need to hold $4,000 of a risky token to get the 2% rate).

Cons:

- Requires a basic understanding of Web3/Crypto wallets.

- Customer support is primarily digital/chat-based.

Ideal For: Tech-savvy users and crypto natives who want a “de-banked” experience with high rewards.

5. Monzo (Best for Rotating Perks & Budgeting)

The Budgeter’s Best Friend

Originally a UK giant, Monzo has successfully cracked the US market with a focus on intense budgeting features and flexible rewards. Their tiered plans allow users to choose their own “cashback destiny.”

The Rewards Structure

- Choice of Categories: Depending on your plan (Monzo Perks or Max), you can select up to 5 categories (e.g., Supermarkets, Transport, Dining) to earn varying cashback rates.

- Global Offers: Occasional high-value offers (e.g., 5% at specific grocery chains) appear in the app feed.

Pros:

- Incredible app interface with “Pots” for separating bill money from spending money.

- No foreign transaction fees on any plan.

- Cashback is paid instantly or monthly into a dedicated Pot.

Cons:

- The free plan has very limited cashback features compared to the paid tiers.

- US and UK feature sets still differ slightly.

Ideal For: Users who love categorizing their expenses and want rewards tailored to their specific spending habits (e.g., commuters or foodies).

6. Varo Bank (Best for Brand Partnerships)

The Strategic Shopper’s Choice

Varo holds a unique spot as the first consumer fintech to get a full national bank charter. Their cashback program is distinct because it relies on high-yield partnerships with massive brands rather than a flat rate on all spend.

The Rewards Structure

- Varo Cashback Perks: Earn up to 6% cashback when you shop at participating brands using your Varo Debit or Varo Believe card.

- Partners: Past and current partners have included giants like Nike, McDonald’s, Shake Shack, and Zara.

- Auto-Redemption: Cashback is deposited into your Varo Bank Account once you reach $5 in earnings.

Pros:

- Extremely high rates (6%) if you shop at the partnered brands.

- Works with the credit-building “Believe” card, helping you fix credit while earning.

- No monthly fees.

Cons:

- If you don’t shop at the specific partner brands, you earn $0.

- Requires activating offers in the app before shopping.

Ideal For: Brand-loyal shoppers who frequent major retail chains and fast food franchises.

7. Current (Best for Points Accumulation)

The Gamified Banking Experience

Current targets the Gen Z and gig economy sector with a “points-heavy” system. If you enjoy gamification—watching a points balance grow and “cashing out” for rewards—Current offers high earning potential.

The Rewards Structure

- Points Multipliers: Earn up to 7x points per dollar at participating merchants (over 14,000 locations).

- Redemption: Points are redeemable for cash directly into your account or for goods in their shop.

- Gas Station Perks: Often features specific point multipliers for fuel, making it a favorite for rideshare drivers.

Pros:

- Get paid up to 2 days early with direct deposit.

- Excellent toolset for parents (teen banking) and gig workers.

- High potential return if you maximize the multiplier locations.

Cons:

- Points value can be harder to calculate mentally than straight “2% cash.”

- Slightly more cluttered app interface due to the gamification elements.

Ideal For: Younger users, students, and gig workers who drive frequently.

How to Choose the Right Neobank Reward Account

Choosing a neobank in 2026 isn’t just about the highest percentage number. Here is the “math” you need to do before signing up.

1. Calculate the “Net” Reward

If a bank offers 2% cashback but charges a $10 monthly fee, you need to spend $500 per month just to break even.

- Formula: (Monthly Spend x Reward Rate) – Monthly Fee = Real Value

- Tip: If you spend less than $1,000/month on a card, stick to Upgrade or Varo (no fee options).

2. Check the “MCC” Exclusions

“MCC” stands for Merchant Category Code. Many banks exclude codes for “Utilities,” “Insurance,” or “Rent” from earning cashback.

- Upgrade is rare because it explicitly includes utilities and phone bills in its 2% category.

- Bleap and crypto cards often have fewer exclusions but strictly block “financial services” (like paying off a credit card).

3. Crypto vs. Fiat Redemption

Do you want $50 cash to buy groceries, or $50 in Bitcoin that might become $100 (or $20) next year?

- Risk-Averse: Choose Upgrade or Varo.

- Growth-Oriented: Choose Bleap (Stablecoin yield) or SoFi (Invest rewards).

Neobank Debit vs. Credit Cards: The Reality Check

Why choose a neobank debit card when the Chase Sapphire or Amex Gold exists?

- Debt Avoidance: The average American credit card debt is rising. Debit rewards allow you to earn without the psychological trap of “spend now, pay later.”

- No Hard Pull: Opening a neobank account rarely affects your credit score (no hard inquiry).

- Accessibility: Neobanks like Chime, Varo, and Current often accept users with lower ChexSystems scores who might be rejected by traditional banks.

Expert Note: “In 2026, the gap has narrowed. While premium credit cards still rule for business class flights, neobank debit cards now effectively compete with ‘Tier 2’ cash back credit cards.”

Final Thoughts

The banking landscape of 2026 proves that loyalty to traditional institutions is costing you money. With neobanks now offering competitive cashback rates on debit spending, your checking account should be an active income stream, not just a digital storage vault. The “best” account isn’t necessarily the one with the highest headline rate, but the one that aligns with your actual spending habits—whether that’s travel, groceries, or crypto accumulation.

Don’t let the perceived friction of switching hold you back; modern portability rules and instant digital issuance make moving funds easier than ever. Take a hard look at your last month’s bank statement. If you see monthly fees instead of earnings, it’s time to move on. Select the neobank that fits your lifestyle, open an account in minutes, and start getting paid for every swipe you make this year.