Ever feel totally confused when you hear terms like “digital dollars” or see new money apps popping up? You are definitely not alone. Money is changing incredibly fast right now. Terms like digital currency, legal tender, and blockchain can sound completely overwhelming. This is especially true if you just want to know how it all affects your own bank account. Here is a surprising fact for you. Over 130 countries are currently studying or testing something called a Central Bank Digital Currency, or CBDC. That means the future of money worldwide is going digital, even if the US is taking its own unique path.

In this post, we are going to break down exactly what is a CBDC and why should you care. We will keep the words simple, skip the heavy jargon, and look at the real facts. Grab a cup of coffee, and let’s go through it together. I will show you everything you need to know about how these changes might affect your wallet!

What Is a Central Bank Digital Currency (CBDC)?

A Central Bank Digital Currency, or CBDC, is money made by a country’s central bank in digital form. It stands apart from other digital coins and brings its own twist to how we use cash today.

Definition of CBDC

A Central Bank Digital Currency, or CBDC, is a type of electronic money. The main authority for this money is a country’s central bank, like the US Federal Reserve. Unlike the paper cash you keep in your physical pocket, this currency lives entirely online. People and businesses can use it just like paper bills, but they do it through phones or computers.

You might wonder how this is different from using digital payment methods like PayPal or Venmo. Apps like Venmo simply move around commercial bank money, which is tied to your regular checking account.

A CBDC is a direct digital liability of the government itself. Only the government produces and controls them as legal tender. This makes them very different from Bitcoin or other cryptocurrencies, which are private and often unregulated.

A CBDC may sound high-tech, but at its core, it is simply government-backed digital money.

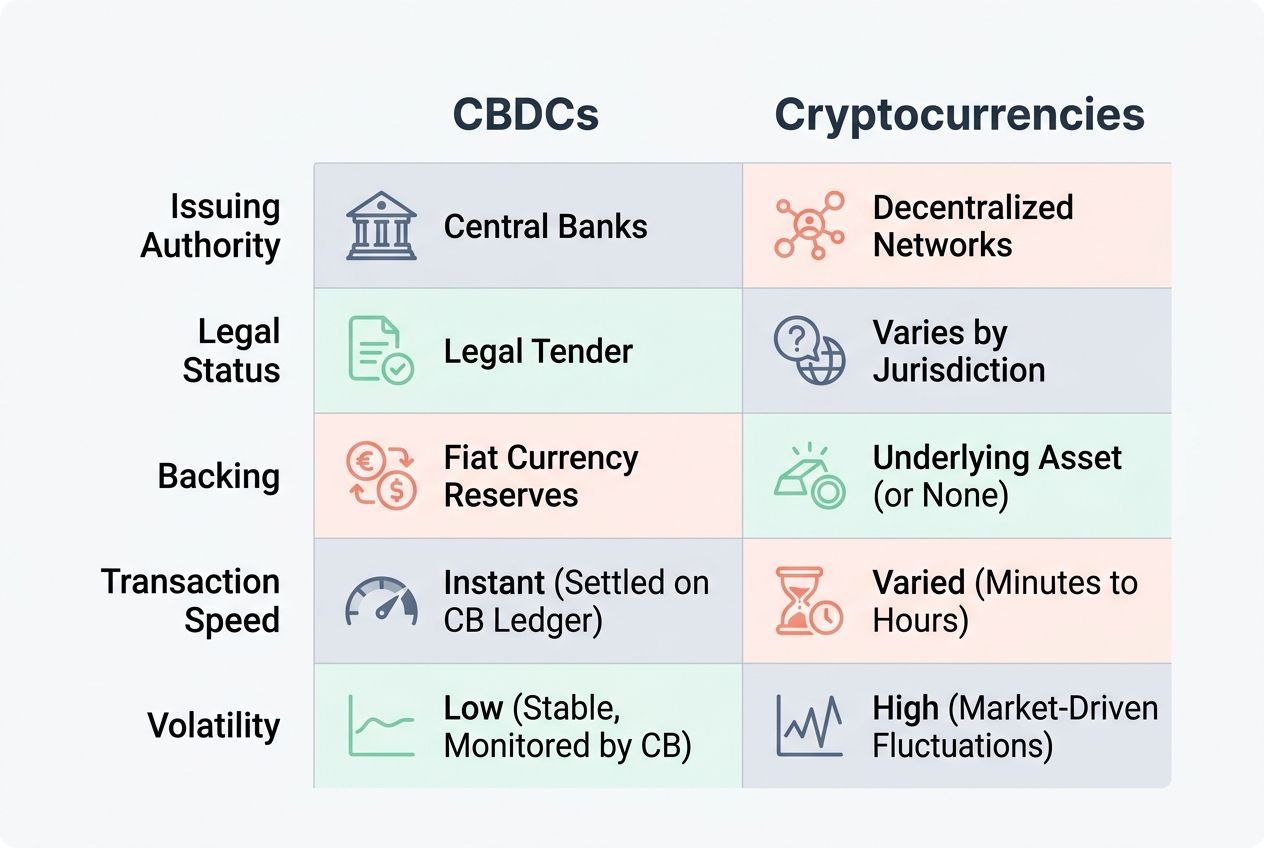

How CBDCs differ from cryptocurrencies

Understanding the gap between CBDCs and cryptocurrencies can save you a lot of confusion. Here is exactly how they stack up side by side:

| Feature | CBDCs | Cryptocurrencies |

|---|---|---|

| Issuing Authority | Issued and managed by a country’s central bank, like the Federal Reserve or the People’s Bank of China | Created by individuals, companies, or communities; examples include Bitcoin (2009, Satoshi Nakamoto) and Ethereum (2015, Vitalik Buterin) |

| Legal Status | Recognized as legal tender, the same as traditional cash | Rarely legal tender; accepted only by choice, sometimes restricted or banned |

| Backing | Backed by government reserves, usually pegged 1:1 to the national currency | Value based on market demand; no backing from governments |

| Transaction Speed | Designed for quick, everyday transactions; aims for instant settlement | Can face delays; Bitcoin, for example, averages 10 minutes per block |

| Privacy | Transactions traced by central banks; full privacy not guaranteed | Varying privacy; some like Monero focus on anonymity, most are pseudo-anonymous |

| Volatility | Stable, reflects government currency value; $1 CBDC equals $1 cash | Highly volatile; prices can swing wildly in hours, as seen during the 2021 Bitcoin rally and crash |

| Technology | Often uses permissioned blockchain or centralized ledgers | Runs on public blockchains, open to anyone for validation and participation |

| Purpose | Built for mass use, government payments, and social welfare distribution | Used for investing, speculation, sometimes as a store of value or for cross-border transfers |

| Examples | Digital yuan (China, 2020 pilot), eNaira (Nigeria, 2021 launch) | Bitcoin (BTC), Ethereum (ETH), Dogecoin (DOGE) |

Next, let’s walk through a quick history of these digital currencies.

A Brief History of CBDCs

Banks did not always think about digital money, but new tech made them curious. Soon, some countries started to test these digital coins in real life.

Origins of the concept

Central Bank Digital Currency is not a brand-new idea. Way back in the 1980s, a computer scientist named David Chaum shared early ideas about digital cash and financial privacy.

Fast forward to 2008, and the creation of Bitcoin introduced blockchain technology to the masses. This changed digital finance forever.

The People’s Bank of China took notice very early. They began working on their digital yuan version back in 2014. Other central banks watched closely as Sweden tested its e-krona pilot around 2020.

“Digital currencies are like electronic cash. They are easy to use, but they are backed by your country’s trusted bank.”

CBDCs grew from years of exploring safe digital payments and modern legal tender. Governments wanted money that worked as fast as a text message but stayed secure for everyone. With financial systems becoming more global each year, these conversations kept picking up steam across the world.

Early adoption and pilot programs

Some countries moved fast to test their own Central Bank Digital Currency. These pilot programs helped them learn exactly how digital money works in real life.

- Sweden started its e-krona pilot in 2020 to test digital payments alongside cash.

- China launched the Digital Yuan trial in 2019, allowing people to pay via phones for transit and shopping.

- The Bahamas rolled out the Sand Dollar in 2020, making it one of the first fully operational CBDCs.

- Nigeria began using the eNaira in 2021 to help unbanked citizens pay bills easily.

- Jamaica successfully launched its JAM-DEX digital currency in 2022 to provide legal tender to everyone.

These pilots showed what works well and what needs fixing before a global rollout.

Key Characteristics of CBDCs

CBDCs act much like digital cash, but with some high-tech twists. They could change the way we pay for things or save money, making old habits feel a bit outdated.

Digital nature and accessibility

You can use a CBDC on your phone, computer, or tablet. It is money in pure electronic form, not physical paper you keep in a wallet. This digital currency moves rapidly across the internet and modern payment systems.

Anyone with a basic smartphone and internet access can join this new type of financial system. This setup helps reach people who live far from physical bank branches or do not have bank accounts at all. Even small everyday payments get handled quickly and safely using this technology.

Backed by central banks

CBDCs get their true power from the support of central banks. This backing makes them official money, just like traditional coins and paper bills. Each digital euro or digital yen is tied directly to a real one in that country’s financial system. Therefore, it holds its exact value as legal tender.

Most countries rely on their central banks to control these digital currencies. They help keep the economy stable during massive changes in global payment systems.

You can trust that this electronic money is safe because it comes straight from a national bank and follows strict monetary policy rules.

Use in daily transactions

You could simply tap your phone or scan a QR code to pay with a CBDC. Buying groceries, paying utility bills, or sending money to friends happens instantly with digital currency. Shop owners can accept these payments right at the checkout counter, just like they do with cash or debit cards.

With CBDCs backed by the central bank, everyone gets equal access. You do not need a fancy credit card or even a traditional bank account to buy what you need.

CBDCs have the potential to nearly eliminate the 1.5% to 3.5% credit card processing fees that burden small businesses today.

Kids, parents, and grandparents all could use digital currency for everyday needs. People have used CBDC for bus fares and school lunches already, showing how easy it can be to fit digital finance into normal daily life.

Benefits of CBDCs

CBDCs open doors to better ways of handling money. They bring fresh changes that could reshape how we live and spend each day.

Enhanced financial inclusion

People without bank accounts often struggle to save money, pay bills, or safely receive their wages. A Central Bank Digital Currency offers a direct solution to this problem. It provides digital money straight from the central bank through a simple phone app or a smart card.

Even folks living in remote rural areas or small towns can easily join the mainstream financial system. According to the World Bank, roughly 1.4 billion adults worldwide had no access to regular banking services in 2022. By using CBDCs as legal tender, more people can send and receive electronic money safely.

Local stores and farmers’ markets can accept these digital payments just like physical cash. No expensive smartphone is required, just safe and fair access for the people who need it most.

Increased payment efficiency

CBDCs move money as fast as lightning. A digital payment backed by a central bank means you can send or receive funds within seconds.

Physical cash and paper checks take their sweet time, but CBDCs leave them completely in the dust. You never have to wait for the next business day or cross your fingers hoping a payment clears.

- Instant cross-border transfers

- Fewer middlemen are slowing down the process

- Blockchain-powered error reduction

Merchants get paid faster, which keeps their small businesses humming like well-oiled machines.

Reduced transaction costs

Sending money with traditional electronic money often comes with hidden fees. Even physical cash has hidden costs, like printing the bills or securely moving coins in armored trucks. Central Bank Digital Currencies can dramatically cut these everyday expenses. Digital payments simply run faster and require far less manual staff to process.

For example, using a CBDC could mean you pay absolutely zero extra charges for small purchases at your local corner store.

Small businesses could save thousands of dollars on credit card swipe fees each year. Banks can move funds more quickly between accounts without relying on costly clearinghouses in the middle. This all adds up to more savings for both shoppers and shop owners, making everyone’s wallet a little bit happier.

Improved transparency and security

Every single digital dollar in a CBDC system leaves a clear record. People and businesses can track payments with highly visible trails.

This transparency makes it incredibly hard for bad actors to hide illegal money moves. Banks and government agencies can spot fraud or accounting mistakes much faster by following these digital records.

Key security features include:

- Transparent digital tracking trails

- Advanced blockchain encryption

- Built-in fraud detection tools

Hackers find it much harder to break into CBDCs than regular cash systems that are protected by simple passwords. As more countries adopt CBDCs, security experts keep sharpening their tools so your funds stay safe.

Potential Challenges and Criticism

Not everyone is excited about digital cash from central banks. Many folks worry deeply about their private information and personal freedoms. Hackers might see these centralized systems as a tempting target, and old-school banks could face massive changes. Let’s look at the biggest hurdles.

Privacy concerns

Privacy is the absolute biggest concern when discussing government digital money. A CBDC could technically let a central bank see every single digital payment you make.

While this data trail might help stop crimes, it also makes it easy for your daily spending habits to be tracked. Many Americans worry this could lead to government overreach or the misuse of sensitive financial information.

“Financial privacy is a cornerstone of American freedom, and any decision to authorize a CBDC must remain with the American people.”

The US government took major action on this exact issue recently. In January 2025, President Donald Trump signed an Executive Order prohibiting federal agencies from creating a US CBDC, citing severe risks to individual privacy.

Following that, in March 2026, the US Senate passed a housing bill containing an amendment that temporarily bans the Federal Reserve from issuing a retail CBDC until 2030. These choices show how deeply people value their financial privacy.

Risk of cyberattacks

Online thieves and sophisticated hackers target digital currency platforms all the time. A national CBDC faces incredibly high risks from state-sponsored cyberattacks. Bad actors could try to steal money or leak the private financial data of millions of citizens at once.

Even the biggest commercial banks have fallen victim to data breaches in the past, proving that no system is ever fully foolproof. Hackers move fast, inventing new tricks every single day. One massive successful attack might destroy public trust in a CBDC overnight.

Strong cybersecurity protocols, smart rules, and teamwork between banks and tech experts are required to lower this risk, but the threats never truly sleep.

Impact on traditional banking systems

While cyberattacks pose a clear danger, CBDCs also bring massive new waves to traditional banking. Local banks may see far fewer customer deposits if people keep their digital currency directly with the central bank.

This sudden shift could make it very tough for community banks to lend money for mortgages or small business loans as freely as before.

Central banks might start handling the day-to-day transactions that your local bank teller usually manages. That means traditional financial institutions need to completely rethink their roles in money services.

To adapt, many banks are now partnering with financial technology companies to offer new, private digital payment solutions just to keep pace. Money always finds a way to flow, but its journey might take some sharp turns ahead.

Global CBDC Efforts

Countries everywhere are actively testing digital cash issued by their central banks. Some places already use these new currencies every day, completely changing how their citizens pay for things.

According to a 2026 update from the Atlantic Council’s CBDC Tracker, over 130 countries are currently exploring digital currencies.

These 130 nations represent a staggering 98% of the entire global GDP, showing a massive worldwide shift.

Cross-border CBDC projects

Cross-border CBDC projects allow digital money to move faster and much more safely between different nations. The Bank for International Settlements is currently working with central banks in places like Singapore, Hong Kong, Thailand, and the United Arab Emirates.

Their famous Project mBridge uses custom blockchain technology so people can send international payments without the old, frustrating delays.

Experiments like Project Dunbar brought together banks from Australia, Malaysia, Singapore, and South Africa. These efforts prove that different countries can successfully build a shared payment system using digital currency.

Such global teamwork helps cut costs for families who send money home, and it helps businesses pay their overseas partners without losing money to high exchange fees.

Examples of CBDCs in circulation

Digital currency is not just a wild theory anymore. Some countries have fully launched their own central bank digital currencies, and people use them for daily shopping.

- China’s Digital Yuan (e-CNY) has been used by millions since 2020 for daily snacks and transit.

- The Bahamas’ Sand Dollar helps more people access banking directly through their smartphones.

- Nigeria’s eNaira makes it much easier for citizens to buy household items and send money to relatives quickly.

- Jamaica’s JAM-DEX gives everyone access to electronic money that acts as official legal tender across the country.

The Role of CBDCs in Everyday Life

CBDCs or similar digital assets could soon show up in your digital wallet, sitting right next to your saved credit cards. They might completely change how you pay for your morning coffee or how you receive your weekly paycheck.

- Faster checkouts at local stores

- Instant cross-border payments

- Lower fees for merchants

How could they change commerce

Shoppers could soon pay for groceries in exact seconds using digital currency, entirely skipping cash or plastic cards. Merchants would receive their funds right away, making it much smoother and less stressful to run a local store.

Small businesses might reach totally new customers because anyone with a smartphone could buy from them securely. Sending money to a supplier overseas would take minutes instead of days, all thanks to faster payment systems built on blockchain technology.

Prices may become much clearer since every digital transaction leaves a transparent trace. Fraud gets dramatically tougher, too, because verified digital payments leave very few shadows for scammers to hide inside. Digital assets help businesses tighten their security and trim their operating costs at the exact same time.

Potential applications for businesses and consumers

CBDCs and private stablecoins could totally change how people and companies manage their finances. This new type of legal tender offers huge benefits for both small shops and giant financial players.

- People could pay for everyday goods with a simple phone tap using digital currency, making it just as easy as handing over a paper dollar.

- Small retail businesses might save thousands by skipping the swipe fees that credit card companies charge for every single sale.

- Companies could pay their workers much faster since digital currencies do not depend on slow bank transfer networks.

- Family members could send each other money securely across the globe, day or night, without paying high wire transfer fees.

- Government programs, like tax refunds or emergency aid, could arrive directly into a person’s digital wallet, completely skipping mail delays.

Why Should You Care About CBDCs?

CBDCs could fundamentally shape the way you spend, save, and manage your financial life. They might soon touch parts of your daily routine that you never guessed needed a modern upgrade.

Economic implications

A Central Bank Digital Currency completely changes how money physically moves through the economic system. Governments can send emergency payments rapidly and at a much lower cost using digital currency. This speed can help citizens receive crucial aid during tough times, such as a natural disaster or a sudden economic crisis.

If more folks use digital money directly from the central bank, traditional banks will have fewer customer deposits to lend out. That could mean your local bank needs to find totally new ways to offer mortgages or collect savings.

Even if the US restricts its own digital dollar, American multinational corporations will still have to interact with foreign CBDCs. A 2025 report from the Digital Dollar Project noted that US businesses must adapt to these global digital networks to stay competitive internationally.

Influence on monetary policy

CBDCs give central banks a lightning-fast way to adjust the total money supply in a country. They can add or remove digital currency from the system almost in real time.

“Central banks view digital currencies as a real-time tool to manage inflation and steady the national economy.”

This immediate control helps officials manage inflation and support broad economic stability much faster than using traditional, outdated methods.

Interest rates attached to CBDCs could directly change how people choose to save or spend their earnings. If digital interest rates go up, folks might decide to hold more digital currency in their wallets.

Role in the future of digital payments

Digital currency from a central bank could make all your monthly payments much faster and smoother. People might use their phones to instantly pay utility bills, shop at online boutiques, or split a dinner check with digital cash. These modern digital payment systems work perfectly every single day, even during bank holidays or late weekends.

Central banks can easily watch for risky money laundering moves and stop bad actors much more effectively. In 2026, the global interest in CBDCs is pushing the entire financial industry to modernize.

Whether a country uses a public CBDC or relies on private dollar-backed stablecoins, these new digital tools aim to open fresh doors for how we all pay each other.

Wrapping Up

Central Bank Digital Currencies sit right at the fascinating crossroads of traditional money and modern technology. Central banks across the globe are testing these digital assets, looking for ways to make payment systems faster and much safer.

In China, millions of citizens already use the e-CNY daily for shopping and public transit. Meanwhile, the Bahamas uses its Sand Dollar as legal tender to boost financial inclusion across its beautiful islands.

The US is taking a cautious approach, with recent 2026 legislation aiming to protect consumer privacy by limiting the Federal Reserve’s digital currencies. Yet, the global shift is undeniable. Payments everywhere will soon move quicker than a wink, reducing costs for businesses and shoppers alike.

Every new swipe, tap, or scan brings us all a little closer to a brand-new chapter in digital finance, answering exactly what is a CBDC and why you should care.