Standing out in a saturated business landscape is becoming increasingly difficult. Efficient business operation management might seem inconsequential but it can lead to high-impact benefits.

If you wish to streamline business operations and reduce unnecessary downtime, this guide is for you. Here are five steps you can take to maximize potential and achieve business goals:

1. Automate Repetitive Tasks

Whether you run a law firm or manage a marketing firm, repetitive tasks are inevitable. Luckily, recent technological advancements have simplified such processes. Routine tasks, such as email marketing, workflow management, invoice clearance, and client follow-up, can be scheduled beforehand.

The benefits of automation for businesses include:

Increased Productivity

When mundane tasks are automated, employees can focus on more high-value and creative assignments and exude greater productivity.

Cost Reduction

The cost of manual labor can overwhelm business finances. Cloud computing, for instance, can save the cost of managing physical documents and a storage unit.

Reduced Errors

Despite continuous employee training, document processing errors are inevitable. Implement accounts payable process automation to streamline invoice processing. AP automation services use artificial intelligence (AI) and optical character recognition (OCR) to ensure error-free payment management.

Customer Satisfaction

With automated customer response software, you can improve the customer satisfaction ratio and turn viewers into consumers.

2. Implement Document Management Systems

The sheer volume of files overwhelms businesses worldwide. Without efficient document management, businesses can lose time searching for documents and suffer from security breaches. It can also hinder teamwork and communication, leading to reduced productivity.

Here are some steps you can take to streamline document management:

Centralize all Documents

Spending time on retrieving documents is counterproductive. To tackle this, use centralized document management systems so employees don’t have to comb through stacks of paper. It is also beneficial for remote teams.

Implement Access Control

Access control features make sure only authorized individuals can view or edit sensitive documents. This can reduce data breaches and ensure compliance with industry regulations. Access control also improves accountability and transparency as there is a clear record of who viewed a file and when.

Use Scanning Services

Turning physical documents into digital files can save your business from reduced downtime. You can avail dedicated document scanning services that comply with security standards. Free up valuable space and reduce manual labor.

Leverage Technology

Technological facilities, such as e-signatures, OCR, and cloud computing, have simplified document management to unprecedented levels.

Research shows that efficient document management reduces document search time by 50% and audit preparation time by 30%. Thus, you can maximize business operations without breaking the bank.

3. Implement Cybersecurity Measures

The security of your business data is just as important as document management. Here are some steps you can take to prevent unauthorized access and downtime:

Strong Passwords

Research shows that more than 80% of security breaches in companies occur due to weak passwords. Set difficult-to-guess passwords using a mix of letters and mixed characters. You can also institute centralized password management systems.

Regular Security Audits

Just like financial audits, security audits identify compromised areas and create a comprehensive data protection plan to prevent losses.

Educate Employees

Despite using stringent firewalls, employee mistakes can expose you to cyber security threats. Invest in employee training regarding phishing attempts and unsafe site messages.

Data Backup

Regularly backup client and investor files to recover data in case of a security breach or hardware malfunction. Taking preventative measures can save you from large-scale financial losses.

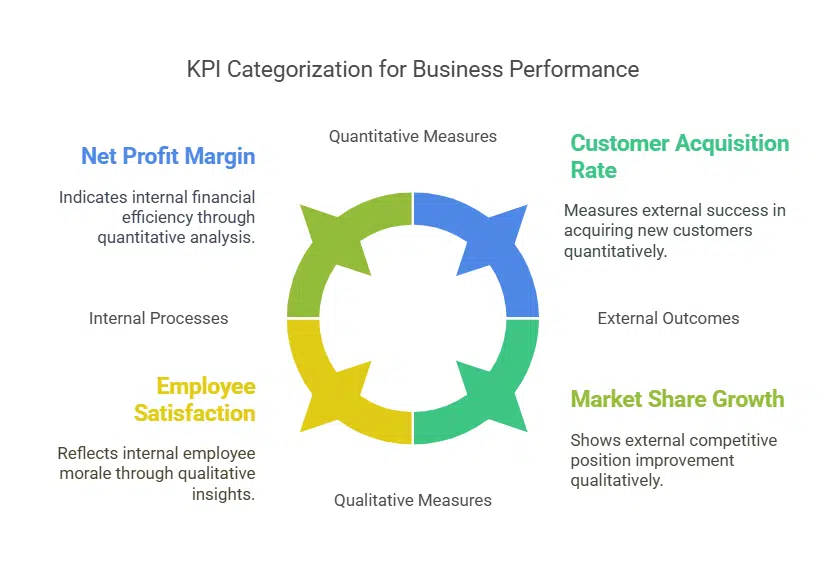

4. Monitor Key Performance Indicators

Key performance indicators (KPIs) are quantifiable measures of progress. Once you have set business goals, set KPIs to objectively track your performance against them. You can measure the following aspects of your business with KPIs:

- Financial performance, such as net profit, revenue growth, and investor revenue

- Customer acquisition and conversion rates

- Employee goals and performance ratios

- Sales performance, such as sales cycle length and deal closing ratio

Key performance indicators allow you to assess your business’s strengths and weaknesses and create a plan based on data-driven insights. They can also enhance communication between employees, management, and investors.

KPIs allow you to adapt to changing business needs and market conditions. They can be aligned directly with your business goals and lead to actionable insights.

5. Invest in Employee Training

The benefits of employee training are unmatched. They not only increase the skill level of your resources but also boost company performance. Here’s how you can get started:

- Identify individual training gaps.

- Create tailored strategies for every employee and build on their previous experience.

- Reach out to industry experts and mentors and create a chain of communication between them and your employees.

- Set learning goals for each employee and track their performance against them.

- Make sure the training strategies align with your business objectives.

Employee training can increase retention and reduce turnover. It can also boost morale, fostering a culture of innovation and future leadership.