The streaming wars have officially transitioned from a chaotic battle for production volume to a calculated war for efficient retention. On January 15, 2026, Netflix and Sony Pictures Entertainment (SPE) announced a landmark expansion of their partnership: a global Pay-1 licensing deal that grants Netflix exclusive post-theatrical streaming rights to Sony’s slate worldwide. So let’s see what this Netflix Sony Global Deal 2026 is about.

Why Does the Netflix Sony Global Deal 2026 Matter Right Now?

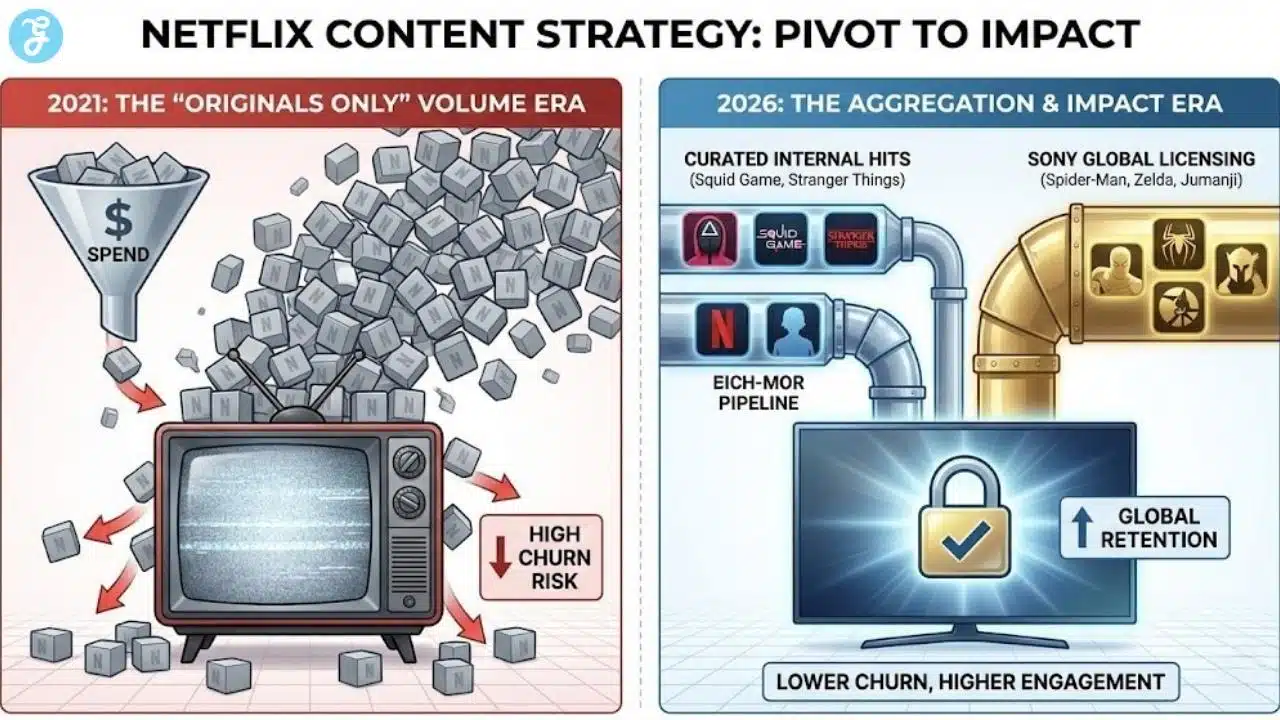

It signals a definitive pivot in Netflix’s strategy—admitting that even with a projected $18 billion content budget for 2026, it cannot manufacture enough culture-defining blockbusters internally to satisfy a global audience. For Sony, it cements its status as the industry’s smartest “arms dealer,” profiting from the streaming wars without suffering the casualties of fighting in them. This deal isn’t just about movies; it represents the stabilization of the media ecosystem where “renting” hits is once again as valuable as owning them.

Contextual Background: The “Great Re-Bundling” (2021–2026)

To understand the magnitude of the 2026 Netflix-Sony global pact, we must dissect the trajectory of the last five years. The early 2020s were defined by the “Gold Rush” mentality. Every major studio—Disney, Paramount, Warner Bros., and NBCUniversal—pulled their content from Netflix to launch their own “Netflix Killer” services. They built walled gardens, believing that exclusive IP would force consumers to subscribe to five or six different apps simultaneously.

However, by late 2025, the economic reality had shattered that dream. The “Great Re-Bundling” began as churn rates spiked to record highs. Consumers, fatigued by subscription fragmentation, began rotating services monthly, canceling platforms as soon as a specific show ended. Wall Street stopped rewarding subscriber growth and started demanding profitability.

In this chaotic environment, Sony Pictures stood alone. They famously refused to launch a “Sony+” service. Instead, they doubled down on their identity as a traditional studio, selling their Pay-1 window rights to the highest bidder—first Starz, then Netflix in the US (2021), and now Netflix Globally (2026). While their competitors lost billions trying to build tech stacks, customer service centers, and global billing infrastructure, Sony posted record profits.

This new deal is the final capitulation of the “Walled Garden” era. It proves that the future of streaming isn’t about everyone having their own app; it’s about a few “Super Aggregators” (Netflix, Amazon, Disney) paying rent to the content landlords (Sony) to keep their shelves stocked. The era of fragmentation is over; the era of consolidation and aggregation has begun.

Core Analysis: The Mechanics of the Deal

1. The “Arms Dealer” Strategy: Sony’s Masterstroke

While Disney, Paramount, and Warner Bros. Discovery spent the last half-decade bleeding billions to build D2C (Direct-to-Consumer) platforms, Sony sat out. They recognized early that the most profitable position in a gold rush isn’t digging for gold—it’s selling shovels.

By licensing its content to Netflix, Sony Pictures has remained the only consistently profitable major film studio division without the drag of a money-losing streaming service.

- Financial Efficiency: Sony effectively outsources the technology costs, customer acquisition costs (CAC), and churn risks to Netflix. They simply deliver the file and cash the check. In 2025 alone, while Disney+ struggled to reach double-digit profit margins, Sony’s Pictures segment reported operating margins closer to 11-12% due to this low-overhead model.

- Creative Independence: Because they don’t need to feed a specific streaming algorithm or fill a “content quota” for a weekly release schedule, Sony can focus purely on theatrical viability. This leads to bigger, event-style films like Spider-Man and Uncharted rather than “filler” content designed just to keep subscribers from canceling.

This strategy has allowed Sony to maintain a “clean” balance sheet, making them the most stable entity in Hollywood in 2026. While others are cutting costs and laying off staff to plug streaming holes, Sony is investing in new IP, such as the massive Legend of Zelda production.

2. The Quality vs. Quantity Correction

Netflix’s 2026 content budget is projected to hit $18 billion, an 11% increase from 2024. However, the allocation of this spend has shifted dramatically. In 2021, the focus was on volume—flooding the zone with originals to prove they didn’t need Hollywood. In 2026, the strategy is “Impact per Dollar.”

Netflix has learned a hard lesson: Producing a blockbuster from scratch is incredibly risky. For every Glass Onion or Red Notice, there are dozens of expensive failures like The Gray Man or Rebel Moon that failed to generate long-term cultural cachet. The “Netflix Original Movie” brand often struggled to shed the stigma of being “TV movies with big budgets.”

Licensing a guaranteed hit like Venom 3 or the upcoming Beatles biopics often delivers better engagement-per-dollar than producing a high-risk $200 million original film. This deal allows Netflix to keep its “quantity” high with high-quality, recognized IP. It frees up its internal production capability to take creative risks on potential breakouts like Squid Game rather than forcing “manufactured” blockbusters. It is a shift from “Volume” to “Curated Scale.”

3. The Global Retention Game & Marketing Efficiency

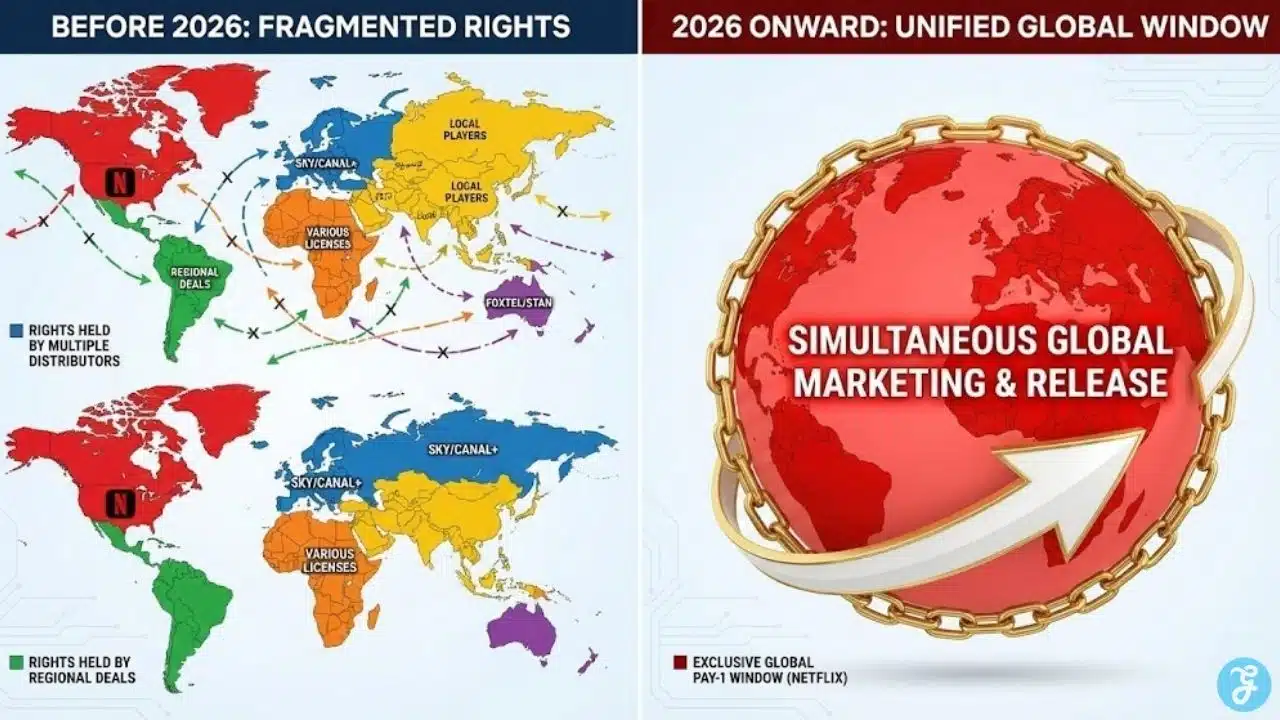

The key differentiator of the 2026 deal is the global scope. Previously, rights were fragmented—Netflix had the US, but Sky held rights in the UK, Canal+ in France, and various local players held rights in Asia. This fragmentation made global marketing impossible.

- Unified Marketing Machine: Netflix can now push a “Coming to Netflix” notification for a Sony blockbuster to 300M+ subscribers simultaneously. This creates a global “watercooler moment” that mirrors a theatrical release.

- Churn Reduction in Emerging Markets: In emerging markets (LATAM, APAC, India), access to Hollywood blockbusters is a primary driver for subscription. These audiences often value established franchises (Marvel, Jumanji) over niche indie dramas or US-centric comedies. This deal plugs the gap where Netflix’s local originals might be too specific or culturally nuanced to travel globally.

- The “Second Life” Phenomenon: We have seen repeatedly that theatrical “flops” often become massive hits on Netflix (e.g., Madame Web, 65). By owning the global window, Netflix guarantees it captures this value capture worldwide, effectively monetizing the “long tail” of Sony’s slate better than anyone else could.

4. The Ad-Tier Equation

We cannot analyze this deal without looking at Netflix’s booming advertising business. By Jan 2026, over 40% of Netflix’s new sign-ups are on the ad-supported tier. Advertisers crave “brand-safe” premium content. They want their commercials running next to Spider-Man, not an obscure, edgy documentary that might be controversial.

Sony’s content is, by definition, broad-appeal and advertiser-friendly. This deal is as much about securing inventory for Netflix’s ad partners as it is about pleasing subscribers. It allows Netflix to charge higher CPMs (Cost Per Mille) because they can guarantee placement alongside globally recognized, safe IP. This transforms the Sony library into a high-yield ad revenue generator.

5. The Shadow of Consolidation (The WBD Factor)

This deal cannot be viewed in isolation. It occurs against the backdrop of persistent reports that Netflix is exploring an acquisition of Warner Bros. Discovery assets. If Netflix were to acquire WBD, they would own the DC Universe. With this Sony deal, they effectively lease the Spider-Man corner of the Marvel Universe.

The Super-Aggregator: Netflix is moving toward becoming the default operating system for entertainment. By securing Sony (the last independent major) and potentially eying WBD assets, they are building a moat that prevents competitors (like Amazon Prime or Disney+) from locking down this critical supply of films. This is a defensive move to starve the competition as much as it is an offensive move to gain content.

Regional Impact Analysis

Europe (EMEA):

In Europe, this deal is a blow to local broadcasters like Sky and Canal+, who have historically relied on US studio output deals to maintain their subscriber bases. For Netflix, it solves the European “content quota” puzzle by ensuring high-demand content is available alongside their local European productions. It solidifies Netflix’s dominance in markets like Germany and France where local competition remains stiff.

Asia-Pacific (APAC):

In markets like Japan and South Korea, Sony’s anime content (via Crunchyroll/Sony Pictures Animation) is hugely valuable. While the press release focuses on live-action, the deepened relationship likely greases the wheels for more anime licensing, which is a critical growth vector in APAC. Furthermore, for the Indian market, where Sony has a massive footprint, this deal could eventually lead to deeper integration of Sony’s Indian theatrical slate onto Netflix, challenging local players like JioCinema.

Latin America (LATAM):

LATAM audiences have statistically shown a higher preference for dubbed Hollywood blockbusters over subtitled prestige TV. The addition of the Spider-Man and Venom franchises is a direct retention tool for the massive, price-sensitive subscriber base in Brazil and Mexico, preventing them from churning to lower-cost ad-supported alternatives.

The Talent Equation & The Algorithm’s New Diet

The “Best of Both Worlds” for Hollywood Talent

Beyond the boardroom economics, this deal solves a critical personnel crisis for Netflix. Top-tier directors and A-list stars have historically been hesitant to sign with streamers because they fear their work will vanish into the “digital void” without a proper cultural moment. They crave the prestige of a theatrical red carpet—something Netflix has struggled to provide at scale.

The Sony-Netflix pipeline offers the perfect compromise. A filmmaker can sign with Sony, get the massive global marketing push and box office bonuses of a theatrical release, and then enjoy the “immortality” of the Netflix homepage four months later. This structure makes Sony a more attractive home for talent than a pure streamer. For Netflix, it indirectly improves the quality of the incoming library; they are receiving films made by creators who were incentivized by box office backend, meaning the content is engineered for maximum audience appeal, not just algorithm retention.

Feeding the Algorithm “High-Octane” Data

Table 1: Evolution of the Partnership (2021 vs. 2026)

| Feature | 2021 Pay-1 Deal | 2026 Global Pay-1 Deal | Strategic Implication |

| Geographic Scope | US, Germany, SE Asia (Selected) | Worldwide (Rolling out to 2029) | Netflix becomes the only global movie screen, simplifying rights management. |

| Key IP Included | Spider-Man: Across the Spider-Verse, Uncharted | Legend of Zelda, Spider-Man: Beyond, Beatles Biopics | Shift from comic books to broader Video Game IP & Prestige Biopics. |

| Window Timing | ~120 Days post-theatrical | Flexible/Tiered (Market dependent) | Respects theatrical exclusivity to maximize box office revenue before streaming. |

| Library Access | Limited Selection | Expanded Vault (Deep catalog) | Fills the “long tail” library for retention; keeps users in the app longer. |

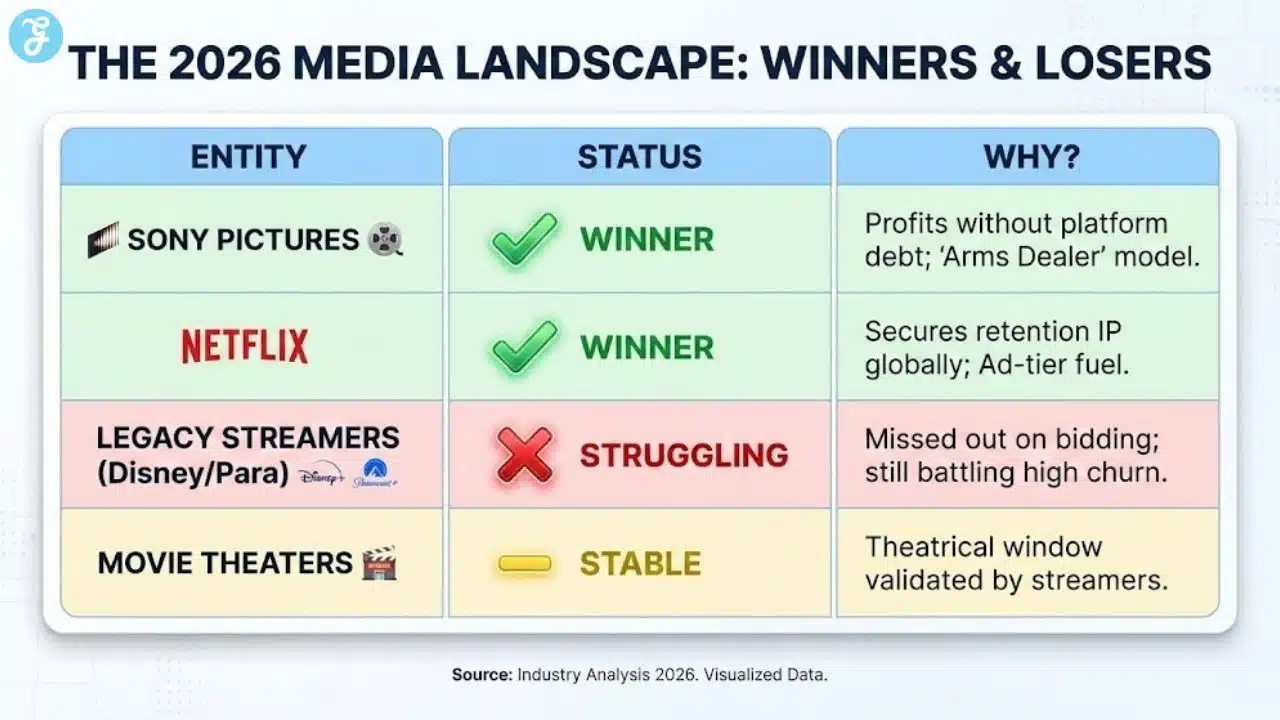

Table 2: The “Winners and Losers” of the 2026 Landscape

| Entity | Status | Why? |

| Sony Pictures | Winner | Maximizes revenue without streaming losses; stock remains stable; avoids tech debt. |

| Netflix | Winner | Secures “Must-Watch” IP without production risk; reduces churn; attracts advertisers. |

| Disney/Hulu | Loser | Loses potential to bid for Sony content to bolster their catalog gaps; faces stronger Netflix. |

| Movie Theaters | Neutral/Positive | The deal validates the “Theatrical Window” model; movies must hit theaters to trigger the deal. |

| Indie Producers | Loser | As Netflix spends heavily on Sony, there may be less budget for acquiring smaller, independent films. |

Table 3: Estimated Content Valuation vs. Production Cost (2026 Estimates)

| Content Type | Estimated Cost | Reach/Impact | Risk Level |

| Netflix Original Blockbuster | $200M+ (Production + Marketing) | High (Global launch) | High (If it flops, money is gone) |

| Sony Licensed Blockbuster | ~$80M-$100M (Licensing Fee) | High (Built-in Fanbase) | Low (Quality is known pre-purchase) |

| Mid-Budget Original | $40M | Medium | Medium (Hit or miss) |

Expert Perspectives

The Bull Case for Sony (Financial Prudence):

“Sony’s refusal to launch a ‘Sony+’ service will go down as the smartest strategic non-move of the decade. They are capturing the upside of streaming valuations through licensing fees while maintaining the discipline of a traditional studio. In 2026, cash flow is king, and Sony has the best cash flow story in Hollywood. They are effectively the Switzerland of the streaming wars—neutral, wealthy, and banking with everyone.” — Dr. Elena Ross, Media Economist at Stern School of Business.

The Bear Case for Netflix (Dependency Risk):

“While this secures content, it highlights a structural weakness. Ten years into original production, Netflix still relies on Spider-Man and Jumanji to drive Q4 engagement. If Sony ever decides to sell to a tech giant like Apple, Netflix loses a critical limb. Renting your success is a viable strategy, but it’s never as secure as owning it. They are patching a hole in their own production pipeline with Sony’s cement.” — Marcus Thorne, Senior Analyst at Vitrina AI.

The Advertiser’s View:

“The holy grail for us is predictability. Netflix Originals are great, but they are unpredictable. We know what we get with Sony IP. Placing a global campaign around the streaming debut of ‘The Legend of Zelda’ is a safe, high-ROI bet. This deal makes the Netflix Ad Tier significantly more attractive to Fortune 500 brands.” — Sarah Jenkins, Chief Strategy Officer at Omnicom Media Group.

The Road to 2029

Checklist:

- Unlike the 2021 US-centric deal, this 2026 agreement locks in Sony’s slate (Spider-Man, Jumanji, The Legend of Zelda) for Netflix members worldwide by 2029, unifying global marketing efforts.

- Sony avoids the churn and cash-burn of running a general entertainment streamer, securing billions in high-margin licensing revenue while competitors like Disney and Paramount bleed cash on infrastructure.

- The deal arrives amidst rumors of broader industry consolidation, highlighting a dual strategy: acquire distressed assets while licensing stable hits to reduce volatility.

- The deal upholds the theatrical window, confirming that streamers now rely on the “cinema halo effect” to drive value on their platforms rather than trying to kill movie theaters.

Short Term (2026-2027): The “Sony Hub” Integration

Expect to see “Sony Hubs” appear more prominently on the Netflix interface globally, similar to the “Disney” tile on Disney+. The release of the live-action Legend of Zelda will likely be the first major test of this global coordination—a massive theatrical run followed by a simultaneous global drop on Netflix, creating a second “cultural moment” that drives Q3/Q4 earnings. Netflix will likely use these releases to test new interactive features or merchandise tie-ins, leveraging Sony’s gaming prowess.

Medium Term (2028): The Tiered Window Experiment

As the global rights fully align, Netflix may experiment with “Premium Access” models. While they have historically avoided Pay-Per-View, the pressure to increase Average Revenue Per User (ARPU) might lead them to offer Sony blockbusters to “Premium” tier subscribers a week earlier than “Standard with Ads” subscribers. This would incentivize users to upgrade their plans, using Sony content as the carrot.

Long Term (2029 and beyond): The Utility Phase

By 2029, the distinction between “Netflix Original” and “Netflix Exclusive” will vanish for the consumer. The platform becomes a utility, like electricity or water. The danger for Netflix is complacency; if they rely too heavily on Sony’s output, their internal muscle for creating IP might atrophy. However, for the next three years, the content pipeline is more secure than it has been in a decade. We may also see this partnership evolve into co-productions, where Netflix puts up equity for Sony films in exchange for faster windows, blurring the line between studio and streamer even further.

Final Thoughts

The 2026 deal proves that the “Streaming Wars” were never about who could build the best app—they were about who could build the best business. Sony proved that you don’t need an app to win. Netflix proved that you don’t need to own everything to rule. Together, they have stabilized an industry that was dangerously close to collapsing under its own weight.