The landscape of Irish healthcare eligibility has undergone significant shifts heading into 2026, with the Government continuing to expand access to free primary care. While the “Medical Card” remains the gold standard for comprehensive coverage—including GP visits, prescriptions, and hospital care—the criteria for qualifying are more data-driven than ever. For those navigating the how to get a medical card in Ireland 2026 process, success lies in understanding the precise intersection of income thresholds, allowable expenses, and the HSE’s discretionary powers.

This guide provides a clinical breakdown of the current systems to help you determine which pathway offers your household the best financial protection.

Our Selection Methodology

To build this 2026 guide, we analyzed the latest National Assessment Guidelines from the Primary Care Reimbursement Service (PCRS), the HSE’s 2026 Income Threshold updates, and the recent “Median Income Expansion” legislative changes. We focused our selection on the five most reliable legal pathways to coverage, prioritizing those that offer the broadest range of services. Our data is grounded in the current 2026 weekly basic rates and the “Discretionary Hardship” protocols used by HSE assessment officers to ensure that even those slightly above the limits can find a route to eligibility.

5 Key Ways to Get a Medical Card in Ireland

Whether you are an employee, a pensioner, or a student, the HSE uses specific financial “gateways” to determine your entitlement.

1. The General Means Test (Aged Under 70)

For the majority of applicants under 70, the General Means Test is the primary route. This is a “net income” assessment, meaning the HSE looks at what you have left after essential taxes and living costs.

-

Best for: Working individuals and families with moderate incomes and high living expenses like rent or childcare.

-

Why We Chose It: This is the most flexible pathway because it allows you to subtract “allowable expenses” from your gross pay to meet the threshold.

-

Things to consider: You must provide proof of income (payslips/social welfare) and expenses dated within the last 3 months to pass the audit.

The HSE calculates your qualifying threshold by adding a basic rate to allowances for dependants and expenses. The table below outlines the basic weekly rates effective for 2026.

| Category | Basic Weekly Rate (<66 Years) | Basic Weekly Rate (66+ Years) |

| Single Person Living Alone | €184.00 | €201.50 |

| Single Person Living with Family | €164.00 | €173.50 |

| Married/Cohabiting Couple | €266.50 | €298.00 |

| Lone Parent Family | €266.50 | €298.00 |

2. The Over-70s Gross Income Pathway

Once you or your partner turn 70, the HSE shifts from a “net” assessment to a much simpler “gross income” test.

-

Best for: Retirees with stable pensions who may not have high deductible expenses like mortgages or childcare.

-

Why We Chose It: The income limits for this age group are significantly higher than the general means test, making it easier for pensioners to qualify.

-

Things to consider: If your gross income is slightly over these limits, the HSE will automatically re-assess you under the “Under 70” rules to see if your medical expenses allow for a discretionary card.

For 2026, the gross weekly income thresholds for those aged 70 and over remain a cornerstone of the system.

| Applicant Type | Gross Weekly Income Limit |

| Single Person | €550.00 |

| Married/Cohabiting Couple | €1,050.00 |

3. The “Undue Hardship” Discretionary Route

If your income exceeds the 2026 thresholds, you are not automatically disqualified. The HSE has the legal power to grant a “Discretionary Medical Card” if your medical costs would cause financial hardship.

-

Best for: Individuals with chronic illnesses, high medication costs, or frequent consultant visits.

-

Why We Chose It: It serves as a vital safety net for “the squeezed middle” who earn too much for a standard card but cannot afford private healthcare.

-

Things to consider: You must provide a detailed medical report from your GP or consultant outlining your condition and the associated ongoing costs.

This route emphasizes that the Medical Card system is a health-based welfare tool, not just a strict financial ledger.

4. The Median Income Expansion (GP Visit Card)

While technically a “GP Visit Card” rather than a full Medical Card, this 2026 pathway is the fastest-growing eligibility group. It covers the cost of the doctor but not the prescriptions.

-

Best for: Households earning up to the median national income who primarily need help with GP consultation fees.

-

Why We Chose It: The 2026 income thresholds for this card are roughly 50% higher than the full Medical Card, making it accessible to over 500,000 additional residents.

-

Things to consider: If you apply for a Medical Card and fail the means test, the HSE will automatically assess you for this card as a “consolation” benefit.

The 2026 GP Visit Card thresholds are designed to capture a broader segment of the working population.

| Category (Under 70) | Weekly Basic Rate (2026) |

| Single Person Living Alone | €418.00 |

| Single Person Living with Family | €373.00 |

| Couple / Lone Parent | €607.00 |

5. Automatic Entitlement Groups

Certain individuals qualify for a Medical Card regardless of their income due to specific social or legal circumstances.

-

Best for: Foster children, persons with EU entitlements (S1 forms), and those on specific social schemes.

-

Why We Chose It: It bypasses the bureaucracy of the means test for vulnerable groups, ensuring immediate access to care.

-

Things to consider: Even if you qualify “automatically,” you must still complete an application form to register your details and choose a GP.

Common automatic groups include children in foster care, people affected by the drug Thalidomide, and residents whose only income is a social welfare payment.

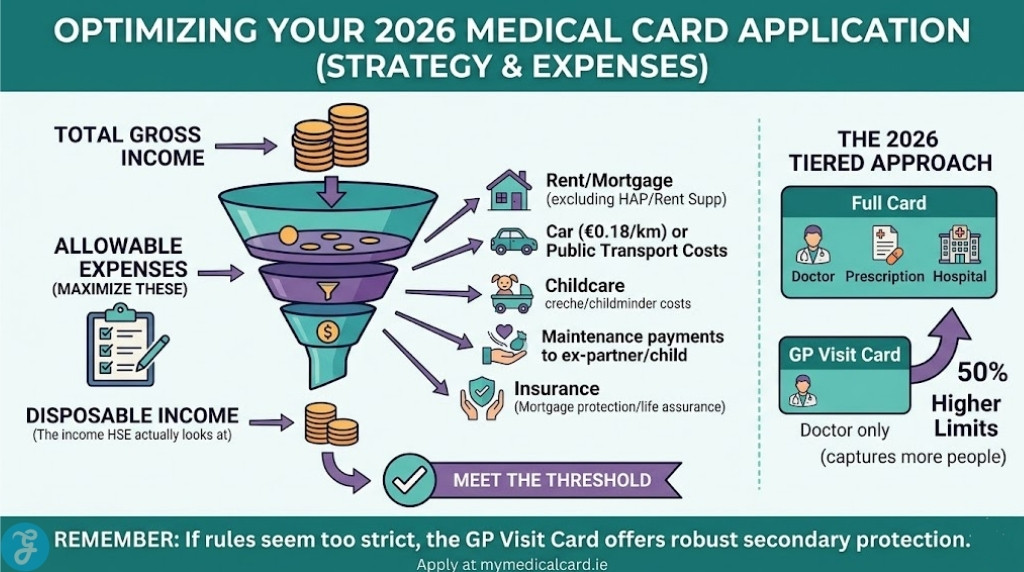

Strategic Analysis: Optimizing Your 2026 Application

To succeed in your how to get a medical card in Ireland 2026 application, you must maximize your “Allowable Expenses.” These are the costs that the HSE subtracts from your income to bring you under the threshold.

| Allowable Expense | 2026 Standard Deduction Tip |

| Housing | Full rent or mortgage (excluding HAP/Rent Supplement portions). |

| Travel to Work | €0.18 per km if using a car, or full public transport costs. |

| Childcare | Full weekly cost of creche or childminder. |

| Maintenance | Legally required payments made to an ex-partner or child. |

| Insurance | Mortgage protection and associated life assurance premiums. |

Refining Your Healthcare Strategy

Securing a Medical Card in 2026 is less about your total salary and more about how you present your “disposable” income to the HSE. By utilizing the online portal at mymedicalcard.ie, you can receive an instant preliminary assessment. Remember that the system is designed to be tiered; if you don’t meet the stringent rules for a full Medical Card, the 2026 expanded GP Visit Card thresholds offer a robust secondary defense against healthcare costs. In an era of rising costs, the Medical Card remains Ireland’s most significant tool for ensuring that your health is never compromised by your bank balance.

FAQs

-

Can I keep my Medical Card if I get a job? If you have been unemployed for 12 months, you can often keep your card for 3 years after starting work, regardless of your new salary.

-

How long does the application take? The HSE aims to process complete online applications within 15 working days.

-

Does the card cover dental? Yes, the full Medical Card covers an annual dental exam and specific treatments under the Dental Treatment Services Scheme (DTSS).