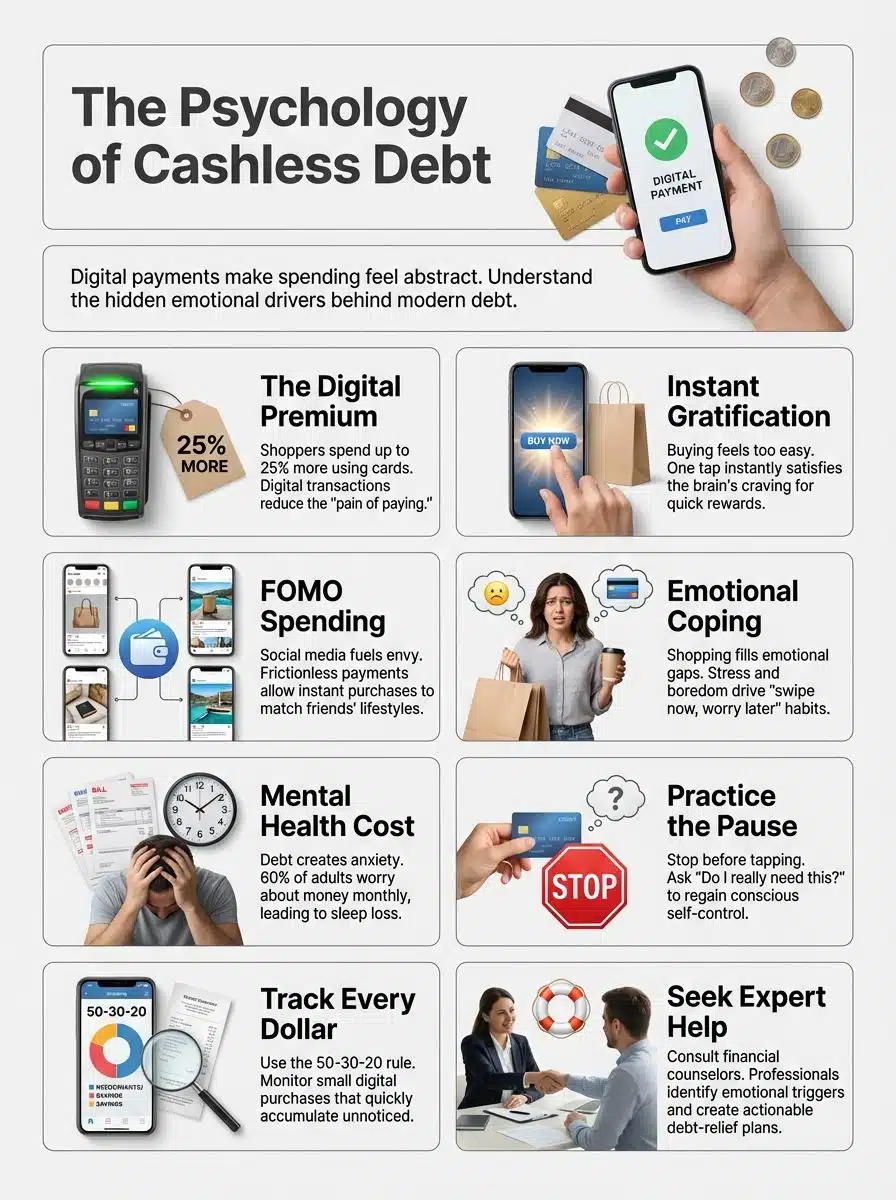

Have you ever wondered why it feels so easy to tap your card or phone and buy things, even if you do not need them? If your money seems to disappear faster than you expect, you are not alone. Many people find themselves stuck in debt because swiping or clicking makes spending less real. Here is one eye-opening fact: recent data suggests shoppers can spend significantly more when using digital payments compared to cash.

This blog will shed light on how living in a cashless economy affects your financial decisions. You will learn simple ways to take control of your spending habits by understanding the Psychology Of Debt. Keep reading, as your next smart move might just be a scroll away.

Emotional Drivers of Spending in a Cashless Society

Swiping a phone or tapping a card can feel almost too easy, right? Feelings push many people to spend, even when their bank account says “no.”

Instant Gratification and Impulse Purchases

Paying with a tap or click makes buying too easy. Digital payments act like magic wands, turning wishes into purchases within seconds. People get a thrill from seeing new items arrive fast.

The brain craves quick rewards, and cashless transactions feed this itch. In fact, services like Buy Now, Pay Later (BNPL) have revolutionized impulse buying. A 2023 study by Keil and Burg found that the availability of these options makes impulsive shopping visits 13% more likely to result in a purchase.

It is not just about ease; it is about removing the friction. In stores and online, flashy ads tempt shoppers at every turn. Bright “Buy Now” buttons create pressure to act before thinking twice. Many folks end up with things they never planned to buy, just for that rush of instant joy.

This habit can send budgets spinning out of control faster than expected fees on your phone bill. To combat this, try disabling “one-click” ordering on sites like Amazon. Forcing yourself to enter your shipping address every time creates a helpful pause that lets your rational brain catch up.

Fear of Missing Out [FOMO]

Fear of Missing Out, or FOMO, makes people feel left behind if they do not buy the latest thing. Social media shows pictures and posts about new gadgets, fancy meals, and trips. This can spark quick buying impulses.

In a cashless economy, digital payments make spending fast and easy. You see a trending product online; one tap on your phone sends money right away. Friends talk about deals or events you did not join in on, and that feeling grows stronger with each post you scroll past.

The fear pushes many to spend more than planned using credit cards or apps. FOMO changes consumer habits without most even noticing it happens so quickly. It fuels emotional spending as people chase what others seem to enjoy every day.

Emotional Spending and Coping Mechanisms

A bad day can drive anyone to swipe and shop. Buying things brings quick joy. Stress, sadness, or even boredom push people to make unnecessary purchases. In a cashless economy, shopping apps and tap-to-pay options tempt us more than ever.

Experts call this emotional spending. It becomes a coping mechanism that fills an emotional gap for just a moment. Digital payments blur the line between need and want in consumer habits. That small buzz after tapping your card feels good but fades fast, leaving some with regret or debt.

“Swipe now, worry later” has become an easy motto for many dealing with stress in today’s cashless world.

The Role of Payment Methods in Spending Habits

Tapping your phone or swiping a card feels so quick, it’s easy to forget you’re spending real money. With just a click, buying can lose its sting, and your wallet might scream for help later.

Reduced “Pain of Paying” with Digital Transactions

Swiping a card or using a phone to pay feels easy. Cash does not leave your hand, so spending seems painless. This phenomenon is known as the “Cashless Effect.”

A 2024 meta-analysis by the University of Adelaide confirmed that consumers tend to spend more when using cashless methods, especially on status items like jewelry or clothes. Because you do not physically hand over bills, you do not feel the loss as intensely.

Digital payments make it simple to buy things fast, almost on autopilot. This can trick your brain into ignoring the true cost. Consumer behavior shifts in a cashless economy as buying impulses grow stronger when no bills leave your wallet. That’s how transaction pain drops and overspending risks rise with digital transactions.

Convenience vs. Overspending Risks

Digital payments make shopping easy. A few taps and the deal is done. No need to count bills, wait for change, or feel cash leave your hand. This speed saves time in busy lives, but it can blur spending awareness.

Recent data from Capital One Shopping highlights a stark contrast in spending behavior. Here is how cash compares to credit in the modern market:

| Payment Method | Spending Behavior Risk | Usage Trend |

|---|---|---|

| Cash | High Friction: You feel the money leaving your hand, which naturally curbs spending. | Used in only roughly 11% of in-store transactions. |

| Credit Cards | Low Friction: Shoppers can spend up to 4x more compared to cash purchases. | Preferred by 83% of shoppers for daily transactions. |

Impulse buying grows in a cashless economy. It takes seconds to order food, games, or clothes from your phone—sometimes before you know you want them! Small amounts add up fast this way; many Americans struggle to track these digital purchases until their account runs low or credit card debt piles up. Easy payments boost comfort, but they also raise overspending risks for every age group and income level.

The Psychological Impact of Debt

Debt can feel like a heavy shadow, always following you around. Sometimes, it even sneaks into your thoughts at dinner or keeps you staring at the ceiling all night.

Anxiety, Stress, and Depression

Mounting debt can pile up stress like dirty laundry. Many people feel anxious each time they see a credit card statement alert on their phone. A growing number of studies show links between high consumer debt and mental health struggles, including depression.

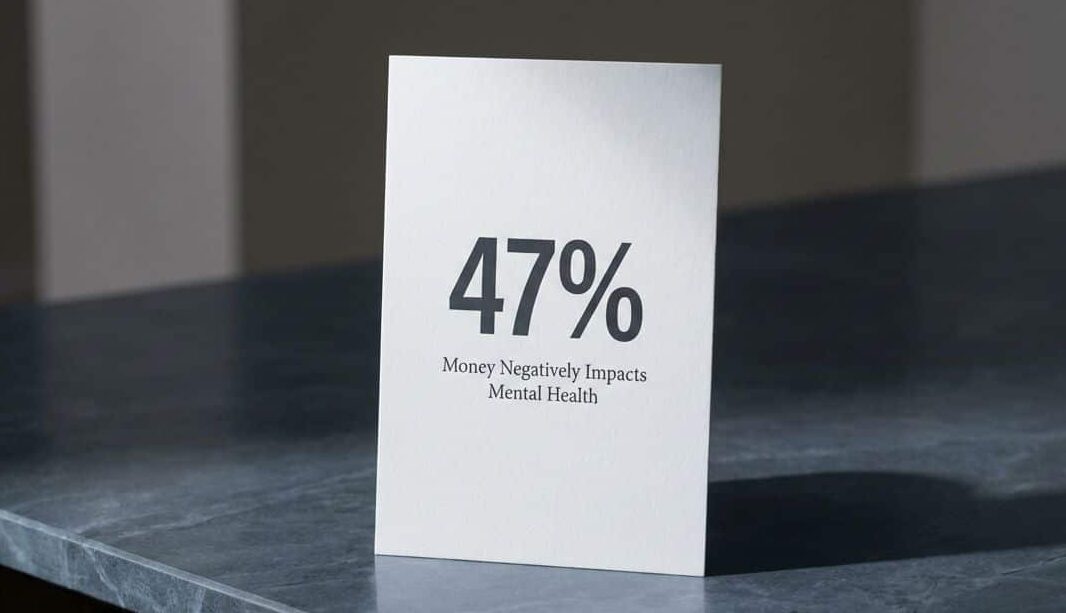

According to a March 2024 Bankrate survey, 47% of U.S. adults say money has a negative impact on their mental health. This worry can hurt sleep and deepen feelings of sadness.

“Financial stress is not just about math; it is a physical burden. 60% of respondents in a 2025 study admitted they avoided seeking mental health care specifically due to financial constraints.”

Late payments or maxed-out cards may weigh on your mind all day long. You might avoid calls or emails from lenders out of fear or shame. This adds to the tension, and guilty thoughts swirl faster in cashless societies where spending happens with just one tap.

Feeling down about finances also chips away at confidence, making it even harder to make smart decisions under pressure. As stress climbs higher, decision fatigue comes next in the cycle of financial psychology challenges many face today.

Decision Fatigue and Cognitive Overload

Endless choices in a cashless economy can wear people out. Choosing between dozens of payment apps, credit cards, and sales leaves the brain tired. Small decisions pile up fast.

By late afternoon, people may grab whatever catches their eye just to be done with it. Digital transactions happen quickly, sometimes too quickly for careful thinking. People swipe or tap without stopping to check their spending limits or ask if they really want that extra coffee.

One study showed consumers using cards spend up to 83 percent more compared to those using cash. Too many daily choices plus instant payments can cause stress, forgetfulness, and mistakes with money management.

Debt and Personal Identity

Debt can shape how people see themselves. Some folks feel shame or guilt about owing money. They might think debt means they failed, even if that is not true.

Credit culture in many places pushes people to spend now and worry later. This thinking can hurt their self-esteem over time. Digital payments make it easy to buy things fast, but that ease hides the emotional cost of spending too much.

People may use shopping as a coping method during stress or sadness; this habit often leads straight to financial trouble. A growing loan balance can then blur a person’s sense of pride or security right along with their bank statements.

Strategies to Address Spending Habits and Debt

You can learn smart ways to control your buying impulses. Stick around and see how you can keep your wallet happy!

Developing Self-Awareness and Mindful Spending

Self-awareness is the first step toward smarter spending. Take a pause before tapping your card or phone. Ask yourself, “Do I really need this?” In a cashless economy, digital payments make it easy to lose track of what you buy.

A powerful technique to regain control is the “72-Hour Rule.” When you see something you want to buy online, leave it in your cart for three days. Often, the emotional urge to buy fades, and you save that money instead.

Mindful spending means paying attention to your feelings while shopping. Sometimes stress or sadness can push us into buying things we do not need. Notice patterns in your own consumer habits; keep a simple notebook or use a budgeting app for tracking each purchase.

Slowing down and thinking twice helps control buying impulses and supports better financial decision-making every day.

Setting Financial Goals and Budgets

Setting clear financial goals creates a plan for your money. Picture saving up for a new phone or building an emergency fund, one small step at a time. Many experts suggest using the 50-30-20 rule: spend half of your income on needs, thirty percent on wants, and save the rest.

Budgets work best if you track every dollar, especially those quick digital payments that add up fast. To make this easier, consider using modern tools:

- YNAB (You Need A Budget): Great for giving every dollar a job and planning ahead.

- Monarch Money: Excellent for couples who need to see their full financial picture in one place.

- Goodbudget: A digital version of the envelope system that helps you stick to strict limits.

Small changes matter; skipping one fancy coffee each week could mean hundreds saved by year’s end. This kind of control brings peace of mind and reduces stress linked with debt management.

Seeking Professional Support

Talking with a financial counselor can stop money stress from growing. Financial psychology experts listen to your worries, then teach simple steps for better debt management. Money coaches often help you build plans, track spending habits, and break cycles of emotional spending.

Having an expert in your corner feels like getting a helpful teammate on a hard day. Some people join support groups or contact the National Foundation for Credit Counseling (NFCC). These places offer trustworthy advice about debt relief options and ways to handle digital transactions wisely.

You might learn about payment methods that limit impulse buying or tips for staying calm when making big decisions. A professional sees patterns you might not spot alone; their guidance brings fresh hope and confidence back into the picture.

Final Thought: Taking Control of the Psychology of Debt

You have seen how paying with a tap or click can change our spending habits, sometimes without us noticing. Simple steps like tracking your money, setting clear goals, and asking for help if needed can make a big difference.

Do you check your balance before buying your morning coffee, or does it slip your mind? Small changes today may save you stress tomorrow, helping you feel more in control of your money and mood.

Even one mindful choice at checkout can put you on the path to less debt and greater peace of mind, I know, because I’ve felt that rush from impulse buys too!