A decade ago, most people used one app for chat, another for payments, and another for shopping. That separation felt normal. Now, the lines are fading. In many markets, the phone is turning into a single doorway where money, messages, and commerce meet.

That doorway has a name. It is the super app.

The promise is simple. You do more without switching apps. You pay a friend inside a chat. You buy a product without filling forms again. You track delivery where the conversation happens. For users, it can feel smooth. For companies, it can feel like a dream: more time in-app, more data, more ways to cross-sell.

But there is a tradeoff. When one platform becomes your wallet, your inbox, and your mall, it holds a lot of power. It also becomes a bigger target for fraud. And it raises hard questions about privacy, competition, and financial stability.

This guide explains how the super app model works, why it grew fast in parts of Asia, why other regions often look different, and what to watch in 2026 and beyond.

What Is A Super App And Why Is It Spreading?

A super app is a host application that bundles many services under one roof, often centered on a high-frequency feature like messaging or payments. It also commonly acts as a platform for “mini apps” that run inside it.

The key idea is not “an app with many features.” The key idea is a platform that becomes your default place to do daily tasks. Once that happens, the app turns into a habit.

Most super apps follow a recognizable path:

-

Start with a sticky core product (chat, ride-hailing, or wallet).

-

Add payments so money can move inside the system.

-

Add commerce and service categories that users need weekly or daily.

-

Open a developer layer so third parties can ship mini apps.

That pattern helps explain why WeChat and Alipay are cited so often. They did not begin as “everything apps.” They became “everything apps” by building outward from a core that people already used constantly.

| Super App Signal | What It Usually Includes | What It Creates |

|---|---|---|

| Core daily hook | messaging or transport | frequent opens |

| Built-in wallet | P2P, merchant pay, bill pay | low-friction transactions |

| Service layers | shopping, food, travel, utilities | fewer app switches |

| Mini apps | third-party services inside | fast expansion |

How The Super App Model Works Behind The Scenes

The user sees one interface. Under the hood, a super app is closer to an operating system for services than a single product.

A simple way to picture it is hub-and-spokes.

The hub is the shared infrastructure:

-

Identity and login

-

Payments and wallet

-

Notifications

-

Customer support

-

Trust and safety systems

The spokes are what users do:

-

Shop and pay

-

Chat and share

-

Book rides or deliveries

-

Pay bills

-

Access financial products

When the hub is strong, new spokes are easy to add. That is why mini apps matter so much. Google’s web.dev explains super apps as hosts for mini apps, with WeChat and Alipay as major examples.

Mini Apps And Mini Programs: The Growth Engine

Mini apps are lightweight services that live inside the host app. Users do not install a separate application. They access it through the super app’s interface and identity.

This helps the platform scale in two ways:

-

It adds many services without rebuilding each from scratch.

-

It gives third parties a distribution channel inside a high-traffic environment.

In WeChat’s ecosystem, mini programs are a well-known implementation of this model.

Payments As The Glue

Payments do more than move money. They also reduce friction across everything else.

Once a wallet is trusted and widely accepted:

-

Checkout becomes a one-tap action.

-

Refunds and disputes can stay inside the platform.

-

Loyalty and rewards can be tied to spending.

-

Messaging becomes a commerce channel, not just a chat tool.

| Building Block | What It Does | Why It Matters |

|---|---|---|

| Identity | links a user to services | lowers sign-up friction |

| Wallet | enables payments everywhere | makes services “feel” connected |

| Messaging | keeps users inside | discovery + support flows |

| Mini apps | plug-in services | fast ecosystem growth |

Why Asia Produced The First Famous Super Apps

The super app story is often told through Asia because several markets created the right mix of conditions:

-

High mobile usage

-

Strong QR payment adoption

-

Large platforms that already had daily engagement

-

Dense urban services like delivery and transport

-

Merchant networks that benefited from one payment layer

WeChat and Alipay became everyday infrastructure, not just apps. Tencent’s Weixin/WeChat has reached around 1.4 billion monthly active users, according to reporting on Tencent results.

Ant Group states that Alipay and partner e-wallets provide services for about 1.3 billion users worldwide.

This scale matters because it supports a self-reinforcing loop: more users attract more merchants and services, which attracts more users.

Why Many Western Markets Look Different

In many Western markets, the app ecosystem has stayed more specialized. Instead of one dominant “everything app,” you often see strong category leaders: a top messenger, a top marketplace, a top wallet, a top bank app.

One reason is regulatory and market structure. Policy work on BigTech finance in the EU highlights concerns like systemic risk, competition, data privacy, and cross-border oversight. Those issues can limit how far one platform can expand before it hits resistance.

Another reason is habit. If people already have strong defaults for chat, banking, and shopping, convincing them to merge those habits is hard.

| Factor | Asia-First Pattern | Common Western Pattern |

|---|---|---|

| Platform dominance | a few mega platforms | more fragmented leaders |

| Payments culture | QR + wallet normalization | cards and multiple wallets |

| Regulation focus | varies by country | heavier competition/privacy scrutiny |

| Consumer defaults | “one portal” behavior | best-of-breed apps |

Super App: Banking, Messaging, And Shopping As One Bundle

This is where the model becomes most powerful. The combination of banking features, messaging, and shopping is not random. Each part makes the other parts stronger.

-

Messaging drives daily opens.

-

Payments create trust and dependency.

-

Shopping creates monetization and merchant value.

Messaging As The Front Door

In a super app, messaging is not just talk. It becomes a layer for actions:

-

Order updates

-

Customer service

-

Social recommendations

-

Group buying

-

Merchant chats and support

The result is a tight loop: you discover something in chat, you buy it with the wallet, and you get updates in the same place.

Banking And Wallet Features That Lock In Trust

Many super apps move beyond payments into finance:

-

Stored value and bill pay

-

P2P transfers

-

Small loans or BNPL

-

Insurance offers

-

Savings tools

This is also where regulation starts to matter more, because financial services carry consumer-protection duties.

Shopping And Commerce: The Monetization Core

Shopping inside a super app can include:

-

Marketplaces

-

Food delivery

-

Local services

-

Digital subscriptions

Once commerce is integrated, the platform can build a full economic layer: merchants, payments, logistics, support, and advertising.

| Bundle Component | User Benefit | Platform Benefit |

|---|---|---|

| Messaging | fewer steps for support and updates | retention and engagement |

| Wallet/banking | faster payments and transfers | transaction volume |

| Shopping | convenience and unified tracking | fees, ads, merchant growth |

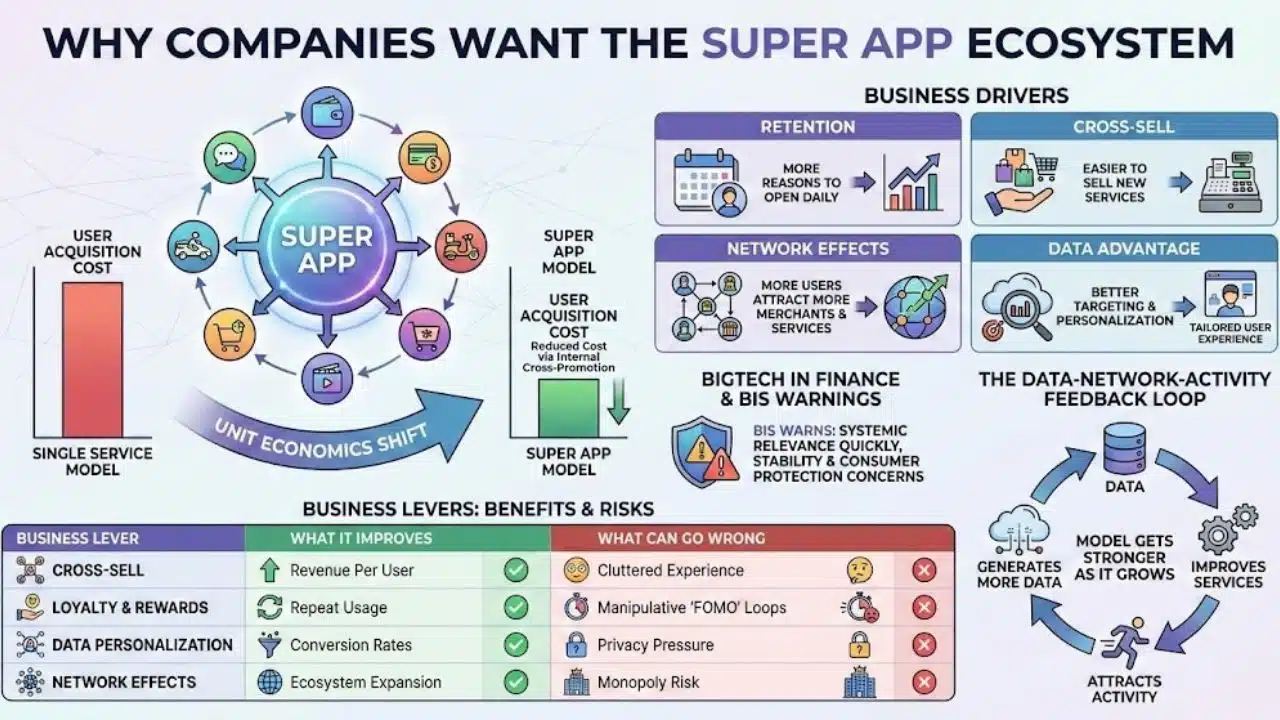

Why Companies Want The Super App Ecosystem

The super app model is attractive because it changes unit economics. It can reduce the cost of acquiring users for each new service, because the platform can cross-promote inside its own walls.

Here are the main business drivers:

-

Retention: more reasons to open the app daily

-

Cross-sell: easier to sell new services to existing users

-

Network effects: more users attract more merchants and services

-

Data advantage: better targeting and personalization

When BigTech enters finance, the BIS has warned that large tech firms can become systemically relevant quickly in payments and finance, raising stability and consumer protection concerns.

BIS research also describes a “data-network-activity” feedback loop in BigTech finance, where data improves services, which attracts activity, which generates more data.

In plain terms, the model gets stronger as it grows.

| Business Lever | What It Improves | What Can Go Wrong |

|---|---|---|

| Cross-sell | revenue per user | cluttered experience |

| Loyalty and rewards | repeat usage | manipulative “FOMO” loops |

| Data personalization | conversion rates | privacy pressure |

| Network effects | ecosystem expansion | monopoly risk |

The Downsides: Privacy, Security, And Too Much Power In One App

A super app can make life simpler. It can also make risk bigger.

When one app becomes the center of communication and money movement, three problems become more serious: data concentration, single-point-of-failure security, and lock-in.

Privacy: One Profile To Rule Them All

A super app can see:

-

what you buy

-

when you buy

-

where you buy

-

who you message

-

what you browse inside the ecosystem

Not every platform uses data the same way. But the potential is there, which is why privacy rules and trust become central.

The European Central Bank’s digital euro project emphasizes “privacy by design” as a core focus, aiming for very high privacy standards for electronic payments.

Even outside CBDCs, that framing signals how important privacy is becoming in modern payment systems.

Security: A Bigger Blast Radius

If a bad actor takes over your account, the damage can spread:

-

identity fraud

-

access to messages

-

access to purchase history and saved cards

-

impersonation inside the ecosystem

This is why strong authentication, monitoring, and dispute resolution are not optional for super apps. They are the foundation.

Competition And Lock-In

A super app can also make it harder for smaller apps to compete. If the platform controls distribution, payments, and discovery, partners may depend on it.

EU policy analysis on BigTech finance lists competition and market concentration among key concerns, alongside data protection and operational resilience.

| Risk | What It Means | What Helps |

|---|---|---|

| Data concentration | deeper profiling, higher stakes | strict controls and transparency |

| Single-point failure | one hack can affect “everything” | MFA, fraud detection, recovery |

| Lock-in | hard to switch platforms | portability and interoperability |

Regulation And Compliance: The Layer That Makes Or Breaks A Super App

Once a super app touches banking, payments, lending, or insurance, it enters regulated territory. That changes everything.

Common regulatory themes include:

-

KYC and identity verification

-

AML and fraud prevention

-

Consumer protection and disputes

-

Data protection and cross-border data

-

Operational resilience and cybersecurity

-

Competition and systemic risk

An IMF note on BigTech in financial services argues that regulation may need hybrid approaches combining entity-based and activity-based oversight, and it stresses cross-border cooperation.

BIS materials on BigTech finance discuss how BigTechs can become systemically important quickly and why public policy must balance benefits and risks.

This matters because the super app model tends to cross sectors. It is not just “finance” or “tech.” It is both.

| Regulatory Issue | What Regulators Want | What Platforms Want |

|---|---|---|

| KYC/AML | safer financial system | less friction in onboarding |

| Data protection | control and consent | personalization and targeting |

| Operational resilience | fewer outages and cyber risks | speed and iteration |

| Competition | prevent abuse of dominance | network effects and scale |

What Consumers Actually Want From A Super App

People do not adopt a platform because it has 40 features. They adopt it because it solves a daily problem with fewer steps.

The most common “jobs to be done” look like this:

-

Pay fast

-

Get support fast

-

Track orders clearly

-

Send money to friends easily

-

Find trusted merchants

-

Keep records in one place

At the same time, many users reject super apps when they become:

-

confusing

-

spammy

-

full of forced bundles

-

unclear on fees

-

aggressive with notifications

A good super app feels like a clean city. A bad one feels like a crowded market where everyone is shouting.

| Adoption Driver | Why It Works | What Can Ruin It |

|---|---|---|

| One-tap payments | removes checkout friction | hidden charges |

| Unified support | solves problems in one place | slow dispute handling |

| Clear navigation | reduces cognitive load | feature overload |

| Trust signals | users feel safe | scams and account takeovers |

The Competitive Landscape In 2026: Everything App Vs Super-ish Apps

Not every market ends with one dominant “everything app.” In many places, what grows instead is a set of “super-ish” platforms that each cover a big vertical.

Common models you see:

-

Full super app: messaging + wallet + mini apps at scale

-

Vertical super app: finance-first, commerce-first, or mobility-first

-

Partnership hub: integrated experiences via partnerships and APIs

The “mini app” idea is also gaining attention outside Asia as web developers look at mini apps and super apps as a platform pattern.

What decides the winner?

-

Distribution power

-

Merchant network strength

-

Payment acceptance

-

Regulatory fit

-

Trust and safety execution

| Model | Strength | Weakness |

|---|---|---|

| Full super app | maximum convenience | highest regulatory and trust burden |

| Vertical super app | clear value in one domain | less universal |

| Partnership hub | flexibility across brands | weaker control and consistency |

Implementation Blueprint: How A Super App Gets Built

Most “super app” attempts fail because they try to bundle too much too early. A realistic build path is staged.

Phase 1: Win A Daily Habit

Pick one core:

-

messaging

-

transport

-

payments

-

commerce

If users do not open the app daily or weekly, the rest will not stick.

Phase 2: Build Identity And Wallet

This phase is heavy work:

-

authentication

-

fraud controls

-

support systems

-

dispute resolution

-

compliance workflows

Phase 3: Add Commerce And Services

Now the platform can layer services:

-

marketplace

-

food delivery

-

bill pay

-

travel booking

-

partner services

Phase 4: Open The Mini App Ecosystem

This is the multiplier step. It brings third parties inside.

Mini app systems require:

-

developer tools

-

review and approval

-

security controls

-

business rules and revenue sharing

| Phase | What You Build | What Success Looks Like |

|---|---|---|

| 1 | daily hook | high retention |

| 2 | wallet + trust | low fraud + high completion |

| 3 | core services | growing transaction volume |

| 4 | mini apps | strong partner ecosystem |

Future Outlook: Will The Super App Become Normal Everywhere?

The future is not one path. It is likely several, depending on regulation, market habits, and platform power.

Here are three realistic scenarios.

Scenario A: One Dominant Portal Per Market

This can happen where:

-

a messenger already dominates

-

merchants accept one wallet widely

-

the platform earns strong trust

Scenario B: Several Competing Super-ish Platforms

This is likely where:

-

regulators push competition

-

consumers already use strong category leaders

-

banks and wallets remain competitive

Scenario C: Interoperability Creates “Super App Convenience” Without One Super App

This is the ideal many policymakers want:

-

easy switching

-

data portability

-

payments that work across networks

-

fewer walled gardens

In payments and finance, policy debates often revolve around this exact tension: convenience vs concentration.

| Scenario | What Users Get | Main Tradeoff |

|---|---|---|

| One dominant app | extreme simplicity | concentration risks |

| Several super-ish apps | choice and specialization | some friction |

| Interoperability | control and portability | slower rollout and standards work |

Final Thoughts: What The Super App Trend Really Means

The super app is not just a product idea. It is a shift in how digital life gets organized.

When banking features, messaging, and shopping sit in one place, daily tasks can feel easier. People switch apps less. Payments become natural. Customer support gets faster when it works.

But the risks also grow. BigTech can become systemically important in payments and finance, and public institutions have warned about consumer protection, stability, and data privacy as these models scale.