In a major development for global energy markets, OPEC+, the extended alliance of the world’s top oil-exporting nations, has announced that eight of its member countries will increase crude oil production by a combined 547,000 barrels per day beginning in September 2025. This marks a pivotal shift in the group’s strategy, as the alliance moves to terminate voluntary production cuts earlier than originally scheduled.

The decision came after a virtual meeting on Sunday, where leading oil producers—Saudi Arabia, Russia, Iraq, the United Arab Emirates, Kuwait, Kazakhstan, Algeria, and Oman—agreed to phase out their self-imposed output cuts, which were initially intended to remain in place until September 2026.

Voluntary Production Cuts Reversed Ahead of Schedule

The eight countries involved had been part of a broader OPEC+ policy introduced in November 2023, aimed at stabilizing global oil prices in response to demand fluctuations and macroeconomic uncertainty. These voluntary cuts were seen as a temporary safeguard to support higher prices during periods of lower demand.

However, current conditions—including a steadier global economic outlook, declining oil inventories, and increasing pressure to maintain market share—have prompted the coalition to recalibrate. The September 2025 production hike will follow a similar move from the previous month, when OPEC+ boosted output by 548,000 barrels per day in August.

This trend indicates a more assertive return to supply-side expansion in response to market fundamentals.

Oil Prices Hold Firm Despite Output Increase

Although increased supply often triggers lower oil prices, the immediate reaction from the market has been relatively muted. Brent crude, the global benchmark for oil prices, has remained stable—trading near $70 per barrel. WTI crude also hovered around $67–$68, reflecting cautious optimism among traders.

Several factors are contributing to price stability:

-

Geopolitical uncertainties, particularly involving Russian oil exports

-

A sharp build-up in Chinese oil inventories, suggesting large-scale stockpiling

-

Continued demand in regions like India, the U.S., and parts of Asia

Despite these offsetting trends, analysts warn that any unexpected disruption—such as sanctions or supply bottlenecks—could quickly tighten the market and push prices upward again.

Geopolitics in Play: Russia Sanctions and Global Energy Stability

A key geopolitical risk influencing OPEC+ decisions involves U.S. policy toward Russia. The Biden administration has signaled it may move forward with secondary sanctions on countries that continue purchasing Russian oil, should Moscow fail to make progress on peace negotiations with Ukraine by August 7, 2025.

These measures could include restrictions on financial transactions and logistics services used to transport Russian oil to third-party nations. Countries like India, which remain among the top buyers of discounted Russian crude, are under diplomatic pressure to reconsider their energy trade strategies.

Should such sanctions be enacted, the global oil supply chain could face severe disruptions, further complicating OPEC+ efforts to stabilize prices through production increases.

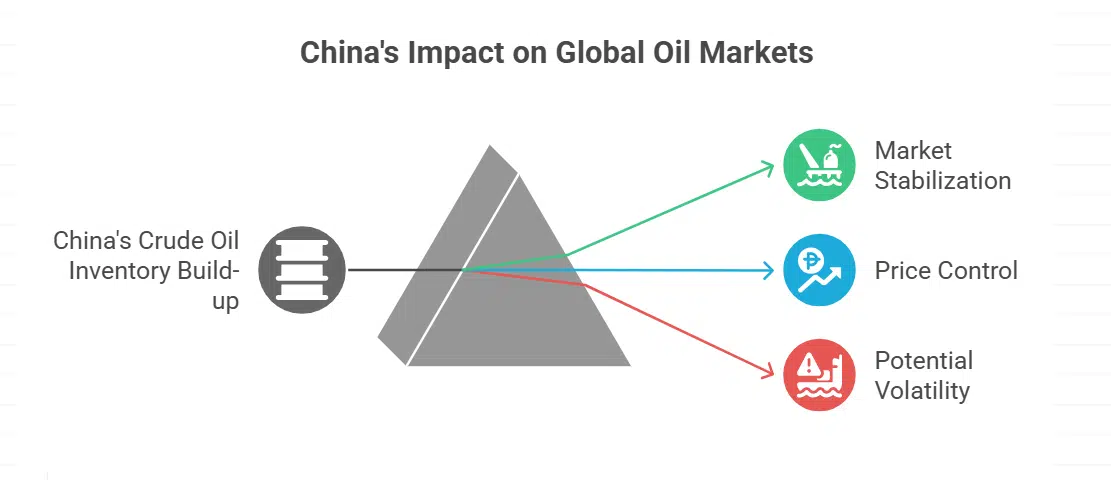

China’s Role: Strategic Stockpiling and Market Buffering

Another significant factor influencing market behavior is China’s crude oil inventory build-up. Over the past few months, Chinese state-run refineries and storage facilities have absorbed excess oil through aggressive purchasing at favorable rates. This surge in imports has allowed China to buffer global supply changes and avoid price spikes domestically.

As a result, even though production is increasing globally, China’s demand and storage capacity are acting as stabilizing forces. However, if China’s import behavior shifts or slows due to domestic economic constraints, oil markets could see renewed volatility.

IEA and Industry Warnings: Surplus Risk Ahead

While OPEC+ aims to balance the market, the International Energy Agency (IEA) has issued forecasts suggesting the possibility of a global oil surplus by the end of 2025. Current IEA data indicates a potential oversupply of 500,000 to 600,000 barrels per day, largely driven by:

-

Weak demand recovery in Asia

-

Strong output growth from non-OPEC producers like the U.S., Canada, Brazil, and Guyana

-

Stable production from OPEC+, even after phasing out voluntary cuts

The IEA has urged oil-producing nations to remain flexible and ready to scale back output again if demand weakens or inventories swell.

The latest production move confirms a growing trend within OPEC+: a pivot from defending price levels to protecting market share. In the face of rising competition from U.S. shale producers and increased exports from Latin America, several key OPEC+ members are reasserting their position in global markets.

This strategy reflects internal concerns that maintaining high prices for too long could encourage competitors and reduce the group’s long-term relevance in setting oil benchmarks. By increasing output gradually, OPEC+ aims to remain central to energy supply discussions while keeping prices at a level that supports economic growth without inviting excessive new production elsewhere.

Next Steps: September 7 Meeting Could Shift Outlook Again

OPEC+ will reconvene on September 7, 2025, to review global oil market trends and reassess its output policy. During that meeting, members are expected to evaluate:

-

The impact of the current supply increase

-

Ongoing developments in the Russia-Ukraine conflict and U.S. sanctions

-

Chinese and Indian energy demand levels

-

Price movements and refinery margins globally

The group has left the door open to pause or reverse the production hikes should market conditions deteriorate or geopolitical risks escalate.

Impact on Consumers: Will Gasoline Prices Fall?

The most immediate concern for many consumers is whether this production increase will lower gasoline and diesel prices. While global oil prices are one component of fuel pricing, other factors—like refining costs, transportation logistics, and local taxes—play a significant role.

Still, with additional crude supply entering the market, there is a possibility that fuel prices may stabilize or decline slightly in the coming weeks, assuming no major supply shocks occur.

However, if geopolitical tensions escalate or refinery capacity fails to keep up with demand, those benefits could be limited.

A Balancing Act with Global Implications

The OPEC+ decision to increase oil production in September marks a significant shift in global energy strategy. As the group walks a tightrope between supporting economic recovery and protecting market relevance, its actions will continue to shape the landscape of oil prices, supply security, and geopolitical alliances.

The early reversal of voluntary cuts signals confidence in the market’s resilience—but with ongoing risks tied to sanctions, demand shifts, and regional instability, the path ahead remains far from predictable.