Purchasing car insurance is a crucial decision that safeguards you against unforeseen expenses, legal issues, and the unexpected challenges of being on the road. While the process might seem straightforward, there are several mistakes to avoid when buying car insurance that can cost you more in premiums, leave you underinsured, or result in claim denials when you need coverage the most.

These mistakes often stem from rushing through the process, overlooking essential details, or failing to align your policy with your specific needs.

By understanding these pitfalls and how to avoid them, you can confidently navigate the complexities of car insurance. This guide highlights the most common mistakes to avoid when buying car insurance, providing actionable tips to help you make informed choices, save money, and secure the protection you deserve.

10 Common Mistakes to Avoid When Buying Car Insurance

When purchasing car insurance, it’s vital to be aware of the most common mistakes to avoid when buying car insurance. By steering clear of these errors, you can ensure you get the best coverage for your needs.

1. Skipping Research and Comparison

Why It Matters:

Neglecting to compare car insurance policies can result in overpaying for coverage or missing out on better options. Insurance providers offer diverse rates and benefits, and selecting the first policy you encounter may not be cost-effective.

Solution:

Invest time in researching and comparing policies from multiple insurers. Utilize online comparison tools to evaluate premiums, coverage options, and customer reviews. This approach ensures you select a policy that aligns with your needs and budget.

At-a-Glance Comparison:

| Insurer | Annual Premium | Coverage Options | Customer Rating |

| Insurer A | $1,200 | Full, Liability | 4.5/5 |

| Insurer B | $1,100 | Full, Liability | 4.2/5 |

| Insurer C | $1,300 | Full, Liability | 4.8/5 |

Key Takeaway:

Conduct thorough research and comparisons to ensure you obtain the best value for your car insurance.

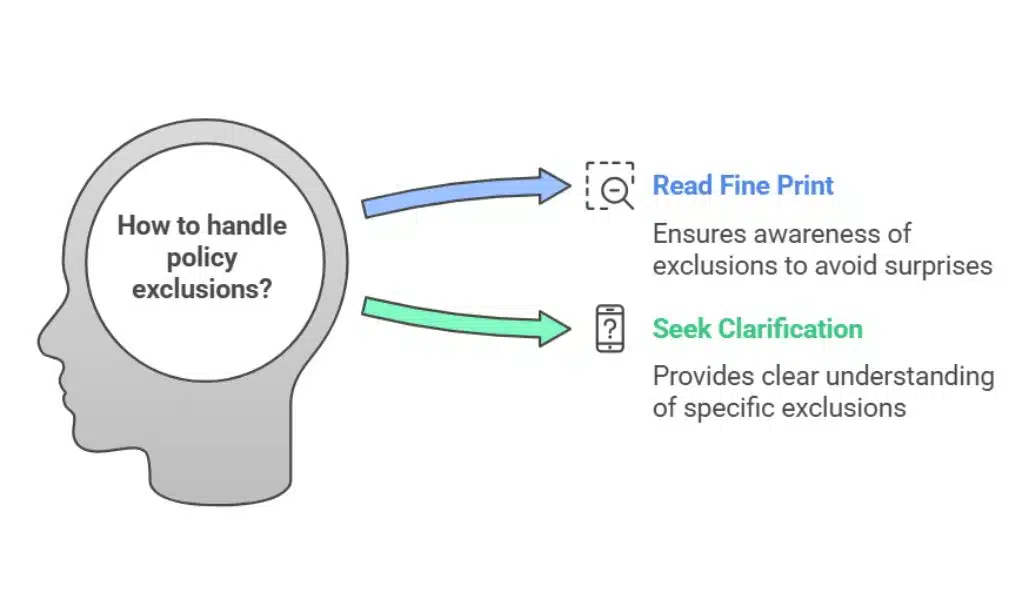

2. Ignoring Policy Exclusions

Why It Matters:

Focusing solely on what a policy covers while overlooking exclusions can lead to denied claims when you need coverage the most. Understanding what is not covered is essential to avoid unexpected financial burdens.

Solution:

Carefully read the policy’s fine print and seek clarification from your insurer regarding exclusions. Common exclusions may include damages from intentional acts, unapproved vehicle modifications, or driving under the influence.

Common Exclusions Overview:

| Coverage Type | Common Exclusions |

| Collision | Driving while intoxicated |

| Comprehensive | War-related damages |

| Liability | Intentional harm to others |

Key Takeaway:

Understanding policy exclusions upfront helps prevent unexpected financial liabilities.

3. Choosing the Cheapest Option Without Considering Coverage

Why It Matters:

Opting for the least expensive policy without evaluating coverage details can leave you underinsured. While saving money is important, inadequate coverage may result in significant out-of-pocket expenses during a claim.

Solution:

Assess your specific needs and balance cost with adequate coverage. Determine whether you require full coverage, which includes both collision and comprehensive insurance, or if liability-only coverage suffices.

Coverage Options Comparison:

| Policy Type | Annual Premium | Coverage Details |

| Liability Only | $800 | Covers damages to others’ property |

| Full Coverage | $1,200 | Includes liability and your car’s damage |

Key Takeaway:

Avoid compromising on essential coverage for a lower premium; prioritize your protection.

4. Failing to Review Coverage Needs Annually

Why It Matters:

Your insurance needs can change over time due to life events, new vehicles, or moving to a different state. Failing to review your policy annually may result in overpaying for unnecessary coverage or lacking necessary protection.

Solution:

Schedule an annual review of your car insurance policy to ensure it aligns with your current needs. Key changes to consider include:

- Adding or removing drivers

- Adjusting coverage limits

- Accounting for new life events, such as marriage or relocation

Example of Coverage Adjustments:

| Year | Coverage Adjustments | Reason |

| 2022 | Added comprehensive coverage | New car purchase |

| 2023 | Increased liability limits | Relocation to busy city |

Key Takeaway:

Regularly reviewing your policy ensures it evolves with your needs and avoids unnecessary costs.

5. Misunderstanding Deductibles

Why It Matters:

Deductibles are the out-of-pocket expenses you must pay before your insurance kicks in. Choosing a deductible that is too high can strain your finances during a claim, while a low deductible may lead to higher premiums.

Solution:

Select a deductible that balances affordability with manageable out-of-pocket costs. Evaluate your financial situation to determine the right balance.

Deductible vs. Premium Comparison:

| Deductible Amount | Monthly Premium | Out-of-Pocket Cost in Claim |

| $250 | $120 | $250 |

| $500 | $90 | $500 |

| $1,000 | $70 | $1,000 |

Key Takeaway:

Choose a deductible that you can comfortably afford in the event of a claim, without overstretching your budget.

6. Overlooking Discounts

Why It Matters:

Many drivers miss out on potential savings by not inquiring about discounts. Insurance providers often offer discounts for safe driving, bundling policies, or having vehicle safety features.

Solution:

Ask your insurer about available discounts and how to qualify for them. Some common discounts include:

- Good driver discounts

- Multi-policy discounts (e.g., bundling home and auto insurance)

- Discounts for installing safety features like anti-theft devices

Example of Common Discounts:

| Discount Type | Savings Potential |

| Safe Driver | 10-20% |

| Multi-Policy | 15-25% |

| Good Student | 10-15% |

Key Takeaway:

Take advantage of discounts to lower your premium without compromising on coverage.

7. Providing Incorrect Information

Why It Matters:

Submitting inaccurate information on your insurance application can lead to policy cancellation or claim denial. Honest mistakes or intentional omissions may result in significant financial consequences.

Solution:

Double-check your application to ensure all information is accurate, including:

- Your vehicle’s make and model

- Annual mileage

- Your driving history

Consequences of Incorrect Information:

| Type of Inaccuracy | Possible Consequences |

| Incorrect mileage | Claim denial |

| Undisclosed accidents | Increased premiums |

| Wrong vehicle details | Policy cancellation |

Key Takeaway:

Provide accurate information to avoid complications and ensure your policy is valid when you need it most.

8. Not Understanding State Requirements

Why It Matters:

Every state has unique car insurance requirements. Failing to meet these minimum standards can result in fines, license suspension, or being underinsured in the event of an accident.

Solution:

Research your state’s specific requirements for minimum coverage levels and ensure your policy meets them. For instance:

- Liability coverage minimums may vary by state

- Some states require uninsured/underinsured motorist coverage

State Requirements Overview:

| State | Minimum Liability Coverage |

| California | $15,000/$30,000/$5,000 |

| Texas | $30,000/$60,000/$25,000 |

| Florida | $10,000/$20,000/$10,000 |

Key Takeaway:

Stay informed about your state’s insurance laws to avoid legal and financial issues.

9. Ignoring Customer Reviews and Ratings

Why It Matters:

Selecting an insurer with poor customer service or slow claims processing can lead to frustration and delays during critical moments.

Solution:

Research online reviews and ratings from reliable sources, such as J.D. Power or the Better Business Bureau, to gauge an insurer’s reliability and customer satisfaction.

Insurer Ratings Snapshot:

| Insurer | Claims Processing Rating | Customer Service Rating |

| Insurer A | 4.5/5 | 4.3/5 |

| Insurer B | 3.8/5 | 3.9/5 |

Key Takeaway:

Choose an insurer with a strong reputation for customer service and claims handling.

10. Waiting Too Long to File a Claim

Why It Matters:

Delaying a claim can complicate the process and potentially result in claim denial. Prompt action ensures smoother resolution and faster payouts.

Solution:

File claims as soon as possible after an incident. Collect necessary documentation, such as photos, witness statements, and police reports, to support your claim.

Filing Timelines:

| Incident Type | Recommended Filing Time |

| Accident | Within 24-48 hours |

| Theft | Immediate |

| Weather damage | As soon as safe to report |

Key Takeaway:

Act promptly to ensure your claim is processed efficiently and without unnecessary delays.

Takeaways

Making informed decisions about car insurance requires an understanding of the common mistakes to avoid when buying car insurance. These mistakes, whether it’s skipping comparisons, underestimating your coverage needs, or neglecting exclusions, can have lasting financial and legal implications. Fortunately, with the right approach, you can easily sidestep these pitfalls.

By taking the time to research policies thoroughly, understanding your specific needs, and asking the right questions, you can secure the right coverage at a fair price. Remember, car insurance isn’t just about fulfilling a legal requirement—it’s about protecting yourself, your vehicle, and your financial well-being. Avoiding the mistakes to avoid when buying car insurance ensures you have peace of mind and confidence every time you hit the road.