Personal injury claims in Australia can be complex, and many claimants are unaware of the legal loopholes that can affect their compensation.

While the legal system aims to protect injured individuals, insurance companies and defendants often exploit these loopholes to minimize payouts.

Understanding these legal intricacies can help you avoid costly mistakes and secure the compensation you deserve.

This article will explore 10 legal loopholes that can affect your personal injury case in Australia, explaining how they impact claims and what steps you can take to protect your rights.

What Are Legal Loopholes?

Legal loopholes are technicalities or ambiguities within the law that may be used to challenge or diminish a personal injury claim.

These loopholes can arise due to legislative gaps, legal interpretations, or procedural oversights. Sometimes, claimants unknowingly fall into these traps, jeopardizing their case and significantly reducing their compensation.

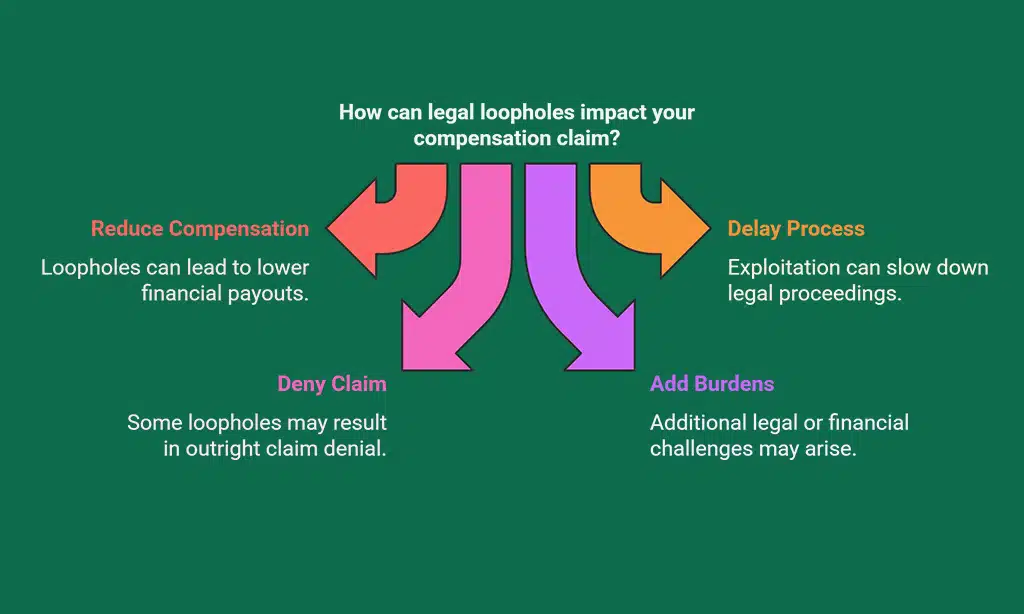

How Loopholes Can Impact Your Compensation Claim

When insurance companies or opposing parties exploit these loopholes, they can:

- Reduce the compensation you receive

- Delay the legal process

- Deny your claim entirely

- Put additional legal or financial burdens on the claimant

Understanding these legal nuances is crucial to navigating the claims process successfully. Being aware of potential loopholes allows you to proactively mitigate risks and strengthen your case.

10 Legal Loopholes That Can Affect Your Personal Injury Case in Australia

Legal loopholes can often go unnoticed, leaving personal injury victims vulnerable to tactics used by insurance companies and opposing parties.

By being aware of these loopholes, you can take proactive steps to ensure that your claim is not unfairly dismissed or undervalued.

Some loopholes revolve around legal timeframes, evidentiary requirements, and even settlement agreements that may limit your future legal rights.

Let’s explore some of the most common legal loopholes and how they can impact your case.

1. Statute of Limitations Restrictions

The statute of limitations dictates how long you have to file a personal injury claim. Missing the deadline could result in losing your right to compensation.

Many claimants mistakenly believe they have unlimited time to file their claim, only to find out later that their case is time-barred.

How Long Do You Have to File a Claim?

Different types of personal injury cases have varying time limits across Australian states.

| Claim Type | Time Limit | State Variations |

| General personal injury | 3 years | Varies by state |

| Workplace injury | 6 months – 3 years | Depends on jurisdiction |

| Motor vehicle accidents | 6 months – 3 years | Subject to state law |

| Medical negligence | 3 years | With some exceptions |

Exceptions and Extensions

Some exceptions allow claims beyond standard limits, such as cases involving minors, delayed injury discovery, or mental incapacity.

Seeking legal advice early ensures you do not miss deadlines that can make or break your case.

2. Pre-Existing Medical Conditions and Their Impact

Insurance companies often argue that your injury was pre-existing rather than caused by the accident.

This tactic is frequently used to dispute claims and reduce payouts. If they can successfully prove that your injury was not directly linked to the incident, they may reject or minimize your compensation.

How Insurers Use Pre-Existing Injuries Against You

- Denying claims by attributing pain to old injuries

- Reducing payouts by arguing that injuries were inevitable

- Demanding extensive medical history to find unrelated past injuries

Ways to Strengthen Your Medical Evidence

- Obtain detailed medical reports from specialists

- Seek expert opinions to confirm the link between the accident and your injury

- Maintain consistent medical treatment records and follow all prescribed treatments

| Key Action | Benefit |

| Documenting all medical visits | Establishes continuity of treatment |

| Consulting independent medical experts | Provides unbiased injury assessment |

| Keeping a personal pain diary | Strengthens subjective claims |

3. Contributory Negligence Rules

If you are found partially responsible for your accident, your compensation may be reduced.

Many claimants are unaware that even minor actions, such as not wearing a seatbelt or failing to take immediate medical treatment, can be used to claim contributory negligence.

What Is Contributory Negligence?

Australian law allows insurers to argue that the injured party was negligent, which can lead to shared liability. Courts then determine how much of the blame is assigned to each party.

How It Can Reduce Your Compensation

Your payout can be reduced in proportion to your level of fault. For example:

| Your Fault (%) | Compensation Reduction (%) |

| 20% | 20% |

| 50% | 50% |

| 75% | 75% |

To avoid this, collect strong evidence proving the other party’s liability. Dashcam footage, eyewitness testimonies, and professional accident reconstruction reports can be crucial.

4. Employment Status and Workers’ Compensation Confusion

Your work status can determine whether you’re eligible for workers’ compensation. Many employers misclassify workers as independent contractors to avoid paying compensation, leaving them without coverage in the event of an injury.

Are You Covered as an Independent Contractor?

- Employees are entitled to workers’ compensation benefits.

- Independent contractors may need to pursue claims through public liability insurance or lawsuits.

Employer Tactics to Deny Claims

- Misclassifying employees as contractors

- Claiming the injury occurred outside of work hours

- Failing to report the injury to insurers on time

| Work Status | Entitled to Compensation? |

| Full-time Employee | Yes |

| Casual Worker | Yes, under certain conditions |

| Independent Contractor | No, unless covered under a policy |

5. Gaps in Medical Treatment Records

Inconsistent medical records can significantly weaken your case, providing insurers with strong grounds to dispute your claim.

When your medical history lacks continuity, insurers may argue that your injuries were not severe or that they resulted from pre-existing conditions rather than the accident in question.

Why Delayed Treatment Can Harm Your Case

- Raises suspicion about injury severity

- Allows insurers to claim the injury wasn’t serious

- Provides a reason to deny or undervalue claims

How to Ensure Proper Medical Documentation

- Seek immediate medical attention after an injury

- Maintain a consistent treatment record

- Document all medical expenses and obtain receipts

| Key Mistake | How It Affects Your Case |

| Delaying treatment | Suggests the injury wasn’t severe |

| Missing medical appointments | Weakens credibility |

| Not following prescribed treatment | Reduces claim value |

6. Misinterpretation of No-Fault vs. Fault-Based Claims

Understanding the difference between no-fault and fault-based compensation is crucial. Many claimants assume they will receive compensation regardless of fault, only to realize later that their claim requires proof of negligence.

Differences Between No-Fault and Fault-Based Systems

- No-fault: Compensation available regardless of fault (e.g., some motor vehicle injury schemes)

- Fault-based: Requires proving liability (e.g., general personal injury claims)

When You Can Still Claim Under a Fault-Based System

If your case is denied under a no-fault system, a fault-based lawsuit may still be an option. Legal representation can help determine whether pursuing a different claim is possible.

| Claim Type | Fault Required? |

| No-Fault Claims | No |

| Fault-Based Claims | Yes |

7. Lack of Proper Legal Representation

Handling a claim without legal guidance can put you at a disadvantage. Many victims believe they can navigate the legal system alone, only to discover they are missing critical evidence or have accepted an unfair settlement.

Risks of Handling a Claim Without a Lawyer

- Lower compensation offers

- Difficulty navigating legal loopholes

- Increased risk of claim denial

What to Look for in a Personal Injury Lawyer

- Experience in Australian personal injury law

- No-win, no-fee representation

- Positive client testimonials and track record

| Key Factor | Why It Matters |

| Experience | Ensures knowledge of local laws |

| No-Win, No-Fee | Reduces financial risk for claimants |

| Client Reviews | Provides insight into past successes |

8. Insufficient Evidence to Prove Liability

Lack of solid evidence can significantly weaken your case, making it easier for insurers to challenge your claim.

Without proper documentation, insurers may argue that your injuries are exaggerated or unrelated to the incident, thereby reducing or outright denying compensation.

This is particularly common in cases where there is a delay in seeking medical treatment or when there is inconsistent testimony from witnesses.

Crucial Evidence That Strengthens Your Case

- Witness statements

- CCTV footage

- Medical records

- Police reports

Using Expert Witnesses for Support

Experts such as accident reconstruction specialists can strengthen your claim.

| Type of Evidence | Importance |

| Medical Reports | Proves extent of injury |

| Witness Statements | Supports your version of events |

| CCTV Footage | Provides indisputable proof |

9. Settlement Agreements with Hidden Clauses

Insurance companies may include unfair clauses in settlement agreements that significantly limit your ability to seek further compensation.

These clauses can be buried in complex legal language, making it difficult for an unrepresented claimant to recognize their long-term impact.

How Insurers Trick Victims with Lowball Offers

- Offering quick but inadequate settlements

- Pressuring victims to sign waivers

- Including clauses preventing future claims

Key Terms to Watch Out for in Settlement Contracts

- Waivers of future claims

- Confidentiality clauses restricting legal action

- Indemnity clauses shifting liability

| Settlement Term | What It Means |

| Waiver Clause | Prevents future claims |

| Indemnity Clause | Shifts liability away from insurer |

| Confidentiality Clause | Limits your ability to discuss case |

10. Failure to Consider Future Medical Costs

Failing to account for future expenses can leave you undercompensated, as medical conditions can deteriorate over time, requiring ongoing care and treatment.

Many injury victims accept settlements that do not cover long-term treatment, rehabilitation, or unexpected complications, resulting in financial hardship later.

Why You Need to Calculate Long-Term Expenses

- Chronic pain management

- Future surgeries or treatments

- Rehabilitation and physical therapy

How to Work with Experts for Accurate Projections

Medical professionals and financial experts can help assess long-term costs and ensure your settlement reflects all potential expenses.

| Expense Type | Estimated Cost |

| Future Surgeries | $10,000 – $50,000 |

| Long-term Therapy | $5,000 – $20,000 |

| Chronic Pain Care | $2,000 – $10,000 |

How to Protect Yourself from Legal Loopholes

Steps to Take After a Personal Injury in Australia

- Report the accident immediately

- Seek medical attention

- Document everything

- Consult a lawyer early

When to Consult a Lawyer for Your Case

Seeking legal advice before signing any documents can help avoid loopholes that impact your claim.

Takeaways

Understanding these 10 legal loopholes that can affect your personal injury case in Australia is essential for maximizing your compensation.

By knowing your rights, avoiding common pitfalls, and seeking professional legal advice, you can protect your claim and ensure a fair outcome.

If you’ve been injured, don’t let legal loopholes diminish your case. Speak to a qualified personal injury lawyer today to ensure your rights are upheld.