You’ve probably heard the saying: “Price is what you pay, value is what you get.” It may sound easy, yet to most investors, it is the most difficult thing to understand in the stock market. We watch the news, we view market trends, and make decisions in line with what others are doing. But here’s the uncomfortable truth: most investors are not even aware of what they are buying.

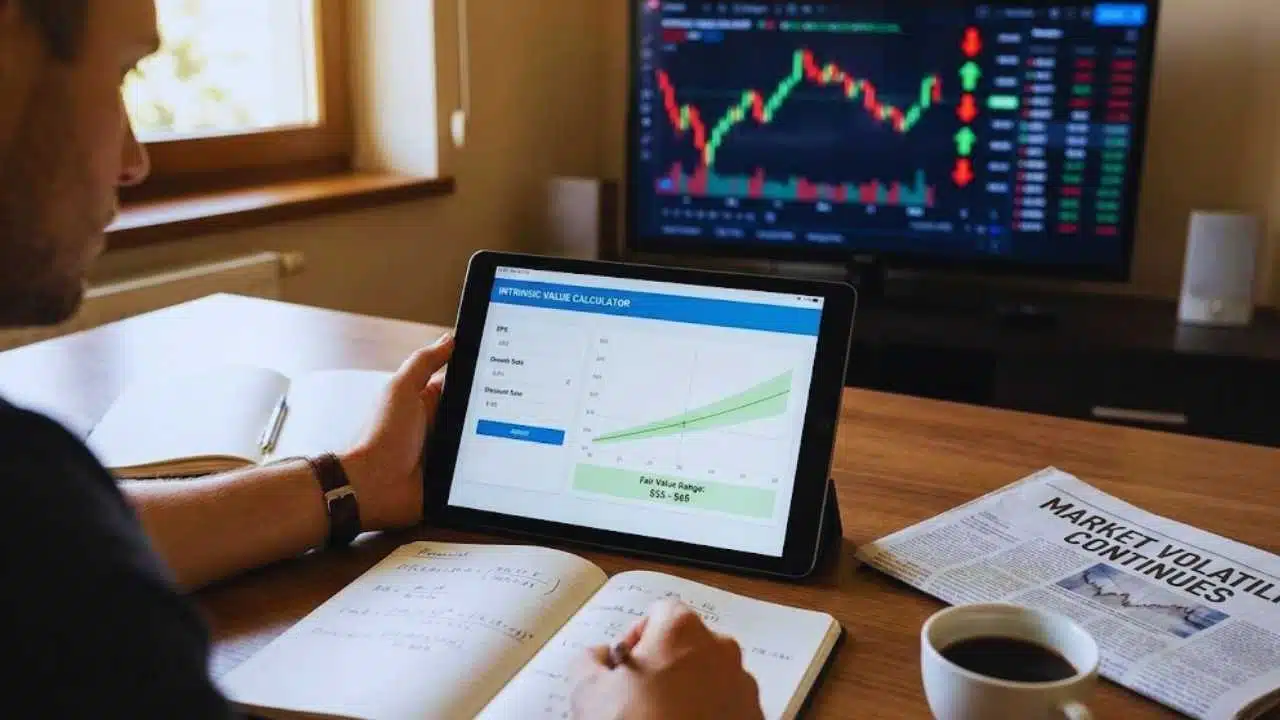

An intrinsic value calculator changes that dynamic completely. It’s not some complicated financial instrument reserved for Wall Street professionals. Rather, it’s a straightforward tool that helps you determine what a company is truly worth, separate from the noise and emotion of the market.

In this article, we won’t just teach you what intrinsic value is, but also tell you how intrinsic value calculator operates, how to use them in the real world of investing, and clarify why your calculations don’t need to be perfect to be useful.

Understanding Intrinsic Value and Its Importance

A good intrinsic calculator can only be utilized successfully once you have an understanding of what intrinsic value is. Intrinsic value refers to the actual economic value of an organization in terms of its capability to produce future cash flows. It is not what the market price provides today, which is usually driven by emotion, speculation, and short-term news cycles. Instead, intrinsic value is rooted in fundamentals.

Think about it this way: if you were buying a rental property, you wouldn’t just look at what similar properties were selling for. You would examine the rental earnings, repairs, cost of maintenance, occupancy, and demand in the long run.

You would work out what you would reasonably expect to make out of that investment in the long run. That is what an intrinsic value calculator does for stocks. It uses the profits of the company, estimates the growth, and identifies the value of those growth cash flows in today’s dollars.

How does an Intrinsic Value Calculator work?

An intrinsic calculator operates on the foundation of Benjamin Graham’s revised formula from 1974. The concept is elegant in its simplicity: it takes three critical pieces of information and combines them to estimate what a company is worth.

Benjamin Graham Formula (for intrinsic value)

Where:

EPS → Trailing 12-month earnings per share

8.5 → Base P/E ratio for a no-growth company (Graham’s assumption)

g → Expected annual growth rate (typically over 7–10 years)

4.4 → Yield of AAA corporate bonds in 1962 (the benchmark year Graham used)

Y → Current yield on AAA corporate bonds at the time of calculation

The formula asks one fundamental question: What is a reasonable price for me to pay today, given the future earnings this business will generate? The calculator takes your answer and transforms it from an abstract idea into a concrete number.

How these three components fit together:

| Component | What It Means | Why It Matters |

| Earnings Per Share (EPS) | What did the company earn per share over the past 12 months? | Establishes the company’s current earning power and profitability |

| Expected Growth Rate | How fast do you expect earnings to grow annually over the next 5-10 years? | Determines future earning potential; higher growth = higher valuation |

| Discount Rate | The return rate you require on your investment, adjusted for risk | Accounts for the time value of money and economic conditions |

The beauty of using an intrinsic value calculator is that it processes these inputs instantly and consistently. Manual calculations are also subject to error and are very time-consuming.

It is worth mentioning that this is not the only method of calculating intrinsic value. Various calculators adopt dissimilar models, including:

- Discounted cash flow,

- Dividend models, or

- Asset-driven valuation,

Based on the type of business and the investor’s preferences.

Using the Intrinsic Value Calculator in Real-World Scenarios

Real investment skill is developed when one knows how to apply the intrinsic calculator in real-life scenarios. Let’s walk through a realistic example that shows how this works in practice.

Example: Suppose you are considering a well-established dividend-paying corporation that is trading at $50 a share.

- You have established the trailing twelve-month earnings per share of the company at $4.

- You are assuming that it will increase earnings by 6% per year, as per its performance and competitive position.

- You decide that the discount rate will be 8% based on the present-day interest rates and the risk profile of the company.

When you plug these numbers into an intrinsic calculator, it returns an estimated value of about $60 per share. This implies the share is selling at about a 17% discount. However, this is where judgment matters; you need to evaluate whether the 6% growth assumption is realistic based on industry trends and previous performance.

Why Your Calculations Don’t Need to Be Perfect?

Many investors make a critical mistake: they obsess over getting the exact intrinsic value calculation. They believe the calculator should produce a precise number down to the penny. This misses the entire point of valuation analysis.

In reality, intrinsic value is best thought of as a range rather than a single number.

When your intrinsic value calculator gives a fair value of $60 with an acceptable range of $55 to $65, then the stock at $52 would appear attractive, but at $70 indicates over-valuation. The calculator provides directional guidance; it tells you whether you’re in the ballpark, not the exact spot.

This strategy is consistent with the margin of safety principle advocated by Graham. Rather than demanding perfect precision from the calculator, use it to identify when a stock offers sufficient downside protection.

An intrinsic value calculator transforms how you approach investing by replacing emotion with mathematics and guesswork with logic. It is a tool to enable you to differentiate between price and value, which is the biggest difference in the whole of investing.

The tool won’t predict the future perfectly, but it will help you think clearly, validate your assumptions, and identify opportunities when the market misprices good businesses. That’s not just a competitive advantage, it’s the foundation of long-term wealth creation.