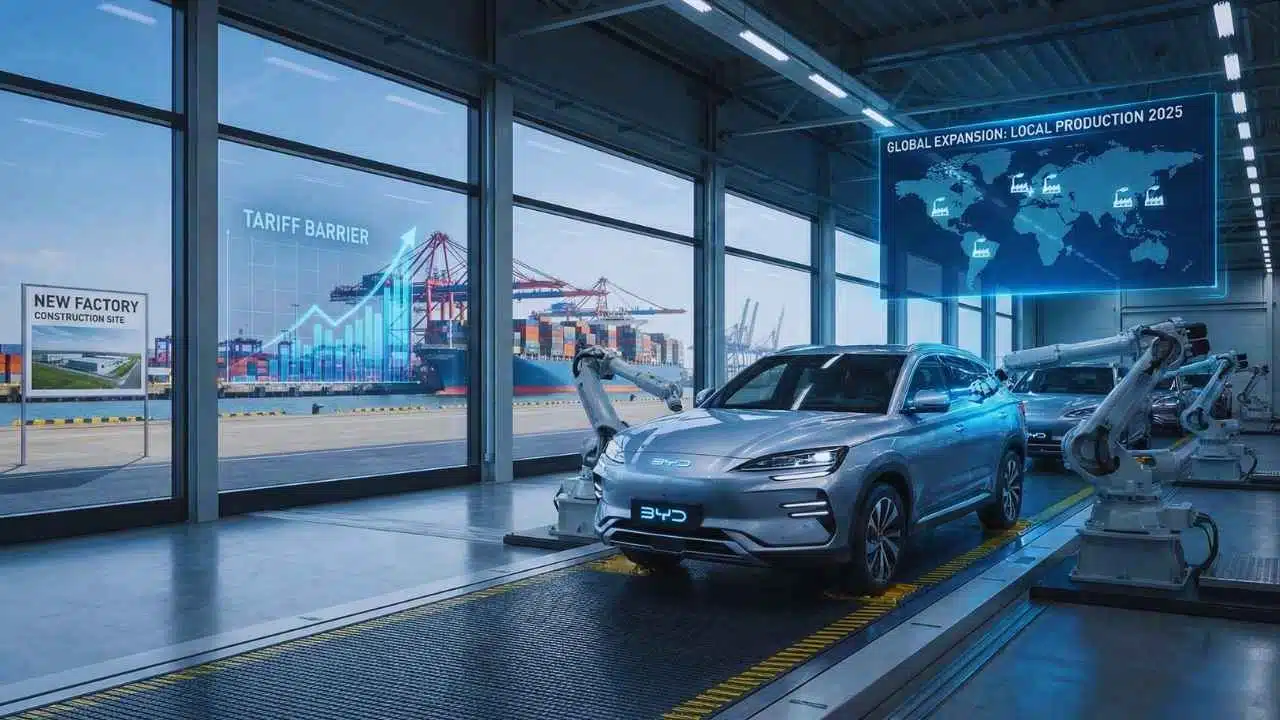

Chinese brands are scaling global sales in 2025 by boosting exports and building factories abroad as Europe and the Americas tighten tariffs, forcing a rapid shift from “ship cars” to “make cars locally.”

The New Export Wave Reshaping Global Car Sales

Chinese automakers entered 2025 with a clear global playbook: use strong export volumes to seed new markets, then expand sales networks and local operations once demand takes hold. That approach has accelerated because competition at home has intensified. In China, dozens of brands are fighting for the same customers, pushing down prices and making overseas growth more attractive for both revenue and brand visibility.

Exports have become the bridge between domestic scale and international market share. China’s outbound vehicle shipments rose again in 2024, reaching about 6.41 million vehicles, and the momentum showed how quickly Chinese manufacturers can redirect capacity toward foreign demand. The export boom matters in 2025 because it gives brands a pipeline of volume while they build longer-term assets like dealers, service centers, spare-parts logistics, and local assembly lines.

But the export story isn’t just about “more cars.” It’s also about what kinds of cars are leaving China. The export mix has been shifting toward electrified models—battery electric vehicles (BEVs), plug-in hybrids (PHEVs), and full hybrids—because Chinese firms have become highly competitive in battery supply chains, electronics integration, and fast model iteration. At the same time, many buyers in emerging markets still prefer gasoline or hybrid options because charging access remains uneven. That has pushed Chinese automakers to ship a broader portfolio than “EV-only,” including low-cost ICE vehicles, hybrids, and plug-in hybrids.

Another reason the export strategy is working: Chinese firms have expanded choice and speed. They often launch fresh models faster than legacy automakers and aggressively refresh interiors, infotainment, and driver-assist features. In markets where consumers are shopping by features-per-dollar, that matters as much as powertrain type.

Why China’s Export Surge Matters in 2025?

| Driver | What It Means | Impact on Global Competition |

| High production scale | Ability to supply multiple regions quickly | Faster market entry and rapid inventory ramp-up |

| Broad powertrain mix | EVs, PHEVs, hybrids, and ICE exports | More segments can be targeted, not just EV buyers |

| Cost advantages | Competitive pricing without stripping features | Pressure on incumbents to cut prices or add value |

| Faster model cycles | Quick launches and frequent updates | Keeps product line “new,” boosting showroom traffic |

Tariffs And Trade Barriers: The Rules Are Changing Mid-Game

As Chinese brands gained traction, governments responded with trade tools designed to protect domestic manufacturing and shape supply chains. In practice, 2025 is less about whether Chinese automakers can sell globally and more about how they can sell—especially where policy is tightening.

In Europe, trade measures have raised the cost of importing China-made BEVs. The policy direction signals that high-volume, low-price imported EVs will face stronger headwinds, and automakers must adapt by adjusting product mix, pricing, and sourcing. For Chinese brands, the immediate consequence is that relying on imports alone becomes less reliable for long-term growth in regulated markets.

In the Americas, policy is also shifting. Some markets introduced or increased tariffs on electrified vehicles to encourage local production, while others signaled broader import restrictions affecting vehicles from China and parts of Asia. These moves create real-world constraints: even if consumer demand is strong, import costs can erase pricing advantages quickly.

What makes 2025 particularly complex is that barriers aren’t uniform. Rules can vary by country and sometimes by product category (BEV vs PHEV vs hybrid) or even by the origin and subsidy classification of the vehicle. That forces automakers to operate like chess players: choosing which models to send where, when to prioritize hybrids over BEVs, and when to pivot to assembly outside China.

Chinese brands are responding in three practical ways:

- Rebalancing shipments toward regions with fewer barriers or faster approvals.

- Expanding hybrid and PHEV offerings in markets where full EV policy or charging support is less mature.

- Accelerating overseas production plans to turn “imported from China” into “built locally,” reducing tariff exposure.

Policy Pressure Points Influencing 2025 Strategy

| Region | Typical Policy Direction | What Automakers Must Do |

| Europe | Stronger import duties and scrutiny on China-made BEVs | Localize production and diversify sourcing |

| Latin America | Tariff schedules that rise over time in some markets | Move from imports to local assembly before tariffs peak |

| North America-adjacent trade hubs | Higher tariffs on certain Asian imports | Rethink pricing, supply chains, and market timing |

| Middle East & parts of Africa | Generally more open import environments | Use as growth markets and volume stabilizers |

From Exporting To Building: Overseas Plants Become the 2025 Growth Engine

Tariffs and policy volatility have turned overseas manufacturing into a strategic necessity rather than a “nice-to-have.” The key shift in 2025 is the move from a simple export model to a localization model—building cars, or at least assembling them, closer to the customer.

Localization doesn’t always mean building a full “end-to-end” plant immediately. Many automakers start with staged approaches:

- Dealer and service build-out to support early imports.

- Knock-down assembly (CKD/SKD) to reduce duties and create local jobs.

- Full manufacturing with deeper supplier localization once volumes justify it.

For Chinese automakers, overseas plants serve multiple goals at once:

- Tariff mitigation: local assembly can lower effective import penalties.

- Faster delivery: shorter shipping routes and better inventory control.

- Brand trust: local jobs and investment can improve acceptance.

- Policy resilience: domestic governments often prefer local production and may reward it with incentives or easier market access.

Brazil illustrates why timing matters. When a country sets a rising tariff schedule, brands that wait too long risk losing their price advantage. Building assembly capability before tariffs peak can preserve affordability and protect sales momentum.

Europe is a different kind of challenge. Localization there is less about basic assembly and more about meeting higher regulatory expectations, quality standards, consumer trust factors, and potential local-content requirements. That means Chinese automakers must invest not only in plants but also in engineering support, compliance teams, and after-sales infrastructure.

Meanwhile, partnerships are becoming a fast lane to global scale. Teaming with established players can unlock distribution, compliance knowledge, and manufacturing footprints faster than building everything from scratch. For Chinese automakers, partnerships also help in markets where consumer trust is still forming and where established networks matter.

What Localization Looks Like in Practice?

| Step | Investment Level | Typical Outcome |

| Dealer + service network | Medium | Builds customer confidence and reduces ownership anxiety |

| Parts and logistics hubs | Medium | Faster repairs and lower warranty friction |

| CKD/SKD assembly | Medium–High | Lower duties, local job creation, quicker scaling |

| Full manufacturing | High | Long-term tariff resilience and deeper market integration |

| Supplier localization | High | Cost stability, policy alignment, better margins |

Where Sales Are Growing Fastest: Europe, Latin America, Middle East, And Emerging Markets

Chinese automakers are not growing everywhere equally. In 2025, expansion is strongest where a combination of price sensitivity, EV adoption momentum, and open-to-competitive-imports policy creates room for new entrants.

Europe remains highly important because it is a prestige market: winning there can elevate a brand globally. Yet Europe is also where tariffs and regulatory scrutiny are most intense. Chinese brands are therefore focusing on clear value positions—strong feature sets, competitive financing, and model lineups that include not just BEVs but also plug-in hybrids where appropriate. They are also investing in brand-building: showrooms, marketing, and visible commitments to after-sales support.

Latin America is often driven by affordability and practical ownership costs. Here, the strongest opportunity is not only selling EVs but also selling electrified vehicles that fit real infrastructure—including hybrids and plug-in hybrids. Charging networks and grid reliability vary widely by country and even by city, so the “right product” is often the one that reduces fuel costs without requiring perfect charging access every day. That makes PHEVs and strong hybrids a natural fit for many buyers.

The Middle East has become a meaningful growth region because many countries have relatively open import environments, strong consumer demand for tech-forward vehicles, and premium segments that value features and design. Chinese automakers are also finding opportunity in fleet and ride-hailing channels, where total cost of ownership and vehicle uptime can matter more than brand legacy.

In parts of Africa and Southeast Asia, the story is about first-time car buyers, growing urbanization, and demand for durable, value-oriented vehicles. EV growth is present but uneven, so brands that bring a flexible lineup—efficient gasoline models, hybrids, and select EVs—often compete better than those relying on EV-only strategies.

Across these regions, two factors are decisive in 2025:

- After-sales readiness: buyers need confidence about repairs, warranty, and spare parts.

- Financing and pricing discipline: competitive sticker prices are not enough if financing costs are high or resale value is uncertain.

Chinese automakers are increasingly addressing these issues by expanding parts warehouses, training technicians, and building warranty programs designed for local conditions.

What Different Regions Want From Chinese Automakers in 2025?

| Market Type | What Buyers Prioritize | Product Strategies That Fit |

| Regulated, high-trust markets | Safety, reliability, compliance, resale value | Localization, strong warranties, proven quality |

| Price-sensitive growth markets | Value, fuel savings, durability | Hybrids/PHEVs, affordable trims, robust service |

| Tech-forward urban markets | Features, connectivity, design | High-spec interiors, advanced infotainment |

| Infrastructure-limited areas | Practical ownership, repairability | Efficient ICE/hybrids, simple serviceable platforms |

What Comes Next For Chinese Automakers Global Car Sales 2025?

The central theme of Chinese automakers global car sales 2025 is that growth is no longer just a volume game—it is an execution game. Export strength opened doors, but tariffs, local rules, and consumer expectations determine who stays and scales.

The winners in 2025 and beyond are likely to be the brands that can do five things consistently:

- Localize fast enough to reduce policy risk without overbuilding too early.

- Match product to infrastructure, offering hybrids and PHEVs where charging remains uneven.

- Prove reliability through service networks, spare parts access, and transparent warranties.

- Compete on total ownership cost, not only sticker price.

- Build trust over time, especially in markets where brand legacy influences resale value.

For consumers, the near-term impact is more choice and sharper competition—often at lower prices or with higher features-per-dollar. For established automakers, the pressure is rising to defend market share through better value, faster product cycles, and localized electrification strategies.

For policymakers, the challenge is balancing industrial goals with consumer affordability and emissions targets. And for Chinese automakers, 2025 is the year when the global push shifts from “selling cars abroad” to becoming part of local auto industries—with factories, jobs, and supply chains outside China.