The mainstream narrative regarding the current trade friction presents a simple, noble struggle: Washington and Brussels are “leveling the playing field” to protect domestic workers from a wave of subsidized imports. We are told that these tariffs are the only way to save the Western middle class while pursuing a green future. But this is political theater. What the general public is missing is that the China EV battery monopoly 2026 has already moved past the point of being solved by a simple tax.

While the US maintains its 100% “Section 301” duties and the EU shifts toward a “price undertaking” framework, they are fighting a tactical battle against a strategic reality. China doesn’t just build the cars; it owns the chemistry, the refining, and the intellectual infrastructure of the electric era. We aren’t just in a trade war; we are witnessing the institutionalization of a new energy dependency that the West is currently losing.

The Surface Illusion vs. The Third-Eye Reality

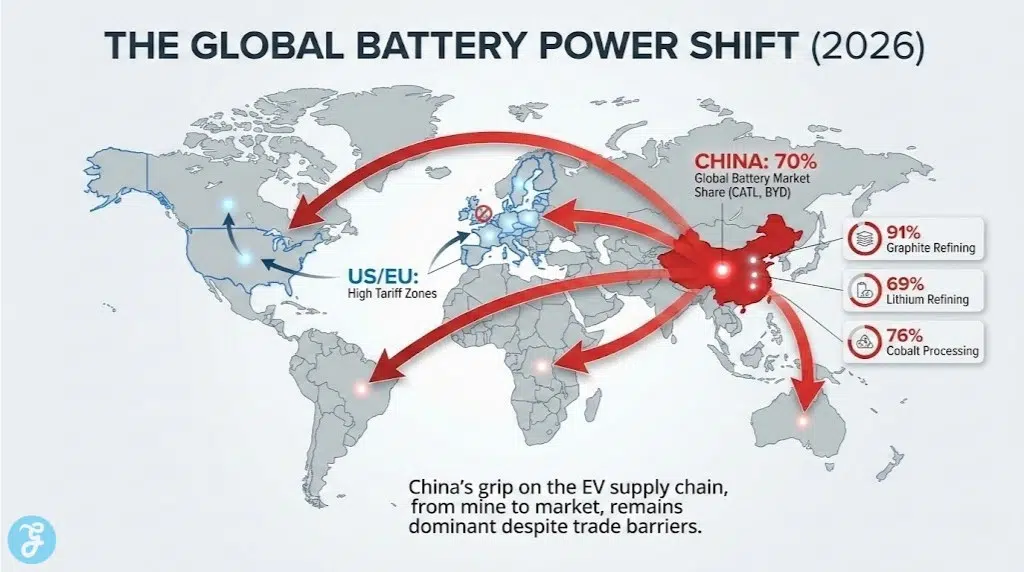

The “Front-Stage” politics suggest that a 15% to 100% import surcharge will provide a protective bubble for Western automakers like Volkswagen, Ford, and Stellantis to “catch up.” The public sees these tariffs as a shield for high-paying manufacturing jobs. However, the “Back-Stage” reality dictates that catch-up is an engineering impossibility under current policy. By the end of 2025, Chinese firms like CATL and BYD already command a staggering 70% of the global power-battery market. Tariffs on finished vehicles are a cosmetic fix for a structural hemorrhage. If the cells inside the car are Chinese, the car is Chinese, regardless of where the final door panel is bolted on.

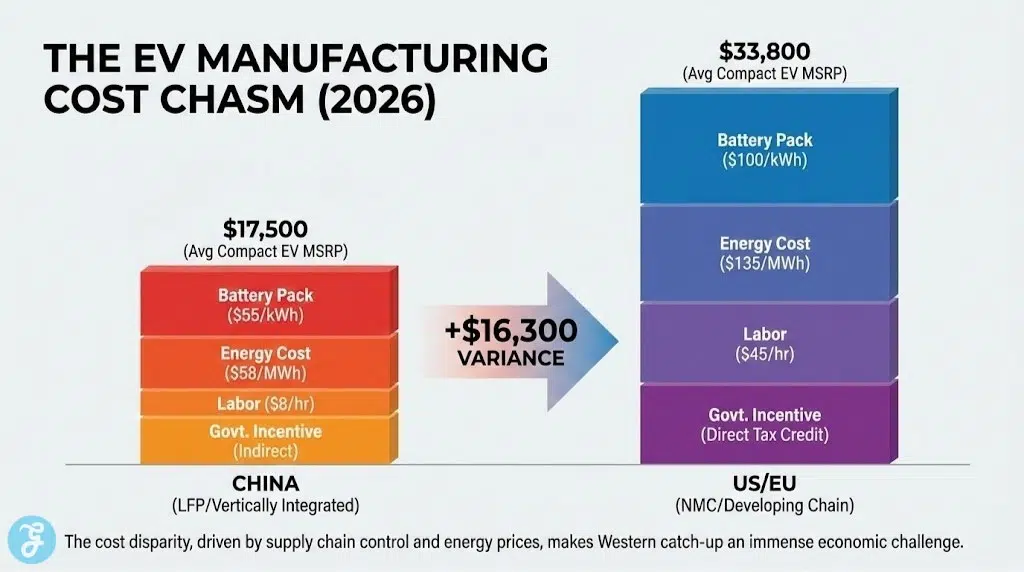

To understand the sheer economic gravity of this situation, we must look at the production math. While Western firms are still amortizing their first-generation Gigafactories, Chinese manufacturers are operating with a decade of vertical integration, leading to a massive price disparity that tariffs can barely dent. The “hidden cost” isn’t just the tax at the border; it is the $20,000 efficiency gap that Western automation has yet to solve.

Table 1: The Manufacturing Cost Gap (February 2026 Estimates)

| Component/Metric | China Cost Basis (USD) | EU/US Cost Basis (USD) | Variance (%) |

| LFP Battery Pack (per kWh) | $55 – $63 | $98 – $112 | +78% |

| Average Compact EV MSRP | $17,500 | $33,800 | +93% |

| Energy Cost for Cathode Processing (per MWh) | $58 | $135 | +132% |

| R&D to Production Cycle (Months) | 18 – 24 | 36 – 48 | +100% |

| Battery Recycling Recovery Rate | 98% | 85% | -13% |

| Government Incentive per Vehicle | $1,200 (Indirect) | $7,500 (Direct Tax Credit) | -84% |

This table illustrates the central irony of Western industrial policy: we are using taxpayer-funded subsidies to bridge a gap created by our own regulatory complexity. While a Chinese firm can iterate a new cell design in 18 months, Western firms are trapped in 48-month environmental and labor review cycles.

The Security Angle: Batteries as the New Geopolitical Chokepoint

From an intelligence perspective, the China EV battery monopoly 2026 is the single greatest vulnerability in Western national security. Military mobility is pivoting toward electrification for stealth and logistics, yet the “nervous system” of these vehicles is tethered to Beijing. This isn’t just about consumer convenience; it is about the fundamental control of the resources that power modern movement.

The vulnerability is rooted in a total dominance of the mid-stream processing stage. While lithium and graphite can be mined in many places, the ability to refine them into battery-grade materials is currently a nearly exclusive Chinese capability. By early 2026, over 90% of the world’s battery-grade graphite—the primary material for anodes—is processed within China.

Intelligence reports now highlight that this isn’t just an economic edge; it’s “Regulatory Jujitsu.” By controlling the processing, Beijing can effectively veto the industrial output of any nation that displeases it.

Table 2: Strategic Resource Control and Processing Dominance (2026)

| Resource Type | China’s Refined Market Share | Western Collective Share (US/EU/AU) | Strategic Vulnerability Level |

| Natural Graphite | 91.2% | 3.8% | Extreme |

| Lithium Refining | 69.5% | 11.2% | High |

| Cobalt Processing | 76.0% | 6.5% | High |

| LFP Cathode Patents | 84.0% | 9.0% | Intellectual Blockade |

| Silicon Anode Innovation | 62.0% | 22.0% | Moderate |

| Rare Earth Processing | 92.5% | 4.0% | Extreme |

While the US focuses on “onshoring” mining, they are ignoring the fact that a mine without a refinery is just a hole in the ground. China’s lead in the processing sector means they can let the West do the dirty work of mining while they extract the high-value profit from the refining stage.

The Economic Undercurrent: Follow the Money

The financial architecture of the EV transition is being rebuilt in real time. While the US Supreme Court recently struck down certain blanket tariffs, forcing a pivot to a 15% surcharge under Section 122 of the Trade Act, the EU has introduced a “price floor” mechanism. This allows Chinese firms like BYD to avoid the blunt force of 35% duties if they agree not to sell below a certain threshold—roughly €30,000.

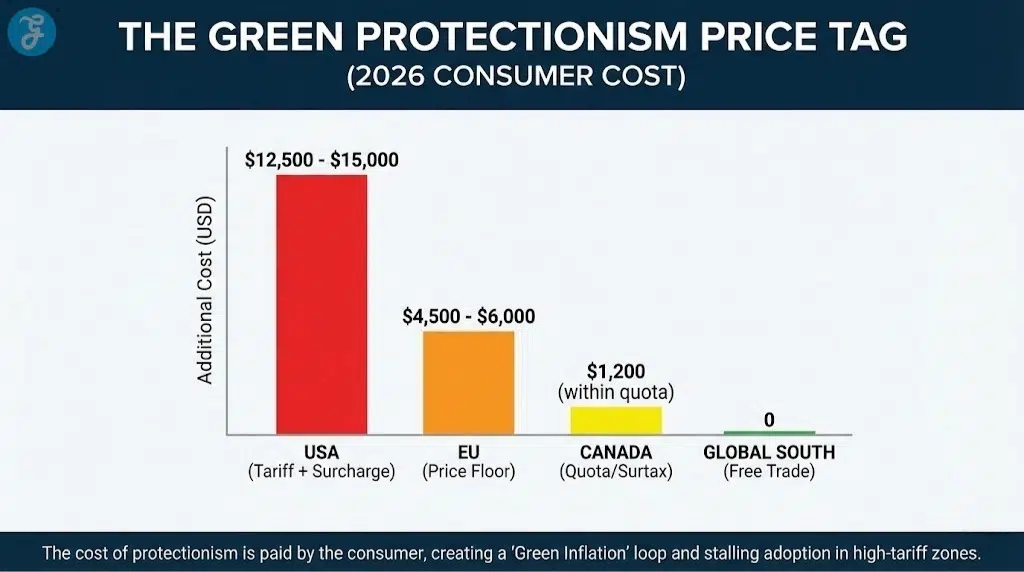

This creates a “Green Inflation” loop where carbon neutrality becomes a luxury for the wealthy. By the time a Western firm sources minerals from a “friendly” mine—which are often 40% more expensive due to ESG compliance—the Chinese competitors have already moved on to next-generation solid-state batteries. The price of protectionism is ultimately paid by the person in the showroom, who is now forced to choose between a $50,000 Western EV or a $15,000 internal combustion car, effectively stalling the green transition.

Table 3: The 2026 Protectionism Price Index

| Region | Tariff/Mechanism | Effective Cost Increase to Buyer | Estimated Impact on Adoption |

| United States | 100% Import Duty + 15% Surcharge | $12,500 – $15,000 | -18% vs 2025 Forecast |

| European Union | Price Undertaking (€30k Floor) | $4,500 – $6,000 | -8% vs 2025 Forecast |

| Canada | 100% Surtax on Chinese EVs | $14,000 | -22% vs 2025 Forecast |

| Australia | 0% (Free Trade Agreements) | $0 | +12% vs 2025 Forecast |

| Brazil/Mexico | 35% Ad Valorem | $3,500 | +25% (Ramping Local Hubs) |

The capital flight in this sector is equally telling. In Q1 2026, venture capital in the Western EV battery startup space dropped by 22% as investors realized that domestic firms cannot achieve the scale required to break the China EV battery monopoly 2026. Investors aren’t betting on the “shield” of tariffs; they are betting on the “engine” of Chinese innovation.

The Geopolitical Chessboard: Superpower Maneuvering

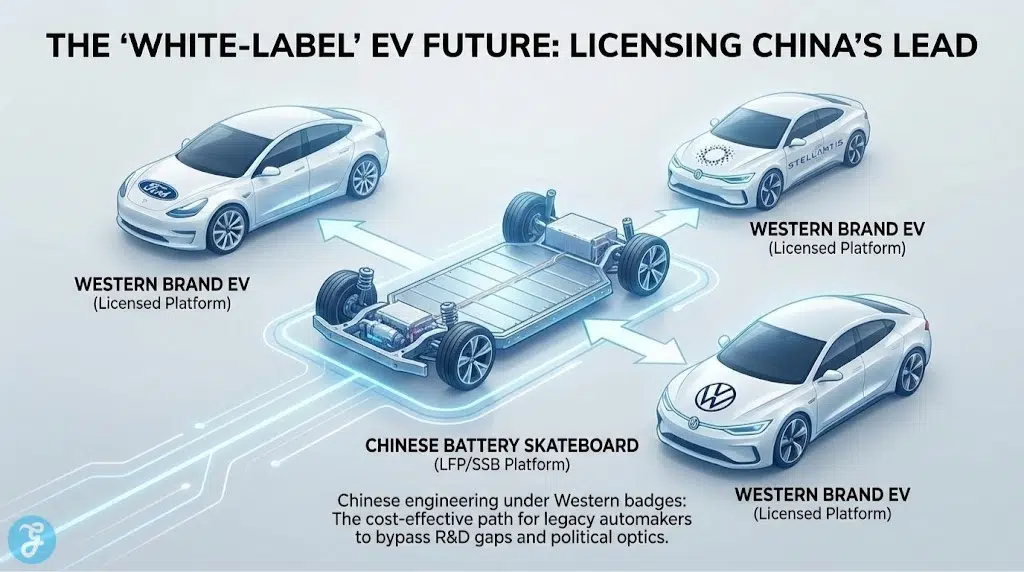

The China EV battery monopoly 2026 has forced a “Regulatory Jujitsu” from Beijing. Instead of fighting the tariffs head-on, Chinese firms are rerouting their influence through third-party nations and strategic partnerships. They are effectively building “Trojan Horse” factories within the very markets that are trying to keep them out.

-

The Mexico/Hungary Play: BYD and Gotion High-Tech are building massive manufacturing hubs in Monterrey and Debrecen. These plants aren’t just for assembly; they are designed to qualify as “local content” under USMCA and EU rules, effectively laundering Chinese technology into Western markets.

-

The Licensing Pivot: Ford and Stellantis have already begun “technology licensing” deals with CATL. This allows Western firms to use Chinese battery chemistry while maintaining the “Made in America” label—a face-saving move for politicians and a massive royalty win for Beijing.

-

The Global South Vacuum: While the West builds walls, China is building bridges. By 2026, 60% of all EVs sold in Southeast Asia, the Middle East, and Latin America are Chinese-branded. The West is winning the battle for its own driveways but losing the war for the rest of the planet.

Table 4: The Power Matrix: Declared vs. Actual Outcomes

| Entity | Declared Narrative | Actual 2026 Reality |

| Western Auto Workers | Saved from “Unfair” competition | Net Losers (High production costs lead to 20% staff cuts) |

| Chinese Battery Giants | Punished by trade barriers | Strategic Winners (Record profits via licensing and PHEVs) |

| Eco-Conscious Consumers | Transitioning to Green | Financial Losers (Paying a 30% “Protectionism Tax”) |

| Legacy Oil Interests | Facing extinction | Stealth Winners (Delayed EV adoption preserves oil demand) |

| Detroit “Big Three” | Protected and Resurgent | Strategic Losers ($60B in combined 2025-26 write-offs) |

| Global South Nations | Sidelined | Pragmatic Winners (Building infrastructure with cheap tech) |

The High-Tech Pivot: LFP and Solid-State Dominance

The hidden mechanics of the China EV battery monopoly 2026 also include a massive technological lead. Western firms spent the last decade chasing expensive Nickel-Manganese-Cobalt (NMC) chemistries. China, meanwhile, perfected Lithium Iron Phosphate (LFP)—a cheaper, safer, and longer-lasting alternative. By early 2026, LFP has captured 81% of the Chinese market and is now the global standard for affordable EVs.

Furthermore, the race for solid-state batteries (SSB) is already being won in the East. While Western prototypes are still in the lab, Chinese semi-solid-state packs are already powering premium sedans in 2026, offering 1,000km of range at a fraction of the cost.

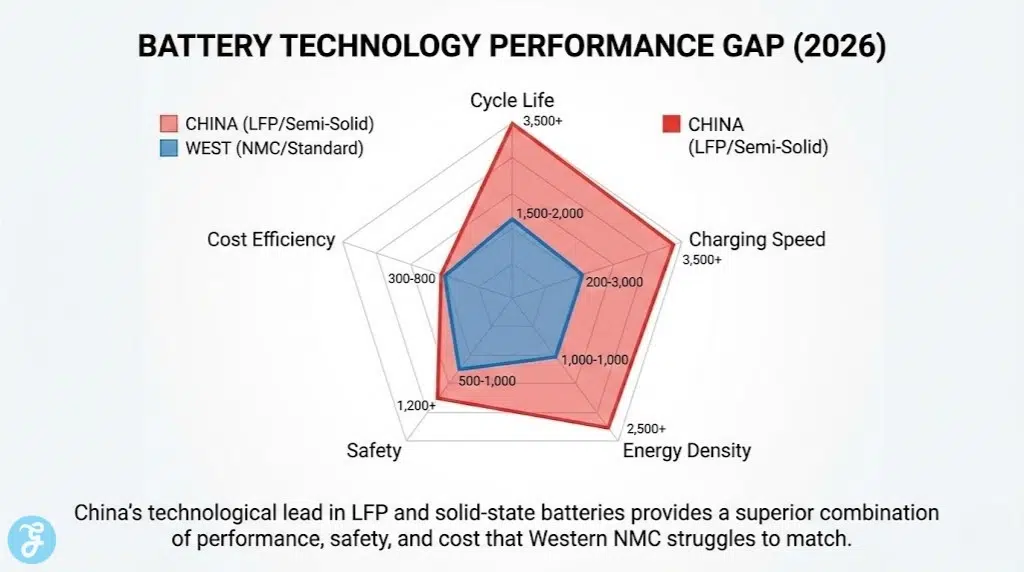

Table 5: Battery Tech Performance Gap (2026)

| Metric | China (LFP/Semi-Solid) | West (NMC/Standard) | Advantage |

| Cycle Life (Charges) | 3,500+ | 1,500 – 2,000 | China (2x Longevity) |

| Charging Speed (10-80%) | 10.5 Minutes | 22 – 30 Minutes | China (Ultra-Fast) |

| Energy Density (Wh/kg) | 280 (LFP) / 360 (SSB) | 240 (NMC) | China (Higher Range) |

| Safety (Nail Pen. Test) | Pass (Zero Thermal Runaway) | Fail (Combustion Risk) | China (Stable) |

Risk Forecast: A 3-Year Strategic Projection

Looking ahead, the next three years will be defined by a painful adjustment period. As Western nations double down on protectionism, the cost of the energy transition will likely peak before any domestic supply chains can reach true scale. The risk of supply chain volatility remains extreme as retaliatory mineral bans—like China’s February 2026 ban on dual-use exports to specific Western defense contractors—become a common diplomatic tool.

Table 6: 2027-2029 Strategic Risk Outlook

| Risk Factor | 2027 Outlook | 2028 Outlook | 2029 Outlook |

| Supply Chain Volatility | Extreme (Retaliatory mineral bans) | High (Price wars in secondary markets) | Stabilizing (New regional blocs) |

| Western EV Prices | Peak Inflation (+25% MSRP) | Plateau (Aggressive cost-cutting) | Declining (via Chinese Licensing) |

| Strategic Autonomy | Total Failure (Hidden reliance) | Forced Tech Partnerships | Permanent Interdependence |

| Geopolitical Tension | Military Supply Anxiety | Local Content Disputes | Institutionalized Decoupling |

The Data Points That Matter:

-

Market Concentration: The top five Chinese battery suppliers (CATL, BYD, CALB, Gotion, SVOLT) now control 82% of global installations.

-

LFP Dominance: LFP batteries now account for 78% of the global market due to their lower cost and higher safety, up from 45% in 2023.

-

The Export Surge: Despite tariffs, China’s power battery exports rose 59.3% year-on-year in January 2026 alone.

-

The Cost Gap: It remains 32% cheaper to produce an LFP battery pack in China than in the United States, even including transport and tariffs.

-

Investment Asymmetry: China is driving 71% of global battery manufacturing investments through the end of 2026.

What’s Ahead?

In the next 12 to 18 months, the unintended consequences of “Eco-Protectionism” will become undeniable. We will witness the birth of the “White-Label Era.” Western legacy brands, unable to bridge the 32% cost gap through internal R&D, will begin quietly licensing Chinese battery platforms (skateboards) and rebranding them as “Domestic.” They will effectively become marketing shells for Chinese engineering to bypass political optics.

The foresight assessment is clear: By 2028, the West will face a choice between admitting that the green transition is a Chinese-led sector or accepting a permanent economic and environmental disadvantage in the name of “security.” The China EV battery monopoly 2026 won’t be broken by 100% tariffs; it will simply be hidden behind Western badges.

The lingering question is this: If we are willing to pay a “protectionism tax” to keep Chinese technology out of our driveways, are we actually protecting our industry—or are we just funding its slow, expensive obsolescence while the rest of the world moves on without us?