Thinking of giving up your U.S. citizenship? You might be tired of filing taxes on money earned overseas, or maybe you want to make a new start in another country. It is a big decision that feels a lot like a breakup. Many people worry the process is confusing and full of surprise costs. You might have heard rumors about massive exit taxes or being stopped at the border.

Here is one fact that might help you sleep better: Most Americans who renounce their citizenship will not owe an exit tax. This only happens if you meet specific financial rules set by the IRS.

Walk you through the exact costs, the forms you need, and the traps to avoid. Let’s clear up the confusion so you can move forward with confidence.

What Does It Mean to Renounce Citizenship?

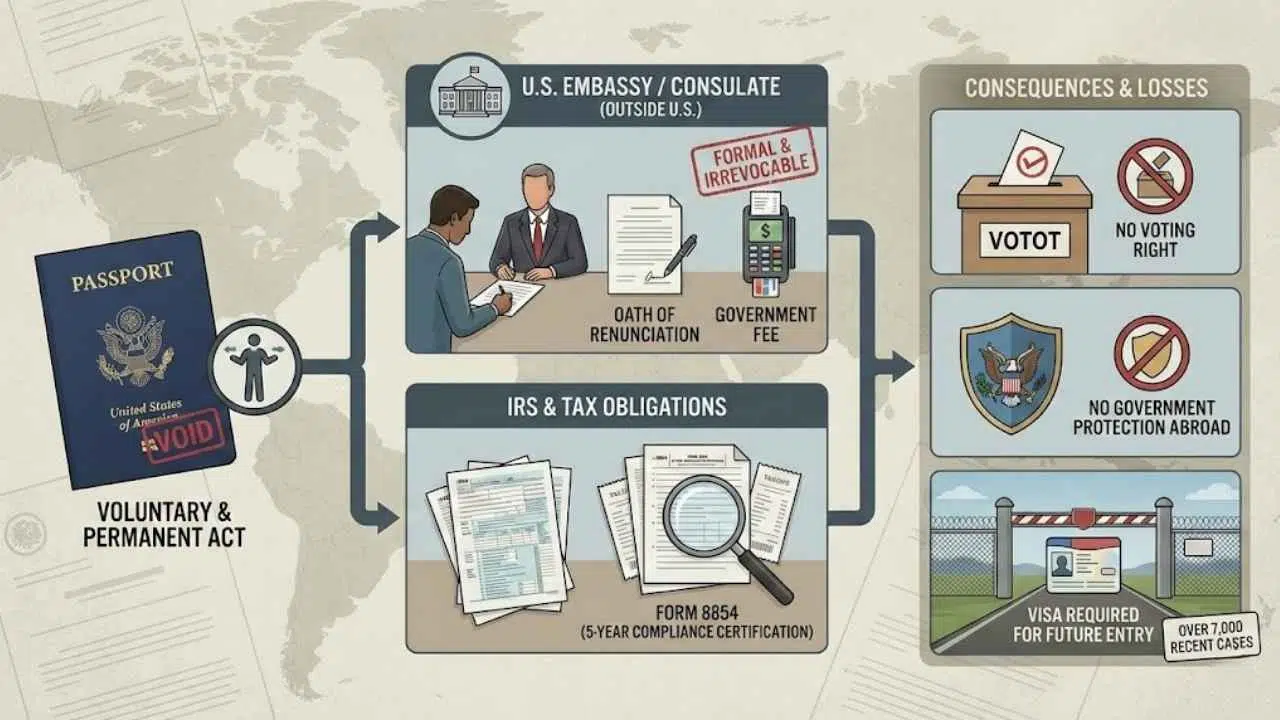

Renouncing citizenship is a voluntary act of giving up your rights and responsibilities as a U.S. citizen. It is not just handing over a passport; it is a legal process that changes your status forever.

You must attend an in-person interview at a U.S. embassy or consulate outside the country. During this meeting, you will sign an oath of renunciation and pay a government fee. This step is formal and irrevocable. You cannot simply change your mind if you decide you miss the benefits later.

The IRS treats this very seriously. They expect every single past tax obligation to be settled before you go. This includes filing a specific form called Form 8854 to certify you have played by the rules for the last five years.

While over 7,000 Americans have taken this step recently, it comes with real consequences. You lose the right to vote, the right to government protection abroad, and the automatic right to enter the U.S. in the future. You will need a visa just like any other foreign visitor.

The Costs of Renouncing U.S. Citizenship

Saying goodbye to Uncle Sam comes with a price tag. The paperwork alone might make your wallet weep before you even pack your bags. It is important to budget for both the immediate government fees and the professional help you might need.

Filing fees

There is a lot of confusion about the government fee. For years, it was $450. Then it jumped to $2,350. While there is a current proposal and a lawsuit pushing to lower it back to $450, the official fee remains higher for now.

As of early 2026, you must pay $2,350 to the U.S. government to renounce your citizenship

This fee is payable at your embassy appointment. It covers the administrative work of processing your Certificate of Loss of Nationality. It is the highest renunciation fee in the world. You should be prepared to pay the full $2,350 until the State Department officially finalizes the rule change to lower it.

Additional administrative costs

The government fee is just the start. You might face other expenses that add up quickly.

- Travel Costs: You must go to a U.S. embassy or consulate in person. If you don’t live near one, you will pay for flights and hotels.

- Document Prep: You may need notary services or certified copies of birth certificates and naturalization papers.

- Professional Help: Many people hire a tax attorney or CPA to handle the complex IRS Form 8854. These pros often charge between $2,000 and $5,000 depending on your situation.

“A common mistake is budgeting only for the embassy fee. You must also budget for the ‘compliance check’ to ensure your tax returns are perfect before you walk into that interview.”

Who Qualifies as a Covered Expatriate?

This is the most critical definition in the entire process. The IRS separates people who renounce into two groups: “Covered Expatriates” and everyone else.

If you are a “Covered Expatriate,” you face extra scrutiny and potentially a massive exit tax. You fall into this category if you meet any one of the following three tests.

1. The Net Worth Test

You are a covered expatriate if your net worth is $2 million or more on the date you renounce. This includes everything you own worldwide.

The IRS counts your home, your retirement accounts, your investments, and even your personal jewelry. It is not just about cash in the bank. If your global assets hit this $2 million mark, you trigger the rule.

2. The Tax Liability Test

This test looks at your average annual net income tax for the five years before you renounce. It is adjusted for inflation every year.

| Year of Renunciation | Average Tax Liability Threshold |

|---|---|

| 2024 | $201,000 |

| 2025 | $206,000 |

| 2026 | $211,000 |

If your average federal tax bill over the last five years is higher than the number for your year, you are a covered expatriate. Note that this refers to the tax you paid, not just your income.

3. The Tax Compliance Test

This is the trap that catches most people. Even if you have very little money, you can become a covered expatriate if you fail this test. You must certify on Form 8854 that you have complied with all federal tax obligations for the five years before you renounce. If you missed a single tax return, or if you forgot to file an FBAR for your foreign bank account, you fail.

Failing this test automatically makes you a covered expatriate. It does not matter if your net worth is zero. This is why reviewing your last five years of returns is the first step you should take.

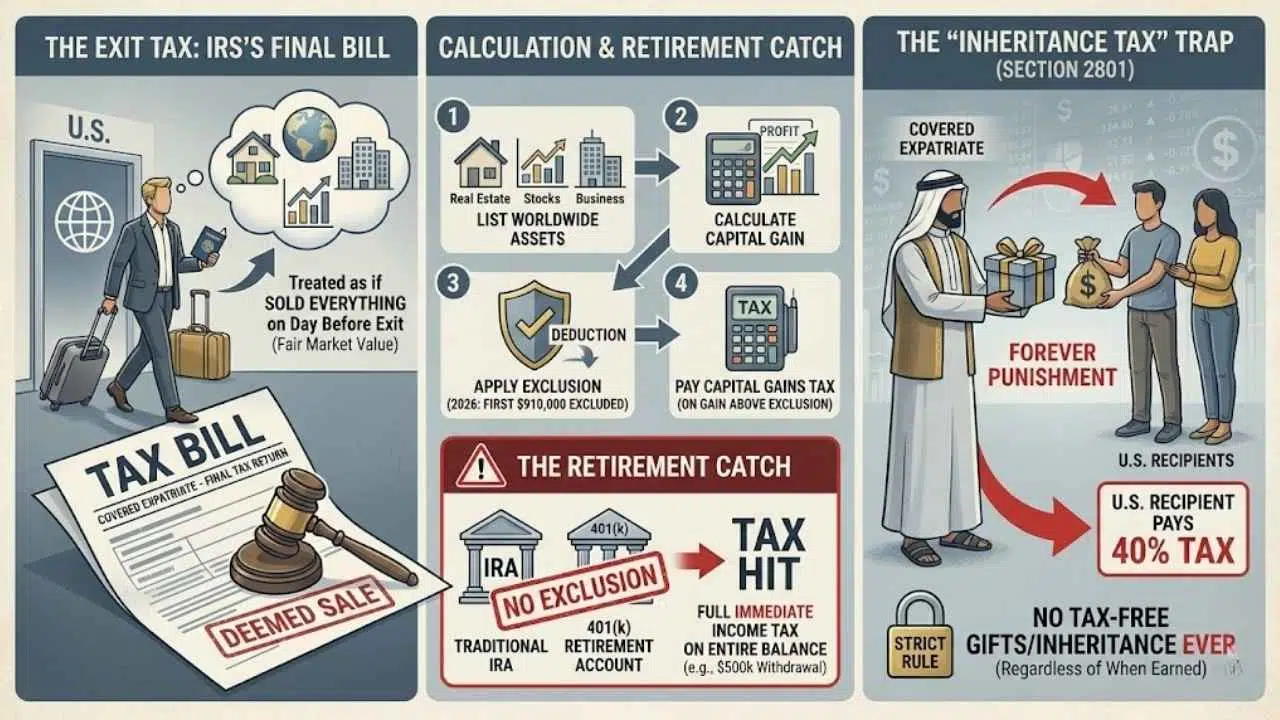

What is the Exit Tax?

The exit tax is the IRS’s final bill. If you are a covered expatriate, the U.S. government treats you as if you sold everything you own on the day before you left.

This is called a “deemed sale.” You have to calculate the capital gains on all your assets as if you sold them for fair market value.

Calculation of the exit tax

The calculation can be complex, but the basic logic follows these steps.

- List Your Assets: Tally up everything worldwide. This includes real estate, stocks, and business interests.

- Calculate the Gain: Figure out how much profit you would have made if you sold them.

- Apply the Exclusion: You get a break on the first portion of the gain. For 2026, you can exclude the first $910,000 of gain. (For 2025, it was $890,000).

- Pay the Tax: You pay capital gains tax on anything above that exclusion amount.

There is a catch for retirement accounts. IRAs and 401(k)s do not get the exclusion. If you have a $500,000 IRA, the IRS treats it as if you withdrew the whole thing at once. You will owe immediate income tax on the entire balance. This can be a huge financial hit.

The “Inheritance Tax” Trap (Section 2801)

There is a hidden cost that many people miss until it is too late. It is called the Section 2801 tax.

If you are a covered expatriate, you can never give tax-free gifts to U.S. citizens again. If you leave money to your U.S. children or send a large gift to a U.S. friend, they must pay a 40% tax on it.

This punishment lasts forever. It does not matter if the money was earned after you renounced. It is a strict rule designed to discourage wealthy people from leaving.

Tax Implications for Non-Covered Expatriates

If you stay under the $2 million net worth limit and pass the compliance test, you are a “Non-Covered Expatriate.” This is the best outcome. You generally will not owe any exit tax.

Filing the final U.S. tax return

Even if you owe zero exit tax, you still have one final job to do. You must file a final Form 1040 for the portion of the year you were a citizen.

You must check the box that says “Dual Status Statement” or “Final Return.” You will report income from Jan 1st up to the date you renounced. After that date, the IRS generally stops taxing your foreign income.

You must also file Form 8854. This form is your official declaration to the IRS. It proves you are non-covered and cuts your tax ties cleanly.

Avoiding exit tax obligations

The best way to win is to plan ahead. If you are close to the $2 million mark, you might consider legally gifting assets to your spouse or charity before you renounce to lower your net worth. You can use your lifetime gift exemption to do this tax-free in many cases.

If you have missed tax returns, fix them first. Use the IRS “Streamlined Filing Compliance Procedures” to catch up on back taxes without huge penalties. Never schedule your embassy appointment until your tax history is spotless.

Tax Considerations for Green Card Holders

You do not have to be a citizen to face the exit tax. Long-term green card holders are treated exactly the same way.

Expatriation for long-term residents

The IRS defines a “Long-Term Resident” as anyone who held a green card in at least 8 out of the last 15 years. It does not matter if you barely lived in the U.S. during those years. If you held the card, the clock was ticking.

If you fit this definition, you must file Form 8854 when you surrender your card. You are subject to the same net worth and tax liability tests as citizens. Surrendering your green card formally (using Form I-407) triggers these rules.

Key differences from U.S. citizens

There is one major escape hatch for green card holders. If you surrender your card before you hit the 8-year mark, you are safe.

You can walk away without filing Form 8854 or worrying about the exit tax. If you are approaching that 8-year anniversary, you should talk to an immigration lawyer immediately. Giving up the card a few months early could save you a fortune.

Steps to Renounce U.S. Citizenship

If you are ready to proceed, following a clear checklist will keep you out of trouble.

Achieving tax compliance

Before you do anything else, get your Social Security Number ready. You cannot file Form 8854 without one.

Review your last five years of tax returns. Did you report all your interest income? Did you file the FBAR for your foreign accounts? If you find a mistake, amend the return now. You want a clean slate before you trigger the IRS review.

Filing Form 8854

Form 8854 is the “Expatriation Information Statement.” You file this with your final tax return. It asks for a balance sheet of your assets and a declaration of your tax compliance.

You must file this form on time. If you file it late, the IRS can fine you $10,000. Even worse, they can refuse to recognize your renunciation for tax purposes, meaning you stay on the hook for U.S. taxes indefinitely.

Completing the renunciation process

- Book the Appointment: Contact the U.S. embassy in your country of residence. Wait times can be months long.

- The Interview: You will go in, sign the forms, and pay the $2,350 fee.

- Wait for the CLN: The State Department will process your paperwork and mail you a Certificate of Loss of Nationality (CLN).

- File Taxes: The next year, you file your final return and Form 8854.

Alternatives to Renouncing Citizenship

Giving up your passport is drastic. Sometimes there are other ways to solve your tax problems.

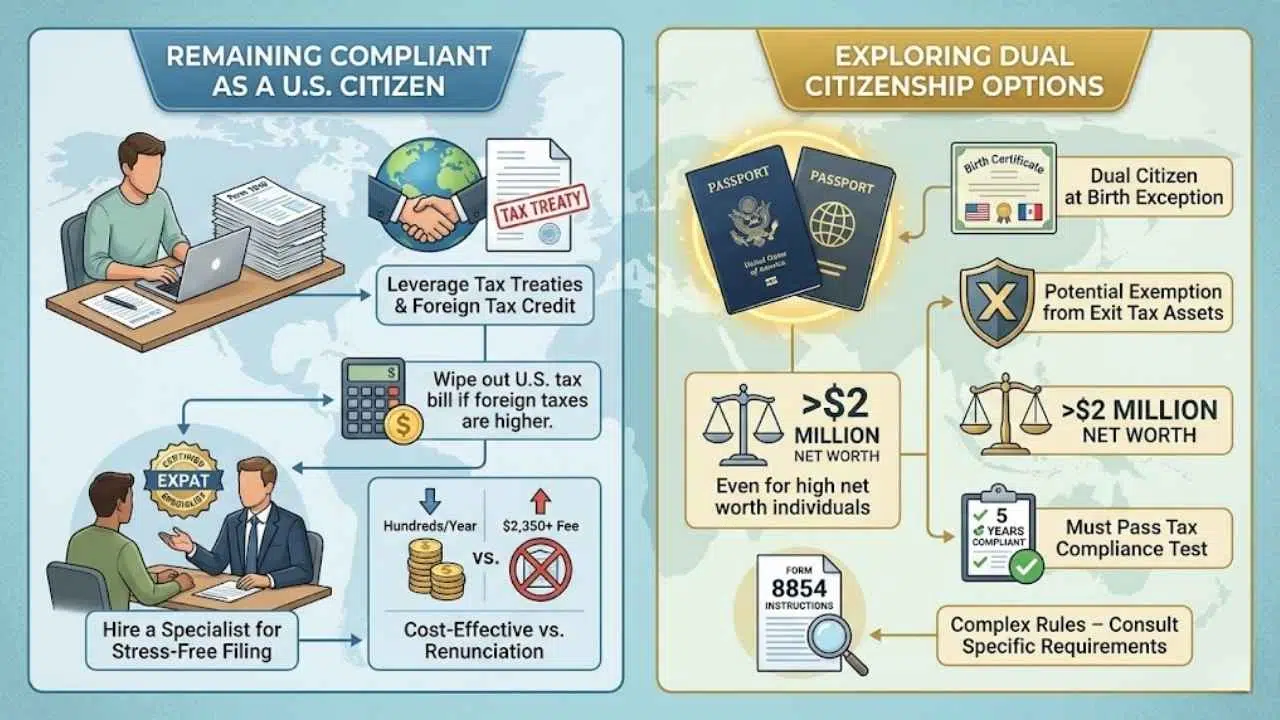

Remaining compliant as a U.S. citizen

You can keep your citizenship and simply manage the paperwork better. The U.S. has tax treaties with over 60 countries to prevent double taxation. You can often use the “Foreign Tax Credit” to wipe out your U.S. tax bill if you pay higher taxes where you live.

Hiring a specialist who knows expat taxes can take the stress out of filing. It might cost a few hundred dollars a year, which is much cheaper than the $2,350 renunciation fee.

Exploring dual citizenship options

If you were born a dual citizen (meaning you had both passports from birth), you might have a special “get out of jail free” card.

The IRS has an exception for dual citizens at birth. You can be exempt from the Covered Expatriate status even if your net worth is over $2 million. You still have to pass the tax compliance test, but you can avoid the exit tax on your assets. This is a complex rule, so check the specific requirements in the Form 8854 instructions carefully.

Final Thoughts

Renouncing your citizenship is a life-changing event with serious math attached to it. You have to navigate the $2,350 fee, the strict Covered Expatriate tests, and the final “deemed sale” tax. The secret to a smooth exit is preparation. Check your net worth against the $2 million limit. Ensure your last five years of taxes are flawless. And most importantly, do not ignore the forms. If you plan carefully, you can turn the page to your new chapter without owing Uncle Sam a parting gift. Take a deep breath, gather your documents, and take it one step at a time.