The 56th Annual Meeting of the World Economic Forum (WEF) has convened under the banner “A Spirit of Dialogue,” but the mood in the Swiss Alps is defined by a stark cognitive dissonance. While plenary sessions extol the virtues of cooperation, the world’s major powers are actively fortifying their borders with the most aggressive industrial policies seen in decades. This is no longer just about tariffs; it is a structural decoupling of the global economy into rival blocs. For businesses and policymakers, the question is no longer if fragmentation will occur, but how to survive the collision between Western security anxieties and China’s export-led “Shock 2.0.”

The Great Disconnect: Rhetoric vs. Reality

To understand the tension at Davos 2026, one must look at the events of the preceding twelve months that have dismantled the post-Cold War consensus. We arrived here through a cascade of defensive measures that have mutated into offensive economic statecraft.

The trajectory began shifting decisively in late 2025. The United States, operating under a renewed “America First” mandate following the political shifts of 2025, moved beyond targeted restrictions to broad-spectrum tariffs on “strategic rival” imports. Simultaneously, the European Union’s Carbon Border Adjustment Mechanism (CBAM) entered its full implementation phase on January 1, 2026, effectively erecting a green tariff wall around the single market.

In response, Beijing—facing its own internal property crisis and softening domestic demand—has doubled down on manufacturing, unleashing what economists are calling “China Shock 2.0”: a flood of high-tech, low-cost exports (EVs, lithium batteries, legacy chips) aimed at the Global South and Europe.

The “Spirit of Dialogue” theme, chosen by WEF founder Klaus Schwab, seems almost aspirational—a counter-narrative to the reality of the “geoeconomic confrontation” which the WEF’s own Global Risks Report 2026 identified as the year’s top threat.

Core Analysis: The Architecture of Fragmentation

This analysis breaks down the current geopolitical stalemate into five distinct sub-themes driving the global agenda in 2026.

1. The “Green Protectionism” Paradox

The most significant shift in 2026 is the weaponization of climate policy. For years, the West urged the world to decarbonize. Now that China has achieved dominance in green supply chains, the West is changing the rules.

The EU’s CBAM is no longer a theoretical threat; as of three weeks ago, importers of steel, cement, and hydrogen must pay for the embedded carbon emissions of their goods. While Brussels frames this as an environmental necessity, the developing world views it as a “green imperialist” tax. India and Brazil have already filed disputes at the WTO (World Trade Organization), arguing that CBAM discriminates against their developing industrial bases.

Meanwhile, the US Inflation Reduction Act (IRA) provisions have tightened, disqualifying any EV with battery components from “Foreign Entities of Concern” (primarily China) from subsidies. The result is a fractured green market: a high-cost, protected Western zone and a low-cost, China-dominated zone for the rest of the world.

Key Insight: Climate action is no longer a cooperative global public good; it is a zero-sum game of industrial competitiveness.

2. “China Shock 2.0”: The Deflationary Tsunami

Unlike the first “China Shock” of the early 2000s, which centered on cheap labor and textiles, the 2026 shock is built on advanced manufacturing and automation. With domestic consumption in China remaining tepid, Beijing has directed state credit into “New Three” industries: solar cells, lithium-ion batteries, and electric vehicles.

Western markets are currently saturated with inventory. In Davos, European CEOs are privately warning of an “extinction event” for their auto industries without steeper tariffs. This puts the EU in a bind: it needs Chinese green tech to meet its 2030 climate goals but cannot afford the deindustrialization that comes with unrestricted imports.

3. The Tech Sovereignty & “Silicon Curtain.”

The technology war has migrated from “choke points” (stopping China from getting advanced chips) to “divergence” (two separate tech stacks). In 2026, we are seeing the emergence of a true “Splinternet” in Artificial Intelligence.

The US has expanded export controls to include “agentic AI” models—software capable of autonomous reasoning—and the specialized data centers required to train them. In retaliation, China has restricted the export of gallium and germanium, critical minerals for semiconductor manufacturing, causing spot price spikes of 40% in Q4 2025.

Implication for Business: Multinational corporations are now forced to operate “in-China-for-China” IT systems, completely air-gapped from their global networks to comply with conflicting data sovereignty laws in Washington and Beijing.

4. The Return of Fiscal Dominance

A quiet but dangerous theme at Davos 2026 is the sheer cost of this industrial nationalism. The “peace dividend” is dead.

- Defense: Europe is attempting to finance an €800 billion defense overhaul.

- Reshoring: The US is subsidizing domestic chip fabrication at a cost of billions per fab.

- Demographics: All major powers are facing aging populations.

This trifecta (Guns, Green Transition, and Geriatrics) is driving deficits higher. Bond vigilantes are circling, and the risk of a sovereign debt crisis in a G7 nation is higher now than at any point since 2012.

5. The “Non-Aligned” Hedges

The “Global South” (a term increasingly resented but still used) is refusing to pick a side. Nations like Saudi Arabia, India, and Indonesia are pursuing a “multi-aligned” strategy—taking US defense guarantees while deepening trade ties with China. At Davos, these delegations are the most confident, positioning themselves as the “connectors” in a fragmented world, demanding technology transfers in exchange for market access.

Market Signals From The Congress Centre

In hallway conversations, the most striking shift is not the rhetoric about cooperation. It is the language of operational contingency. Executives are no longer debating whether fragmentation is real. They are debating which parts of their businesses must split first, and which can remain global for a little longer.

In this Davos 2026 Analysis, three signals stand out across sectors:

-

Capex Is Moving From “Best Cost” To “Best Jurisdiction.” Projects that were uneconomic in 2023 now pencil out once subsidies, tariffs, and security screening are priced in.

-

Compliance Has Become A Strategic Function. Trade lawyers and carbon accountants are sitting next to product and procurement leaders, not behind them.

-

Time Horizons Are Shrinking. Firms that used to plan supply chains over 5 to 10 years are planning in 12 to 24 month windows because policy risk is now the dominant variable.

Why The “Dialogue” Theme Still Matters

It is tempting to dismiss “A Spirit of Dialogue” as branding. Yet the theme functions as a pressure valve. Even rival blocs need rules for contact, especially when the economic and tech systems are separating in ways that can trigger accidental escalation.

Dialogue is also becoming more transactional. The new version is less about shared values and more about narrow guardrails:

-

Preventing tit-for-tat export bans from crippling critical inputs

-

Aligning minimum disclosure standards for carbon accounting

-

Creating carve-outs for humanitarian, medical, and safety-related tech flows

Corporate Survival Guide For A Fragmented Global Economy

The firms best positioned in 2026 are not the ones with the loudest geopolitical narratives. They are the ones with the cleanest operating models. “Clean” now means auditable, localizable, and able to run under multiple regulatory regimes.

Operational Moves Companies Are Implementing Right Now

-

Dual Sourcing With Policy Triggers: Contracts that automatically shift volumes if tariffs, sanctions, or CBAM costs cross a defined threshold.

-

Jurisdictional Product Versions: Slightly different SKUs for the US, EU, and “rest-of-world” markets to match subsidy rules and content requirements.

-

Data Segmentation By Design: Separating training data, customer analytics, and model deployment environments to avoid cross-border contamination under conflicting laws.

-

Supplier Carbon Passports: Requiring suppliers to provide verifiable carbon intensity data, not marketing claims.

Table: The New Corporate Control Panel

| Control Lever | What It Used To Optimize | What It Optimizes In 2026 | Typical Owner |

|---|---|---|---|

| Supplier Selection | Lowest unit cost | Policy resilience and traceability | Procurement + Legal |

| Factory Location | Labor, logistics | Subsidies, security review risk | Strategy + Finance |

| Product Design | Performance, margin | Local content eligibility | Engineering + Compliance |

| Data Architecture | Central efficiency | Sovereignty compliance | CIO + Risk |

| Inventory Strategy | Lean supply | Shock absorption | Operations |

Carbon Compliance Is Becoming A Competitive Weapon

CBAM is changing behavior beyond the EU’s borders because it forces measurement. Once carbon intensity becomes priced and audited, it becomes a market signal. Suppliers who can document lower emissions win contracts, even outside Europe, because buyers want future-proof supply.

This drives a second-order effect: decarbonization investment is shifting toward export-facing industries first. That can widen inequality inside countries where domestic sectors remain unmeasured and underfunded.

Practical Steps For CBAM-Exposed Exporters

-

Map exposure by product line, not just by country

-

Build a verified emissions baseline with third-party assurance

-

Negotiate contracts that share CBAM-related cost changes

-

Invest in process upgrades that cut emissions per unit, not just offsets

-

Prepare for documentation disputes, since paperwork will decide market access

Table: Common CBAM Friction Points

| Friction Point | What Goes Wrong | How Firms Reduce Risk |

|---|---|---|

| Data Quality | Incomplete supplier emissions data | Require standardized reporting templates |

| Verification | Conflicting third-party audits | Use EU-recognized verification pathways |

| Scope Confusion | Misclassified embedded emissions | Train teams on product-specific rules |

| Contract Gaps | No cost-sharing clauses | Add CBAM pass-through mechanisms |

| Timing | Late reporting triggers penalties | Automate reporting deadlines and alerts |

The AI Divide Is Creating A Two-Speed Innovation Map

The “Silicon Curtain” is not only about chips. It is about the rules around model training, data residency, compute access, and model weights. When these diverge, innovation clusters form inside each bloc, and diffusion slows across borders.

Companies at Davos are increasingly treating AI as a regulated asset class:

-

Model lineage matters because a single restricted component can contaminate an entire deployment path.

-

Compute location matters because training outside an approved jurisdiction can trigger legal exposure.

-

Vendor dependency matters because switching costs are rising as stacks diverge.

What “In-China-For-China” Looks Like In Practice

-

Separate cloud tenancy, identity systems, and logging

-

Local model deployment with bounded interfaces to global systems

-

Regional data lakes with strict export controls on data and embeddings

-

Vendor diversification to reduce single-country choke risk

The Middle Powers Are Building The New Toll Gates

A quiet Davos reality is that multi-aligned countries are learning how to price their connectivity. They can offer manufacturing capacity, minerals, ports, and market access. In return, they demand technology transfer, local employment, and sometimes political concessions.

This is not neutral globalization. It is managed bargaining. And it can be highly rational for these states.

Leverage Points “Connector” Countries Are Using

-

Preferential permitting for factories that include local R&D

-

Mineral export licensing tied to downstream processing commitments

-

Digital regulations that require local data storage and local partners

-

Defense procurement offsets linked to civilian industrial investment

Scenario Matrix For The Rest Of 2026

Policy uncertainty is not a fog. It is a set of plausible pathways. Executives in Davos are running scenarios that look less like traditional economics and more like political risk models.

Table: Three Plausible 2026 Pathways

| Scenario | What Happens | Who Benefits | Who Gets Hit |

|---|---|---|---|

| Managed Coexistence | Narrow guardrails stabilize trade friction | Diversified multinationals | Single-market dependent exporters |

| Escalation Loop | New tariffs and export bans spread to more sectors | Domestic champions with subsidies | Consumers and cross-border platforms |

| Patchwork Deals | Sector-by-sector agreements replace broad WTO rules | Firms with strong lobbying capacity | Smaller firms lacking compliance budgets |

A Practical Checklist For Leaders After Davos

The biggest mistake is treating this as a temporary phase. The second biggest mistake is overreacting with expensive duplication everywhere. A smarter approach is to localize what is politically sensitive and keep the rest modular.

-

Identify your top 20 revenue products and map policy exposure per market

-

Build a “compliance-to-design” pipeline so eligibility is engineered early

-

Create a tariff and carbon shock dashboard with clear triggers

-

Stress test cash flow under higher working capital and slower customs

-

Negotiate supplier contracts with origin, data, and emissions clauses

-

Audit your AI stack for restricted components and cross-border data flows

Closing Add-On

The heart of Davos 2026 is not optimism or pessimism. It is realism. The world is reorganizing around security, climate competitiveness, and technological control. Firms and countries that treat rules as strategy will outperform those that treat them as paperwork.

Data & Visualization

To understand the scale of these shifts, we must look at the data. The following tables illustrate the rapid escalation of policy interventions.

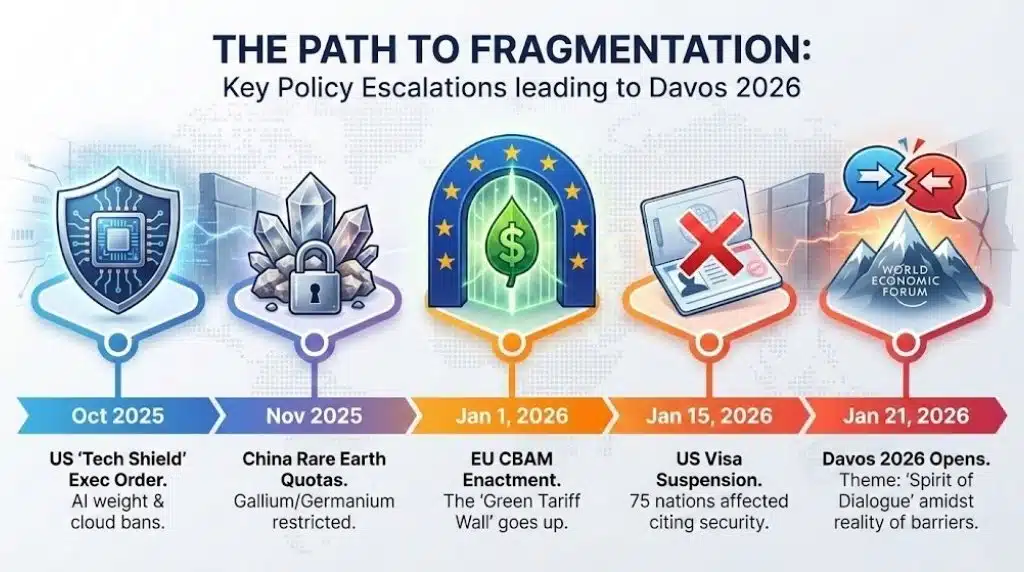

Table 1: The Escalation Timeline (2025–2026)

A chronology of the key policy decisions leading to the current standoff.

| Date | Event | Impact |

| Oct 2025 | US “Tech Shield” Executive Order | Expanded bans on export of AI model weights and cloud compute access to China. |

| Nov 2025 | China Rare Earth Quotas | Strict export quotas placed on Gallium, Germanium, and Graphite. |

| Jan 1, 2026 | EU CBAM Enactment | Full carbon pricing applies to imports; “Green Tariff” wall effectively goes up. |

| Jan 15, 2026 | US-75 Country Visa Suspension | US suspends immigrant visas for 75 nations (including Bangladesh) citing security. |

| Jan 21, 2026 | Davos 2026 Opening | Theme “Spirit of Dialogue” clashes with reality of new trade barriers. |

Table 2: The Subsidy War: Comparative Arsenal

How the three major blocs are funding their industrial nationalism.

| Feature | United States (Post-IRA/Chips Act) | European Union (Green Deal/Defense Fund) | China (15th Five-Year Plan Focus) |

| Primary Tool | Tax Credits & Direct Subsidies | Regulation (CBAM) & State Aid Relaxations | State-Directed Credit & Supply Side Subsidies |

| Focus Sector | Semiconductors, AI, EV Batteries | Green Hydrogen, Wind, Defense | “New Three” (EVs, Solar, Batteries), Legacy Chips |

| Barrier Type | “Buy American” Local Content Rules | Carbon Intensity Standards | Market Access Restrictions |

| 2026 Goal | Re-industrialize the Rust Belt | Strategic Autonomy from US/China | Export Excess Capacity to Global South |

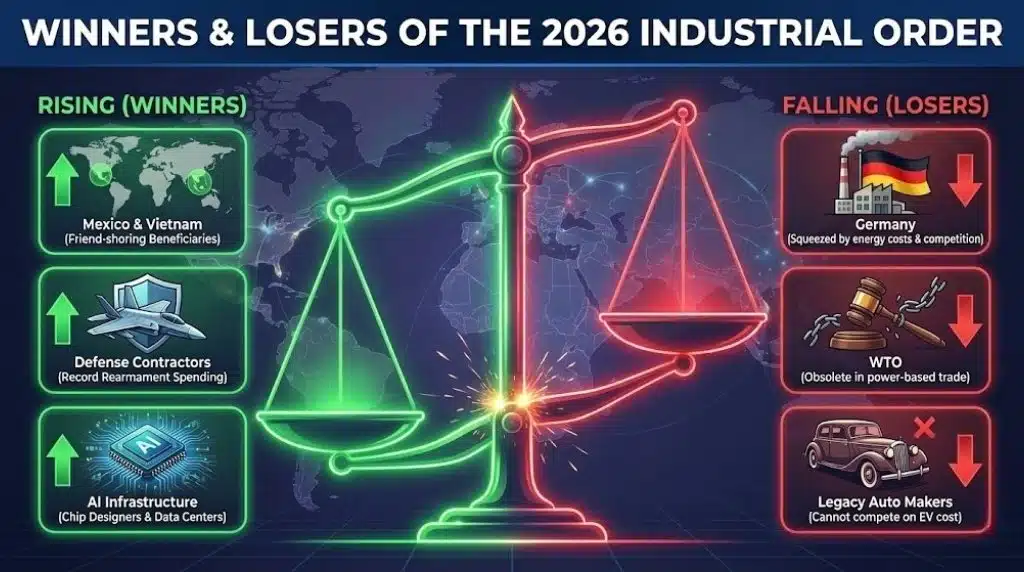

Table 3: Winners & Losers of the New Industrial Order

| Winners | Why? | Losers | Why? |

| Mexico & Vietnam | Primary beneficiaries of “friend-shoring” as supply chains exit China. | Germany | Squeezed between high energy costs and Chinese EV competition. |

| Defense Contractors | Record spending in EU and Asia to re-arm. | WTO | Rendered obsolete as trade disputes are settled by power, not rules. |

| Critical Mineral Exporters | Countries like Chile/Indonesia can demand premiums for lithium/nickel. | Legacy Auto Makers | Cannot compete with Chinese cost structure on EVs without tariffs. |

| AI Infrastructure | Data center builders and chip designers (Nvidia, TSMC). | Consumer Electronics | Prices rising due to supply chain bifurcation. |

Expert Perspectives

To maintain objectivity, it is crucial to synthesize the differing viewpoints emerging from the Congress Centre in Davos.

- The American View: US Trade Representative officials argue that the old system of “hyper-globalization” hollowed out the American middle class and empowered an autocratic rival. They contend that resilience is worth the price of efficiency. “We are not decoupling,” one US diplomat stated off-the-record, “we are de-risking our very existence.”

- The European Dilemma: Christine Lagarde (ECB President) and EU leaders are caught in the middle. They fear that US subsidies are sucking capital out of Europe (the “sucking sound” of investment moving to the US), while Chinese exports crush their manufacturing. Their strategy is “Open Strategic Autonomy”—a polite term for “we will protect our market while trying to keep trade lines open.”

- The Global South Critique: Leaders from the G77 argue that the West’s sudden turn to protectionism is hypocritical. “When you were competitive, you preached free trade,” noted a Brazilian diplomat. “Now that Asian nations are competitive, you preach security and carbon taxes.”

Future Outlook: What Comes Next?

As we look beyond Davos 2026, three milestones will define the remainder of the year.

- The “Carbon Club” Negotiations (Q2 2026): The US and EU will attempt to merge their steel and aluminum tariffs into a unified “Global Arrangement on Sustainable Steel.” If successful, this will create a transatlantic green trade bloc, effectively locking out Chinese dirty steel.

- The AI Safety Summit 2.0 (Q3 2026): Focus will shift to “sovereign AI.” Nations will move to build their own “sovereign clouds” to ensure their data isn’t training American or Chinese models. This will further fragment the internet.

- The emerging “Shadow Trade”: As tariffs rise, we predict a massive increase in trans-shipment fraud—Chinese goods being lightly processed in Mexico or Morocco to bypass Western tariffs. This will lead to a game of regulatory “whack-a-mole” where certificates of origin become the most contested documents in global trade.

The Verdict:

The “Spirit of Dialogue” at Davos 2026 is not a celebration of unity, but a desperate attempt to establish “guardrails” for competition. The era of convergence is over. We have entered the era of Managed Coexistence, where trade is no longer free, but carefully negotiated, monitored, and weaponized. The winners in 2026 will not be those who wait for the old world to return, but those who aggressively adapt to the new logic of industrial nationalism.