In the unforgiving economic climate of early 2026, the era of “growth at any cost” has been definitively replaced by a mandate for “profitability at all costs.” As global interest rates stabilize at historically elevated levels and regulatory scrutiny intensifies across major markets, the neobanking sector stands at a critical juncture. The once-promising digital challengers face an existential bifurcation: evolve into fully chartered, deposit-rich financial institutions or face acquisition, liquidation, and obsolescence. This analysis dissects why the digital-only banking model is under historic pressure and identifies which players are positioned to weather the storm.

Key Takeaways

- The Profitability Pivot: Valuation metrics in 2026 have shifted entirely from vanity metrics like “daily active users” to hard financial ratios like Net Interest Margin (NIM) and Return on Equity (ROE).

- The Compliance Wall: Stringent new regulatory frameworks in the EU, UK, and US (specifically regarding Banking-as-a-Service oversight) have forced neobanks to triple their compliance spending, eroding the “lean cost structure” advantage they once claimed.

- The “Great Threshing”: We are witnessing a massive consolidation wave where mid-tier neobanks are being acquired by traditional incumbents seeking better tech stacks, while “zombie fintechs” without distinct value propositions quietly exit.

- Interest Rate Paradox: While high rates theoretically boost lending income, they have exposed neobanks’ critical weakness: a lack of “sticky,” low-cost operational deposits compared to traditional banks.

- Trust as the New Currency: Consumer trust has become a volatile commodity, with users increasingly migrating primary salary deposits back to perceived “too big to fail” institutions while relegating neobanks to discretionary spending roles.

The Great Correction: How We Got Here?

To fully grasp the magnitude of the 2026 neobanking crisis, one must trace the trajectory from the exuberant days of 2021 to the present reality. During the Zero Interest Rate Policy (ZIRP) era, neobanks flourished on a steady diet of venture capital subsidies. They aggressively acquired customers by offering fee-free accounts, high-yield savings (often subsidized by VC cash), and slick mobile interfaces. Investors rewarded “growth” above all else, often ignoring unit economics.

However, the persistent inflation fight of 2023-2025 fundamentally altered the mathematical reality of banking. As central banks across the Federal Reserve, ECB, and Bank of England hiked rates and held them higher for longer, the cost of capital soared. Venture funding for late-stage fintechs dried up, dropping by over 60% by late 2025. Simultaneously, the “primary account problem” became glaringly obvious. Most consumers kept their salaries in traditional banks (using them as secure vaults) while using neobanks merely for travel or discretionary spending (using them as digital wallets).

In a high-interest environment, this behavior is fatal. Traditional banks are now earning massive interest income on those sticky salary deposits, which they pay little interest on. Neobanks, conversely, must fight for deposits by offering 4% or 5% yields, crushing their margins. The “freemium” model that defined the last decade of fintech has effectively collapsed, forcing a mature, albeit painful, reckoning for the industry.

The Profitability Paradox: High Rates and the Deposit Battle

The central challenge for neobanking stability in 2026 is the widening, often fatal, gap between Customer Acquisition Cost (CAC) and Average Revenue Per User (ARPU). For years, the prevailing logic was that once a user is acquired, they could eventually be cross-sold into high-margin lending products like mortgages or personal loans. The data from 2025 and early 2026 shows this pivot has been far harder than anticipated.

High interest rates have a dual effect. While they allow banks to charge more for loans, they also increase the risk of consumer default. Neobanks, many of which lack the decades of credit risk data possessed by century-old incumbents, have been forced to tighten lending standards just when they need to lend the most to generate revenue. Furthermore, their funding costs are significantly higher. A traditional bank like JPMorgan or HSBC sits on trillions of dollars of deposits that cost them near zero percent interest. A neobank, to attract that same capital, must offer market-leading rates. This is known as “deposit beta”—and for neobanks, the beta is dangerously high.

Recent market reports indicate that less than 15% of the global neobank cohort is operating profitably on a GAAP basis. The market has bifurcated into “Full-Stack Winners” who secured banking licenses and built robust lending engines, and “Interchange Dependents” who rely on swipe fees and are slowly bleeding cash.

The Winners vs. The Strugglers

| Feature | The Scaled Winners (e.g., Starling, Monzo, NuBank) | The Struggling Mid-Tier (Generic “Spend” Apps) | Traditional Incumbents (Digital Arms) |

| Primary Revenue Source | Net Interest Income (Lending, Mortgages, SME Credit) | Interchange Fees (Payments only) & Subscriptions | Net Interest Income & Wealth Management Fees |

| Average ARPU | $50 – $150+ annually | < $15 annually | $250 – $400+ annually |

| Banking License | Full Banking Charter (Direct relationship with Central Bank) | Partner/Sponsor Bank Dependence (BaaS Model) | Full Banking Charter |

| Cost of Funds | Low (Access to direct consumer deposits) | High (Reliance on wholesale funding or partner banks) | Ultra-Low (Legacy “sticky” deposits) |

| 2026 Strategy | IPO readiness; M&A acquisitions of smaller rivals | Pivot to B2B niche or “Fire Sale” exit | Buying fintech tech stacks; Closing branches |

The Regulatory Reckoning and Compliance Costs

In 2026, regulation has become the single biggest line item on a neobank’s Profit & Loss statement. The “move fast and break things” ethos is officially dead. Following the high-profile fintech failures and compliance lapses of 2024 and 2025, regulators such as the Consumer Financial Protection Bureau (CFPB) in the US and the Financial Conduct Authority (FCA) in the UK have imposed strict “operational resilience” standards.

This regulatory siege impacts stability in two critical ways:

- The BaaS Crackdown: Regulators are now aggressively penalizing “Banking-as-a-Service” (BaaS) partner banks for the compliance failures of the fintechs they sponsor. This has created a chilling effect known as “de-risking.” Partner banks are offboarding risky fintech clients to avoid regulatory wrath, leaving many neobanks without a license to operate overnight. The cost of “renting” a charter has skyrocketed, squeezing margins further.

- Anti-Money Laundering (AML) Costs: As digital fraud becomes increasingly sophisticated—driven by AI-generated identity theft—the cost of AML and Know Your Customer (KYC) checks has exploded. Traditional banks can amortize these massive infrastructure costs across trillions in assets and millions of customers. A neobank with a smaller balance sheet cannot absorb these fixed costs as easily, putting them at a structural disadvantage.

Key Regulatory Milestones Impacting Neobanks (2024-2026)

- 2024 (Q4): Enhanced “Third-Party Risk Management” guidelines issued by US banking regulators, effectively making sponsor banks liable for every action of their fintech partners.

- 2025 (Q2): Implementation of stricter capital adequacy requirements for digital-only banks in the EU, forcing many to raise capital at lower valuations.

- 2025 (Q4): The “BaaS Purge,” where several major sponsor banks announced they would cease onboarding new fintech programs to focus on compliance remediation.

- 2026 (Current): Introduction of “real-time fraud reporting” mandates, requiring significant investment in AI-driven monitoring tools.

The Great Consolidation: Winners, Losers, and M&A

We are currently in the midst of the “Great Threshing.” Market sentiment has shifted from optimism to pragmatic skepticism. The days of a thousand different neobanks—one for musicians, one for pet owners, one for gamers—are ending. The market simply cannot support that level of fragmentation in a high-cost environment.

However, this does not mean the death of fintech; rather, it signifies its maturation. The “unbundling” of the bank that characterized the 2010s is being reversed by a massive “re-bundling.” Consumers are experiencing “app fatigue.” They are tired of checking five different apps to manage their finances. They want a single “Super App” that handles spending, saving, investing, and borrowing. The surviving neobanks are those that have successfully built this ecosystem.

Meanwhile, traditional Tier-2 and Tier-3 banks are on a shopping spree. They are acquiring distressed neobanks not for their customer bases (which are often low-value), but for their tech stacks. It is often cheaper and faster for a regional bank to buy a failing neobank to acquire its modern, cloud-native core banking system than it is to attempt a risky internal migration from legacy COBOL systems.

M&A Drivers in 2026

| Buyer Archetype | Motivation | Target Type |

| Global Mega-Bank | Acquiring specific product capabilities (e.g., BNPL engines, AI fraud detection). | High-performing niche fintechs. |

| Regional Bank | Modernizing legacy IT infrastructure (“Acqui-hire” of engineering teams). | Distressed neobanks with great tech but poor unit economics. |

| Dominant Neobank | Eliminating competition and acquiring banking charters in new geographies. | Smaller local competitors. |

| Private Equity | stripping assets and consolidating portfolios for operational efficiency. | Mid-tier neobanks with steady but stagnant cash flows. |

Technological Divergence and the Future of Trust

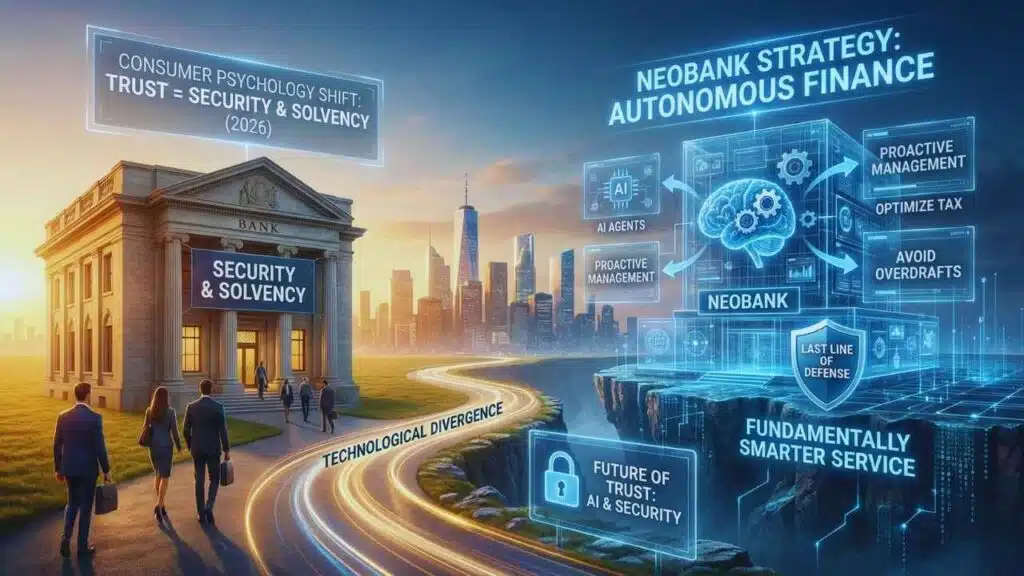

Beyond economics and regulation, a subtle but profound shift is occurring in consumer psychology. In the early 2020s, “trust” was synonymous with “good user experience.” If an app was fast and didn’t crash, users trusted it. In 2026, after waves of cyberattacks and the collapse of several high-profile shadow banks, the definition of trust has reverted to “security and solvency.”

Consumers are increasingly asking: “Is my money safe if a crisis hits?” This flight to safety favors incumbents. While neobanks have superior technology for spending, traditional banks are winning the war for saving.

To combat this, leading neobanks are doubling down on “Autonomous Finance.” They are moving beyond simple data visualization (pie charts of your spending) to proactive financial management. Using advanced AI agents, these apps now automatically switch users to better utility providers, optimize tax harvesting, and manage cash flow to avoid overdrafts. This technological divergence is the last line of defense for neobanks. If they cannot offer a service that is fundamentally smarter—not just prettier—than a traditional bank, they have no reason to exist in a high-rate world.

Future Outlook: What Happens Next?

As we look toward the remainder of 2026 and into 2027, three distinct trends will define the trajectory of neobanking stability:

- The Rise of the “Specialist” Charter: Generalist neobanks will continue to fade. The most successful new entrants will be highly specialized vertical banks (e.g., banking for the healthcare industry, cross-border banking for the global gig economy) that can underwrite specific risks better than any generalist algorithm.

- The End of Free Banking: The “freemium” model will be largely abandoned. Expect to see the normalization of monthly subscription fees (SaaS-ification of banking) as the primary revenue driver for neobanks. Users will pay $10-$20/month for a bundle of premium AI-driven financial services, replacing the reliance on hidden interchange fees.

- The “Super App” Endgame: The surviving giants (the top 2-3 in each region) will cease to be just “banks.” They will become lifestyle operating systems, monetizing data, media, and commerce rather than just relying on spread lending. They will resemble Asian super-apps more than Western banks.

The question is not “Will neobanks survive?” but “Which type of neobank will survive?” The era of the digital wallet masquerading as a bank is over. The survivors of 2026 will be those who successfully transitioned from being a secondary spending app to a primary financial hub, backed by robust balance sheets, rigorous compliance frameworks, and a clear path to Net Interest Income. For the rest, the high-interest volatility of 2026 will likely be the final curtain.