The end of the “wild west” of remote work is here. As 2026 dawns, Europe’s most popular digital nomad destinations are pivoting from broad attraction to strict regulation, forcing a massive operational shift in wealth management. With Italy’s proposed “Digital Nomad Tax Bonus” debating strict income thresholds and Portugal’s NHR regime fully sunsetted for new entrants, the era of easy tax arbitrage is over.

For high-net-worth mobile talent, the question is no longer just “Where can I go?” but “How do I survive the compliance minefield?” This analysis explores why wealth managers are now becoming cross-border legal architects.

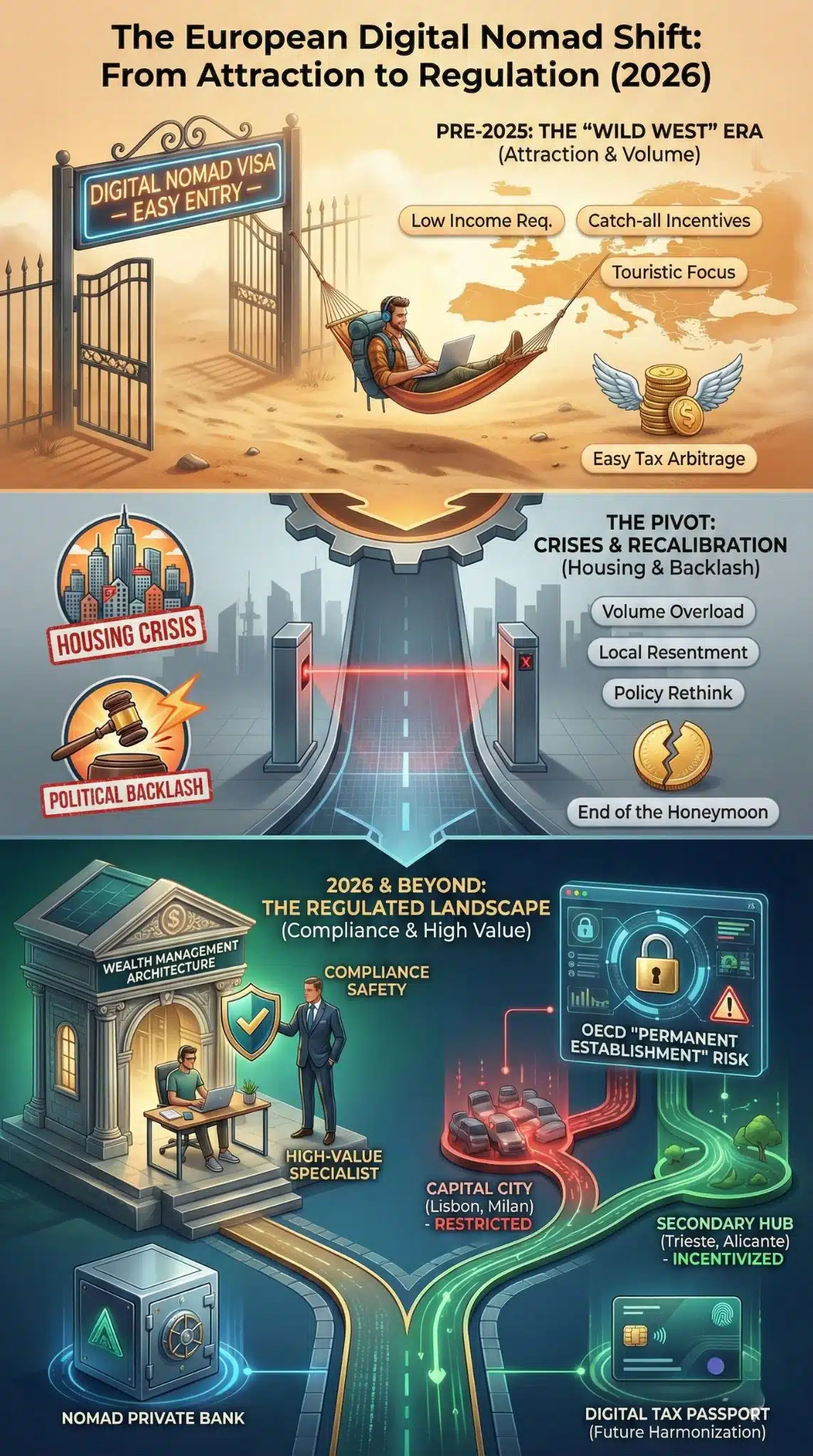

The End of the Honeymoon: How We Got Here

The narrative of the digital nomad has shifted dramatically between 2020 and 2026. Following the pandemic, countries like Portugal, Spain, and Greece raced to replenish tourism-starved coffers by offering “Digital Nomad Visas” (DNVs) with low income requirements and generous tax breaks. It was a volume game: attract as many remote spenders as possible.

However, by late 2024, the side effects became politically untenable. Housing crises in Lisbon, Milan, and Malaga sparked local backlash, leading governments to recalibrate. 2025 marked the turning point where “attraction” was replaced by “curation.” Governments now want quality over quantity—high earners who contribute to the tax base rather than just consuming infrastructure. Today, we are seeing the maturation of this policy shift: the digital nomad is no longer a backpacker, but a recognized, regulated, and taxable asset class.

1. The Policy Shift: From Volume to Value

The most significant trend in 2026 is the aggressively tiered nature of new immigration policies. Italy’s 2026 budget discussions regarding a “Digital Nomad Tax Bonus” exemplify this.1 Unlike previous catch-all incentives, the new proposals are anticipated to target “highly skilled” profiles with rigorous educational or income benchmarks, specifically designed to align with the country’s need for human capital, not just consumption.

This mirrors the closure of Portugal’s Non-Habitual Resident (NHR) program to new entrants in 2024, replaced by a much narrower “scientific and innovation” tax regime. The message is clear: Europe is open for business, but only if you are high-value. Wealth management firms are responding by creating “migration desks” that pre-screen clients not just for investment potential, but for visa eligibility, treating residency permits as a form of alternative asset class.

2. The “Permanent Establishment” Trap

The hidden crisis for 2026 is corporate risk. The OECD’s 2025 updates to the Model Tax Convention have tightened the definition of a “Permanent Establishment” (PE).2 Previously, a remote worker sitting in a boundless “somewhere” was a grey area. Now, if a senior executive or a high-revenue generator spends more than 50% of their time in a foreign jurisdiction, they risk creating a taxable corporate presence for their employer in that country.

Wealth managers are no longer just managing personal portfolios; they are advising business owners on workforce liability. A client moving to Spain under the Beckham Law might save personal tax, but if they trigger a 25% corporate tax bill for their UK company because their home office is deemed a “fixed place of business,” the strategy fails.

3. The Rise of “Compliance-as-a-Service”

In response to the complexity, the wealth management value proposition has shifted. Investment returns are secondary to compliance safety. Firms are deploying AI-driven “day-counting” apps integrated into banking platforms to track tax residency in real-time.

Private banks are moving away from “don’t ask, don’t tell” regarding client location. With the EU’s Directive on Administrative Cooperation (DAC) expanding to cover crypto-assets and e-money, visibility is total. The new service model involves “multi-jurisdictional simulation”—using software to predict how moving from Florence to Valencia in October affects the client’s total tax liability for the fiscal year.

4. The Housing Market Friction

Wealth management is also having to address the reputational and financial risks associated with local housing markets. High-net-worth nomads are increasingly blamed for gentrification. In cities like Barcelona and Amsterdam, local resentment has translated into regulatory risk—bans on short-term rentals or surtaxes on non-primary residences.

Advisors are now steering clients toward “secondary” hubs—Trieste instead of Milan, Valencia instead of Barcelona—to mitigate cost-of-living arbitrage and avoid the political heat of capital cities. This “geographic diversification” is becoming a standard part of the relocation advisory package.

5. Technology: The Great Equalizer and Enforcer

Technology is playing a dual role. For tax authorities, data sharing between border control and revenue agencies is becoming seamless. If you enter the Schengen zone, the clock starts ticking. For wealth managers, “WealthTech” is the defense. New platforms allow for the “tokenization” of residency rights and the automated filing of cross-border tax returns. The “Digital Nomad Visa” is evolving from a physical sticker in a passport to a digital status linked directly to tax IDs, requiring real-time management.

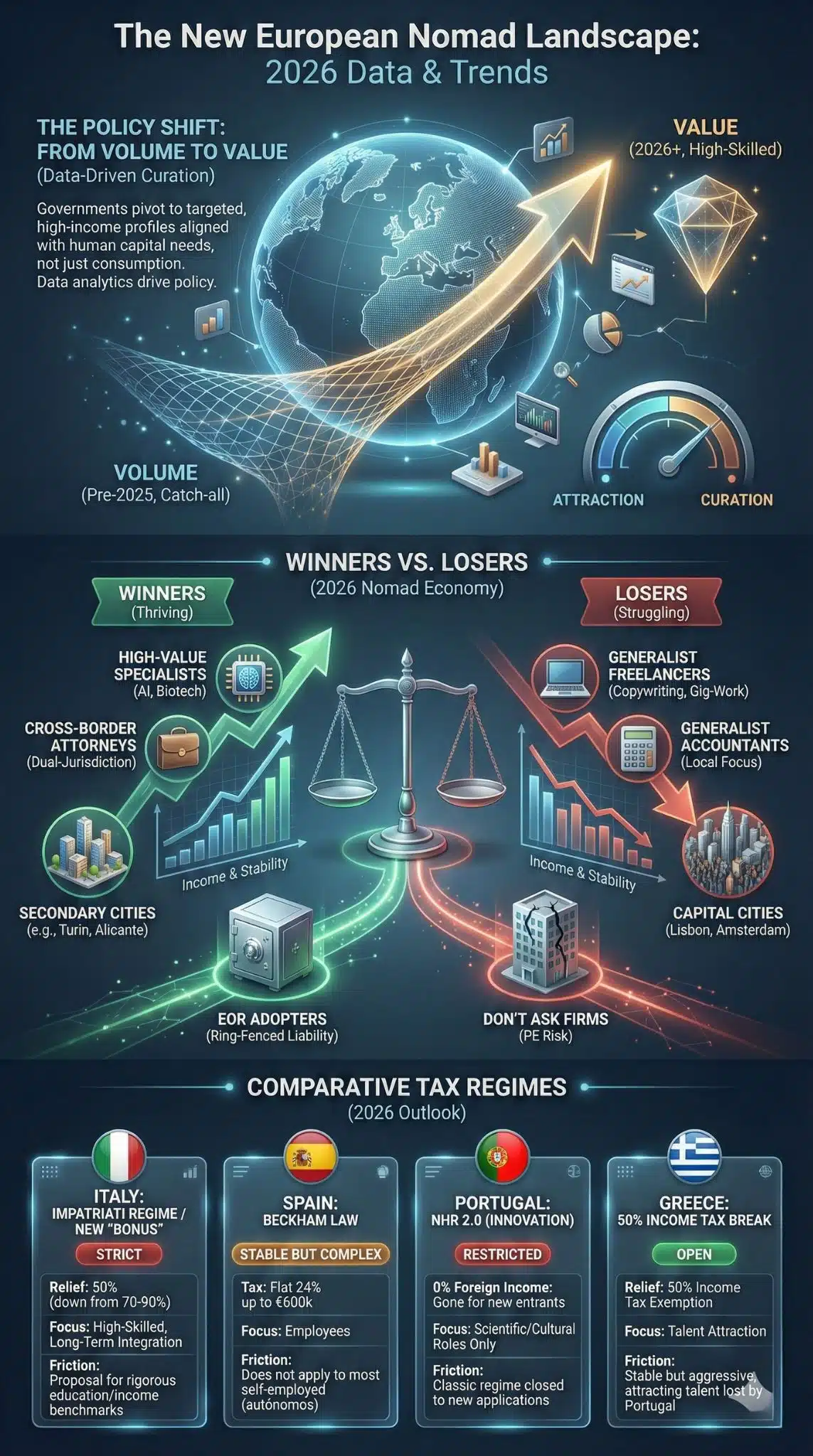

Data & Visualization: The New Landscape

To understand the magnitude of these changes, we must look at the winners and losers of the 2026 regulatory environment, and compare the current tax regimes.

Winners vs. Losers in the 2026 Nomad Economy

| Category | Winners (Thriving) | Losers (Struggling) |

| Profile | High-Value Specialists: AI researchers, biotech execs, and founders with >€100k income. | Generalist Freelancers: Copywriters, graphic designers, or gig-workers earning <€30k. |

| Service Providers | Cross-Border Tax Attorneys: Firms offering dual-jurisdiction liability shielding. | Generalist Accountants: Local CPAs unable to navigate international treaties. |

| Destinations | Secondary Cities: Places like Turin (Italy) or Alicante (Spain) offering incentives without housing crises. | Capital Cities: Lisbon, Amsterdam, and Dublin where housing costs have triggered restrictive policies. |

| Corporate Strategy | EOR Adopters: Companies using “Employer of Record” services to ring-fence liability. | “Don’t Ask” Companies: Firms ignoring employee location, risking massive OECD “PE” fines. |

Comparative Tax Regimes for Nomads (2026 Outlook)

| Country | Key Visa/Tax Regime | 2026 Status & Friction Points |

| Italy | Impatriati Regime / New “Bonus” | Strict: New proposal likely requires “highly skilled” status. 50% tax relief (down from previous 70-90%). Focus on long-term integration. |

| Spain | Beckham Law | Stable but Complex: Flat 24% tax up to €600k. Key friction: Does not apply to most self-employed (autónomos), favoring employees only. |

| Portugal | NHR 2.0 (Innovation) | Restricted: The classic 0% tax on foreign income is gone for new entrants. Now limited to specific scientific/cultural roles. |

| Greece | 50% Income Tax Break | Open: Remains one of the most aggressive, offering a 50% income tax exemption for 7 years to attract talent lost by Portugal. |

Expert Perspectives

The industry is divided on the long-term viability of these strict measures.

The Government View: “We cannot sustain public services if temporary residents use infrastructure without contributing proportionally. The 2026 reforms are about fairness—aligning the contribution of mobile workers with the benefits they enjoy.” — Ministry of Finance Spokesperson (Composite View).

The Wealth Manager View: “The era of the ‘digital gipsy’ is over. Our clients are now ‘jurisdictional shoppers.’ They treat tax residency like an investment portfolio—diversified and hedged. Our role has shifted from asset allocation to liability allocation.” — Senior Partner, Zurich-based Family Office.

The Corporate Risk View: “The OECD’s new guidance on Permanent Establishment is a sleeping giant. We are advising corporate clients to ban ‘stealth’ remote work entirely. If you move, you must switch to a local contract or a B2B contractor setup. The risk of creating a taxable branch by accident is too high.” — International Tax Counsel, Big 4 Firm.

Future Outlook: What Happens Next?

Looking ahead to 2027 and beyond, three key developments are likely:

- The “Tax Passport”: The EU may move toward a standardized “Remote Worker Tax Directive” to prevent a race to the bottom between member states. This would harmonize definitions of tax residency and social security for digital nomads.

- Wealth Management Consolidation: We will see the emergence of “Nomad Private Banks”—boutique firms exclusively dedicated to clients with no single fixed address, offering products like “global health insurance + multi-currency mortgage” bundles.

- The Corporate Clawback: Major corporations may start reducing remote work flexibility, not because of productivity, but because of tax compliance costs. “Work from Anywhere” will likely become “Work from These 5 Approved Jurisdictions.”

Key Takeaways

- The Party is Over: The “Wild West” era of tax-free remote work in Europe has ended; 2026 is defined by strict income thresholds and compliance.

- Corporate Risk is High: Employers face “Permanent Establishment” risks if staff work abroad, making them reluctant to approve moves without legal safeguards.3

- Wealth Management is Legal: Financial advice for nomads is now 80% legal/tax compliance and only 20% investment strategy.

- Secondary Cities Win: Expect a migration shift away from capitals (Lisbon/Rome) to secondary cities to avoid housing market regulations.

Final Thoughts

The landscape of European mobility has matured. For the wealth management industry, the digital nomad is no longer a fringe niche but a complex, high-stakes client segment requiring sophisticated cross-border architecture. The “Digital Nomad Tax” is not just a fee—it is the price of admission to a new, regulated lifestyle.