Do you check your credit report at the three major credit bureaus and hold your breath? You work hard to keep a top credit score, but one late payment can cost you. We share Proven Strategies To Maintain An 800+ Credit Score.

Only 23% of Americans reach an 800 FICO Score. We cover on-time payments, low credit utilization, and a diverse credit mix. We teach you to scan your credit report, spot errors, and pay bills on time, every time.

You get clear tips to lock in your score. Keep reading.

Key Takeaways

- Only 23% of Americans reach an 800+ FICO score. Pay every bill on time to protect the 35% of your score tied to payment history. Use a mobile app or calendar reminders to set up auto-pay.

- Keep your credit use below 30% of each card’s limit. Top scorers average 11.5%. Spread charges across cards, pay high-interest balances first, and ask for higher limits after on-time payments.

- Leave old credit cards open. The length of credit history makes up 15% of your FICO score. No-fee cards can sit idle to boost your account age and lower your overall credit utilization ratio.

- Build a diverse mix of credit. Credit cards, auto loans, mortgages, and credit-builder loans count for 10% of your score. Weigh rates before you apply, keep balances under 30%, and pay on time every month.

- Monitor your credit reports weekly at AnnualCreditReport.com and check Experian, TransUnion, and Equifax. Scan for errors, dispute mistakes within 30 days, and limit hard inquiries to guard your score.

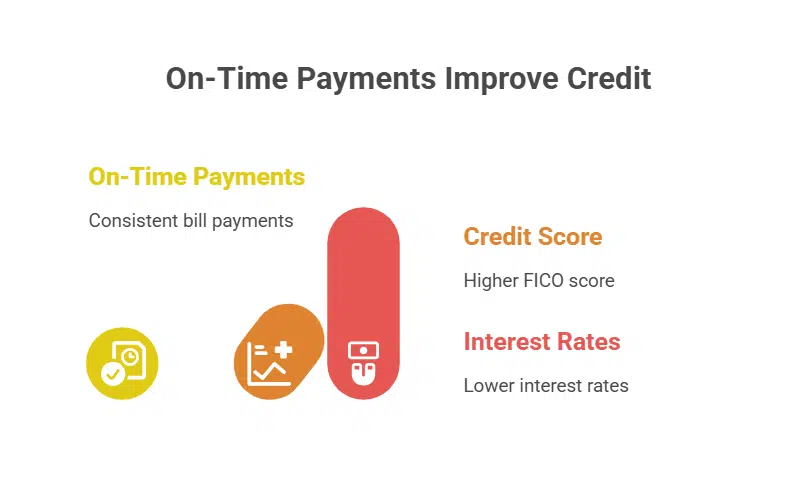

Pay Your Bills on Time

Paying bills on time shapes your payment history. Lenders check this history when they review your credit scores. Missing a due date by thirty days triggers a late mark on your credit report.

Late marks often trigger higher interest rates. That hit can shave points off your FICO Score, since 35 percent of that score rests on payment history.

A mobile application helps set up auto-pay. A calendar reminder nips a missed payment in the bud. That on-time payment history reassures credit bureaus you handle debts well.

Maintain a Low Credit Utilization Ratio

Keeping credit card balances low helps your FICO Score, and it also eases stress on your wallet. This ratio makes up 30% of your credit scoring models, so it packs a punch. Aim for use below 30%, but top scorers hit 11.5% on average.

You can track this on your credit reports, or through online tools at big bureaus.

Spread small charges across each line of credit, so no account looks greedy. A friend jokes that her cards felt jealous when she used just one. Ask for a higher credit limit after you show solid on-time payments, that move gives you more room to breathe.

Focus payments on high-interest balances first, watch that ratio fall.

Keep Old Credit Accounts Open

Old statements act like a treasure map. They show a long credit history that supports your FICO Score. Credit scoring models look at length of credit history. This part accounts for 15% of the final score.

Closing a line of credit lifts your credit utilization ratio. A high ratio can drag down your credit score.

Credit cards with no annual fee often sit idle. You can snap a card open again if you need more credit limit. A credit bureau records each active line. That history shows lenders you handle debt.

It also keeps your credit utilization ratio low. This approach adds depth to your credit report.

Diversify Your Credit Portfolio

Installment loans like auto loans or personal loans boost your credit mix. Mortgages and credit cards also shape a strong profile. Credit mix makes up ten percent of your FICO Score.

Lenders view a healthy blend as proof of on-time payments.

Try adding a small secured credit card or a personal line of credit. Weigh interest rates before new approvals. Keep all accounts open, pay down balances under thirty percent of your credit limit.

Credit bureaus such as Experian, TransUnion, and Equifax record each account.

Monitor Your Credit Reports Regularly

You must guard your credit report. Small mistakes can drag your FICO score down fast.

- Request one free credit report each week at AnnualCreditReport.com to catch errors before they fester.

- Open accounts with Experian, TransUnion, and Equifax for live updates from major credit agencies.

- Scan each record like a detective to protect your credit history from wrong balances and ghost accounts.

- Dispute errors with each agency within 30 days to clear false marks and wrong payment history.

- Watch FICO score trends and credit scoring models to spot odd swings in your credit utilization.

- Enable email or text alerts for new hard inquiries and data breach warnings on your accounts.

Avoid Applying for Too Much New Credit

Too many credit applications send red flags. Each hard inquiry can shave points off your FICO score, because new credit makes up 10% of the total. Lenders view a cluster of inquiries as a sign of financial distress, so they may hesitate on credit approval.

Choose only needed credit card or installment loan accounts. A single application for an auto loan or a new credit card can eyecover expenses. Use a credit monitoring tool to watch your credit report for recent hits, and limit requests to times you must.

Credit bureaus log every check, so guard your score like treasure.

Set Up Automatic Payments for Consistency

Set up autopay and clear utilities, mortgage, and credit card bills on time each month. Online bank portals let you pick dates and amounts. A silent helper takes care of chores while you rest, so you dodge late fees and high-interest debt.

Automatic debit boosts your payment history and lifts your credit score. Federal Reserve data shows on-time payments help maintain an excellent FICO score and protect your credit limit.

Mobile apps from a major card network let you schedule transfers to cover auto loans or installment loans. You choose a due date, link your checking account, and tap save. Text or email alerts warn you if a transfer fails.

This habit trims your credit utilization ratio and keeps large balances at bay.

Limit Large Credit Card Balances

Low credit usage helps boost your FICO score. Aim for a credit utilization ratio below 30 percent on each revolving account. Spread balances across cards like peanut butter on bread so no single credit limit shows a giant balance.

Pay full credit card balances each month to escape high-interest debt. Keep several credit cards open and active, and your total credit limit will grow.

Check your credit utilization on a free credit report or score tool at each credit bureau. That quick glance spots a surprise balance before it hurts your payment history. Installment loans or auto loans sit outside this ratio, but new credit cards count right away.

Stop swiping once you hit the 30 percent line, and you keep that payment history clean.

Takeaway

Maintaining an 800+ credit score is not just about reaching a milestone—it’s about consistently practicing the right financial habits to preserve it. By following these 12 proven strategies, you can safeguard your excellent rating, enjoy better loan terms, and open the door to exclusive financial opportunities. Whether it’s paying bills on time, keeping credit utilization low, or monitoring your reports regularly, every step you take strengthens your credit health. Stay disciplined, review your progress often, and your exceptional score will continue to work in your favor for years to come.

FAQs on Strategies To Maintain An 800+ Credit Score

1. What are the key factors that shape an 800+ FICO score?

Your payment history, credit utilization ratio, length of credit history, new credit steps, credit mix, and credit report details form your FICO score.

2. How do on-time payments help me keep a good credit score?

You pay each credit account on time, every time, and avoid late payments. This boosts payment history and shows lenders you mean business.

3. What limit should I use for my credit cards?

Aim to use less than 30 percent of your credit limit. Spread your card balances across lines of credit to keep credit utilization low.

4. Why do I need different types of credit?

A mix of vehicle loans, fixed payment loans, and credit cards tells credit bureaus you can handle many credit accounts. It adds depth to your credit mix.

5. How do new credit and hard inquiries affect my score?

Each hard inquiry and new credit request may knock points off. Avoid opening too many lines of credit at once, or your score could dip.

6. Why should I check my credit report often?

Think of your credit report like a report card. Review it for wrong late payments, data breach hits or other errors, then dispute errors fast to protect your excellent credit score.