Have you ever tried sending money overseas and felt completely frustrated by the slow speed and high fees? It is a common headache. Exchange rates jump up and down constantly. Your payment might even get held up for days without any explanation. Many people feel locked out of the global financial system or worry about losing their hard-earned value with every transfer. Stablecoins can help fix these exact problems. In my years analyzing digital assets, I have found that having a reliable way to send funds is life-changing for many families. In 2025 alone, the total stablecoin market cap surged past $311 billion. This number keeps growing rapidly as more people seek faster, safer ways to send digital currency.

I am going to walk you through exactly how Stablecoins in Global Finance work. You will learn what these tokens are all about and see how they bring much-needed stability to payments. So, grab a cup of coffee, and let’s go through it together. I will show you everything you need to know in a simple, step-by-step way.

What Are Stablecoins?

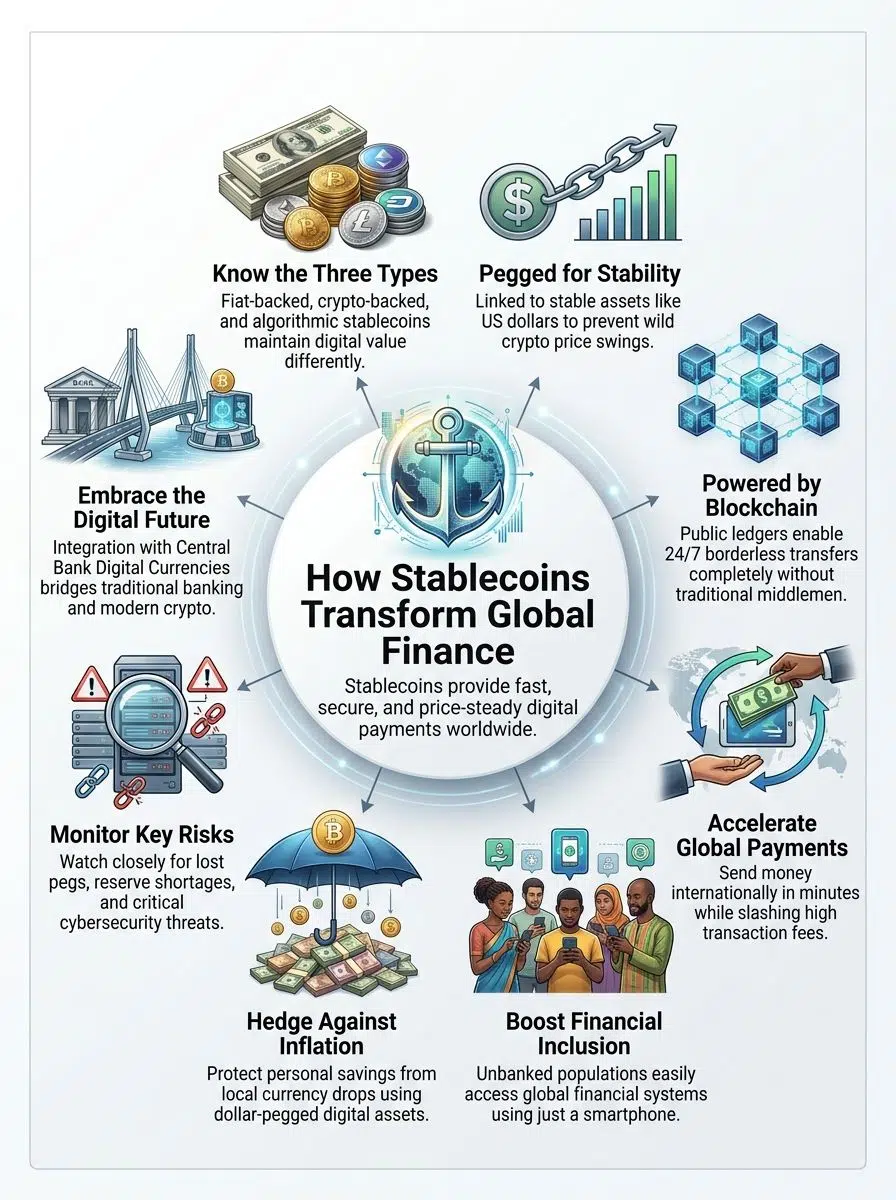

Stablecoins are types of digital money that try to keep a steady value. They work using different methods to avoid the wild price swings usually found with other cryptocurrencies.

Definition of Stablecoins

A stablecoin is a unique type of digital currency. It aims to keep its value steady by linking itself directly to real-world assets like the US dollar or gold. Think of them as a bridge between everyday cash and cryptocurrency. They make payments much smoother and faster for everyone involved.

Many people use stablecoins because they do not swing wildly in price like Bitcoin or Ethereum. Their main goal is to offer stability in payment systems, cross-border transactions, and treasury management. In fact, CoinGecko reported that the total stablecoin market cap hit over $311 billion in late 2025.

As one active trader joked recently, chasing Bitcoin’s price felt like riding a rollercoaster. With stablecoins, they could finally breathe.

Types of Stablecoins: Fiat-Backed, Crypto-Backed, and Algorithmic

After understanding the basics, it is time to zoom in on the different types you will find in digital wallets. Each type tries to maintain its steady price using a different approach. Here is a quick guide that runs through the three main categories.

| Type | How It Works | Example | Strengths | Weaknesses |

|---|---|---|---|---|

| Fiat-Backed |

|

|

|

|

| Crypto-Backed |

|

|

|

|

| Algorithmic |

|

|

|

|

How Stablecoins Work

These digital assets aim to keep their value steady using clever tricks and strong tech. Their secret sits in careful design. This keeps the digital coins extremely close in price to real-world money.

Pegging Mechanism and Stability

A stablecoin uses a pegging mechanism to keep its value steady. Most tie their price directly to the US dollar. For example, Tether (USDT) and Circle’s USD Coin (USDC) currently make up roughly 85% of the entire market. For these two giants, one coin almost always equals exactly $1.

Some issuers keep real cash in reserve for every digital coin out there. Others back their coins with extremely safe assets like US Treasury bonds.

A few older models relied on computer code called algorithms to control supply and demand. However, these algorithmic versions have become less popular due to safety concerns. People simply want a safe harbor from crypto volatility. Pegged stablecoins anchor themselves to real-world assets so users can sleep soundly.

Role of Blockchain Technology

Blockchain acts as the strong backbone for all stablecoins. It records every single transaction in a public ledger. This makes everything transparent and clear to anyone who wants to check.

You can send digital currency across borders with just a simple app and an internet connection. Each step gets verified by many computers spread all over the globe.

This decentralized checking process makes fraud very hard to pull off. Smart contracts help manage the pegging mechanism automatically.

Unlike traditional banks that close at night, blockchain networks work 24/7 without taking breaks. However, transaction costs can vary based on the network you choose.

A 2025 report noted that Ethereum network fees can fluctuate wildly. To beat this, many users now send stablecoins on faster networks like Polygon, where fees drop to a fraction of a cent.

Issuance and Redemption Processes

Stablecoins move in and out of the market through two key steps known as issuance and redemption. These specific actions keep the tokens steady, easy to access, and trusted for daily digital payments.

- To issue new stablecoins, a user gives fiat money to a regulated issuer.

- The issuer takes this money and locks it up safely in a bank. The 2025 US GENIUS Act legally mandates that issuers maintain a strict one-to-one reserve.

- After receiving the funds, the issuer creates an equal number of tokens on a blockchain and sends them to the user.

- These tokens are now ready for instant cross-border transactions or safe treasury management.

- If a user wants their money back, they start redemption by returning their tokens to the issuer.

- The issuer checks the blockchain to confirm the tokens are real.

- The company then permanently removes those tokens from circulation.

- Once confirmed, users get their original fiat currency back into their bank account.

- This system works incredibly fast today. In February 2026, Circle completed $680 million in internal USDC settlements in just 30 minutes.

The Role of Stablecoins in Global Finance

Stablecoins help make money move faster and easier across borders. It feels just like sending a text message instead of mailing a physical letter. They open doors for people who desperately need better ways to pay or save.

Facilitating Cross-Border Payments

Sending money across countries used to take several business days. People paid shockingly high fees and filled out endless forms. Digital currency speeds up this whole process. It makes cross-border transactions much easier for everyone involved.

Money can move at any hour of the day without needing a bank manager’s approval. This amazing change helps families send financial support home fast.

It also lets small businesses pay overseas suppliers in minutes instead of weeks. According to a 2026 World Bank report, the global average cost to send a $200 international remittance remains stubbornly high at 6.49%. In stark contrast, using a stablecoin on a fast blockchain can drop that transfer cost to less than a dollar.

Enabling Financial Inclusion in Underserved Regions

Many people living in underserved regions simply have no access to traditional banks. Digital currency changes that sad story very quickly.

Because a stablecoin runs on a blockchain, anyone with a smartphone and an internet connection can join the global financial system. Farmers in rural Africa use stablecoins for cross-border transactions to avoid expensive local middlemen.

Research shows that roughly 10% of the populations in countries like Kenya and Nigeria are active crypto users. They rely on these digital tools daily. Stablecoins give more than just easy payments. They offer profound financial stability.

Local money may lose its purchasing power overnight due to inflation. Dollar-backed tokens keep family savings safe from those wild swings in volatility.

Reducing Transaction Costs and Delays

Moving away from legacy systems naturally cuts down on fees and wait times. Old payment methods often take days to clear.

With modern blockchain tech, payments settle in seconds regardless of the geographic distance. Here are three specific ways stablecoins are cutting costs today:

- Bypassing SWIFT: Traditional wire transfers use the SWIFT network, which requires multiple intermediary banks. Stablecoins cut out these middlemen entirely.

- Flat Network Fees: Instead of taking a percentage of your transfer, networks like Tron or Solana charge a flat fee that is often under a penny.

- Instant Settlement: Businesses no longer have to tie up working capital for three days while waiting for an international invoice to clear.

Stablecoins as a Tool for Economic Stability

These digital dollars can offer a safe harbor during severe financial storms. You might be surprised at how well they calm wild swings in local value.

Mitigating Currency Volatility in Emerging Markets

People living in emerging markets often watch their local money lose value at a terrifying pace. Digital currencies with a stable value help keep hard-earned savings safe from these wild changes. A worker in Argentina can easily swap local pesos for a stablecoin like USDC or Tether. These tokens stay tied to the U.S. dollar’s value.

This simple action gives families much more control over their financial future. They can completely skip the sudden drops caused by surprise inflation.

Cross-border transactions also get much easier for local businesses. Companies use these digital coins for international deals without worrying about falling exchange rates ruining their profit margins. This creates a powerful new shield against volatility for millions of people worldwide.

Potential as a Hedge Against Inflation

Some stablecoins stay strictly tied to strong assets like the US dollar. These digital currencies help shield money from the rapid price swings seen in weaker local economies.

For example, in countries facing hyperinflation, fast-rising prices can quickly destroy a family’s life savings. Moving those funds into a fiat-backed stablecoin keeps the value steady.

“The ability to hold digital dollars is no longer a luxury for emerging markets; it is an absolute necessity for basic economic survival against inflation.”

Many individuals use stablecoins as a safe digital vault when their own currency loses power. They do not need to rely on local banks that set tight rules or charge huge fees for exchanging money.

The Impact of Stablecoins on Traditional Financial Systems

Stablecoins are shaking up old banks and traditional money rules. This rapid evolution makes many financial leaders wonder exactly what changes are coming next.

Challenges to Central Banks and Monetary Policy

Central banks face totally new hurdles from digital currencies like stablecoins. These coins move incredibly fast between people and across global borders. They can easily skip the usual financial controls. Old tools for managing money flows simply may not work as well anymore.

Interestingly, a 2026 IMF working paper found that massive stablecoin demand actually lowers 1-month US Treasury bill yields by about 1.9 basis points. This proves these tokens are directly impacting traditional bond markets.

People using blockchain-based payment systems might avoid regular banks altogether. This means less data for central authorities who want to track the national money supply. If more folks trust asset-backed coins instead of national currencies, local monetary policy could weaken over time.

Opportunities for Modernizing Financial Infrastructure

While there are challenges, stablecoins also offer massive opportunities to update aging systems. Banks and corporate businesses can move money much faster using this new technology.

Instead of waiting several business days for an international payment to clear, digital currency transactions finish in seconds. This incredible speed makes global trade much less expensive.

To keep up with this incredible innovation, traditional institutions are launching their own upgrades:

- The FedNow Service: The US Federal Reserve launched FedNow to provide instant domestic payments with a low $0.05 fee.

- Tokenized Deposits: Major banks are actively testing ways to turn regular customer deposits into digital tokens.

- Hybrid Networks: Financial giants are building bridges to allow corporate clients to easily swap between traditional bank accounts and digital stablecoins.

Regulatory Landscape for Stablecoins

The legal rules for stablecoins are finally taking a clear shape. These new laws will absolutely determine how fast this technology grows in the future.

Current Regulatory Approaches

Lawmakers in the United States recently took massive steps to treat stablecoins like highly regulated financial instruments. The passing of the GENIUS Act in July 2025 completely changed the US market.

Here is a quick look at how different regions are handling these digital assets today:

| Region | Key Legislation | Main Requirement |

|---|---|---|

| United States | The GENIUS Act (2025) | Requires strict 1-to-1 fiat reserves and bans new algorithmic stablecoins. |

| European Union | MiCA Regulation | Enforces strict liquidity rules and caps the daily transaction volume of non-Euro stablecoins. |

| Japan | 2022 Payment Services Act | Restricts stablecoin issuance strictly to licensed local banks and registered trust companies. |

The Need for Global Standards and Interoperability

While individual countries are passing laws, every nation still has its own unique rulebook. This global patchwork creates massive confusion for developers.

It also slows down the adoption of digital payments. Banks and crypto wallets often cannot communicate easily because they use completely different legal formats.

Global standards are desperately needed to make sure stablecoins work the same way everywhere. Interoperability lets different blockchain platforms connect smoothly.

This ensures that someone in Nigeria can easily send digital currency to a supplier in the United States without any technical glitches. Strong, unified standards also help stop financial scams across different markets.

Risks and Challenges Associated with Stablecoins

Despite their massive benefits, stablecoins still face several serious hurdles. Keeping their promised value steady and protecting user data remain top priorities.

Stability Risks and Collateral Concerns

Some digital currencies promise a steady value, but things can go wrong if the backing assets lose their worth. Tether faced heavy questions in the past about whether it held enough actual cash to cover all its tokens.

If users panic and rush to sell their coins all at once, the price can drop off a cliff. We saw this exact nightmare scenario in late 2025 when a high-yield token called USDe lost 57% of its market cap in just a few weeks.

The token temporarily lost its peg, destroying investor trust instantly. Holding lots of real money in a highly regulated bank vault gives users comfort. Systems need tight daily checks plus simple ways for people to withdraw their funds without any delays.

Privacy and Security Issues

People highly value fast digital payments, but they also deeply worry about who can see their personal data. Stablecoins record every transaction on a public blockchain for anyone to view.

This massive transparency puts personal information at risk if a user does not protect their wallet addresses carefully. Hackers constantly target weak spots in exchanges, sometimes stealing millions in a matter of minutes.

To keep your digital currency safe, always avoid these common security mistakes:

- Reusing Passwords: Never use your standard email password for your digital crypto wallet.

- Ignoring Two-Factor Authentication: Always require a secondary code from your phone to approve any outbound transfer.

- Clicking Suspicious Links: Phishing scams trick users into connecting their wallets to fake websites that drain their funds instantly.

Potential for Market Manipulation

Large token holders can quickly move the price of a smaller stablecoin if they buy or sell in massive amounts. Sometimes, these aggressive moves happen on purpose to trick regular retail traders.

Bad actors often spread false news online to push frightened users into panic selling. This malicious activity can cause a token’s price to drop far below its supposed one-dollar value.

Furthermore, poor exchange rules make it easy for fake trades to hide the true demand for an asset. Analysts at Mizuho Securities noted in March 2026 that Circle’s USDC actually overtook Tether in adjusted transaction volume. They used this specific metric to filter out automated trading bots and measure genuine human economic activity.

The Future: How Stablecoins Work And Why They Matter For Global Finance

Stablecoins are completely changing how we move money and connect traditional banks. New innovations are arriving at a lightning-fast pace.

Integration with Central Bank Digital Currencies (CBDCs)

Central Bank Digital Currencies, or CBDCs, work like official digital versions of a nation’s cash. Many countries are aggressively testing them right now. Stablecoins will likely link directly with these government digital currencies to make daily payments quicker. For example, China expanded its e-CNY project significantly in 2025.

This helps citizens send money fast across borders without paying big banking fees. Pairing CBDCs with private stablecoins could open exciting new ways for payment systems to connect. People might soon swap between a private stablecoin and a government digital dollar right from their banking app.

Bridging the Gap Between Traditional and Digital Economies

As both CBDCs and blockchain networks grow, stablecoins serve as the ultimate bridge. They effortlessly connect old legacy banking with modern digital payment rails.

“Stablecoins are the necessary translation layer. They allow a 1970s banking system to finally speak the language of the modern internet.”

People can use these tokens for lightning-fast cross-border transactions. They can also swap their physical cash for crypto without breaking a sweat.

Banks are noticing these massive changes. Financial companies now settle international trades in minutes using blockchain software. Small business owners in rural Asia can easily accept online payments from American customers thanks to digital dollars.

Driving Innovation in Payment Systems

Stablecoins are currently sparking the biggest changes in payment systems we have seen in decades. They allow users to send digital currency across borders almost instantly.

You no longer have to wait for a branch manager to open the bank doors on a Monday morning. Mainstream financial giants are fully embracing this technology.

In March 2026, PayPal expanded its PYUSD stablecoin to 70 different international markets. This incredible expansion pushed the token’s market cap to over $4.1 billion.

Merchants use this exact blockchain tech to accept safe payments from around the globe. The stable value makes it much easier for shops to avoid the wild price swings associated with standard crypto. This fantastic innovation helps expand digital payments into parts of the world where traditional banking is still unreliable.

Wrapping Up

People across the globe now rely on digital currencies for their daily business, personal savings, and cross-border transactions. Giant companies already let users send stable value tokens to make international checkout much easier.

Even small community shops in emerging markets accept these assets to avoid the painful price swings of their local money. Advances in blockchain technology make incredibly fast, low-cost payment systems a daily reality for millions.

Each year, trillions of dollars move through cryptocurrency platforms, completely cutting expensive bank fees out of the mix. If you want to understand the future of money, learning exactly how stablecoins in global finance work is your absolute best starting point. While some regulatory risks will always exist, more doors continue to open worldwide for amazing economic stability.