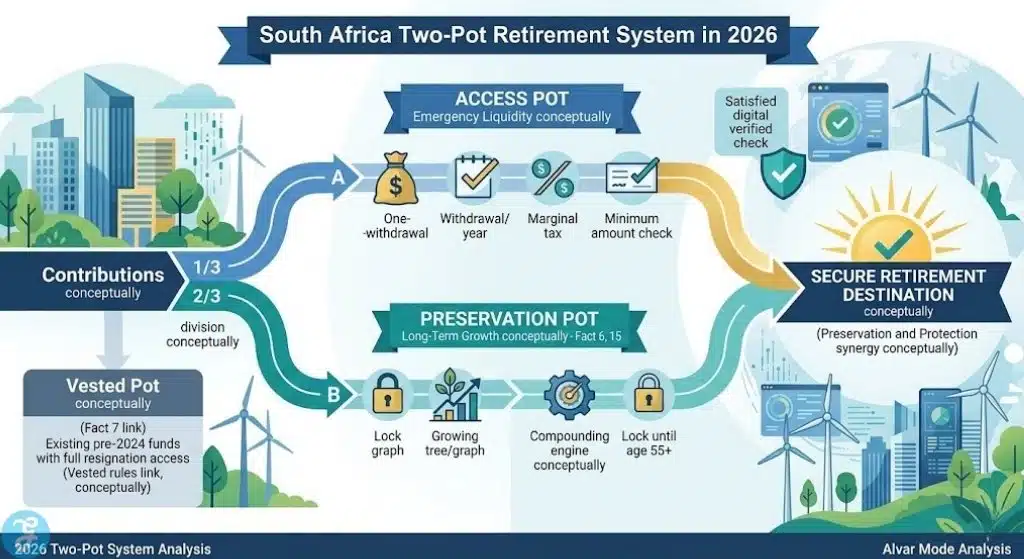

The South African retirement landscape changed forever on September 1, 2024, but as we enter the third full withdrawal cycle on April 1, 2026, the real-world impact is finally coming into focus. The “Two-Pot” system was designed to solve a desperate paradox: South Africans were resigning from their jobs just to access their pensions during financial crises, effectively destroying their future to survive the present. By splitting contributions into a “Savings Pot” for emergencies and a “Retirement Pot” for preservation, the National Treasury has created a hybrid model that demands a much higher level of financial literacy from the average member. In 2026, navigating this system isn’t just about knowing you can withdraw; it’s about understanding the high cost of doing so.

How We Selected Our 17 Best South Africa Two-Pot Retirement System Facts

To build this comprehensive guide, we analyzed the latest 2026/27 tax year directives from SARS and the 18-month performance reviews released by major fund administrators like Sanlam and Old Mutual in March 2026. Our selection criteria prioritized the “hidden” mechanics of the system—such as the interplay between marginal tax rates and the primary rebate, and the long-term compounding loss of sub-R10,000 withdrawals. We also focused on the 2026 “third cycle” behavior, where data shows a shift from panic-withdrawals to strategic liquidity management. These 17 points were chosen to provide a 360-degree view of the system’s benefits, traps, and technical requirements, ensuring you have the data needed to make a “retirement-saving” rather than a “retirement-breaking” decision.

17 Essential Truths About the Two-Pot Retirement System

The following insights break down the technical, fiscal, and behavioral nuances of the South Africa Two-Pot Retirement System in 2026.

1. The One-Withdrawal-Per-Tax-Year Rule

As of today, April 1, 2024, the 2026/27 tax year cycle is officially open. You are entitled to one withdrawal from your Savings Pot every tax year (March 1 to February 28). If you missed your window in the 2025 cycle, that opportunity does not “roll over” into a second withdrawal this year; you still only get one shot at liquidity every 12 months.

Best for: members needing a single, significant injection of emergency cash.

Why We Chose It:

-

It is the most fundamental structural constraint of the new system.

-

It prevents “transactional” use of retirement funds for daily expenses.

Things to consider:

-

If you withdraw R2,000 today, you cannot touch your Savings Pot again until March 1, 2027.

2. The R2,000 Minimum Threshold

To trigger a withdrawal, your Savings Pot must have a balance of at least R2,000. This amount is the gross value before tax and admin fees are deducted. In 2026, many younger members who recently joined the workforce are finding they need at least 6–8 months of contributions to hit this “access floor.”

Best for: entry-level employees tracking their first year of retirement contributions.

Why We Chose It:

-

It sets a clear barrier to entry that protects very small balances.

-

It forces a minimum level of accumulation before the state allows “leakage.”

Things to consider:

-

If your balance is R1,999, the system will automatically reject your application.

3. Taxation at Your Marginal Rate

The most painful surprise for members in 2026 remains the tax bill. Unlike the “Retirement Lump Sum” tables used when you retire (where the first R550,000 is tax-free), Savings Pot withdrawals are added to your annual income and taxed at your marginal rate (18% to 45%). SARS treats this money exactly like a bonus or a salary increase.

Best for: taxpayers who understand that “gross” and “net” are very different numbers.

Why We Chose It:

- It is the government’s primary “nudge” to discourage unnecessary withdrawals.

- It significantly reduces the actual cash that hits your bank account.

Things to consider:

-

A R30,000 withdrawal for a mid-tier earner could lose R7,000+ immediately to tax.

4. The 2026/27 “Tax Bracket Creep” Risk

For the 2026/27 tax year, tax brackets were adjusted by 3.4% for inflation. However, because Savings Pot withdrawals are added to your income, a large withdrawal can easily push you into a higher tax bracket. For example, if you earn R380,000 and withdraw R10,000, your entire “top” portion of income could jump from a 26% to a 31% tax rate.

Best for: members earning near the threshold of a higher tax bracket.

Why We Chose It:

-

It highlights a hidden cost that isn’t apparent until you file your final tax return.

-

It underscores why “maximum withdrawals” are often a poor fiscal choice.

Things to consider:

-

Always use a 2026 tax calculator before clicking “submit” on a claim.

5. Automatic SARS Debt Deduction

If you owe SARS money—whether from an old tax return, a late filing penalty, or an unpaid administrative fine—they will take it directly from your Two-Pot withdrawal before you see a cent. In 2026, SARS has fully integrated its debt management system with the retirement funds’ tax directive process.

Best for: members who have outstanding compliance issues with the tax man.

Why We Chose It:

-

It makes the Savings Pot an accidental “debt collection” tool for the state.

-

It often results in members receiving significantly less (or zero) cash than expected.

Things to consider:

-

Check your “Statement of Account” on eFiling before applying for a withdrawal.

6. The Compulsory “Retirement Pot” Lock

Two-thirds of every cent you contribute from September 2024 onwards is locked in the “Retirement Pot.” In 2026, you cannot access this money under any circumstances until you reach retirement age (usually 55). Even if you resign or are retrenched, this “two-thirds” must be preserved or transferred to a preservation fund.

Best for: long-term protection of your future self.

Why We Chose It:

-

It is the core “preservation” pillar that makes the South Africa Two-Pot Retirement System work.

-

It ends the era of cashing out entire pensions when changing jobs.

Things to consider:

-

This effectively reduces your “liquid” resignation benefit by 66% compared to the old system.

7. The “Vested Pot” Transition Rules

All the money you saved before September 1, 2024, sits in your “Vested Pot.” This pot operates under the “old” rules. If you resign in 2026, you can still take the full cash value of your Vested Pot (subject to the withdrawal tax table), which provides a much-needed bridge for those between jobs.

Best for: long-tenured employees with decade-long savings histories.

Why We Chose It:

-

It honors the “old” social contract for savings accumulated before the reform.

-

It provides a massive liquidity difference between veteran workers and new starters.

Things to consider:

-

Taking cash from the Vested Pot on resignation is still a major setback for retirement.

8. The One-Time Seeding Event (2024)

If you are wondering why your Savings Pot started with a balance in 2024, it was because of “seeding.” 10% of your vested savings (up to a max of R30,000) was moved to kickstart the system. In 2026, this was a one-time event; there is no second “seeding” from your old money into your new savings pot.

Best for: members who were part of a fund before September 2024.

Why We Chose It:

-

It explains the “jump start” many people saw in their accounts.

-

It clarifies that future growth in the Savings Pot must now come from new contributions.

Things to consider:

-

Your Savings Pot now only grows by 1/3 of your current monthly contributions.

9. Admin Fees and the “Small Claim” Trap

Every time you withdraw, your fund administrator (Old Mutual, Momentum, etc.) charges a processing fee. In 2026, these fees usually range from R300 to R600. On a R2,000 minimum withdrawal, a R500 fee plus 18% tax (R360) means you only get R1,140 in your pocket.

Best for: small-balance members tempted by the R2,000 minimum.

Why We Chose It:

-

It highlights the disproportionate cost of small withdrawals.

-

It encourages members to wait until they have a more “efficient” amount to withdraw.

Things to consider:

-

The higher the withdrawal amount, the lower the percentage impact of the admin fee.

10. The 18-Month Engagement Surge

Research from March 2026 shows that member engagement with retirement portals has spiked by over 80% since the Two-Pot launch. Because members can now “see” their money moving into different pots, they are taking a more active interest in fund performance and investment choices.

Best for: administrators and employers looking to improve financial wellness.

Why We Chose It:

-

It is a positive, unintended consequence of the reform.

-

It has transformed retirement funds from “invisible” assets to active digital tools.

Things to consider:

-

Use this engagement to check if your “beneficiary nominations” are up to date.

11. Impact on “Regulation 28” Liquidity

Retirement funds must follow Regulation 28 (asset allocation limits). Because of the annual withdrawal cycles, fund managers in 2026 are keeping higher levels of cash or “liquid” assets in the Savings Pot portion. This ensures they can pay out thousands of claims every March without crashing the fund.

Best for: market-conscious investors concerned about fund stability.

Why We Chose It:

-

It shows the behind-the-scenes engineering required to make the system safe.

-

It slightly alters the “risk-return” profile of the Savings Pot compared to the Retirement Pot.

Things to consider:

-

Your Savings Pot might grow slightly slower than your Retirement Pot due to this liquidity need.

12. The “Provident Fund Over 55” Exception

If you were a member of a provident fund and were 55 or older on March 1, 2021, you were automatically excluded from the Two-Pot system. However, in 2026, you still have the option to “opt-in.” If you don’t opt-in, you continue under the old rules (full access on retirement or resignation).

Best for: older workers near retirement who value the old “all-in-one” flexibility.

Why We Chose It:

-

It protects the retirement plans of those closest to the finish line.

-

It prevents a sudden change in rules for a vulnerable demographic.

Things to consider:

-

If you opt-in, you cannot change your mind later.

13. The “Death Benefit” Consolidation

If you pass away in 2026, the pots are effectively merged for the benefit of your dependents. The Savings, Retirement, and Vested pots are all used to provide for your beneficiaries, either as a lump sum or an annuity, depending on the fund’s rules and the Section 37C process.

Best for: members with families and dependents.

Why We Chose It:

-

It clarifies that the “pots” don’t complicate the death claim process.

-

It ensures that 100% of the accumulated value is available to your heirs.

Things to consider:

-

The trustees of the fund still have the final say on who receives the money based on dependency.

14. Divorce Order Impact

If you are going through a divorce in 2026, the “pension interest” is still calculable across all pots. However, the non-member spouse can only be paid out from the available balance. If you have depleted your Savings Pot through annual withdrawals, there may be less “liquid” cash available for an immediate divorce settlement.

Best for: members undergoing legal changes to their marital status.

Why We Chose It:

-

It is a critical “legal” nuance of the multi-pot structure.

-

It can affect the timing and liquidity of divorce payouts.

Things to consider:

-

The “Retirement Pot” portion may still need to be transferred to the ex-spouse’s preservation fund rather than paid in cash.

15. The Opportunity Cost of “Compound Interruption”

The most significant “hidden” fact of 2026 is the math of lost growth. A R25,000 withdrawal today doesn’t just cost you R25,000; it costs you the 10%–12% annual growth that money would have earned over the next 20 years. In 2026 terms, that R25,000 could have been R250,000 at retirement.

Best for: young members who view the Savings Pot as a “yearly bonus.”

Why We Chose It:

-

It is the single most important long-term financial reality of the system.

-

It helps reframe a “quick win” as a “long-term loss.”

Things to consider:

-

Withdrawing should be the last resort, not the first.

16. Retrenchment Access: The Proposed Phase 2

As of April 2026, National Treasury is still debating “Phase 2” of the reform. The proposal is to allow members who are retrenched (involuntary job loss) to access a portion of their “locked” Retirement Pot if they have no other income. Currently, this is not yet law, so the “lock” remains total.

Best for: workers in volatile industries concerned about unemployment.

Why We Chose It:

-

It signals where the legislation is heading.

-

It addresses the biggest criticism of the system: being “asset rich but cash poor” while unemployed.

Things to consider:

-

Until the law changes, “Retirement Pot” remains 100% inaccessible.

17. Enhanced Digital “Directive” Speed

In 2024, tax directives took weeks. In 2026, the SARS interface with major funds is nearly instantaneous for compliant taxpayers. If your details are correct (Home Affairs, Tax Number, Bank Details), you can now often receive your “net” payout within 3 to 5 business days of the directive being issued.

Best for: members in genuine, time-sensitive emergencies.

Why We Chose It:

-

It reflects the technological maturity of the system in its third year.

-

It reduces the “anxiety period” for members waiting on funds.

Things to consider:

-

Any mismatch in your ID or bank details will still cause a manual delay.

Strategic Summary of the Two-Pot Reform Impact

The South Africa Two-Pot Retirement System is a double-edged sword that has finally institutionalized the “emergency fund” within the retirement framework. By April 2026, the data confirms that while many are using the system to survive the cost-of-living crisis, the “locked” two-thirds is creating a massive wave of forced preservation that will result in a much wealthier generation of retirees. The key to “winning” in this system is to treat the Savings Pot as a ghost—something that is there if you are haunted by an emergency, but otherwise left to grow undisturbed at the lower tax rates available at retirement.

Visualizing the Two-Pot System: Rules and Returns

The tables below provide a clear breakdown of the financial mechanics of the 2026/27 tax year to help you calculate the true cost of a withdrawal.

Withdrawal Math: Gross vs. Net (2026 Estimates)

This data illustrates the impact of tax and fees on common withdrawal amounts for a mid-level taxpayer (26% marginal rate).

| Withdrawal Amount (Gross) | Admin Fee (Est.) | SARS Tax (26%) | Net Cash to Member | Effective “Cost” |

| R2,000 (Min) | R500 | R390 | R1,110 | 44.5% |

| R10,000 | R500 | R2,470 | R7,030 | 29.7% |

| R30,000 | R500 | R7,670 | R21,830 | 27.2% |

| R50,000 | R500 | R12,870 | R36,630 | 26.7% |

Our Top 3 Picks and Why?

-

Taxation at Marginal Rates: This is our top pick because it is the biggest “reality check.” Knowing that the government takes nearly a third of your “emergency” money changes the decision-making process for most people.

-

The “Retirement Pot” Lock: We chose this because it is the hero of the story. Even if people spend their Savings Pot every year, the locked two-thirds ensures they won’t be destitute at 65.

-

The Opportunity Cost (Compounding): This is an essential pick because it’s the most invisible cost. Visualizing R25,000 becoming R250,000 is the most powerful deterrent to unnecessary spending.

Navigating this system by yourself requires a high level of “tax-aware” thinking. In 2026, the portals are easy to use, but the consequences are complex.

The Selection Framework

-

Assess the Emergency: Is this a “need” (medical, housing, debt) or a “want” (holiday, new tech)? If it’s a want, you are paying a 26%–45% “tax penalty” for that item.

-

Check the “Tax Bracket Creep”: If you are earning R240,000, a R10,000 withdrawal pushes you over the R245,100 limit, moving your top income from 18% to 26% tax.

-

Verify Your SARS Compliance: Do not apply if you have outstanding returns. SARS will treat your withdrawal as a “collection event” and you may end up with nothing.

-

Calculate the Fee Percentage: If you are withdrawing less than R5,000, the admin fee is a massive percentage of your cash. It is mathematically better to wait until the balance is higher.

Refer to the decision matrix below to see if a withdrawal makes sense for your current 2026 financial profile.

Decision Matrix

| If your situation is… | Choose X if… | Choose Y if… |

| High Interest Debt | Withdraw from Savings Pot if the debt is >20% interest. | Get a Bank Loan if you can get <15% interest. |

| Medical Emergency | Withdraw immediately to avoid physical/financial ruin. | Use Medical Aid/Gap Cover first to preserve growth. |

| Job Change/Resignation | Access the Vested Pot for your primary bridge fund. | Keep Retirement Pot locked to ensure long-term wealth. |

| Planned Big Purchase | Wait and Save Salary to avoid the tax penalty. | Withdraw only if the item is a core necessity. |

The Final Checklist: 5-Point Two-Pot Readiness Plan

-

Log into your fund portal (Momentum, Sanlam, Old Mutual, etc.) and confirm your mobile number and email.

-

Check your “Savings Pot” balance to ensure it is above the R2,000 floor.

-

Perform a “Clean-up” on eFiling to ensure no outstanding tax debt is linked to your ID.

-

Use a 2026/27 Tax Calculator to estimate your “Net” payout after marginal tax.

-

Set a 10-year goal for your “Retirement Pot” to stay motivated about the locked portion.

Steering Your Financial Future in the Two-Pot Era

The South Africa Two-Pot Retirement System is no longer a “new” experiment; it is the settled law of the land in 2026. While the ability to access cash once a year provides a vital safety valve for a nation struggling with high interest rates and living costs, the true value of the system lies in its silence. Those who succeed in this new era are those who ignore the “Savings Pot” noise and focus on the steady, compounding growth of the “Retirement Pot.” By understanding that every withdrawal is a taxable event that steals from your future, you can use the system as it was intended: a shield for emergencies, but a vault for your legacy.