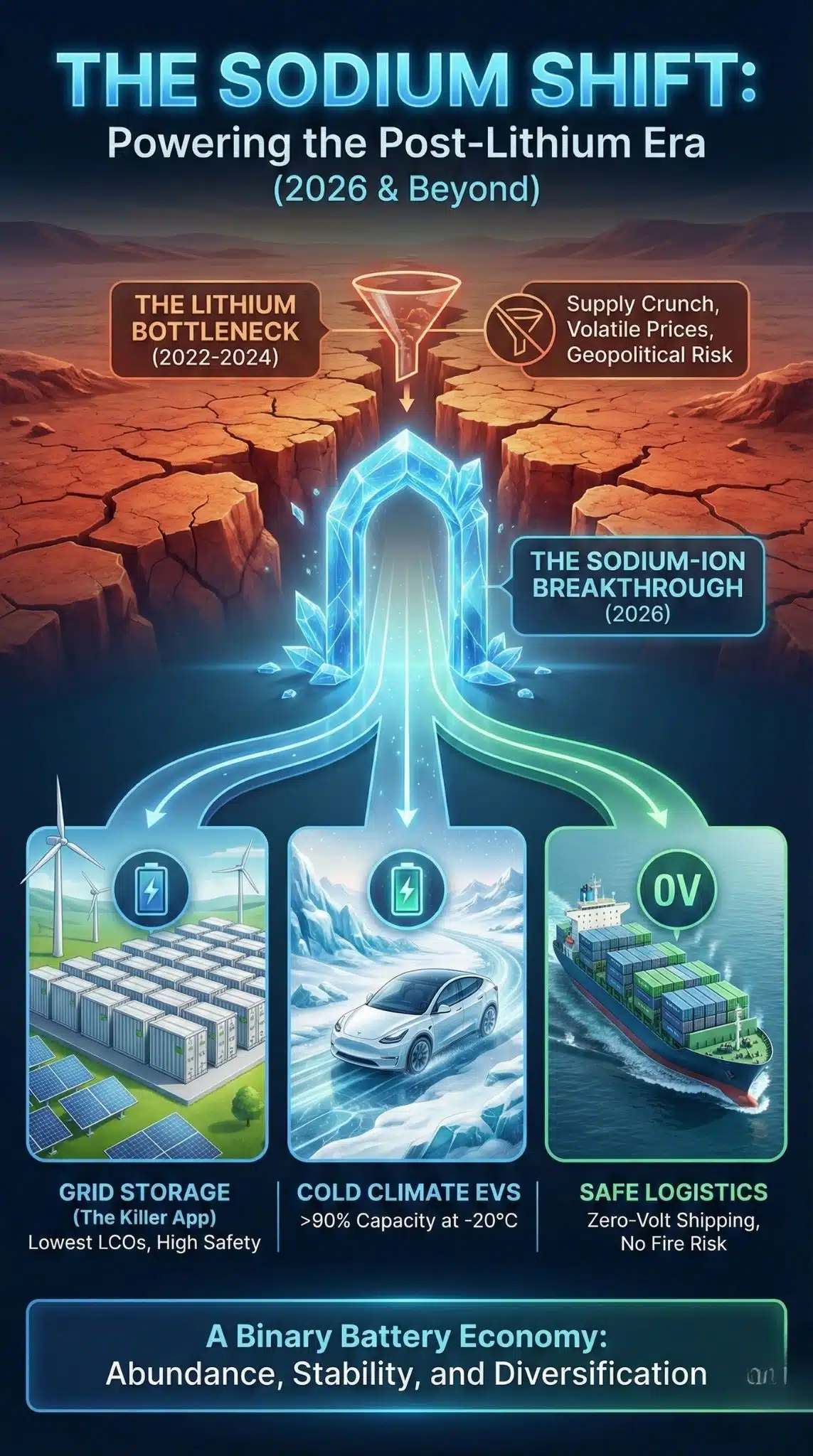

Why this is significant right now By early 2026, the “laboratory promise” of Sodium-Ion batteries has finally converted into industrial reality. With CATL and BYD initiating mass production runs exceeding 100 GWh and Northvolt delivering commercial cells at 160 Wh/kg, the energy market is witnessing the first viable alternative to Lithium-Ion.

This shift is not just about cheaper EVs; it marks the decoupling of renewable energy storage from the volatile economics of lithium mining, fundamentally altering the trajectory of the global energy transition.

Key Takeaways

- Commercial Reality: Sodium-Ion is no longer experimental; major players like CATL (Naxtra) and BYD have integrated it into entry-level EVs and grid storage as of late 2025.

- Cost Parity: With production scaling, cell costs are projected to drop to $40/kWh, undercutting LFP (Lithium Iron Phosphate) batteries by nearly 20-30%.

- Cold Weather Dominance: Unlike Lithium, Sodium batteries retain over 90% capacity at -20°C, solving a critical pain point for EV adoption in northern climates.

- Supply Chain Sovereignty: Abundant sodium reserves eliminate reliance on the “Lithium Triangle” (Chile, Bolivia, Argentina) and Chinese lithium refining dominance.

- The “Zero Volt” Advantage: Sodium cells can be transported at 0% charge (0V), significantly reducing fire risks and logistics costs compared to Lithium-Ion.

The ascent of Sodium-Ion technology is the direct result of the “Lithium Crunch” of 2022-2024. During that period, lithium carbonate prices spiked violently, exposing the fragility of a single-chemistry energy economy. Automakers and energy providers realized that relying solely on lithium—a metal concentrated in geologically specific regions and subject to refining bottlenecks—was a strategic vulnerability. While lithium prices have stabilized in 2025, the industry had already committed billions to diversifying. The result is a “Sodium Shield”: a parallel supply chain that uses aluminum and soda ash, materials available almost everywhere, to insure against future volatility. We have moved from a “Lithium Monopoly” to a “Binary Battery Economy.”

The Economics of Salt: Breaking the Cost Floor

The primary driver for Sodium-Ion adoption is raw arithmetic. For the last decade, the battery industry has been obsessed with energy density (how much power fits in a box). In 2026, the focus has shifted to cost per kilowatt-hour (how cheap is that power).

Sodium-Ion batteries replace lithium with sodium (harvested from soda ash or sea salt) and, crucially, replace the expensive copper current collectors used in lithium batteries with cheap aluminum foil. Sodium does not react with aluminum at low voltages, a chemical quirk that allows manufacturers to strip out one of the most expensive components of a battery cell.

The implications for the energy grid are profound. For a stationary storage facility—think of a massive battery park storing solar energy for night use—weight is irrelevant. If a sodium battery is 30% heavier than a lithium one but 40% cheaper, it wins the contract. This economic leverage is opening the door for terawatt-scale grid storage projects in cost-sensitive markets like India and Southeast Asia.

The Battery Economics Showdown (2026 Status)

| Feature | Lithium-Ion (NCM) | Lithium-Ion (LFP) | Sodium-Ion (Na-Ion) |

| Primary Use Case | Long-range EVs, Premium Tech | Standard EVs, Grid Storage | Entry EVs, Grid Storage, 2-Wheelers |

| Est. Cell Cost | $90 – $110 / kWh | $55 – $70 / kWh | $35 – $45 / kWh (Projected) |

| Energy Density | High (250+ Wh/kg) | Medium (160-170 Wh/kg) | Moderate (160-175 Wh/kg) |

| Cycle Life | 1,500 – 2,500 cycles | 3,000 – 6,000+ cycles | 3,000 – 5,000+ cycles |

| Safety Risk | Moderate (Thermal Runaway) | Low | Very Low (Can ship at 0V) |

| Raw Material Risk | High (Cobalt/Nickel/Lithium) | Medium (Lithium) | Negligible (Sodium/Iron) |

Performance vs. Reality: The Density Gap

Critics often point to Sodium’s lower energy density as a dealbreaker. Chemically, a sodium ion is larger and heavier than a lithium ion. In 2020, this was a valid concern. However, recent engineering breakthroughs by CATL and Northvolt have narrowed the gap significantly.

As of early 2026, commercial sodium cells are hitting 160-175 Wh/kg. To put this in perspective, this is roughly equivalent to the energy density of the LFP batteries used in the Tesla Model 3 just a few years ago. This makes sodium viable for “City EVs”—cars with a range of 300-400km—which constitute the bulk of the mass market in Europe and Asia.

Furthermore, the “Performance” metric is being redefined. It isn’t just about range; it’s about availability. Sodium batteries charge faster (reaching 80% in 15 minutes) and perform exceptionally well in freezing temperatures. For an EV owner in Norway or Canada, a Lithium battery that loses 40% of its range in winter is effectively less energy-dense in practice than a Sodium battery that only loses 10%.

Geopolitical Shift: The End of the “Lithium Triangle” Dominance?

The rise of sodium is a geopolitical maneuver as much as a technological one. Currently, the “Lithium Triangle” (Chile, Argentina, Bolivia) holds the world’s largest lithium brine reserves, while China controls the vast majority of lithium refining. This creates a choke point similar to OPEC’s control over oil.

Sodium-Ion batteries shatter this dependency. Sodium carbonate is the 6th most abundant element in the Earth’s crust and is evenly distributed globally. The United States possesses roughly 90% of the world’s soda ash reserves (in Wyoming), yet has lagged in battery manufacturing. Conversely, Europe and China are racing to build Sodium supply chains that require zero inputs from South America or Australia.

This democratization of resources means that battery factories can be built anywhere with access to standard industrial chemicals, rather than being tethered to specific mining corridors. It lowers the barrier to entry for nations wishing to establish their own energy security infrastructure.

Geopolitical Supply Chain Risk Assessment

| Critical Mineral | Primary Source Region | Geopolitical Risk Level | Supply Chain Bottleneck |

| Lithium | Australia, Chile, China | High | Refining capacity & Water usage in mining |

| Cobalt | DRC (Congo) | Critical | Ethical labor issues & Export bans |

| Nickel | Indonesia, Russia | High | Export restrictions & Environmental impact |

| Sodium | Global (US, China, Europe) | Low | None (Ubiquitous industrial chemical) |

| Aluminum | Global | Low | Energy cost for smelting |

Applications: Where Sodium Wins (and Where it Doesn’t)

The market is bifurcating. We are seeing a clear split in application suitability based on the physics of the materials.

- Grid Storage (The Big Winner): This is Sodium’s “killer app.” Utility companies do not care if a battery bank is 20% heavier; they care about the Levelized Cost of Storage (LCOS). Sodium’s safety profile (non-flammable electrolytes, lower thermal runaway risk) makes it ideal for urban deployments where fire codes are strict.

- Micro-Mobility: E-scooters and E-bikes are rapidly switching to sodium. The safety factor is paramount here—lithium fires in e-bikes have been a major regulatory headache in cities like New York and London. Sodium eliminates this fire risk almost entirely.

- Entry-Level EVs: Budget models (sub-$20,000 cars) are adopting hybrid packs—mixing Lithium cells for range with Sodium cells for cold-weather performance and cost reduction.

However, Sodium will not replace Lithium in high-performance sectors. Long-haul trucking, luxury sedans with 800km+ range, and aerospace applications will continue to demand the superior energy density of Lithium-NCM or emerging Solid-State Lithium batteries.

Expert Perspectives

To maintain a balanced view, it is crucial to analyze conflicting expert opinions regarding the speed of this transition.

- The “Bull” Case:

- Dr. Robin Zeng (CATL Chairman) has famously pushed for the “Dual-Star” strategy, integrating Sodium and Lithium cells into single packs to balance cost and range. Proponents argue that as Lithium prices inevitably cycle upward again due to scarcity, Sodium will capture 30-40% of the total battery market by 2030.

- The “Bear” Case:

- Analysts at BloombergNEF and Wood Mackenzie have cautioned that if Lithium prices remain depressed (below $15/kg) throughout 2026, the economic urgency to switch to Sodium diminishes. They argue that the existing LFP supply chain is so mature and optimized that Sodium faces a “scale-up trap”—it needs massive scale to be cheaper, but needs to be cheaper to get massive scale.

- The Technological Skeptics:

- Some electrochemists note that the hard carbon anodes required for Sodium batteries are currently more expensive to produce than the graphite used in Lithium batteries. Until the hard carbon supply chain matures, the theoretical cost savings of Sodium might be eaten up by processing costs.

Future Outlook: What Comes Next?

Looking ahead through 2026 and into 2027, three major milestones will determine the trajectory of Sodium-Ion technology:

- The Solid-State Convergence: Companies like Zhaona New Energy are already prototyping solid-state sodium batteries.20 These remove the liquid electrolyte entirely, pushing energy densities toward 300 Wh/kg. If successful, this would nullify Lithium’s main advantage.

- Recycling Standardization: As the first wave of Sodium batteries hits the market, the recycling industry must adapt. Unlike Lithium batteries, where the value lies in recovering Cobalt and Lithium, Sodium batteries have low material recovery value (sodium is cheap). This may require new policy frameworks—like “battery passports”—to mandate recycling, as market forces alone won’t drive it.

- Western Adaptation: Will US and European automakers adopt Sodium, or will it remain a Chinese-dominated technology? With trade barriers and tariffs on Chinese EVs rising in the West, local production of Sodium cells (like Northvolt’s initiatives in Europe) will be critical.

Prediction: By the end of 2026, we will see the first “Sodium-Only” grid storage tenders awarded in the US and EU, signaling the technology’s acceptance as bankable infrastructure.

Final Thoughts

Sodium-Ion is not the “Lithium Killer”—it is the “Lithium Savior.” By taking over the heavy lifting for grid storage and low-range mobility, it frees up scarce lithium resources for high-performance applications where they are truly needed. We are entering an era of battery diversity, where the question isn’t “which battery is best,” but “which battery is right for the job.” For the energy grid of 2026, the answer is increasingly looking like plain old salt.