Managing money effectively often depends on how well finances are organised. As incomes grow and financial goals multiply, many people begin to wonder whether a single account is enough. Opening more than one savings account has become increasingly common, especially with digital banking making account management easier.

Understanding the advantages and drawbacks of holding multiple accounts can help determine whether this approach suits your financial habits.

Why People Consider Multiple Savings Accounts

A single account often ends up serving too many purposes at once. Daily expenses, emergency funds, short term goals, and savings all compete for the same balance.

Opening separate accounts allows people to assign specific purposes to each one. For example, one savings account may be used for regular expenses, while another is reserved for emergencies or planned purchases. This separation can improve clarity and reduce accidental overspending.

Pros Of Having Multiple Savings Accounts

There are several reasons why multiple accounts can be beneficial when managed correctly.

Before deciding, it helps to understand the potential advantages.

- Better Financial Organisation: Separating money by purpose makes it easier to track progress towards goals.

- Reduced Spending Temptation: Funds kept in a dedicated account are less likely to be used impulsively.

- Goal Based Saving: Different accounts can support different timelines, such as travel or education.

- Improved Budget Discipline: Clear boundaries help reinforce saving habits.

Using more than one savings account can create mental structure that supports consistent financial behaviour.

Cons Of Opening Multiple Accounts

While multiple accounts offer structure, they also come with responsibilities. Without careful management, they can create confusion rather than clarity.

Some common drawbacks include the following.

- Account Maintenance Effort: Tracking balances and transactions across accounts requires attention.

- Minimum Balance Requirements: Some accounts may require maintaining a certain balance, which can lock funds unnecessarily.

- Fragmented Funds: Splitting money too thinly can reduce flexibility during emergencies.

- Overcomplication: Too many accounts may make financial planning harder instead of simpler.

These issues are more likely when accounts are opened without a clear purpose.

How Many Accounts Are Enough?

There is no ideal number that applies to everyone. For most individuals, two or three accounts are sufficient to separate spending, savings, and emergency funds.

The key is intentionality. Each account should serve a specific role. If an account no longer has a clear purpose, it may be better to consolidate funds rather than maintain it out of habit.

A well managed savings account structure should simplify decisions, not multiply them.

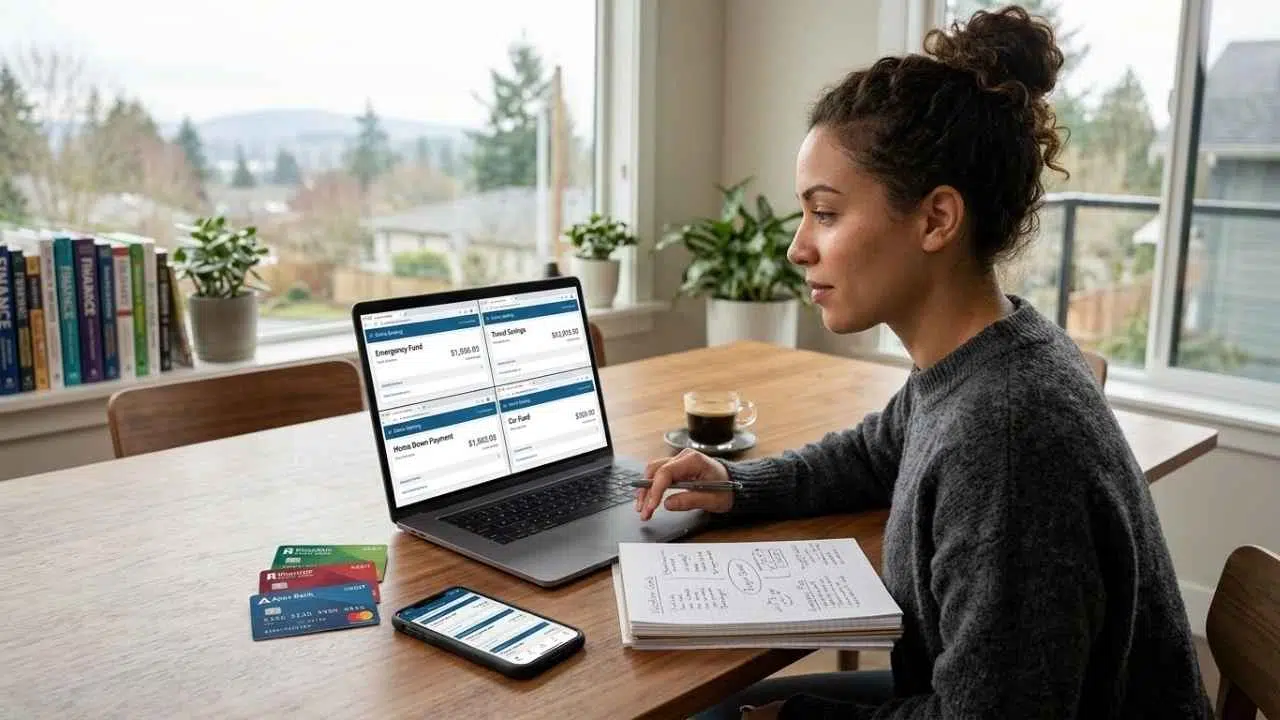

Digital Banking And Account Management

Digital banking has made it easier to manage multiple accounts from a single interface. Mobile apps allow users to view balances, transfer funds, and track activity without effort.

However, ease of access should not encourage unnecessary account opening. Convenience works best when paired with restraint and planning.

When Multiple Accounts Make Sense

Multiple accounts are useful for people with clear financial goals, stable income, and a preference for organised money management. They are also helpful for families managing shared and personal expenses separately.

On the other hand, individuals who prefer simplicity may benefit more from fewer accounts with clear budgeting practices.

Reviewing And Adjusting Over Time

Financial needs change over time. Accounts that were useful at one stage may become redundant later.

Periodic reviews help ensure that each account continues to add value. Closing or merging unused accounts keeps finances streamlined and easier to manage.

Final Thoughts

Opening multiple savings accounts can improve financial organisation and support goal-based saving when done thoughtfully. The approach works best when each account has a clear purpose and is actively monitored. However, too many accounts can create unnecessary complexity and reduce flexibility. By balancing structure with simplicity, individuals can decide whether multiple accounts enhance or hinder their money management.