As of January 2026, the era of “voluntary” sustainability reporting in Asia has officially ended. With Singapore, Hong Kong, Australia, and China simultaneously enforcing mandatory climate disclosures aligned with the International Sustainability Standards Board (ISSB), we are witnessing a fundamental restructuring of how capital is allocated in the region.

This is no longer a compliance exercise; it is a “license to operate” that will aggressively filter winners from losers based on data transparency rather than just green promises.

Key Takeaways

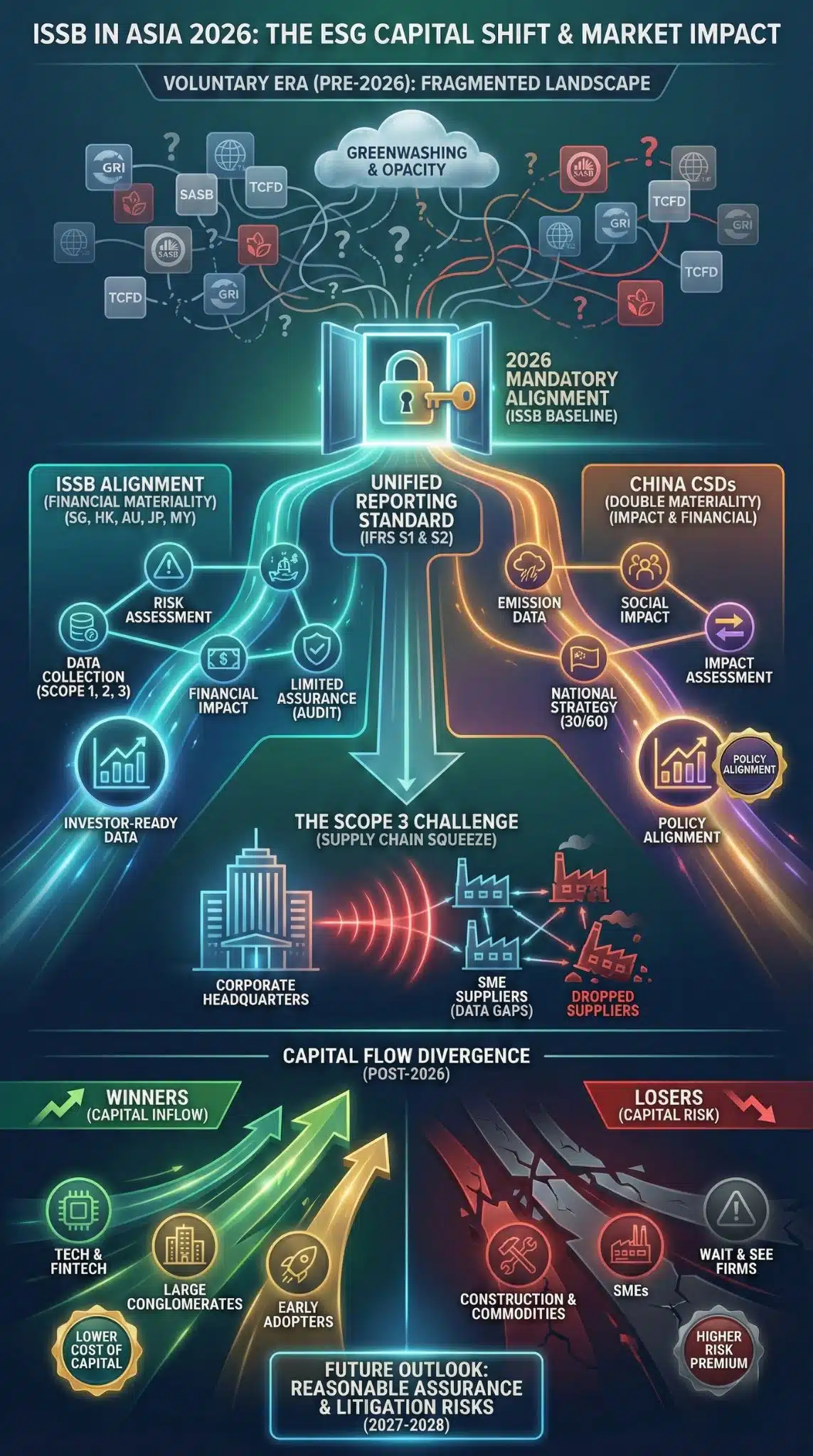

- The “Alphabet Soup” is Dead: The fragmented era of GRI, SASB, and TCFD has consolidated into a single global baseline (ISSB) in 2026, reducing regulatory arbitrage.

- Scope 3 is the New Trade Barrier: Mandatory Scope 3 reporting in major hubs (Singapore, Hong Kong) is forcing a “data squeeze” down the supply chain, threatening SME suppliers who cannot calculate carbon footprints.

- China’s Strategic Pivot: The implementation of CSDS (aligned with ISSB but adding “impact” materiality) signals Beijing’s intent to lead global green standards, not just follow them.

- Capital Cost Divergence: Early data from 2025 filings suggests a widening cost-of-capital gap between firms with auditable ESG data and those relying on estimates.

- The Assurance Cliff: While reporting is now mandatory, the requirement for external assurance (audit) is the next hurdle, with capacity crunches expected in late 2026.

The convergence of global sustainability standards has been discussed for a decade, but 2026 marks the year it became an operational reality in Asia. Following the ISSB’s release of IFRS S1 and S2 in 2023, Asian regulators spent two years preparing their markets. That grace period is over. We have moved from the “awareness” phase to the “enforcement” phase. This shift is driven not merely by environmental altruism but by a desperate need to secure foreign direct investment (FDI). As European and American capital markets tighten their ESG screening (driven by the EU’s CSRD), Asian markets risk capital flight if they remain opaque. The harmonization we are seeing now is a defensive economic moat.

The Great Harmonization: Ending the “Wild West”

For years, Asian conglomerates navigated a confusing “alphabet soup” of voluntary frameworks. Companies would cherry-pick the framework that made them look best—using GRI for social impact while ignoring TCFD for climate risk. The 2026 mandates in Singapore (ACRA) and Hong Kong (HKEX) have effectively closed this loophole.

By aligning legally with the ISSB (IFRS S1 & S2), these jurisdictions have standardized the language of risk.1 In 2026, a bank in Tokyo can now directly compare the climate risk exposure of a semiconductor firm in Taiwan with a logistics giant in Singapore without needing a translation layer. This transparency is stripping away the “greenwishing” where vague net-zero pledges hid a lack of interim targets.

Analysis: This standardization is a double-edged sword. While it simplifies cross-border investment, it also exposes laggards. Companies that previously hid behind “proprietary methodologies” for carbon accounting are now finding their risk premiums rising as standardized data reveals their true exposure to carbon pricing and transition risks.

The “Scope 3” Shockwave: A Supply Chain Crisis

The most disruptive element of the 2026 mandates is the treatment of Scope 3 emissions (indirect value chain emissions). While some jurisdictions have offered temporary relief, the writing is on the wall. For “Group 1” entities in Australia and “STI constituents” in Singapore, the pressure to report Scope 3 is immediate.

This creates a massive ripple effect. A large listed multinational in Singapore cannot report its Scope 3 numbers without data from its suppliers in Vietnam, Indonesia, and Thailand.

The Squeeze:

- Top-Down Pressure: Large buyers are sending “comply or die” notices to suppliers: provide carbon data or lose the contract.

- The SME Gap: Small and Medium Enterprises (SMEs) lack the funds for sophisticated carbon accounting software.

- Data Quality: We are currently seeing a chaotic mix of high-quality “primary data” from top-tier suppliers and “spend-based estimates” from lower tiers.

Note: Analysts predict that 2026 will see the first wave of “supplier shedding,” where multinationals drop smaller suppliers simply because they cannot provide the necessary ESG data, opting instead for larger, more bureaucratized competitors.

China’s “Double Materiality” Gambit

While Singapore and Hong Kong closely mirror the ISSB’s “financial materiality” (how climate hurts the company), China’s 2026 implementation of its Corporate Sustainable Disclosure Standards (CSDS) introduces a critical divergence: “Double Materiality.”2

China requires companies to report not just on financial risk, but on their impact on the environment and society.3 This aligns China more closely with the European Union’s approach than the US/ISSB approach.

Why this matters:

- Geopolitics: By adopting a rigorous standard that includes “impact,” China is positioning its companies to be compatible with EU markets (CSRD), potentially outmaneuvering US firms that only focus on financial risk.

- State Strategy: It allows Beijing to use corporate reporting as a tool to drive national decarbonization goals (the 30/60 target), forcing state-owned enterprises (SOEs) to publicly disclose their contribution to national net-zero targets.4

Comparative Analysis: The 2026 Implementation Matrix

The landscape is not uniform. The speed and depth of adoption vary significantly across the region, creating a complex compliance map for multinationals.

2026 Mandatory ESG Reporting Status in Key Asian Markets

| Jurisdiction | Standard | 2026 Mandate Status | Scope 3 Requirement | Primary Focus |

| Singapore | ISSB-aligned (ACRA) | Mandatory for all listed issuers (FY2025 filings). | Mandatory for STI Index firms; deferred for others. | Financial Materiality & Capital Attraction |

| Hong Kong | HKFRS S1/S2 (ISSB) | Mandatory for Main Board issuers (FY2025). | “Comply or Explain” moving to Mandatory for Large Caps. | Global Finance Integration |

| China | CSDS (ISSB + EU hybrid) | Mandatory for SSE 180 / SZSE 100 / Dual-listed. | Phased in; strong focus on “Impact”. | National Strategy & EU Market Access |

| Australia | AASB S2 (ISSB) | Live for “Group 1” (Large entities). | Mandatory from commencement (with liability relief). | Climate Risk & Litigation Protection |

| Japan | SSBJ Standards | Finalized; Early adoption encouraged. | Mandatory rollout expected 2027 (Market Cap based). | Supply Chain Resilience |

| Malaysia | ISSB (Bursa Malaysia) | Mandatory for Main Market issuers (Phased). | Required for Main Market from FY2026/27. | Competitiveness of Key Exports (Palm Oil/Tech) |

Winners and Losers in the New Regime

The mandatory nature of these disclosures creates distinct economic outcomes. It acts as a filter, rewarding capital-rich, data-savvy sectors while penalizing fragmented, low-margin industries.

Sectoral Impact Analysis (Winners vs. Losers)

| Category | Winners (Capital Inflow) | Losers (Capital Risk) | Why? |

| Sector | Tech, Fintech, High-End Mfg | Construction, Agriculture, Commodities | Tech has lower Scope 3 complexity; Commodities face massive data collection hurdles and high transition risks. |

| Company Type | Large Conglomerates | SMEs & Family Businesses | Conglomerates have dedicated ESG teams; SMEs are drowning in paperwork and consultancy fees. |

| Geography | Singapore, Hong Kong | Developing ASEAN (Vietnam, Cambodia) | Mature hubs have the ecosystem (auditors, software); developing markets lack the infrastructure to verify data. |

| Strategy | Early Adopters (Pre-2024) | “Wait and See” Firms | Early adopters have historical data baselines; laggards are reporting “volatile” numbers that scare investors. |

Expert Perspectives: The “Cost vs. Value” Debate

Critics argue that the 2026 mandates have imposed a “compliance tax” on Asian economies at a time of slowing growth.

- The Skeptic’s View: “We are spending millions on consultants to produce a PDF that few investors read,” argues a CFO of a mid-sized Malaysian manufacturing firm. The concern is that resources are being diverted from actual decarbonization (buying solar panels) to reporting on decarbonization (hiring auditors).

- The Pragmatist’s View: Institutional investors counter that this data is essential for pricing risk.5 “We cannot insure or invest in a company if we don’t know their exposure to carbon taxes or flood risks in 2030,” notes a strategy lead at a major Singaporean sovereign wealth fund. “The cost of reporting is lower than the cost of stranded assets.”

Future Outlook: The Assurance Cliff of 2027

As we look beyond 2026, the next major hurdle is Assurance. Currently, most mandates only require “limited assurance” (a lower level of auditor scrutiny). However, roadmaps in Australia and Singapore point toward “reasonable assurance” (the same rigor as financial audits) by 2027-2028.

Predictions for the next 12-24 months:

- The Talent War: There will be a massive shortage of qualified ESG auditors in Asia. Big 4 firms are already poaching climate scientists.

- Litigation Risks: As companies publish mandatory data, greenwashing lawsuits will rise. In Australia, the “safe harbor” provisions for forward-looking statements will be tested in court.

- Tech Consolidation: The market for ESG software will consolidate. Startups offering “AI-driven carbon accounting” will be acquired by legacy ERP giants (SAP, Oracle) to integrate carbon data directly into financial ledgers.

The 2026 mandatory reporting wave is not just a regulatory update; it is a structural reform of Asian capitalism. It signals the end of opacity. For Asian markets, the alignment with ISSB is a strategic bid to remain the factory of the world and a hub for global capital. The companies that treat this as a strategic data exercise will unlock lower costs of capital. Those that treat it as a box-ticking exercise will find themselves increasingly uninvestable.

Final Thoughts

The transition to mandatory ISSB reporting is the digital transformation of sustainability. It turns vague promises into hard, auditable code. For investors, the fog is lifting, and the view of who is truly resilient—and who is not—has never been clearer.