The 2026 financial landscape has reached a point of no return as Central Bank Digital Currencies (CBDCs) and private stablecoins clash for control over the $150 trillion global payments market. This struggle represents more than just a technological shift; it is a fundamental redesign of how national sovereignty and private innovation will coexist in the digital age.

Key Takeaways

- Legislative Clarity: The full implementation of the GENIUS Act in the United States and MiCAR in Europe has transformed stablecoins from speculative “crypto-assets” into regulated, “narrow bank” digital cash.

- Volume Paradox: In 2025, stablecoin annual transfer volumes reached $18.4 trillion, surpassing the annual volumes of legacy giants Visa ($15.7 trillion) and Mastercard ($9.8 trillion).

- Wholesale Dominance: While retail CBDCs face privacy hurdles, “Wholesale CBDCs” (wCBDCs) like the Project Agorá prototype are set to report in the first half of 2026, aiming to replace the aging SWIFT system.

- Banking Disintermediation: Central banks are introducing “holding limits” (e.g., €3,000) to prevent a massive flight of deposits from commercial banks into digital currency wallets.

- Digital Dollarization: US dollar-backed stablecoins still account for over 99% of the stablecoin market cap, effectively extending American monetary influence despite the rise of foreign CBDCs.

The transition to a digital-first monetary system did not happen overnight. For much of the early 2020s, the “battle” was viewed as a fringe experiment. Stablecoins were tools for crypto-traders to park capital, and CBDCs were white papers discussed in the quiet halls of the Bank for International Settlements (BIS). However, the post-pandemic inflation crisis and the increasing weaponization of traditional payment rails forced a shift in 2024 and 2025.

As we enter 2026, the global financial architecture is being rebuilt from the ground up. The realization that money can be “programmed” to settle instantly, $24/7$, without the need for a chain of five different intermediary banks, has made the legacy “correspondent banking” model obsolete. This is no longer an “if” scenario—it is a “who” scenario. Who will control the ledger: the public central bank or the private, algorithmically-backed issuer?

The Regulatory Watershed: The GENIUS Act and MiCAR

In January 2026, the regulatory dust has finally settled. The passage of the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act in late 2025 provided the legal “green light” that Wall Street had been waiting for. This act mandates that stablecoin issuers be treated as regulated financial entities, requiring $100\%$ reserves in liquid assets like US Treasuries.

Across the Atlantic, the Markets in Crypto-Assets (MiCAR) regulation has already begun weeding out unregulated issuers, forcing a consolidation of the market into a few highly transparent players. This regulatory clarity has turned stablecoins into the “digital plumbing” of the global economy.

| Feature | Pre-Regulation (2023-2024) | Post-Regulation (2026) |

| Issuer Status | Often offshore/unregulated (e.g., Early Tether) | Regulated “Payment Stablecoin Issuers” |

| Reserve Quality | Mix of commercial paper, crypto, and cash | $100\%$ Government Treasuries & Cash |

| Audit Standards | Occasional “Attestations” | Monthly PCAOB-registered audits |

| Institutional Trust | “High Risk” / Speculative | “Cash Equivalent” / Settlement Asset |

| Legal Recourse | Unclear / Jurisdiction dependent | Priority claim in bankruptcy proceedings |

The result is a market that has moved beyond “on-ramping” to crypto. By 2026, stablecoins are being used for B2B cross-border payments, corporate payroll, and even the tokenization of real-world assets (RWA).

The Great Divergence: Wholesale vs. Retail CBDCs

While stablecoins have claimed the “open” internet, central banks are fighting back with two distinct tools: Retail CBDCs (rCBDCs) and Wholesale CBDCs (wCBDCs). The year 2026 marks a clear divergence in strategy between these two.

Retail CBDCs are intended for the general public—essentially digital banknotes. However, they have faced significant social and political headwinds regarding surveillance. In contrast, Wholesale CBDCs operate behind the scenes, allowing banks to settle accounts with each other instantly using tokenized central bank money.

| Type of CBDC | Primary User | Main Objective | 2026 Status |

| Retail (rCBDC) | General Public | Financial inclusion, competition with Visa | High political pushback; limits on holdings |

| Wholesale (wCBDC) | Banks & Institutions | $24/7$ interbank settlement, lower costs | Project Agorá enters prototype phase |

| Synthetic (sCBDC) | Private Issuers | Backing stablecoins with CB reserves | Increasing adoption by “Narrow Banks” |

The Project Agorá initiative, involving the Federal Reserve of New York, the Bank of Japan, and the Bank of France, is the most ambitious effort yet. By the end of Q2 2026, this project aims to prove that a “unified ledger” can combine the safety of central bank money with the efficiency of private tokenized deposits.

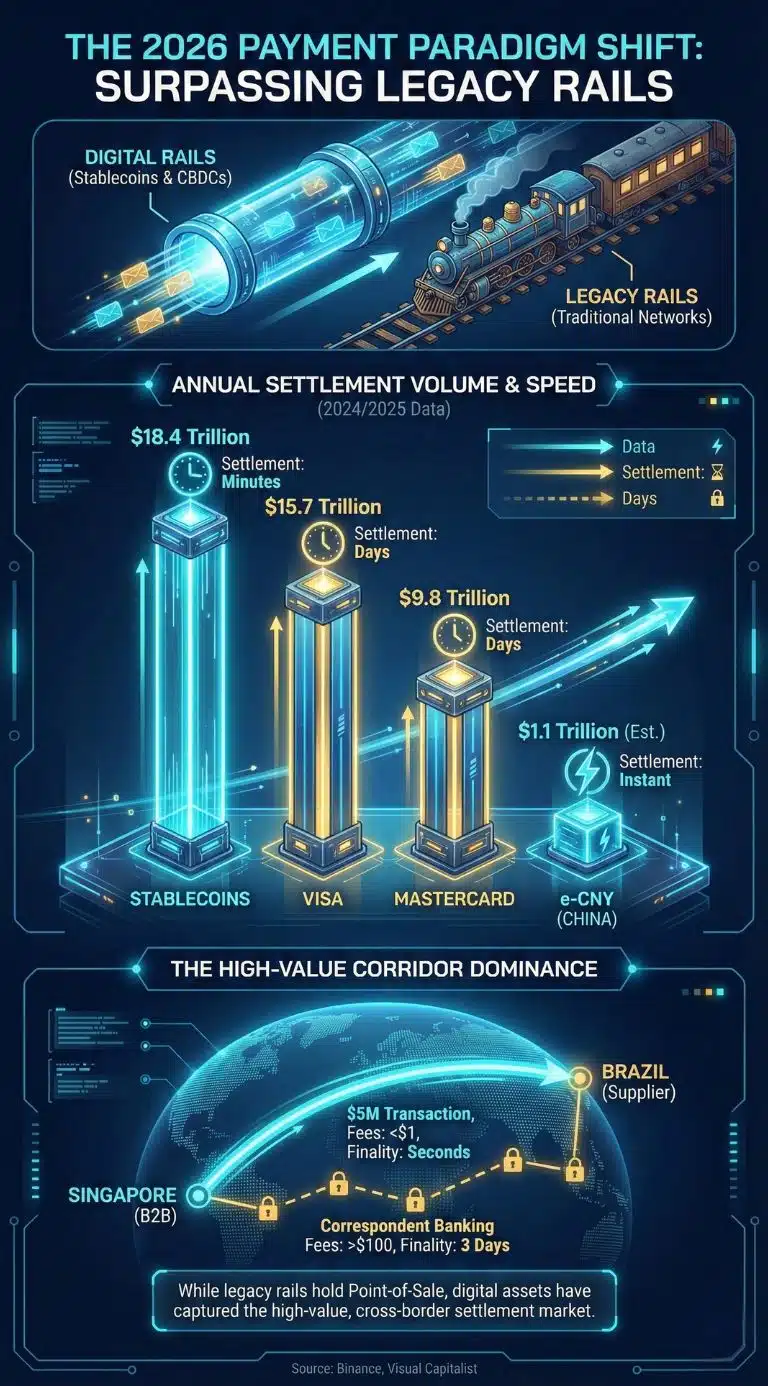

The Numbers Tell the Story: Surpassing Legacy Rails

One of the most startling developments of 2026 is the sheer volume of value moving through these digital pipes. Data from the most recent Binance and Visual Capitalist reports suggests that stablecoins have already “flipped” the traditional card networks in terms of annual settlement volume.

| Payment Rail | Annual Transfer Volume (2024/2025) | Average Settlement Time |

| Stablecoins | $18.4$ trillion | Minutes |

| Visa | $15.7$ trillion | Days (Net settlement) |

| Mastercard | $9.8$ trillion | Days (Net settlement) |

| e-CNY (China) | $1.1$ trillion (Est.) | Instant |

While Visa and Mastercard still dominate “point-of-sale” (buying a coffee), stablecoins have won the “high-value corridor.” When a company in Singapore needs to pay a supplier in Brazil, it is increasingly opting for USDC or USDT over a traditional wire transfer because the settlement is final in seconds, rather than days, and the fees are a fraction of what banks charge for currency conversion.

Geopolitical Sovereignty: The “Digital Dollarization” Problem

For many nations, the battle is not just about technology—it is about the survival of their local currency. This is especially true in the “Global South.” In 2026, we are witnessing a phenomenon called “Digital Dollarization.” In countries like Argentina, Nigeria, and Turkey, citizens are abandoning local currencies in favor of USD-pegged stablecoins.

Because 99% of stablecoins are pegged to the US dollar, the US has effectively exported its monetary policy to the rest of the world via the blockchain. This has put central banks on the defensive.

- China’s Response: The e-CNY (Digital Yuan) is being integrated into international trade corridors (mBridge) to bypass the US dollar.

- Europe’s Response: The Digital Euro is being framed as a “sovereignty” project. In 2026, the European Central Bank (ECB) is finalizing the rulebook to ensure that a European-controlled digital currency exists to counter the dominance of American tech giants and stablecoins.

- India’s Strategy: Leveraging the Unified Payments Interface (UPI) and the E-Rupi, India is focusing on domestic efficiency to ensure private stablecoins do not gain a foothold in the local economy.

The Bank Disintermediation Crisis

If every citizen can hold their money in a Digital Euro wallet at the ECB or in a high-yield stablecoin, what happens to the neighborhood bank? This is the “Disintermediation” risk. In 2026, this is no longer a theoretical concern. Central banks are implementing strict “guardrails” to prevent a collapse of the commercial banking system.

| Risk Factor | Impact on Banks | Mitigation Strategy (2026) |

| Deposit Flight | Customers move money to CBDC/Stablecoins | Holding Limits: (e.g., €3,000 max in CBDC) |

| Lost Fee Income | Banks lose $3\%–5\%$ on cross-border fees | Pivot to Custody Services and “Deposit Tokens” |

| Liquidity Squeeze | Banks have less cash to lend | Central bank provides liquidity “backstops” |

The ECB recently estimated that the digital transition would cost the European banking sector between €4 billion and €5.8 billion in infrastructure and lost revenue. However, forward-thinking banks like JP Morgan and HSBC have pivoted, launching their own “Deposit Tokens” which act like private stablecoins but remain on the bank’s balance sheet.

Expert Perspectives: A Divided Front

The debate over the “winner” of this battle remains highly contentious among financial experts.

- The Technocrats: “Central banks are too slow. Stablecoins have the network effect. You can’t put a CBDC into a decentralized finance (DeFi) protocol easily. The innovation will stay private.” — Chief Economist at a major DeFi protocol.

- The Regulators: “Stablecoins are ‘shadow banks.’ Without the trust of a central bank, they are prone to runs. The only ‘safe’ digital money is central bank money.” — IMF Senior Policy Advisor.

- The Geopoliticians: “This is the new Cold War. The country that provides the most usable, liquid digital currency will dictate global trade for the next century.” — Global Strategist at a D.C. Think Tank.

Future Outlook: What Happens Next?

As we look toward the second half of 2026 and into 2027, the “battle” is evolving into a “cohabitation.” We are likely to see the following milestones:

- The Rise of “Hybrid” Money: Most consumers won’t know if they are using a CBDC or a stablecoin. Their digital wallet will simply show a balance, and the “plumbing” will switch between private and public rails depending on the cheapest path.

- Programmable Tax: We expect the first pilot programs where government subsidies are distributed via CBDCs with “smart contracts”—ensuring the money can only be spent on food or education.

- The “Yield War”: Regulated stablecoins will begin offering “native yield” (passing through interest from Treasury holdings). This will force traditional banks to either raise interest rates on savings accounts or risk losing $20\%$ of their deposit base by 2028.

- Interoperability Standards: By the end of 2026, the G20 is expected to announce a set of standards for “Cross-Chain Interoperability,” allowing a Digital Euro to be instantly swapped for a US-regulated stablecoin without a centralized exchange.

The “Battle for the Future of Digital Forex” is nearing its climax. While stablecoins have won the race for efficiency and market volume, CBDCs are positioning themselves as the ultimate “layer of trust.” The winner won’t be a single currency, but the ecosystem that manages to balance privacy, speed, and safety.