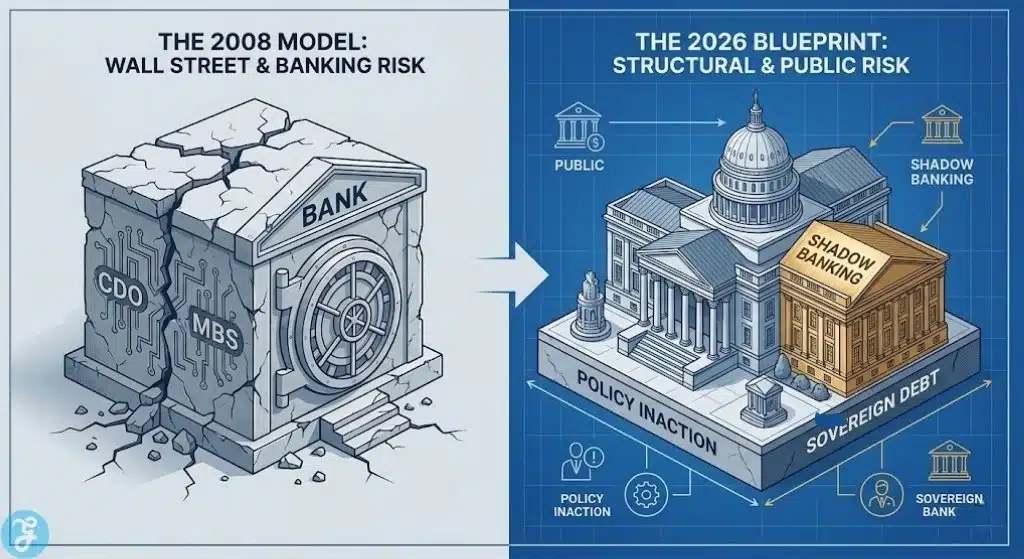

When economic historians eventually sift through the macroeconomic wreckage of the late 2020s, they will invariably conclude that the Causes of the Next Global Financial Crisis were not forged by rogue algorithmic traders on Wall Street, but systematically cultivated by the deliberate, cowardly inaction of global policymakers. We have spent the nearly two decades since the 2008 collapse obsessively regulating the private commercial banking sector, operating under the dangerous delusion that the next great economic unwinding would perfectly mirror the subprime mortgage meltdown. We built massive regulatory fortresses around traditional banks, implemented extreme stress tests through frameworks like Dodd-Frank and Basel III, and severely curtailed proprietary speculative trading.

Yet, while we were busy fighting the ghosts of the past and congratulating ourselves on the stability of consumer deposits, the actual systemic risk silently migrated. It moved away from the fast-paced, highly scrutinized trading desks of private finance and pooled directly into the slow-moving, deeply opaque, and politically protected corridors of sovereign legislatures, central banks, and unregulated shadow markets.

The greatest systemic threat to the global economy today is no longer unchecked corporate greed; it is the “cowardice of the commons.” Elected officials and regulatory heads are willfully ignoring massive, slow-building structural vulnerabilities simply because fixing them requires inflicting immediate, severe political and economic pain. By prioritizing their immediate survival in the next election cycle, they are guaranteeing a catastrophic mathematical reckoning for the global middle class. We are watching a slow-motion train wreck where the conductors are fully awake, staring directly at the missing tracks ahead, and actively choosing not to touch the brakes because it might temporarily disrupt the comfort of the passengers.

The following breakdown illustrates how the epicenter of global economic fragility has fundamentally shifted from the private sector to the public sector over the last two decades.

| Risk Dimension | The 2008 Paradigm (Private Risk) | The 2026 Paradigm (Public & Structural Risk) |

| Origin of Crisis | Reckless subprime consumer lending and complex derivative packaging. | Unfunded sovereign liabilities, shadow banking leverage, and structural deficits. |

| Primary Actors | Investment banks, mortgage brokers, and rating agencies. | Legislators, Treasury departments, Central Banks, and Private Credit firms. |

| Pace of Collapse | Sudden, liquidity-driven market crashes happening in days. | Slow, corrosive insolvency, currency debasement, and systemic stagflation. |

| Proposed Solution | Dodd-Frank, Basel III, enhanced capital reserve requirements. | Severe fiscal austerity, entitlement reform, and enforced political accountability. |

The Architecture of Cowardice and the Causes of the Next Global Financial Crisis

To truly understand the nature of this impending disaster, we must first dissect the underlying political architecture that enables it. The fundamental mismatch driving the Causes of the Next Global Financial Crisis is the irreconcilable, widening gap between the political election cycle and the macroeconomic debt cycle. A politician operates on a strict two-to-four-year timeline, wherein their primary, overriding objective is to secure re-election by promising uninterrupted economic prosperity, artificially lowered taxes, and perpetually expanded social safety nets.

Conversely, macroeconomic structural vulnerabilities, such as aging demographics, crumbling physical infrastructure, and compounding sovereign debt interest, take decades to fully materialize and require decades of highly disciplined, deeply unpopular fiscal restraint to resolve.

When a modern leader is faced with the choice between enacting necessary austerity today (mathematically guaranteeing they lose the next election) or deferring the problem to their successor (mathematically guaranteeing a future crisis), the incentive structure of modern democracy virtually mandates that they choose the latter. This is not mere incompetence; it is a calculated, highly rational abdication of fiduciary duty. Policymakers are actively utilizing the sheer complexity of modern monetary mechanics to obscure the reality that the math no longer balances. They are masking fundamental insolvency with engineered liquidity, relying heavily on central banks to monetize sovereign debt that the open, free market would otherwise reject out of hand.

This matrix highlights the specific mechanisms of delay utilized by modern governments to postpone inevitable structural reckonings, contrasting the political spin with the economic reality.

| Mechanism of Delay | Political Justification (The Spin) | True Economic Consequence (The Reality) |

| Perpetual Deficit Spending | “Stimulating economic growth and supporting citizens during temporary headwinds.” | Embedding permanent inflation and actively crowding out productive private sector investment. |

| Yield Curve Manipulation | “Ensuring the smooth, uninterrupted functioning of government bond markets.” | Financial repression, effectively punishing savers and entirely destroying organic price discovery. |

| Deferred Infrastructure Maintenance | “Optimizing current budget allocations for urgent, immediate social needs.” | Exponentially higher future replacement costs and the guarantee of catastrophic systemic failures. |

| Entitlement Expansion | “Protecting the most vulnerable demographic cohorts from economic hardship.” | Guaranteeing the ultimate mathematical insolvency of sovereign safety nets for future generations. |

Sovereign Debt: The Silent Drivers Among the Causes of the Next Global Financial Crisis

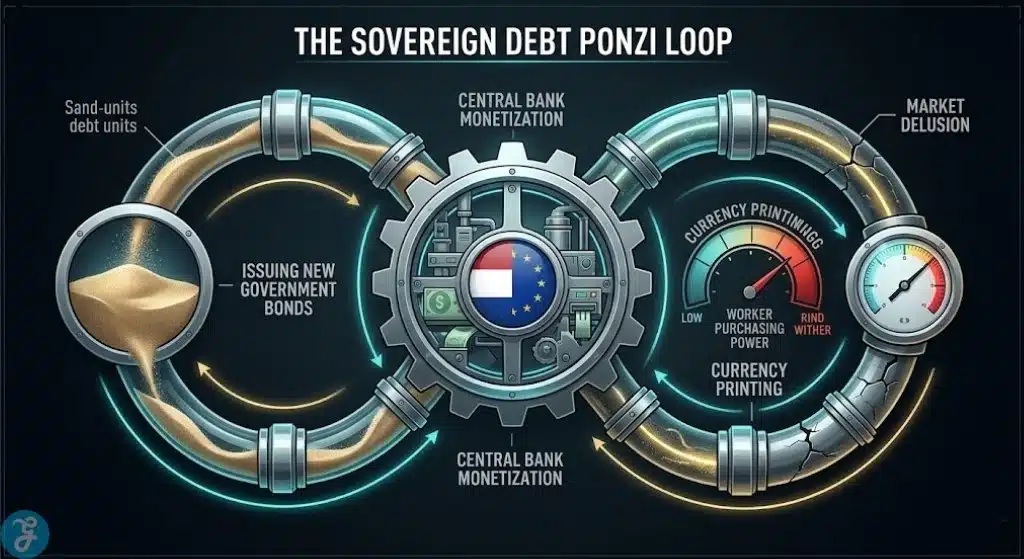

Nowhere is this cowardice more apparent, and more dangerous, than in the handling of global sovereign debt, which stands as the absolute most critical element among the Causes of the Next Global Financial Crisis. We have definitively entered an era of “fiscal dominance.” This is a state where the sheer, overwhelming volume of government debt dictates the actions of central banks, entirely stripping them of their independence. For years following the 2008 crisis, governments borrowed astronomically at zero-bound or even negative interest rates, operating under the highly dangerous, historically ignorant assumption that the cost of capital would remain perpetually negligible.

Today, as interest rates have normalized to fight embedded inflation, the interest payments alone on these massive sovereign debt loads are beginning to consume double-digit percentages of national tax revenues. In some advanced economies, the annual cost of simply servicing the debt now exceeds the entire national defense budget.

Instead of restructuring the debt, raising revenues, or dramatically cutting expenditures, governments are engaging in what is functionally a sophisticated, state-sponsored Ponzi scheme by issuing massive tranches of new, higher-yielding debt simply to pay the interest on the old debt. When a private, publicly traded corporation engages in this behavior, it is eventually forced into bankruptcy and aggressively liquidated. When a sovereign government engages in this behavior, it forces its captive central bank to artificially suppress interest rates or outright print new currency to buy the debt, a process that fundamentally destroys the purchasing power of the working class through inflation.

The crisis will not arrive with a dramatic, televised Lehman Brothers moment; it will arrive when international bond vigilantes and foreign creditors finally refuse to finance the delusion, triggering a sudden, violent reprisal and a failed auction in the sovereign bond market.

The data grid below demonstrates the escalating, inescapable trap of sovereign debt across major developed economies, tracking the shift from artificial stability to systemic vulnerability.

| Economic Metric | The Era of “Free Money” (2010s to early 2020s) | The Era of Fiscal Dominance (2026 and Beyond) |

| Cost of Sovereign Debt | Near-zero or negative real yields across major developed nations. | Historically normalized yields compounding rapidly against massive, unreduced principal balances. |

| Debt-to-GDP Ratios | Elevated, but theoretically manageable through sustained, high economic growth. | Mathematically unpayable through standard taxation or organic GDP growth projections. |

| Central Bank Posture | Fiercely independent, focusing solely on inflation targeting and employment. | Subservient to treasury funding needs; trapped by the threat of triggering sovereign insolvency. |

| Market Discipline | Entirely absent, as central banks acted as buyers of first and absolute last resort. | Returning violently, as persistent inflation strictly prevents further quantitative easing bailouts. |

Demographic Time Bombs as Causes of the Next Global Financial Crisis

Moving beyond the ledgers of central banks, a far more insidious and entirely irreversible biological reality is setting in. The shifting global demographic pyramid represents one of the most undeniable, mathematically certain, and aggressively ignored Causes of the Next Global Financial Crisis. The developed world, alongside massive, highly industrialized economies like China, is aging at an unprecedented, historic rate. The “demographic dividend” (the highly lucrative economic period when a large, productive working-age population supports a relatively small number of dependents and retirees) has fully inverted. We are now entering a harsh new era where a rapidly shrinking pool of younger, productive workers is being taxed at increasingly punishing rates to support the unfunded pension, healthcare, and infrastructure liabilities of a massive, politically untouchable older generation.

Every credible economist and policymaker is fully aware of this looming demographic cliff. The actuarial math has been glaringly clear for decades. Yet, attempting to meaningfully raise the retirement age, reduce defined pension benefits, or fundamentally restructure healthcare delivery costs is universally considered political suicide. Therefore, leaders actively choose absolute inaction. They maintain the elaborate illusion that these massive, mid-20th-century social contracts can be fully honored in the 21st century without triggering a catastrophic tax burden on the productive economy.

When the dependency ratio (the ratio of non-working citizens to working citizens) crosses the critical threshold, the resultant collapse in national productivity and the simultaneous explosion in mandatory state expenditures will shatter national budgets. This dynamic will cause severe capital flight, as the young and highly skilled simply refuse to participate in an economy designed exclusively to extract their wealth to fund the past.

This comparative matrix highlights the profound structural shift in global demographics and the resulting, unavoidable fiscal strain it places on the macro-economy.

| Demographic Reality | The Post-War Boom Economy | The Aging Economy (2026 and Beyond) |

| Worker-to-Retiree Ratio | Highly favorable, generating massive tax surpluses (e.g., 5 workers to 1 retiree). | Rapidly deteriorating, crushing tax bases (approaching 2 to 1 or worse in key industrialized nations). |

| Tax Base Dynamics | Expanding organically, easily funding the creation of modern safety nets. | Shrinking in real terms, requiring significantly higher individual tax burdens to maintain baseline services. |

| Capital Allocation | Directed aggressively toward innovation, infrastructure buildout, and growth. | Diverted massively away from innovation, absorbed by healthcare, pensions, and elder care. |

| Political Leverage | Balanced between future infrastructure investment and current consumption. | Heavily, disproportionately skewed toward preserving current consumption for older, highly active voting blocs. |

Regulatory Paralysis and the Causes of the Next Global Financial Crisis

The systemic cowardice extends far beyond elected politicians; it deeply infects the supposedly independent regulatory bodies and central banks. Central bankers are currently trapped in a paralyzed state of their own making, establishing their institutional hesitation as one of the primary Causes of the Next Global Financial Crisis. Having spent more than a decade aggressively manipulating markets to smooth out every minor economic bump through quantitative easing, they have effectively destroyed the natural, necessary business cycle.

Now, they face an impossible, historic trilemma. They cannot raise interest rates high enough to truly kill embedded, structural inflation without immediately bankrupting their highly leveraged sovereign governments and crashing the commercial real estate market. They cannot lower rates without instantly re-igniting devastating inflationary fires that crush the working class. And they cannot simply maintain the restrictive status quo without starving the private sector of vital growth capital.

Instead of admitting that a painful, protracted recession is the necessary, healthy cure for a decade of rampant malinvestment, regulators rely on convoluted forward guidance, semantic games, and targeted market manipulation to delay the inevitable pain. This regulatory paralysis ensures that “zombie companies” (unprofitable, highly indebted firms that only survive because they can roll over artificially cheap debt) continue to drain labor and resources from productive, innovative enterprises. According to various economic monitors, the percentage of these zombie firms has crept upward globally. By refusing to let the economic forest burn naturally, policymakers have allowed the deadwood to pile up so high that the inevitable fire will take down the entire ecosystem.

The metrics below demonstrate the impossible corners into which regulatory bodies have painted themselves, sacrificing long-term stability for short-term optics.

| Regulatory Dilemma | The Necessary Action (Economic Reality) | The Institutional Reality Preventing Action (The Fear) |

| Zombie Corporations | Allow mass bankruptcies to clear out deep, systemic malinvestment. | Utter fear of triggering immediate spikes in unemployment and a severe GDP contraction. |

| Inflation Control | Maintain deeply restrictive, positive real interest rates for years. | Immense political pressure from highly leveraged governments facing debt death-spirals. |

| Banking Regulation | Force strict mark-to-market accounting on all sovereign bond holdings. | The terrifying acknowledgment that many regional banks are technically insolvent today. |

| Market Volatility | Allow natural price discovery to return, even if it causes a severe stock market crash. | The unwritten institutional mandate to “protect” financial markets and retirement accounts from any significant drawdown. |

The Illusion of Liquidity: Unseen Causes of the Next Global Financial Crisis

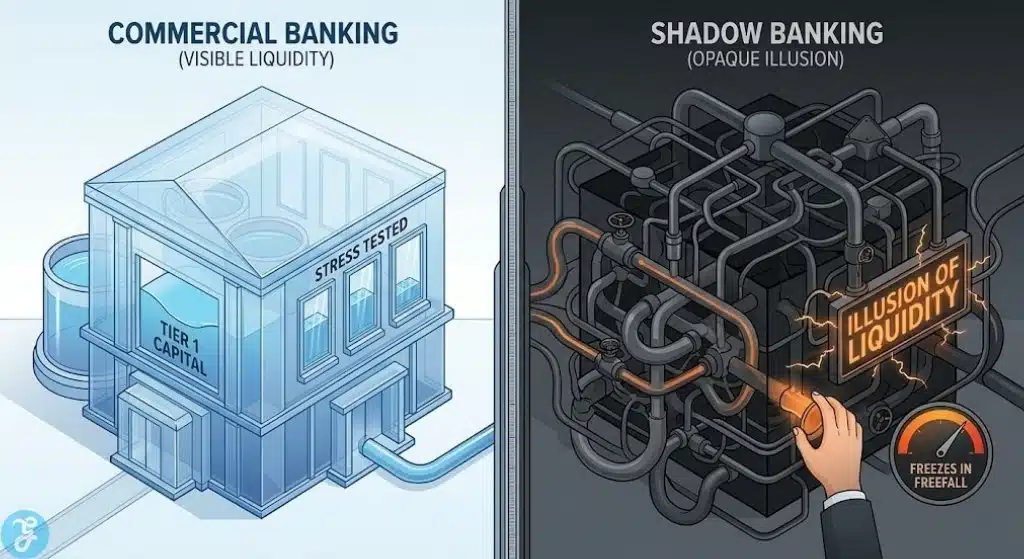

While global regulators frequently point to heavily capitalized, tier-one commercial banks as definitive proof of a safe, de-risked financial system, they willfully ignore the fact that the systemic risk hasn’t actually disappeared; it has simply hidden in the shadows. The massive, unregulated explosion of the shadow banking system, encompassing private credit, unlisted bespoke derivatives, and highly leveraged non-bank financial institutions (NBFIs), is a direct, intended result of public policy, firmly positioning it among the Causes of the Next Global Financial Crisis. When regulators aggressively squeezed the traditional banks with capital requirements after 2008, the demand for capital didn’t vanish; it simply flowed to the least regulated, most opaque corners of the financial universe. The private credit market alone has ballooned into a multi-trillion-dollar industry, operating largely outside the purview of traditional central bank oversight.

Policymakers celebrate the apparent stability of the main street retail banks while conveniently ignoring the trillions of dollars of unseen, interwoven leverage building up in private markets. This creates a dangerous “illusion of liquidity.” Because these private credit markets and bespoke assets are rarely marked to market, the assets appear completely stable and highly valuable on paper. However, in a true systemic stress event, when institutional investors all rush for the exit simultaneously, they will discover that the liquidity they assumed was readily available was entirely fictional. The failure of policymakers to drag these shadow systems into the light, entirely out of fear of disrupting the fragile credit status quo, guarantees that the next crash will occur in markets we cannot even accurately measure until they are already in freefall.

This structural analysis breaks down the dangerous migration of systemic risk, moving from visible, regulated sectors into invisible, highly leveraged shadows.

| Financial Sector | Transparency & Oversight Level | Leverage Dynamics | Systemic Threat Level in 2026 |

| Traditional Commercial Banks | Very High (Heavily Regulated and Audited) | Tightly constrained by Basel III and rigorous stress tests. | Low to Moderate (Well-capitalized, but holding vulnerabilities in sovereign debt and commercial real estate). |

| Private Credit Markets | Very Low (Opaque, Bilateral Agreements) | High, increasingly involving complex, covenant-lite loans to heavily indebted corporations. | Critical (Massive pools of illiquid assets masquerading as stable, reliable investments). |

| Non-Bank Market Makers | Low (Proprietary Algorithmic Trading) | Extreme leverage utilized to provide micro-second liquidity in equities and treasuries. | High (Highly prone to flash-crashes and sudden, coordinated withdrawals of liquidity). |

| Sovereign Bond Markets | High (Publicly Traded and Tracked) | Maximum leverage, backed entirely by the future taxation of shrinking demographics. | Severe (The foundational collateral of the entire global financial system is fundamentally deteriorating). |

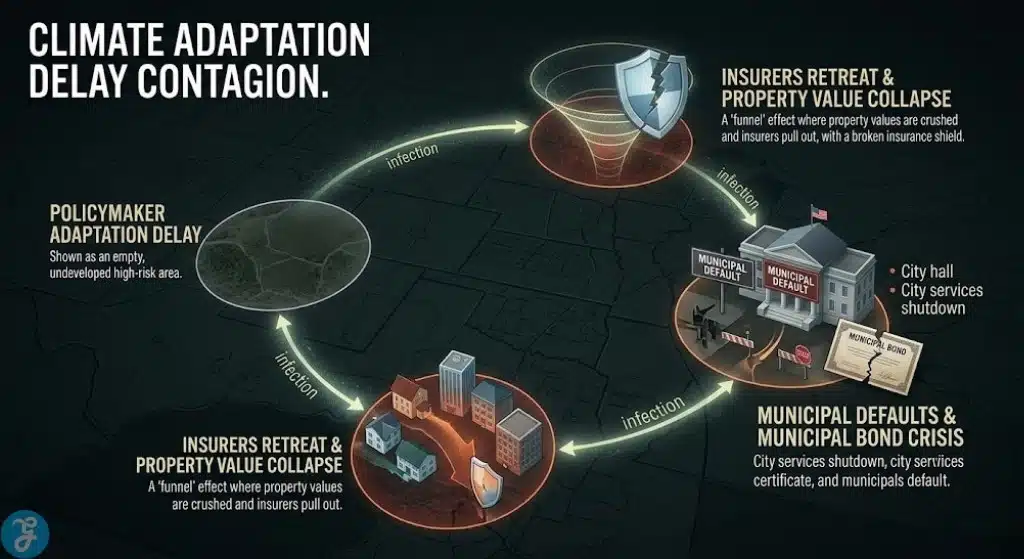

Climate Adaptation Delay as One of the Causes of the Next Global Financial Crisis

Finally, it is absolutely critical to understand that the economic threat of climate change is no longer just a distant environmental issue; it is a profound, immediate financial crisis driven entirely by political delay, solidifying it as one of the major Causes of the Next Global Financial Crisis. We are not talking about abstract carbon credits or the long-term green energy transition; we are talking about the deliberate, willful failure of local and federal governments to adapt physical infrastructure and financial models to a mathematically certain increase in severe, highly destructive weather events.

Global real estate markets and entire regional economies are entirely, inextricably dependent on the availability of affordable property insurance. Yet, because local policymakers have refused to implement realistic zoning laws or mandate incredibly expensive infrastructure upgrades in high-risk coastal and wildfire zones, the insurance industry is quietly but rapidly retreating. Major insurers pulling out of states like California and Florida are not anomalies; they are the canary in the coal mine.

When uninsurable physical risks are finally priced into the market by the private sector, property values in these highly vulnerable, over-developed areas will collapse overnight. This will wipe out trillions in middle-class generational wealth, trigger a wave of mortgage defaults, and precipitate massive municipal bankruptcies. Politicians are currently subsidizing coastal and fire-zone insurance to keep local voters happy today, socializing a catastrophic, inevitable risk that will ultimately bankrupt the state tomorrow.

The breakdown below highlights the financial contagion spreading from ignored, unmitigated environmental realities directly into the core economy.

| Sector Impacted | The Political Inaction | The Resulting Financial Contagion |

| Property Insurance | Refusing to let private insurers accurately price premiums based on updated actuarial risk models. | Insurers completely abandon entire states, leaving homeowners functionally uninsurable and crashing regional mortgage markets. |

| Real Estate Markets | Continuing to incentivize and subsidize residential development in high-risk flood and fire zones. | Sudden, catastrophic repricing of coastal and high-risk real estate, utterly destroying localized generational wealth. |

| Municipal Bonds | Failing to aggressively upgrade seawalls, drainage systems, and grid resilience due to budget constraints. | Cities face massive disaster recovery costs without a functioning tax base, leading inevitably to municipal bond defaults. |

| Supply Chain Logistics | Ignoring the extreme vulnerability of vital shipping ports and rail hubs to rising sea levels and extreme weather. | Severe, highly inflationary disruptions to global trade when critical logistics nodes are unexpectedly incapacitated. |

Breaking the Cycle: Mitigating the Causes of the Next Global Financial Crisis

We are rapidly running out of runway to kick this can down the road. The Causes of the Next Global Financial Crisis are fully formed, clearly visible to anyone willing to look at the math, and entirely structural in nature. Averting a total, systemic collapse requires a fundamental, aggressive rewiring of our political and economic incentives. We can no longer afford to reward leaders who deliver short-term sugar highs at the expense of long-term national solvency. The era of easy money, state-subsidized risk, and collective demographic denial must end voluntarily and violently, or it will end involuntarily and catastrophically.

To break this vicious cycle of cowardice, we must demand the institution of independent fiscal councils with the actual, legally binding authority to cap deficit spending, operating much like independent central banks cap inflation. We must force strict mark-to-market accounting on sovereign debt and private credit alike, ruthlessly stripping away the illusion of solvency. Above all, we must mature as an electorate and embrace the painful, absolutely necessary recessions that clear out corporate malinvestment, rather than allowing politicians to continually borrow against our children’s future to buy today’s fleeting complacency.

The final structural overview outlines the necessary, incredibly painful steps required to force accountability and stability back into the global system.

| Required Intervention | Immediate Pain (The Intense Political Cost) | Long-Term Benefit (The Economic Salvation) |

| Strict Austerity & Entitlement Reform | Massive voter backlash, guaranteed loss of elections, and widespread social unrest. | Securing the long-term solvency of the state and preventing total currency collapse. |

| Allowing True Price Discovery in Sovereign Debt | Spiking borrowing costs, forcing immediate, draconian government spending cuts. | Restoring vital market discipline and finally ending the destructive era of fiscal dominance. |

| Transparent Pricing of Climate Risk | Crashing property values in vulnerable, heavily over-developed coastal and forest zones. | Preventing a massive, systemic banking crisis tied inextricably to uninsurable residential real estate. |

| Letting Zombie Companies Fail | Sudden spikes in unemployment and a severe, deep, and protracted recession. | Freeing up and reallocating trapped capital to highly productive, genuinely innovative industries. |

The Bill Comes Due: Surviving the Causes of the Next Global Financial Crisis

The great tragedy of the modern global economy is that our impending doom is entirely, one hundred percent self-inflicted. We are not facing a mysterious virus, an unpredictable meteor strike, or a sudden, uncontrollable technological failure. We are facing the cold, hard mathematical certainty of compounding debt, shifting demographics, and dangerously delayed maintenance. The politicians and regulators of 2026 have built a massive, incredibly fragile glass house, and rather than undertaking the hard work of replacing the shattered panes, they are simply drawing the curtains and praying the wind doesn’t blow.

When the macroeconomic wind finally does blow, the subsequent collapse will inevitably be blamed on everything from unregulated algorithmic trading to the malicious actions of foreign adversaries. But do not be fooled by the inevitable political misdirection. When the sovereign bond auctions fail, when the state pensions are aggressively slashed, and when the illiquid shadow banking markets permanently freeze, remember exactly where the failure originated.

The next financial crisis will not be a failure of free-market capitalism; it will be a towering monument to the cowardice of those elected and appointed to manage it. Prepare your portfolios and your businesses accordingly, because the bill is finally coming due, and the policymakers have already signaled, through their inaction, that they fully intend to make you pay it.