The New Zealand financial landscape has shifted dramatically into 2026, with traditional “Big Four” banks facing stiff competition from agile, app-based platforms. Whether you are trying to outpace inflation with a high-interest savings account, automate your sole trader taxes, or trade global stocks with a few taps, the current crop of digital finance tools offers levels of transparency and speed that were previously unavailable to Kiwis.

How Did We Select Our 9 Best Neobanks and Digital Finance Apps?

To define the top performers for 2026, we evaluated platforms based on their regulatory standing in New Zealand, the competitiveness of their fee structures, and the actual utility they provide to local users. Our selection process filtered out apps that lack specific NZD support or local compliance.

-

Local Utility: We prioritized apps that offer NZ-specific features like IRD tax automation or local bank transfer capabilities.

-

Cost Efficiency: We looked at foreign exchange margins and transaction fees to ensure users keep more of their money.

-

Ease of Access: We tested the onboarding speed and the intuitiveness of the mobile interface.

The following framework highlights the specific metrics we used to rank these digital finance solutions.

| Feature Category | Primary Focus | User Benefit |

| Regulatory Status | FSP Registration | Security and consumer protection |

| Interest Returns | Annual Percentage Yield | Passive wealth growth |

| FX Transparency | Mid-market rates | Cheaper international travel and shopping |

| Platform Versatility | Multi-asset support | Consolidation of financial tasks |

The Top 9: Best Neobanks New Zealand 2025 and 2026 Options

These platforms represent the cutting edge of Kiwi fintech, ranging from full-service neobank experiences to specialized tools for home buyers and freelancers. Navigating these options allows you to build a custom financial stack that works harder than a standard current account.

1. Revolut

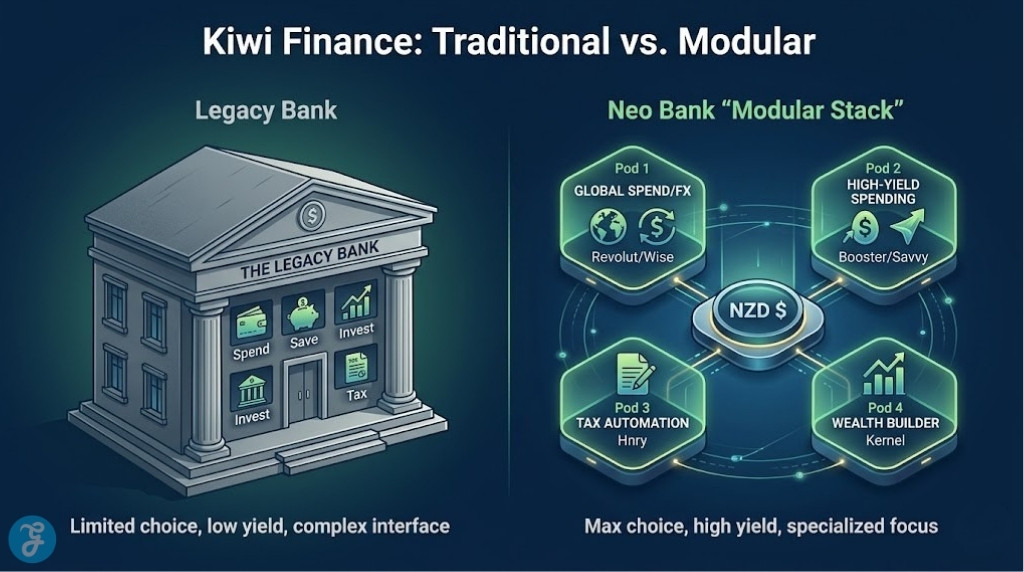

As the most complete “neobank” experience available in New Zealand, Revolut offers a sophisticated multi-currency account that handles everything from daily budgeting to global travel. In 2026, it remains a powerhouse for those who want a single app for spending, sending, and saving across dozens of different currencies.

Best for: Digital nomads and frequent international travelers.

Why We Chose It: It provides an unrivaled suite of features including instant bill splitting, virtual disposable cards for security, and mid-market exchange rates during market hours.

Things to consider: Premium features like airport lounge access and higher ATM limits require a monthly subscription fee.

2. Wise (formerly TransferWise)

Wise has become the gold standard for Kiwis who need to move money across borders without the hidden markups typically charged by major banks. While not a traditional bank, its multi-currency debit card is an essential tool for anyone shopping on international websites or receiving income from overseas.

Best for: Low-cost foreign exchange and receiving international payments.

Why We Chose It: They are extremely transparent about their fees and use the real mid-market exchange rate with no hidden spreads.

Things to consider: It does not currently offer the same level of domestic “daily banking” features, such as automated direct debits, as some local competitors.

3. Dosh

Dosh is New Zealand’s first true homegrown digital wallet and has expanded significantly into the rewards space. By partnering with major local retailers, it allows users to earn “Phone Dollars” and other rewards on their everyday spending while offering a sleek, mobile-first payment experience.

Best for: Earning rewards on daily NZ-based spending.

Why We Chose It: The 1% cashback (in Phone Dollars) on eligible spend and the ability to send money instantly to any mobile number in NZ makes it highly convenient for local use.

Things to consider: The platform is primarily mobile-based, which may not suit users who prefer managing large finances via a desktop interface.

4. Booster Savvy

Booster Savvy functions like a high-interest transaction account, offering a competitive return on every dollar you hold in the account. Unlike a term deposit, your funds remain fully accessible via a Mastercard debit card, making it a hybrid between a savings and a checking account.

Best for: Maximizing interest on money you plan to spend.

Why We Chose It: It currently offers a return of 2.25% p.a. (before tax) on all balances, with no monthly fees or minimum deposit requirements.

Things to consider: As it is technically a PIE (Portfolio Investment Entity) fund, the “interest” is a fund return, though it is designed for high stability.

5. Kernel Wealth

Kernel has evolved from a simple index fund provider into a comprehensive wealth app. Their “Smart Saver” account is one of the most popular low-risk options for Kiwis looking for a better return than a standard bank savings account without the complexity of the stock market.

Best for: Long-term passive investors and cash savers.

Why We Chose It: The Smart Saver account offers a high 2.25% p.a. interest rate with no transaction fees, and the app makes it incredibly easy to automate your savings.

Things to consider: You must be a New Zealand resident to use the platform, and withdrawals can take 1–2 business days to hit your main bank account.

6. Hnry

For the growing population of Kiwi freelancers and contractors, Hnry is an indispensable digital finance app. It acts as both a bank account and an automated accountant, calculating and paying your taxes, ACC, and student loan contributions every time you get paid.

Best for: Sole traders, freelancers, and contractors.

Why We Chose It: It completely removes the stress of “tax time” by automating all filings for a simple 1% fee, capped annually.

Things to consider: It is specifically designed for self-employed income and is not a replacement for a standard personal bank account for employees.

Sharesies remains the most accessible gateway for New Zealanders to enter the world of investing. With no minimum investment and a highly educational interface, it allows users to buy fractional shares in thousands of companies across the NZX, ASX, and US markets.

Best for: Beginner investors and those wanting to build a portfolio with small amounts.

Why We Chose It: The user experience is world-class, and their “Save” account offers a decent interest rate for cash waiting to be invested.

Things to consider: Their fee structure has shifted toward a monthly subscription model for high-frequency traders, which may be more expensive for occasional investors.

8. Tiger Brokers

Tiger Brokers provides a more advanced “pro-level” trading experience compared to other local apps. In 2026, it has integrated sophisticated AI analysis tools and deeper market data to help serious traders navigate global derivatives, options, and stocks.

Best for: Experienced traders and those looking for deep technical analysis tools.

Why We Chose It: They offer some of the lowest brokerage fees in the market and provide a very high level of market insight and data for global exchanges.

Things to consider: The interface can be overwhelming for beginners and is better suited for those with some trading experience.

9. Aera

Aera is a niche digital finance app specifically targeting the first-home buyer market in New Zealand. It uses a unique “Fast Track” system to help users build their deposit faster through high-interest accounts and “Aera Credits” earned through financial coaching modules.

Best for: Young Kiwis saving for their first home deposit.

Why We Chose It: It combines financial advice from registered advisors with a high-interest savings environment to make the goal of homeownership feel more attainable.

Things to consider: Its utility is limited once you have actually purchased a home, as its features are highly specialized for the pre-purchase phase.

An Overview Of Best Neobanks New Zealand 2025 and 2026

The current digital finance market is highly fragmented, with each app serving a specific niche. To understand where your money belongs, you should compare the primary utility and the expected returns or costs associated with each platform.

| App Name | Primary Function | Key Benefit | Typical Cost |

| Revolut | Daily Banking / FX | Multi-currency ease | Free to $22.99/mo |

| Wise | International Transfers | Mid-market FX rates | Transaction-based fees |

| Booster Savvy | High-Yield Spending | 2.25% p.a. return | No monthly fees |

| Hnry | Tax & Accounting | Automatic tax filing | 1% of income (capped) |

| Kernel | Saving & Investing | 2.25% p.a. Saver | No fee for basic plan |

Our Top 3 Picks and Why?

-

Revolut: This is the top choice for the modern Kiwi lifestyle. It is the closest thing New Zealand has to a global neobank, providing a level of budgeting and currency flexibility that traditional banks simply cannot match.

-

Hnry: For anyone earning “side-hustle” or freelance income, Hnry is non-negotiable. The peace of mind that comes from knowing your taxes are already paid and filed is worth the 1% fee many times over.

-

Booster Savvy: We selected this because it solves the “interest vs. access” dilemma. Earning 2.25% on money you are actively spending via a debit card is a highly efficient way to manage a daily budget in 2026.

How to Choose the Right Best Neobanks New Zealand 2025 by Yourself?

Selecting your digital finance stack depends entirely on your specific goals—whether that is saving for a home, traveling the world, or simplifying your taxes. Use the following framework to identify which tools align with your current financial priorities.

The Selection Framework

-

Identify Your Pain Point: Are you losing money on bank fees, or are you struggling to save? Choose an app that solves your specific problem first.

-

Check the Interest Rates: In the current 2026 environment, look for at least 2% p.a. for any “on-call” or transaction-linked savings.

-

Verify Tax Compliance: If you are using international apps like Revolut or Tiger Brokers, ensure you understand your Resident Withholding Tax (RWT) obligations.

-

Ease of Withdrawal: Always test how quickly you can move your money back to a traditional NZ bank account in case of an emergency.

The following matrix helps you decide which app to prioritize based on your primary financial behavior.

| Choose this App if… | Primary User Profile |

| You want to spend 2.25% interest via a card. | The “Daily Maximizer” |

| You get paid by overseas clients. | The “Global Freelancer” |

| You are starting your first investment. | The “Beginner Wealth Builder” |

| You want to see your tax paid in real-time. | The “Sole Trader” |

The Final Checklist

-

Verify that the app is registered on the New Zealand Financial Service Providers Register (FSPR).

-

Check if the account offers a physical debit card or just a virtual one.

-

Ensure your smartphone is compatible with the app’s latest 2026 security updates.

-

Confirm the withdrawal timeframes for any “Smart Saver” or “Wallet” accounts.

-

Compare the foreign exchange margins if you plan on using the card overseas.

Optimizing Your Financial Future in 2026

The era of the “all-in-one” traditional bank is fading, replaced by a modular approach where you can pick and choose the best tools for every aspect of your life. By combining a high-interest spending account like Savvy with a tax-automation tool like Hnry and a global travel card like Revolut, you can create a financial ecosystem that is more efficient, more profitable, and significantly easier to manage than a single legacy bank account.

Frequently Asked Questions About Best Neobanks New Zealand 2025

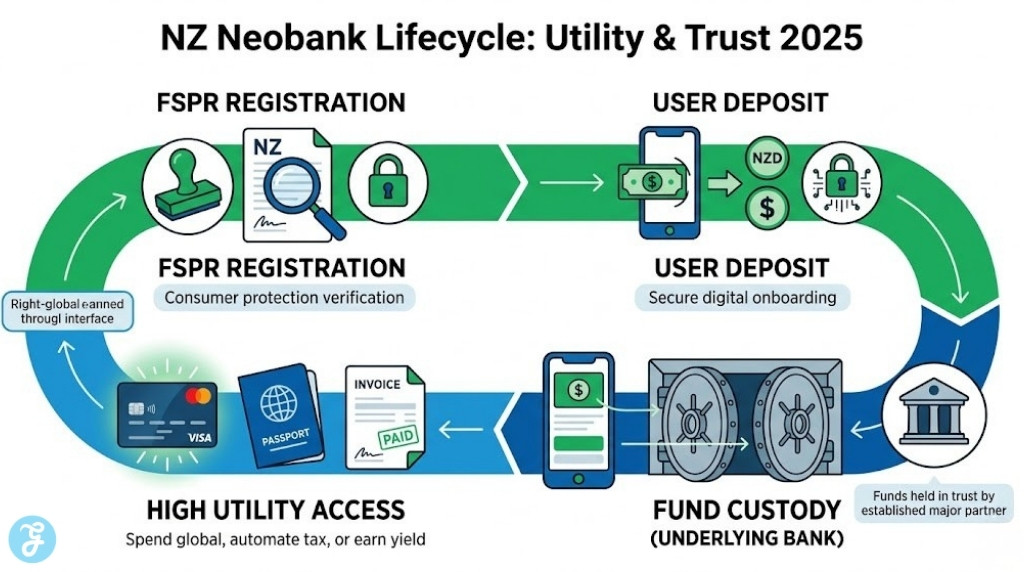

Are neobanks in New Zealand safe?

Answer: Yes, provided they are registered Financial Service Providers (FSP) and adhere to local anti-money laundering and consumer protection laws. Most “neobanks” in NZ partner with registered banks to hold user funds in trust.

Can I have my salary paid directly into these apps?

Answer: For apps like Revolut or Booster Savvy, you can generally provide your account number to your employer for direct credit. For specialized apps like Hnry, this is actually the required way to operate.

Do I have to pay tax on the interest I earn in these apps?

Answer: Yes, you are liable for Resident Withholding Tax (RWT) or PIE tax on any returns. Most NZ-based apps like Kernel and Booster automate this for you based on your provided IRD number.

Can I use these apps at any ATM in New Zealand?

Answer: If the app provides a physical Mastercard or Visa debit card (like Wise, Revolut, or Booster), it will work at any NZ ATM, though some third-party ATM fees may apply.

Which app is best for kids and teens?

Answer: Revolut and Sharesies both offer specific “junior” or “kids” accounts that allow parents to oversee spending and investing while teaching financial literacy in a digital-first environment.