Groceries and gas are not “fun” expenses, but they are reliable. Most people buy food every week, and many drivers fill up several times a month. That is why the best credit cards for gas and groceries can make a real difference without changing your lifestyle. This guide is built for everyday use, not complicated points tricks. You will see cards that pay extra cash back at supermarkets, cards that reward fuel and EV charging, and flexible options that adjust to how you spend each month.

Rewards change, and each bank defines categories in its own way. So the goal is not to chase a perfect headline number. The goal is to pick a card that matches where you shop, how much you spend, and how simple you want your setup to be. If you want quick results, focus on two things. First, get a strong rate on groceries or gas. Second, use a backup card for everything that does not fit the bonus rules.

| What You Want | What You Will Learn Here |

| Earn more on essentials | Which cards reward groceries and gas the most |

| Avoid reward surprises | Caps, category rules, and common “does not count” traps |

| Keep it simple | Easy 1-card and 2-card setups that work all year |

| Choose with confidence | Who each card fits, and who should skip it |

Quick Comparison: Best Cards at a Glance

There is no one card that wins for every person. Some households spend far more on groceries than gas, especially families. Some spend more on fuel, especially commuters and drivers who travel for work. Others shop mostly at warehouse clubs, where many “supermarket” bonuses do not apply. A smart way to start is by narrowing the list to three or four options. Look for your main shopping style, then check the caps. A card that earns a high rate but caps your spending quickly can still be great, but you may need a backup card once you hit the limit.

Also pay attention to annual fees. Some fee cards easily pay for themselves if you spend enough in the top categories. If your grocery and gas budget is modest, a no-fee card can be the better long-term choice. Finally, keep redemption in mind. “Cash back” is not always cash to your bank account. Some cards pay rewards as a statement credit, some as a deposit, and some as store or carrier rewards.

| Card | Best For | Grocery Rewards | Gas Rewards | Main Limit To Watch |

| Amex Blue Cash Preferred | Big supermarket spending | 6% up to $6,000 yearly, then 1% | 3% | Annual fee and grocery cap |

| Amex Blue Cash Everyday | No-fee everyday | 3% up to $6,000 yearly per category, then 1% | 3% up to $6,000 yearly, then 1% | Category caps |

| Citi Custom Cash | One-category maxing | Up to 5% if top category | Up to 5% if top category | $500 cap per billing cycle |

| PNC Cash Rewards | Strong gas focus | 2% | 4% | $8,000 annual cap on bonus categories |

| Bank of America Customized Cash | Custom gas pick | 2% | 3% choice category | $2,500 cap per quarter on bonus categories |

| Chase Freedom Flex | Rotating planners | Sometimes 5% | Sometimes 5% | Activation and quarterly cap |

| Discover it Cash Back | Rotating planners | Sometimes 5% | Sometimes 5% | Activation and quarterly cap |

| AAA Daily Advantage | Grocery-heavy households | 5% (capped yearly rewards) | 3% | Annual cap on high rewards |

| AAA Travel Advantage | Drivers and EV charging | 3% | 5% (capped yearly rewards) | Annual cap on top gas rewards |

| Costco Anywhere Visa | Costco fuel routine | Not a top grocery card | 5% at Costco gas, 4% elsewhere (cap) | Membership and annual cap |

| Sam’s Club Mastercard | Sam’s fuel routine | Not a top grocery card | 5% gas up to $6,000 yearly, then 1% | Membership and cap |

| U.S. Bank Shopper Cash Rewards | Big-box grocery runs | 6% at chosen retailers (cap) | 3% choice category (cap) | Annual fee after first year |

| Verizon Visa | Verizon customers | 4% | 4% | Rewards tied to Verizon |

| Venmo Credit Card | Auto-adjusting rewards | Can be top category | Can be top category | Rates depend on your spend mix |

| Citi Double Cash | Simple backup | 2% | 2% | Must pay bill to earn full 2% |

Best Credit Cards for Gas and Groceries: What to Look For

Choosing the right card is mostly about matching rules to your habits. The biggest mistake people make is assuming “groceries” means any place that sells food. Many cards mean traditional supermarkets, not warehouse clubs or big discount superstores. The same goes for gas, where paying inside the station can sometimes code differently than fuel at the pump. Caps matter just as much as rates. A 6% grocery rate looks amazing, but it may only apply up to a yearly limit. If your household spends above that, you need a plan for overflow. That is where a flat-rate 2% card often saves the day.

Fees can be worth it, but only if you earn enough extra cash back to beat the fee. If you are unsure, start with a no-fee card. You can always upgrade later once you see your real spending pattern. Also check redemption. Some issuers let you cash out easily as statement credit or bank deposit. Others push you toward brand-specific rewards. Neither is “bad,” but it should match what you want.

Grocery Category Rules That Change the Results

Many issuers exclude warehouse clubs, superstores, and some online grocery platforms from the grocery category. If most of your food spending happens at those places, a “supermarket card” may underperform. In that case, you may want a big-box rewards card or a flexible category card.

Gas, EV Charging, and How Purchases Code

Some cards now include EV charging in their gas category, while others treat it separately. If you drive an EV or plan to switch soon, look for clear language about charging stations. For gas vehicles, paying at the pump is usually the safest way to ensure the purchase codes as fuel.

| Question | Why It Matters |

| Where do you buy most groceries | Supermarket vs warehouse vs superstore changes rewards |

| How much do you spend monthly | Helps you judge caps and annual fees |

| How do you fuel up | Gas station, warehouse gas, or EV charging affects best card |

| Do you want simplicity | Determines whether rotating categories are worth it |

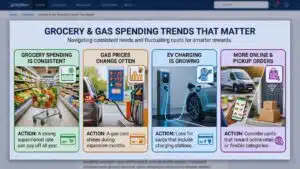

Grocery and Gas Spending Trends That Matter

Groceries tend to be steady because eating at home is a normal budget item. Even when prices change, most households still buy similar types of items each week. That makes grocery rewards one of the most predictable ways to earn cash back, especially if your card codes your store as a supermarket. Gas is different. Your driving might stay the same, but prices can rise or fall over the year. That means your fuel spending can swing even if your habits do not. A strong gas category card helps most when prices are high, but a stable 2% backup can keep things consistent when category rules get messy.

Another shift is EV charging. More cards now mention charging stations, but not all. If you are in a mixed household with both gas and EV spending, look for a card that covers both in one category or use two cards with clear rules. Finally, shopping patterns matter. Many people now mix in pickup orders, grocery delivery, and online retailers for pantry basics. Those purchases may not always count as “groceries,” so it helps to choose a card with flexible categories or online retail bonuses.

| Trend | What to Do |

| Grocery spending is consistent | A strong supermarket rate can pay off all year |

| Gas prices change often | A gas card shines during expensive months |

| EV charging is growing | Look for cards that include charging stations |

| More online and pickup orders | Consider cards that reward online retail or flexible categories |

15 Best Credit Cards for Gas and Groceries

This list covers a mix of styles so you can match the card to your routine. Some picks are best as your main card. Others work best as a “specialist” card for one category, paired with a backup card for everything else. As you read, focus on three details. First, does your main store match the card’s grocery definition. Second, can your spending fit under the cap. Third, do you like how the rewards are paid out.

If you want a simple approach, choose one strong grocery-and-gas card, then add a flat-rate 2% backup for overflow. If you enjoy optimizing, you can combine a 5% category card with a rotating-category card and get great returns, but only if you stay organized.

| Your Style | Cards to Consider First |

| Traditional supermarkets most weeks | Blue Cash Preferred, Blue Cash Everyday, AAA Daily Advantage |

| Big fuel budget | PNC Cash Rewards, AAA Travel Advantage, Costco Anywhere Visa, Sam’s Club Mastercard |

| Want set-it-and-forget-it | Blue Cash Everyday, Verizon Visa, Citi Double Cash |

| Want one-category maxing | Citi Custom Cash |

| Big-box grocery shoppers | U.S. Bank Shopper Cash Rewards |

| Like rotating deals | Chase Freedom Flex, Discover it Cash Back |

1) Amex Blue Cash Preferred

This card is built for people who spend heavily at supermarkets. The headline benefit is a high cash back rate on supermarket purchases, but it comes with a yearly cap. If your grocery budget fits under that cap, the value can be strong and easy to feel every month. It also earns a solid rate on gas, which makes it useful beyond just grocery runs. Many people use it for groceries and fuel, then switch to a backup card for everything else.

The tradeoff is the annual fee. For families and bigger households, the extra grocery rewards can cover the fee and then some. For smaller budgets, a no-fee option may be more practical. This card is best if you buy groceries at traditional supermarkets. If most of your food spending is at warehouse clubs or superstores, you may not get the rate you expect.

| Detail | Summary |

| Grocery rewards | 6% at supermarkets up to $6,000 yearly, then 1% |

| Gas rewards | 3% at gas stations |

| Best for | High supermarket spenders who can beat the annual fee |

| Watch for | Annual fee and the $6,000 grocery cap |

2) Amex Blue Cash Everyday

This is the simpler, no-fee sibling. It earns bonus cash back on supermarkets and gas stations, and also adds an online retail category. The key difference is that the bonus rate is capped each year in each category. For many people, this card is a clean starting point because it covers everyday spending without complicated tracking. If your grocery and gas totals are moderate, the caps may never bother you.

It also fits well in a two-card setup. You can use it for groceries, gas, and online shopping, then use a 2% card for everything else. Like most grocery-focused cards, the biggest risk is category definition. Some stores that feel like grocery stores may not code that way.

| Detail | Summary |

| Grocery rewards | 3% up to $6,000 yearly, then 1% |

| Gas rewards | 3% up to $6,000 yearly, then 1% |

| Extra bonus | 3% on online retail up to $6,000 yearly, then 1% |

| Watch for | Category caps and supermarket definition |

3) Citi Custom Cash

This card is a strong fit if you want 5% back in one category each billing cycle. It automatically gives the top rate in the category where you spend the most, up to a fixed spending limit, then drops to a lower rate. It works well when your spending is predictable. If groceries are always your top category, it becomes a grocery 5% card. If gas is your top category, it becomes a gas 5% card. You do not need to activate rotating categories.

The limit is the main drawback. Once you spend above the cap in that billing cycle, the extra spending earns the lower rate. Many people pair this card with a flat-rate 2% card. They use Custom Cash for the first chunk of groceries or gas each month, then switch to the backup card.

| Detail | Summary |

| Top rewards | 5% in your top eligible category |

| Cap | Up to $500 per billing cycle at the 5% rate |

| Best for | People who want one-category maxing without rotating calendars |

| Watch for | Spending above the cap earns a lower rate |

4) PNC Cash Rewards

If you want strong gas rewards with simple rules, this card is easy to understand. It offers a higher rate at gas stations, plus decent returns on dining and a lower bonus on groceries. The big detail is the annual cap across the bonus categories. Once you hit the combined yearly spending limit, the rate drops. For moderate spenders, this may not matter. For heavy spenders, you will want a backup card once you reach the cap.

This card is a good fit for drivers who spend more on fuel than groceries. It is also useful for people who want to avoid rotating categories and still earn better-than-average rewards on gas. Like all gas rewards cards, it helps to pay at the pump when possible. That can reduce the chance of odd category coding.

| Detail | Summary |

| Gas rewards | 4% at gas stations |

| Grocery rewards | 2% at grocery stores |

| Bonus cap | First $8,000 yearly in gas, dining, grocery combined |

| Watch for | Rate drops after the yearly cap |

5) Bank of America Customized Cash Rewards

This card is about control. You choose a 3% category, and gas is one of the options. At the same time, the card automatically earns 2% at grocery stores and wholesale clubs. The key limit is the quarterly cap shared across the 3% and 2% categories. If you spend heavily, you may hit the cap faster than expected, especially if you shop at warehouse clubs often.

This card can be especially useful if you already bank with the same institution and qualify for relationship perks. Those perks can increase your effective cash back rate, which changes the value a lot. It is best for people who want gas as a fixed bonus category and still want some grocery rewards. It is less ideal for people who want high grocery rates at traditional supermarkets.

| Detail | Summary |

| Gas option | 3% in a chosen category that can be gas |

| Grocery rewards | 2% at grocery stores and wholesale clubs |

| Cap | Up to $2,500 per quarter on combined bonus categories |

| Watch for | Quarterly cap can limit heavy spenders |

6) Chase Freedom Flex

This card is built around rotating 5% categories. Some quarters include groceries or gas, and other quarters focus on different categories. The upside is strong rewards when your spending matches the quarter. The main habit you need is activation. If you forget, you miss the 5% benefit for that quarter. There is also a quarterly cap on the 5% category spend.

Many people use this card as a “booster.” When the quarter matches groceries or gas, they use it heavily. When it does not, they switch to a different card. It is a good fit for organized people who like tracking categories. If you want a simple setup, a steady grocery-and-gas card may feel easier.

| Detail | Summary |

| Bonus model | 5% rotating categories with activation |

| Cap | Up to $1,500 per quarter in the bonus categories |

| Best for | People who will activate and track quarterly changes |

| Watch for | Missing activation means missing the 5% rate |

7) Discover it Cash Back

Discover uses a similar rotating model. You earn 5% in bonus categories each quarter after activation, up to the quarterly cap. When groceries or gas shows up, it can be a great way to boost returns. A major perk many people like is the first-year match on rewards for new cardholders. That can make the first year unusually valuable if you use the card heavily.

This card fits people who want strong rewards without an annual fee and are willing to activate categories. It also works well as a second card in a small two- or three-card wallet. For early 2026, groceries and wholesale clubs appear as a rotating quarter category, which shows how useful this card can be when it lines up with your needs.

| Detail | Summary |

| Bonus model | 5% rotating categories with activation |

| Cap | Up to $1,500 per quarter in bonus categories |

| Best for | People who like rotating deals and can stay organized |

| Watch for | Categories change each quarter, so you must adapt |

8) AAA Daily Advantage

This card is popular for one simple reason. It offers a very strong grocery rate, plus a solid return on gas and EV charging. For families that spend heavily at grocery stores, it can be a serious contender without an annual fee. The catch is an annual limit on high-rate rewards. After you hit the cap, the return drops. That means the best strategy is to use it for groceries until you reach the limit, then switch to a backup card.

It can also be useful if you shop at warehouse clubs, since some versions include those merchants in bonus categories. That can help households that split groceries between supermarkets and clubs. This card is best for people who want high grocery returns and are okay tracking a yearly cap. If you do not want any tracking, a flat-rate setup might feel easier.

| Detail | Summary |

| Grocery rewards | 5% (with an annual rewards cap) |

| Gas and EV | 3% on gas and EV charging |

| Best for | Grocery-heavy households seeking strong rates without a fee |

| Watch for | Annual cap on top rewards |

9) AAA Travel Advantage

This card flips the focus toward fuel. It offers a high return on gas and EV charging, with an annual cap on the top-tier gas rewards. It also adds a decent grocery rate, which keeps it from being a one-trick card. It fits drivers who want strong fuel rewards and still want some grocery coverage. If you commute daily or travel often, it can be a useful main gas card.

The annual cap matters, so heavy drivers should plan for overflow. That can be as simple as using a 2% card once you hit the limit. This card also works well for households that want to prepare for EV charging expenses. If you are adding an EV to the household, having clear charging rewards can be a plus.

| Detail | Summary |

| Gas and EV | 5% (with an annual rewards cap) |

| Grocery rewards | 3% at grocery stores |

| Best for | Drivers and EV chargers with consistent fuel spend |

| Watch for | Annual cap on top gas rewards |

10) Costco Anywhere Visa

This is a strong gas card for Costco members. It offers a high rate on gas purchased at Costco and a strong rate on eligible gas purchases elsewhere and on EV charging, up to a yearly spending cap, then a lower rate after that. It is not a top choice for grocery rewards in the traditional sense, because Costco is a warehouse club and many cards treat that differently. The real value is for people who regularly buy fuel at Costco.

Another key detail is redemption style. Rewards are typically provided in a yearly cycle rather than as instant monthly cash back. If you prefer monthly statement credits, this may feel less convenient. This card is best for Costco households that fuel up there often. Pair it with a supermarket-focused card if you also shop at regular grocery stores.

| Detail | Summary |

| Costco gas | 5% back at Costco gas |

| Other gas and EV | 4% on eligible gas and EV charging (combined cap) |

| Cap | First $7,000 yearly in eligible gas and EV spend, then 1% |

| Watch for | Membership requirement and yearly rewards schedule |

11) Sam’s Club Mastercard

This card is designed for Sam’s Club members who buy fuel often. It offers a high return on gas purchases up to an annual spending cap, then drops to a lower rate. For commuters, that cap can still cover most of the year. The value is strongest when Sam’s is already part of your routine. If you rarely shop there, the membership tie-in may not make sense.

This card also tends to be less impressive for groceries unless you specifically want rewards within the Sam’s system. Many people use it mainly as a gas card, then keep a separate grocery card. If you want a simple system, a good plan is to use this card for gas, then use a separate supermarket-focused card for groceries and a 2% card for overflow.

| Detail | Summary |

| Gas rewards | 5% on gas up to $6,000 yearly, then 1% |

| Best for | Sam’s members who buy gas regularly |

| Watch for | Membership and the $6,000 gas cap |

| Pair with | A supermarket card for groceries and a 2% backup |

12) U.S. Bank Shopper Cash Rewards

This card is a practical solution for people whose “grocery” spending is really big-box shopping. You can choose two retailers and earn a high rate on eligible spending at those retailers up to a quarterly cap. It also lets you choose an everyday category for extra rewards, and gas and EV charging is one of the common choices. That makes it useful for households that buy groceries at big retailers and want stronger fuel rewards too.

The big tradeoff is the annual fee after the first year, plus the need to manage quarterly caps. If your spending matches the chosen retailers, the math can still work out well. This card is best for people with consistent spending at a few major retailers. If you want a card that works anywhere without planning, a simpler cash back card may feel better.

| Detail | Summary |

| Retailer rewards | 6% at two chosen retailers (quarterly cap) |

| Gas and EV | 3% choice category (quarterly cap) |

| Fee | Annual fee after the first year |

| Watch for | Caps and choosing the right retailers |

13) Verizon Visa

This card is a strong everyday option for Verizon customers. It offers a high rate on grocery stores and gas, and it can include EV charging. If you already pay for Verizon service, the rewards can be easy to use. The main tradeoff is how rewards are redeemed. Rewards often work best inside the Verizon ecosystem, such as paying bills or buying devices and accessories. If you want pure cash to your bank account, this may feel limiting.

For the right person, though, it can be a clean one-card setup for groceries and gas. Many people like that it is simple and does not rely on rotating categories. It is best for people who plan to stay with Verizon long-term. If you switch carriers often, you may prefer a more universal cash back card.

| Detail | Summary |

| Grocery rewards | 4% at grocery stores |

| Gas and EV | 4% on gas and often EV charging |

| Best for | Verizon customers who can use Verizon-based rewards |

| Watch for | Rewards may feel less flexible than pure cash back |

14) Venmo Credit Card

This card adjusts to your spending each month. It gives the highest rate on your top eligible category and the second-highest rate on your next category. Groceries and gas are both eligible categories, which makes the card helpful for households with changing routines. It is a good fit for people who do not want to think about categories, but still want better-than-average returns. The card figures out your top categories based on where you spent the most.

The downside is that you cannot always “force” it to prioritize groceries and gas if other categories take over. For example, a big travel purchase can shift your top category in that month. If your spending is consistent, it can still perform well for groceries and gas most months. It works best when combined with a flat-rate card for purchases that do not earn well.

| Detail | Summary |

| Rewards model | 3% top category, 2% second, 1% everything else |

| Groceries and gas | Both can be eligible categories |

| Best for | People whose spending changes month to month |

| Watch for | Large one-time purchases can change your top categories |

15) Citi Double Cash

This is the “simple wins” card. It earns 2% cash back on purchases in a straightforward way, and there are no categories to track. It is one of the easiest ways to make sure you always earn decent rewards even when bonus categories fail. It is especially useful for overflow. If you hit a grocery cap on another card, this becomes your next best option. If a gas purchase codes oddly, this can protect you from earning only 1% elsewhere.

It is also a strong choice for people who do not want to juggle multiple cards. While it will not beat a 5% grocery card, it avoids all the fine-print headaches. The main detail is that you earn part of the reward when you pay your bill. So the best habit is to pay on time and in full.

| Detail | Summary |

| Flat rate | 2% total cash back |

| Structure | 1% when you buy, 1% as you pay |

| Best for | Backup card, overflow spending, simple rewards |

| Watch for | You need to pay to earn the full 2% |

How to Maximize Cash Back on Groceries and Gas?

If you want the biggest reward with the least effort, build a simple system. Most people do best with two cards. One card handles groceries at a high rate. The other handles gas at a high rate. Then you add a flat-rate backup card for anything that falls outside bonus rules. The simplest two-card plan is this. Use a strong grocery card for supermarket trips. Use a gas-focused card for fuel and charging. If either card has a cap, switch overflow spending to your 2% backup card.

If you enjoy optimizing, add a rotating-category card. When a quarter includes groceries or gas, use the rotating card up to the cap. Then go back to your normal grocery or gas card. This is a smart “seasonal boost” strategy. Also think about where you buy groceries. If most of your grocery spending is at big-box retailers, a retailer-focused card can beat a supermarket card. The best setup is the one that fits your real receipts.

| Setup | Who It Fits | Why It Works |

| Grocery card + 2% backup | Most households | Strong grocery rewards without stress |

| Gas card + grocery card | Commuters and families | Covers both essentials at high rates |

| Rotating card + 2% backup | Organized maximizers | Adds a 5% boost when categories match |

| Warehouse fuel card + supermarket card | Costco or Sam’s shoppers | Maximizes member fuel perks and grocery rewards |

A Clean 2-Card Plan

Pick one strong grocery card and one strong gas card. Use each in its lane. Add a 2% card for overflow once you hit caps. This plan is easy to follow and works even if you forget details.

How to Handle Caps Without Losing Rewards?

Track caps loosely, not perfectly. If a card caps at a yearly number, check your spending every few months. If it caps quarterly, check near the end of each quarter. When you are close, switch to your backup card and keep earning.

A Simple Example That Shows the Value

If you spend heavily at supermarkets, moving from a 1% card to a 3% or 5% grocery card can add up fast over a year. If you also spend a lot on fuel, a higher gas rate can add another meaningful chunk. The result is not magic, but it is steady, repeatable savings.

Common Mistakes That Reduce Your Rewards

A lot of people choose a great card and still earn less than expected. The reason is usually category rules. “Grocery stores” may exclude warehouse clubs, superstores, and some delivery services. “Gas stations” may not always include convenience store purchases inside the station. Another common issue is missing activation on rotating-category cards. These cards can be excellent, but only if you activate the quarter and stay under the cap. If you forget, you fall back to a lower base rate.

Caps are another hidden leak. A card might advertise a high rate, but once you pass the limit, the return drops. If you do not have a backup card, you keep spending at a weak rate without noticing. Finally, rewards only matter if you avoid interest. Paying interest can wipe out the value of cash back quickly. The strongest strategy is simple: use rewards cards for purchases you can pay off.

| Mistake | What Happens | Better Move |

| Shopping at excluded stores | You earn the lower base rate | Match the card to your main store type |

| Forgetting rotating activation | You miss the 5% quarter | Set a calendar reminder for activation |

| Blowing past caps | Rewards drop without warning | Switch to a 2% backup when near the cap |

| Paying interest | Interest can exceed rewards | Pay in full to keep rewards meaningful |

Grocery Category Traps

Warehouse clubs and superstores can break supermarket bonuses. If your main “grocery store” is a club or supercenter, choose a card that rewards that merchant type or use a flexible category card.

Gas Category Traps

Paying at the pump often codes cleanly as fuel. In-store purchases can sometimes code differently. If you want to be safe, use your gas card at the pump and use another card inside.

Online Grocery and Delivery Confusion

Online grocery orders may code differently depending on the platform. If you rely on delivery, test a small order and check your statement. If it does not earn the bonus, switch to a card that rewards online retail or flexible categories.

Final Thoughts

The best credit cards for gas and groceries are the ones that match your habits and keep you earning without friction. A high grocery rate is only helpful if your store codes as a supermarket. A high gas rate is only helpful if your purchases code correctly and you do not blow past caps without a backup plan.

If you want a clear next step, start simple. Pick one grocery-and-gas card that fits your routine. Then add a flat-rate 2% card as your safety net. That one move can protect you from caps, odd category coding, and missed rotating quarters.