The days of operating in a regulatory gray area down under are officially over. As we step deeper into the year, Australia crypto regulation has evolved into one of the most comprehensive, heavily structured, and closely monitored financial frameworks in the world. For years, everyday investors and innovative blockchain startups had to blindly navigate rules built for traditional finance. They tried to force decentralized tech into decades-old legal boxes, which often led to confusion, accidental compliance breaches, and a hesitant traditional banking sector.

Now, the Australian government, in lockstep with major regulators like the Australian Securities and Investments Commission (ASIC) and the Australian Transaction Reports and Analysis Centre (AUSTRAC), has finally laid down the law. They are rolling out highly targeted legislation designed to protect consumers from the next massive exchange collapse while ideally keeping the door open for genuine tech innovation. Whether you hold a diverse portfolio of altcoins, run a local digital currency exchange, or just watch the market from the sidelines, you need to understand how these massive changes impact your money. Dive into these fifteen eye-opening facts about the current state of Australia crypto regulation that you simply cannot ignore.

1: The Landmark Digital Assets Framework Bill

The most seismic shift we have seen recently is the introduction of the Corporations Amendment (Digital Assets Framework) Bill. Instead of trying to reinvent the wheel and build an entirely new legal universe just for cryptocurrency, Australian lawmakers made a highly calculated, practical move. They decided to amend the existing Corporations Act 2001 and the ASIC Act 2001. This approach forces any company holding or managing digital assets for Australian consumers to meet the exact same rigorous standards as traditional banks, stockbrokers, and superannuation funds. It effectively erases the tired excuse that “crypto is different,” bringing centralized digital asset platforms strictly under the traditional financial services umbrella.

Furthermore, this legislative strategy speeds up the regulatory process significantly. Writing completely new laws from scratch takes years of parliamentary debate and endless revisions. By simply slotting digital assets into existing corporate law, the government instantly gives regulators the authority they need to start policing the market today. It creates a massive barrier to entry for fly-by-night operators who previously set up shop with nothing more than a basic website and a server. If you want to hold other people’s money in Australia, you now have to prove you run a legitimate, well-capitalized business.

Why Amending Existing Laws Makes Sense?

This legislation is the undisputed cornerstone of the new regulatory landscape. By amending existing corporate laws, the government instantly gives ASIC the teeth it needs to enforce compliance, issue heavy fines, and mandate basic consumer protections without having to test entirely new legal theories in court.

| Key Aspect | Details | Impact on the Market |

| Legislation Name | Digital Assets Framework Bill | Sets the primary legal foundation |

| Core Strategy | Amending existing financial laws | Speeds up the regulatory rollout |

| Primary Goal | Apply traditional financial standards | Weeds out undercapitalized startups |

| Regulator Empowered | ASIC | Gains immediate enforcement authority |

2: Introducing DAPs and TCPs

Say hello to the newest acronyms in the financial sector: DAPs and TCPs. Under the updated legal framework, the government has carved out two highly specific categories of regulated financial products to eliminate any lingering confusion about who needs to comply. Digital Asset Platforms (DAPs) cover the heavy hitters. This label applies to your standard cryptocurrency exchanges, digital brokers, and any centralized entity holding digital tokens directly on behalf of everyday users. If a company holds the private keys to your Bitcoin, they are a DAP.

Tokenised Custody Platforms (TCPs), on the other hand, deal with a slightly different beast. These platforms handle the increasingly popular practice of tokenizing real-world assets. Think about companies that issue tokens representing fractions of commercial real estate, physical gold bars, or traditional equities. Because these tokens represent ownership of a tangible, non-crypto asset, they require a slightly different regulatory touch. By clearly defining these two platform types, regulators have drawn a hard line in the sand, ending the debate over which specific compliance rules apply to different business models.

Categorizing the Crypto Ecosystem

If your business model involves taking custody of someone else’s digital assets or tokenizing physical assets, you fall into one of these two buckets. There is no more hiding behind vague technological jargon; you must prepare for stringent licensing requirements immediately.

| Platform Type | Acronym | Primary Function | Real-World Example |

| Digital Asset Platform | DAP | Holds crypto assets for retail users | Centralized crypto exchanges |

| Tokenised Custody Platform | TCP | Tokenizes real-world, physical assets | Platforms fractionalizing real estate |

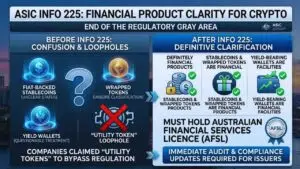

3: ASIC INFO 225 and Financial Product Clarity

For years, the loudest debate in the crypto community was whether a specific token should be legally classified as a financial product. ASIC dropped a massive update to their Information Sheet 225 (INFO 225) to finally put this argument to rest. Following intense consultations with industry leaders, ASIC made it undeniably clear: yes, many widely traded digital assets are definitively financial products under Australian law. This includes popular fiat-backed stablecoins, wrapped tokens that represent assets on other blockchains, and specific digital wallets that offer yield or staking rewards.

This sweeping clarification fundamentally changes how projects launch and market themselves in Australia. Previously, many token issuers claimed they were simply offering “utility tokens” to bypass strict financial regulations. ASIC has effectively closed that loophole. If your token acts like a security, a derivative, or a managed investment scheme, ASIC will treat it as one, regardless of what you call it in your whitepaper. This means the companies issuing or distributing these newly classified assets are legally obligated to hold an Australian Financial Services Licence (AFSL).

The End of the Regulatory Gray Area

This updated guidance officially ends the era of speculation. It forces platforms to audit their token offerings immediately and delist anything that might trigger severe licensing requirements they are not prepared to meet.

| Clarification Area | ASIC’s Stance (INFO 225) | Impact on Local Businesses |

| Stablecoins & Wrapped Tokens | Classified as financial products | Must operate under an AFSL |

| Yield-Bearing Wallets | Treated as financial facilities | Subject to strict regulatory oversight |

| “Utility Token” Loophole | Effectively eliminated | Forces immediate compliance updates |

4: The June 2026 No-Action Grace Period

Regulators know you can’t flip the rulebook overnight without accidentally destroying the local market. Because the updated INFO 225 suddenly classified so many existing tokens as financial products, ASIC realized that perfectly legitimate, well-meaning businesses would need a lifeline. To prevent mass panic and operational shutdowns, ASIC granted a sector-wide “no-action” position running until the end of June 2026. This grace period allows companies to keep their doors open while they scramble to get their licenses in order.

However, do not mistake this grace period for a free pass to behave recklessly. ASIC explicitly stated that this is a conditional lifeline. Companies must prove they are making a genuine, active effort to transition to the new framework and apply for their licenses. If a platform drags its feet or tries to exploit the grace period to push shady tokens, ASIC will strike. They retain the full right to aggressively prosecute any platform engaging in blatant fraud, market manipulation, or actions causing widespread consumer harm during this transition window.

A Conditional Lifeline for Exchanges

This window is strictly about allowing administrative catch-up. It recognizes the massive paperwork bottleneck that occurs when an entire industry suddenly needs highly complex financial licenses all at once.

| Grace Period Detail | Specifics | Practical Meaning |

| End Date | June 30, 2026 | Hard deadline for compliance |

| Primary Purpose | Allow time for AFSL applications | Prevents an immediate market crash |

| Core Condition | Businesses must transition actively | No lazy delays tolerated |

| The Exceptions | ASIC will still prosecute fraud | Bad actors are not protected |

5: AUSTRAC Registration Remains the Baseline

While ASIC grabs most of the headlines with its new corporate licensing rules, AUSTRAC remains the absolute foundational gatekeeper of the Australian crypto industry. Even with the shiny new laws, any business functioning as a digital currency exchange must first register with AUSTRAC before they even think about onboarding a single customer. Operating without this baseline registration isn’t just a minor administrative misstep; it’s a serious criminal offense that can result in prison time for the founders.

AUSTRAC’s primary mission is hunting down dirty money. Therefore, registered exchanges must enforce rigorous Know Your Customer (KYC) protocols, meaning mandatory ID checks and facial recognition for every user. They must also actively monitor trading patterns for suspicious activity and report large or unusual transactions directly to the agency. No matter what new licenses ASIC introduces in the future, this baseline registration and the strict reporting obligations that come with it are permanently baked into the system.

The Unmovable Compliance Pillar

Before you can worry about whether a token is a financial product, you have to prove you know exactly who is buying it. AUSTRAC ensures the crypto market doesn’t become a playground for organized crime.

| AUSTRAC Requirement | Description | Consequence of Failure |

| Mandatory Registration | Must register as a Digital Currency Exchange | Criminal prosecution and jail time |

| KYC Implementation | Must verify the identity of all customers | Massive fines and operational bans |

| Activity Reporting | Flag and report unusual transaction behavior | Severe financial penalties |

6: Sweeping AML/CTF Reforms and the Travel Rule

The Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) landscape in Australia is expanding at breakneck speed. Sweeping reforms are currently tearing through the industry, vastly expanding the legal definition of “designated services” to catch a wider net of crypto startups. However, the most controversial and impactful change is the strict enforcement of the crypto “Travel Rule.” This is a massive operational headache for local exchanges, but an absolute necessity for international compliance.

The Travel Rule, pushed globally by the Financial Action Task Force (FATF), forces exchanges to collect, verify, and seamlessly share the personal data of both the sender and the recipient for virtual asset transfers. If you send Bitcoin from an Australian exchange to a platform in the UK, your local exchange must securely transmit your identity data alongside the blockchain transaction. This effectively kills the concept of anonymous exchange-to-exchange transfers and requires serious technological upgrades for platforms to share data without violating privacy laws.

Aligning with Global FATF Standards

Implementing the Travel Rule brings Australia crypto regulation directly in line with traditional international wire transfers, ensuring the country isn’t blacklisted by global financial watchdogs.

| Reform Element | Practical Impact | Industry Challenge |

| Expanded Designated Services | Pulls more startups into AML compliance | Higher barrier to entry for founders |

| The Travel Rule | Requires sharing user data between exchanges | Needs massive backend tech upgrades |

| Data Collection | Eliminates anonymous institutional transfers | Friction for high-volume traders |

7: The ATO Unwavering Stance on Crypto as Property

If you were hoping the taxman would eventually treat your Bitcoin like a foreign currency to save you some money, think again. The Australian Taxation Office (ATO) has maintained a brutally consistent and highly lucrative stance: cryptocurrency is property, plain and simple. Because it is legally treated as an asset rather than money, it falls squarely under Capital Gains Tax (CGT) rules. This creates a highly complex tax environment for anyone doing more than just buying and holding.

Every single time you dispose of crypto, you trigger a taxable event. This includes selling crypto for Australian dollars, trading your Ethereum directly for a shiny new altcoin, or even using a crypto debit card to buy a cup of coffee. You are legally required to calculate your profit or loss based on the exact market value of the asset at the specific second the transaction occurred. For active retail traders or DeFi farmers executing hundreds of trades a week, keeping meticulous, line-by-line records is not just a good idea—it is a strict legal necessity to avoid a painful audit.

The Heavy Burden of Record-Keeping

The ATO doesn’t care if a decentralized exchange didn’t give you a receipt. The burden of tracking cost basis and market value falls entirely on the taxpayer.

| Transaction Type | ATO Legal Classification | Tax Implication |

| Selling Crypto for Fiat | Disposal of Property | Triggers Capital Gains Tax (CGT) |

| Swapping Crypto to Crypto | Disposal of Property | Triggers Capital Gains Tax (CGT) |

| Buying Goods with Crypto | Disposal of Property | Triggers Capital Gains Tax (CGT) |

8: The Arrival of the Crypto Asset Reporting Framework

If you think you can hide your decentralized trades from the government by using offshore exchanges, the incoming Crypto Asset Reporting Framework (CARF) is about to give you a harsh reality check. Developed by the Organization for Economic Cooperation and Development (OECD) and fully embraced by Australia, CARF creates a standardized, automated system for global tax authorities to share crypto transaction data. The days of siloed, national tax databases are coming to an end.

By 2027, every regulated Australian exchange will be forced to automatically report highly detailed user transaction histories directly to the ATO. The ATO will then seamlessly share that data with international tax bodies, and receive data on Australian citizens trading on foreign platforms in return. This framework permanently removes the veil of pseudo-anonymity that early crypto adopters heavily relied on. Your cross-border trading activities, gains, and hidden losses will soon be fully visible to the government, making international tax evasion practically impossible.

The End of Borderless Tax Evasion

CARF represents a monumental shift in global tax enforcement. It treats crypto data exactly like traditional banking data shared under the Common Reporting Standard (CRS).

| CARF Feature | Detail | What it Means for Users |

| Originator | OECD | It’s a globally recognized standard |

| Rollout Timeline | Full compliance expected by 2027 | Time is running out to fix past tax mistakes |

| Core Mechanism | Automatic data sharing | No more manual audits to find hidden funds |

| Global Reach | ATO shares data internationally | Offshore accounts offer zero protection |

9: Stablecoins Fall Under Payments Modernization

Stablecoins have quietly become the fundamental plumbing of the decentralized finance world, moving billions of dollars daily. The Australian government has clearly noticed this trend and, rather than banning them out of fear, they are actively modernizing the traditional payments framework to bring stablecoin issuers into the fold. Through the Treasury Laws Amendment (Payments System Modernisation) Bill, payment stablecoins are being formally grouped together with other modern financial tools.

The government is essentially treating major, fiat-backed stablecoins the same way they treat digital wallets like Apple Pay or Buy-Now-Pay-Later (BNPL) services. By regulating stablecoins under standard, boring payment laws, the government is officially acknowledging that these digital assets are legitimate tools for everyday commercial transactions, not just highly speculative casino chips. It paves the way for mainstream merchants to start accepting stablecoin payments without fear of sudden regulatory crackdowns.

Legitimizing Crypto for Everyday Use

This specific move is actually incredibly bullish for the local industry. It signals that Australia sees blockchain as a viable backend for the future of commercial payments.

| Regulatory Action | Impact on Stablecoins | Long-term Outlook |

| Payments Modernisation | Integrates them into payment frameworks | Mainstream merchant adoption becomes easier |

| Classification | Treated like digital wallets and BNPL | Removes the “speculative asset” stigma |

| Market Perception | Legitimizes stablecoins for daily use | Encourages fintech companies to build on crypto |

10: Tackling the Crypto De-Banking Crisis

Ask any crypto founder in Australia about their biggest headache over the last five years, and they will almost certainly say the same thing: de-banking. Traditional “Big Four” banks have routinely refused to open corporate accounts for crypto businesses. Worse, they frequently shut down existing accounts with zero notice, citing opaque and undefined “risk” concerns. This forced legitimate startups to use expensive, second-tier payment processors just to pay their employees.

The new regulatory framework was actively designed to solve this massive operational bottleneck. By forcing crypto platforms to acquire a stringent AFSL and operate under intense ASIC scrutiny, the government is handing these businesses a shiny badge of absolute legitimacy. The core strategy here is straightforward: once a digital asset platform achieves rigorous, bank-grade compliance standards, the major Australian banks lose their easy excuse to deny them basic corporate banking facilities. It forces the traditional finance sector to finally play fair.

Forcing the Banks’ Hands

Regulators essentially told the banks that if a crypto company passes ASIC’s brutal licensing checks, they are safe to do business with, removing the banks’ internal risk-aversion excuses.

| The Industry Problem | The Regulatory Solution | Expected Outcome |

| Banks denying service | Mandating AFSLs and ASIC oversight | Legitimizes crypto businesses on paper |

| Abrupt account closures | Establishing clear, legal operational standards | Banks can safely onboard crypto clients |

11: Meaningful Exemptions for Smaller Players

Not every blockchain project is a multi-billion-dollar juggernaut. Lawmakers realized that forcing a tiny, two-person startup to pay millions in compliance costs and legal fees would instantly kill local innovation and drive talent overseas. Thankfully, the Digital Assets Framework includes highly specific, meaningful exemptions designed to protect the grassroots startup ecosystem from being crushed by red tape.

For example, there is a low-value exemption explicitly designed for smaller platforms testing new ideas. If a platform holds less than $5,000 per individual customer and processes under $10 million in total annual transactions, they can bypass the most crushing and expensive AFSL licensing requirements. Additionally, there is an “incidental activity” exemption for traditional businesses where handling crypto is only a minor, secondary function. This ensures that a local café experimenting with accepting Bitcoin isn’t suddenly regulated like a Wall Street investment bank.

Protecting the Startup Ecosystem

These exemptions show that regulators actually listened to industry feedback. They want to catch the whales without accidentally squashing the minnows.

| Exemption Type | Qualification Criteria | Primary Benefit to Business |

| Low-Value Platform | < $5K per user AND < $10M total volume | Bypasses the heaviest AFSL requirements |

| Incidental Activity | Crypto is a minor, secondary function | Prevents over-regulation of regular retail |

12: Regulating the Custodian, Not the Code

One of the smartest and most practical decisions Australian lawmakers made was choosing their targets wisely. The new framework relentlessly targets the centralized companies—the custodians, the exchanges, the fiat on-ramps—that hold digital assets for everyday users. They explicitly avoided the massive mistake of trying to regulate the underlying decentralized blockchain code itself, recognizing that regulating open-source math is practically impossible.

This approach fundamentally respects the original, decentralized ethos of cryptocurrency. If you choose to hold your own private keys in a self-custody hardware wallet and interact directly with smart contracts on a decentralized exchange, the government stays out of your way. They are not trying to regulate your direct, peer-to-peer interactions with the blockchain. The heavy hand of the law only steps in when a corporate middleman takes control of your money, ensuring consumer protection where the actual risk of embezzlement or mismanagement lies.

Self-Custody Remains Free

By focusing on the centralized bottlenecks, regulators protect average consumers without strangling the brilliant developers building the decentralized future.

| Regulatory Target | Government Stance | Real-world Implication |

| Centralized Exchanges | Heavily regulated, requires strict auditing | High barrier to entry, highly secure for users |

| Underlying Code | Left unregulated to foster innovation | Devs can build freely without licensing |

| Self-Custody Wallets | Direct user interaction remains unrestricted | “Not your keys, not your coins” remains true |

13: The Six-Month Countdown for AFSL Authorization

The clock is ticking very loudly for currently unregistered platforms. Once the Digital Assets Framework is officially fully legislated, any affected firm operating without an AFSL will face a brutal, strict six-month countdown to get authorized. Applying for an AFSL is famously difficult and incredibly time-consuming. It requires exhaustive background checks on company directors, proof of immense financial stability, and demonstrating total operational competence.

If a company fails to secure its license before that six-month buzzer sounds, the consequences are fatal. They will have to pack up their Australian operations entirely, offboard all their local users, or face crippling civil penalties and asset freezes. This short window is intentionally designed to act as a brutal filtration process. Only well-capitalized, highly professional platforms will survive this transition, which will rapidly consolidate the fragmented Australian market into a handful of trusted, heavily audited providers.

A Brutal Filtration Process

Expect to see a wave of smaller exchanges either shutting down or merging with larger competitors as this six-month deadline approaches.

| Compliance Step | Details | Impact on the Sector |

| Deadline Window | Six months from the passing of the Framework | Triggers a massive rush for compliance lawyers |

| Requirements | Prove financial stability and competence | Filters out underfunded, amateur projects |

| Penalty for Failure | Forced operational shutdown | Rapid market consolidation |

14: Enhanced Consumer Protections and Market Integrity

Ultimately, the driving force behind all this bureaucratic heavy lifting is consumer protection. Retail investors have been burned too many times by shady offshore exchanges collapsing overnight and taking billions in customer funds with them. Under the new rules, licensed DAPs are legally bound to act efficiently, honestly, and fairly. This isn’t just a suggestion; it is a strict legal mandate enforceable by ASIC.

Platforms must provide crystal-clear disclosure documents detailing exactly how and where user assets are stored, proving they aren’t gambling with customer deposits. Furthermore, they must implement mandatory external dispute resolution mechanisms. This gives angry or scammed customers an actual legal avenue to pursue, usually through the Australian Financial Complaints Authority (AFCA), if their funds go missing. Minimum capital requirements also guarantee that platforms have enough cash reserves to survive sudden market crashes without going bankrupt.

Building a Bulletproof Ecosystem

These protections are designed to prevent the next FTX-style disaster from wiping out the life savings of everyday Australians.

| Consumer Protection Measure | What It Means for You |

| Clear Disclosure Documents | You know exactly how your crypto is stored and managed |

| Dispute Resolution via AFCA | You have a formal, legal way to seek financial restitution |

| Minimum Capital Requirements | Platforms must hold cash reserves to prevent insolvency |

15: Aiming for Global Leadership in Digital Assets

Australia isn’t just grudgingly accepting crypto because they have to; the government actively wants to dominate the sector in the Asia-Pacific region. By setting up these clear, tough, but highly fair rules, the government is signaling to the world that Australia is a safe, stable haven for institutional digital asset capital. Initiatives like the Reserve Bank of Australia’s ongoing research into wholesale tokenized markets and Central Bank Digital Currencies (CBDCs) show a genuine commitment from the very top down.

The message to global talent is unmistakable: Australia is wide open for blockchain innovation, provided you are willing to play by adult financial rules. This clarity is a massive competitive advantage. It actively attracts serious Web3 developers and institutional investors who are fleeing the chaotic, “regulation-by-enforcement” environments currently plaguing countries like the United States. Australia is positioning itself to be the adult in the room for the next crypto bull run.

Open for Compliant Business

By offering a clear rulebook, Australia becomes highly attractive to massive international firms that require legal certainty before investing billions of dollars.

| Strategic Goal | Actions Taken | Desired Outcome |

| Global Leadership | Implementing clear frameworks early | Attract global institutional capital to Australia |

| Institutional Trust | RBA research into tokenization | Legitimize the market for major traditional funds |

| Attracting Talent | Offering absolute regulatory certainty | Make Australia a premier hub for Web3 developers |

Final Thoughts

We have officially crossed the threshold from regulatory chaos to structured legitimacy. The comprehensive Australia crypto regulation rollout—driven by the pragmatic Digital Assets Framework, ASIC’s relentless licensing push, and AUSTRAC’s tightened travel rules—means the local industry must grow up immediately. Yes, the compliance burden is heavy, and we will undoubtedly see several smaller exchanges fold under the intense pressure of acquiring an AFSL. However, these rules establish a critically needed, bank-grade standard for digital asset custody.

By flushing out the bad actors and enforcing strict consumer protections, Australia is actively building a much safer sandbox for retail investors. More importantly, it is setting the stage to become a trusted global powerhouse in the tokenized economy. If you are touching crypto in Australia, ignorance of the law is no longer an option—get compliant, or get left entirely behind.