The US China Trade War 2026 outlook has opened not with a bang, but with a tense, calculated silence. In November 2025, a handshake between President Trump and Premier Li momentarily halted the spiraling escalation of duties that had defined the previous year.

This “November Truce” was hailed by global markets as a return to stability, but for those navigating the global supply chain, the reality on the ground is far more complex. While the headlines celebrate a pause in rate hikes, the underlying architecture of the trade conflict remains dangerously intact, leaving businesses to operate in a precarious geopolitical fog.

Key Takeaways

- Status- “Armed Stability”: The “November 2025 Truce” has paused daily escalation, stabilizing the effective US tariff rate on Chinese goods at ~32% (down from a peak of 42%). However, this is a ceasefire, not a peace treaty; structural tariffs on EVs (100%) and Batteries (50%) remain locked in place.

- The “Sword of Damocles” (Legal Risk): The single biggest variable in Q1 2026 is the Supreme Court ruling on the International Emergency Economic Powers Act (IEEPA). With 61% of current tariffs relying on this authority, a ruling against the administration could void billions in duties overnight.

- The “Great Rerouting” vs. Decoupling: Global trade data confirms that supply chains are not breaking, but bending. Chinese exporters are bypassing tariffs via “transshipment” hubs in Vietnam and Mexico. In response, the USTR has launched aggressive “Country of Origin” investigations, targeting these third-party partners.

- China’s “Global South” Pivot: China has successfully offset the loss of the US market by pivoting to the developing world. In 2025, China recorded a record $1.19 trillion trade surplus, driven by double-digit export growth to ASEAN, Africa, and Latin America.

- The “Tech Thaw” Signal: A quiet regulatory shift by the Bureau of Industry and Security (BIS) on Jan 15, 2026, has moved AI chip exports from “presumption of denial” to “case-by-case,” signaling that the US is refining its tech blockade to preserve market share for American semiconductor firms.

The Illusion of Peace: Armed Stability

We are currently living in a state of “Armed Stability.” The daily barrage of new tariff announcements has ceased, but it has been replaced by a high-stakes legal battle and a covert restructuring of global trade routes. The effective tariff rate on Chinese imports sits at a stubborn 32%, and a “Sword of Damocles” hangs over the entire system in the form of the upcoming Supreme Court ruling on the International Emergency Economic Powers Act (IEEPA).

This ruling, expected in early 2026, has the potential to either cement the tariff regime for decades or dismantle it overnight, triggering a chaotic flood of refunds and policy scrambles. Far from being over, the trade war has simply mutated. It is no longer just about how much you pay at the border; it is about where your goods are really from, and whether the Executive Branch has the constitutional authority to act as the economy’s gatekeeper.

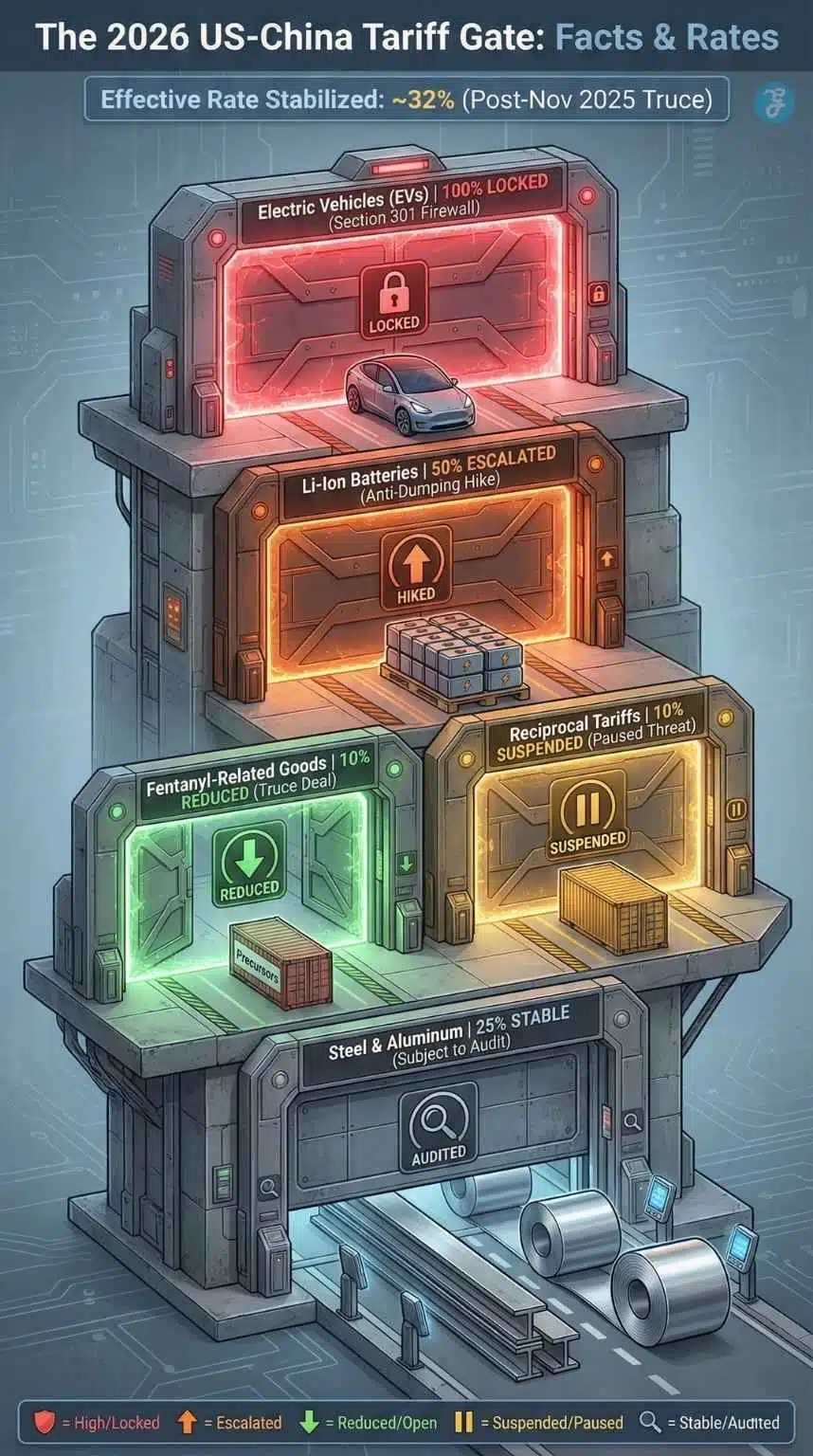

The New Tariff Architecture: Facts & Rates

To understand the 2026 landscape, one must look past the political rhetoric and examine the hard numbers that now govern trans-Pacific trade. The current period is defined by a specific set of compromises and rigidities that leave businesses in a precarious position.

The “Fentanyl Compromise”

The cornerstone of the current truce is the so-called “Fentanyl Compromise” reached in late 2025. In a rare moment of bilateral cooperation, Beijing agreed to strict controls on precursor chemicals used to manufacture fentanyl. In return, the United States offered a strategic concession:

- Tariff Reduction: Duties specifically linked to “Fentanyl sanctions” were slashed from 20% to 10%.

- Reciprocal Pause: The threat of an additional 24% “reciprocal tariff”, which would have mirrored China’s own duties on US goods, was suspended.

This quid pro quo successfully lowered the effective tariff rate from its April 2025 peak of ~42% to roughly 32% today. However, this relief is conditional. The agreement includes a “snap-back” clause, allowing the US to immediately reinstate the higher rates if China’s enforcement on chemical precursors is found lacking by the Department of Homeland Security.

The Tariff Scorecard [Jan 2026]

| Product Category | Previous Rate (2025 Peak) | Current Rate (Jan 2026) | Status / Note |

| Electric Vehicles (EVs) | 100% | 100% | Locked: Section 301 “Firewall” remains active. |

| EV Batteries (Li-Ion) | 25% | 50% | Escalated: Hiked to prevent component dumping. |

| Fentanyl-Related Goods | 20% | 10% | Reduced: Part of the “Nov 2025 Truce” deal. |

| Reciprocal Tariffs | 34% (Threatened) | 10% (Suspended) | Paused: The 24% hike was suspended pending compliance. |

| Steel & Aluminum | 25% | 25% | Stable: Subject to new “melt & pour” audits in Mexico. |

The Section 301 Reality

While the “Fentanyl Tariffs” offered a glimmer of hope, the structural “Section 301” tariffs remain a formidable wall around key US industries. The Biden-era hikes, which were aggressively expanded in 2025, are locked in place for strategic sectors:

- Electric Vehicles (EVs): 100% tariff.

- Lithium-Ion Batteries: 50% tariff (increased from 7.5%).

- Steel & Aluminum: 25% tariff.

These rates are designed to be prohibitive. They are not meant to raise revenue but to act as a dam, preventing Chinese heavy industry and green tech from flooding the US market. As of January 2026, there is zero indication that these specific duties will be relaxed; in fact, the USTR has signaled they are “non-negotiable” components of national security.

The “Plan B” [Section 122]

Perhaps the most critical piece of intelligence for 2026 is the Administration’s contingency plan. White House advisors are acutely aware that the Supreme Court could strike down the use of IEEPA. If that happens, the administration has already drafted executive orders to invoke Section 122 of the Trade Act of 1974.

- The Mechanism: This little-used provision allows the President to impose temporary import surcharges to deal with “balance of payments” deficits.

- The Threat: If IEEPA fails, the White House is prepared to slap a blanket 15% tariff on all imports for 150 days using Section 122. This would buy time for the USTR to launch new investigations and rebuild the tariff wall under different legal authorities.

Key Stat: As of Jan 2026, the IMF estimates the global effective US tariff rate has stabilized at 18.5% (averaged across all partners), down from 25% in early 2025, largely due to the truce.

The Legal War: IEEPA at the Supreme Court

The most significant event on the 2026 trade calendar is not a diplomatic summit, but a court case: United States v. Importers Association. This landmark case challenges the constitutional bedrock of the trade war.

The Constitutional Question

At the heart of the case is the International Emergency Economic Powers Act (IEEPA). Historically used for sanctions against rogue states like Iran or North Korea, the Trump administration repurposed IEEPA to impose broad tariffs on China, arguing that the trade deficit itself constituted a “national emergency.” The plaintiffs, a coalition of major US importers, argue that this is a gross overreach of executive power that bypasses Congress’s constitutional authority to set taxes and duties.

The Stakes for Business

The financial implications of this ruling are staggering.

- 61% of Tariffs at Risk: Legal analysts estimate that roughly 61% of the current tariff volume relies on IEEPA authority. This amounts to approximately $180 billion in annualized duties.

- The Refund Chaos: If the Court rules against the administration, those tariffs could be declared void ab initio (from the beginning). This would theoretically entitle importers to billions in refunds. However, the government would likely fight tooth and nail to limit retroactive payouts, leading to years of litigation.

The uncertainty is palpable. Major US corporations are currently hoarding cash and delaying capital expenditures (CapEx), paralyzed by the possibility that the cost of doing business could drop by 30% or spike due to a Section 122 retaliation within a single afternoon in February.

The “Great Rerouting”: The Transshipment Game

While lawyers battle in Washington, logistics managers are fighting a different war in Southeast Asia. The narrative of “decoupling” is largely a myth; the US and China are still deeply economically entwined, but the connection has become indirect, opaque, and more expensive.

The Loophole: Minimal Transformation

Chinese manufacturers have mastered the art of “transshipment.” Instead of shipping finished goods directly to Long Beach or Savannah, they ship components to third-party countries for “minimal transformation”, just enough assembly to legally change the “Country of Origin” label.

Vietnam: The “Assembly Hub”

Vietnam has emerged as the primary beneficiary and target of this practice.

- The Data Anomaly: In 2025, Vietnam’s exports to the US surged by nearly 40%. However, this boom was perfectly mirrored by a massive spike in Vietnam’s imports of intermediate goods from China.

- The Crackdown: The USTR is not blind to this. In January 2026, the US launched a series of aggressive “Country of Origin” investigations targeting Vietnamese exports of solar panels and consumer electronics. The message is clear: if you are just a “pass-through” for Beijing, you will face the same tariffs as Beijing.

The Mexico Corridor

Closer to home, the US-Mexico-Canada Agreement (USMCA) is facing its sternest test. Chinese auto-parts manufacturers have aggressively set up shop in Northern Mexico, establishing maquiladoras to assemble Chinese components into “Mexican” goods that enter the US duty-free.

- Political Friction: This has caused significant friction between Washington and Mexico City. The US has demanded stricter “Steel and Aluminum” monitoring, effectively asking Mexico to act as a deputy customs enforcer for US trade policy. The threat of reimposing tariffs on Mexican goods remains a potent lever in these negotiations.

The Takeaway: Supply chains are not getting shorter; they are getting longer. The “Great Rerouting” adds layers of cost and complexity, creating a “Hidden China Risk” for companies that believe they have diversified by simply moving a contract to Hanoi or Monterrey.

China’s “Two-Speed” Economy

The trade war has fundamentally altered China’s economic DNA, creating a sharp divergence between its external muscle and its internal health.

The Export Engine Roars

Contrary to predictions of collapse, China’s export machine is running hotter than ever. In 2025, China recorded a staggering $1.19 trillion trade surplus, the largest in history.

- The Shift: The destination of these goods has shifted dramatically. With the US market partially walled off, China has aggressively pivoted to the “Global South.” Exports to ASEAN (+14%), Africa (+26%), and Latin America surged in 2025.

- Strategic Dominance: China is effectively building a “Non-Aligned” trade bloc, cementing its role as the factory for the developing world while the West tries to isolate it.

Domestic Stagnation

However, this export success masks deep domestic rot. The property sector remains in a deflationary spiral, and consumer confidence is near historic lows. The Chinese economy is now running on one leg: it must export to survive. This makes the “November Truce” just as vital for Beijing as it is for Washington. Premier Li’s acceptance of the deal was likely driven by a desperate need to keep the external engine running while he attempts to fix the internal crisis.

Sector Spotlight: Winners & Losers

The erratic nature of the 2026 landscape has picked winners and losers with brutal efficiency.

Losers

- US Retailers (The Inventory Hangover): Fearing a total collapse of trade talks in late 2025, major US retailers engaged in massive “front-loading,” importing months’ worth of inventory in Q4. Now, they are sitting on bloated warehouses with slowing consumer demand, leading to deep discounting and margin compression in Q1 2026.

- Chinese Solar: The combination of Section 301 tariffs and the new investigations into Vietnamese transshipment has effectively locked Chinese solar out of the US market. This has forced them to dump excess capacity into Europe, crashing prices there and triggering new trade defense measures from the EU.

Winners

- Logistics & Warehousing: The “front-loading” panic was a bonanza for the logistics sector. Warehousing rates in Southern California and New Jersey remain at premium levels as companies store their “panic buys.”

- India & Indonesia: As companies look for genuine alternatives to China (not just transshipment hubs), India and Indonesia are seeing record Foreign Direct Investment (FDI). They offer the scale and labor force to actually replace Chinese production, rather than just repackage it.

The Hidden Fronts: Q1 2026 Strategic Intelligence

While the headline tariffs dominate the news cycle, the real tactical shifts of the trade war are happening in the quiet corners of regulatory policy and geopolitical friction. As of late January 2026, four critical developments have emerged that contradict the standard “decoupling” narrative and demand immediate attention from strategic planners.

1. The “Tech Thaw”: A Pivot in the Semiconductor War

On January 15, 2026, the Bureau of Industry and Security (BIS) quietly implemented a significant doctrinal shift regarding AI chip exports. Moving away from the blanket “presumption of denial” that characterized 2024-2025, the BIS has adopted a “case-by-case” review process for mid-tier processors (specifically those with a Total Processing Performance < 21,000).

- The Nuance: This is not a surrender; it is a surgical refinement. The US has realized that a total blockade was incentivizing China to develop its own domestic alternatives faster than anticipated. By allowing US companies to sell “commercial-grade” AI chips to Chinese firms, Washington aims to maintain market share and dependency for US tech giants like Nvidia and Intel, while still “choking” the high-performance chips required for military-grade AI training. This subtle regulatory pivot is a massive, under-reported “buy signal” for the US semi-cap equipment sector.

2. The “Western Hemisphere” Agriculture Pivot

A quiet revolution is occurring in the American heartland. While US agricultural exports to China have plummeted by approximately 55% year-over-year (Jan 2026 data), the American agricultural sector has not collapsed. Instead, it has successfully executed a “friend-shoring” pivot.

- The Shift: Exports of corn, soy, and pork to the Western Hemisphere (Mexico, Colombia, and Canada) have surged to record highs, effectively offsetting the losses from the Chinese market. This data point is critical because it challenges the long-held assumption that US farmers are hostages to Beijing’s goodwill. The 2026 reality is that the US food supply chain is decoupling from East Asia and integrating more deeply with the Americas, creating a more resilient, shorter, and politically aligned export market.

The Agriculture Pivot [Export Shift]

It visually proves the “Friend-shoring” argument.

| Export Destination | 2025 YoY Change | 2026 Trend | Strategic Shift |

| China | ▼ -55% | Stagnant | Decoupling: China shifting buys to Brazil/Argentina. |

| Mexico | ▲ +18% | #1 Market | Integration: Replaced China as the top US Ag buyer. |

| Colombia | ▲ +12% | Rising | New Market: Emerging buyer for US Corn/Pork. |

| Canada | ▲ +9% | Stable | Friend-shoring: Deepening North American food security. |

3. The “Critical Minerals” Tightrope: Price Floors vs. Tariffs

Perhaps the most sophisticated policy maneuver of 2026 occurred on January 14, when the White House issued a new proclamation regarding Section 232 investigations into critical minerals. The administration faced a dilemma: slapping high tariffs on Chinese lithium and cobalt would crush the US EV industry, which is still dependent on these inputs.

- The Solution: Instead of blunt tariffs, the USTR is negotiating “Price Floors” and Import Quotas. This mechanism sets a minimum price for imported minerals, preventing China from flooding the market with artificially cheap supply to kill Western mines, while still allowing US automakers to access the materials they need. This “managed trade” approach admits a hard truth: the US cannot yet survive without Chinese minerals, so it must manage the flow rather than stop it.

4. The Geopolitical Wildcard: The Greenland Dispute

In a volatile twist that complicates the “Western Alliance” narrative, a new friction point has opened up on the Atlantic front. The US administration has unexpectedly threatened 10-25% tariffs on Denmark and the wider EU stemming from a dispute over the “Greenland Purchase” proposal.

- The Implication: While seemingly unrelated to China, this dispute is a major distractor. It forces the EU to fight a trade war on two fronts, weakening the coordinated “Trans-Atlantic tech ban” against China that was gaining momentum in late 2025. For global investors, this is a reminder that the 2026 trade policy is not just about economics; it is increasingly weaponized for geopolitical real estate strategies, adding a layer of unpredictability that standard risk models fail to capture.

The Strategic Imperative: Agility is Survival

For business leaders and investors, 2026 is not a year to coast. The looming IEEPA Supreme Court ruling stands as a potential “Black Swan” event capable of rewriting trade rules overnight. Meanwhile, the USTR’s aggressive crackdown on transshipment dictates that supply chain audits can no longer stop at Tier 1 suppliers; knowing the true origin of raw materials is now non-negotiable.

In this environment, compliance transforms from a back-office function into a frontline competitive advantage. Success belongs to those who can navigate these gray zones and adapt to a world where trade is managed, monitored, and weaponized. In 2026, agility is not just an advantage; it is the only survival mechanism.

Final Words: A Temporary Ceasefire, Not Peace

The US China Trade War 2026 narrative is defined not by resolution, but by systemic complexity. The “November Truce” serves merely as a diplomatic bandage rather than a structural cure. While it has purchased valuable time for the global economy, it has failed to address the fundamental incompatibilities between Washington’s market-driven goals and Beijing’s state-led economic model. We are not witnessing the end of the conflict, but rather its evolution into a more sophisticated and legally fraught phase.