The “growth at all costs” era isn’t just over; it’s been replaced by a ruthless new reality. As we settle into 2026, the B2B SaaS landscape is undergoing a violent shakeout. Capital is expensive, AI is cannibalizing seat-based pricing, and the “Rule of 40” has morphed from a gold standard into a survival baseline.

Why does this significant shift matter right now? Because for the first time in a decade, software companies are dying not because they lack a product, but because they lack a viable business model in an AI-first economy.

The Hangover: How We Got Here

To understand the severity of the 2026 shakeout, we must look back at the economic whiplash of the last five years. The Zero Interest Rate Policy (ZIRP) era fueled a generation of “unicorn” startups valued on revenue multiples that defied gravity—often 50x or 100x ARR. When interest rates spiked in 2023 and stabilized in the 4-5% range through 2025, the cheap capital faucet turned off.

By late 2025, the market had bifurcated. On one side were the AI “Supernovas”—infrastructure giants like OpenAI and Anthropic—sucking up the remaining venture capital oxygen. On the other were thousands of “zombie” SaaS companies: decently growing businesses (20-30% YoY) with unsustainable burn rates and no path to further funding.

Now, in early 2026, the bill has come due. The “First Light” of the AI era has exposed a critical vulnerability: traditional SaaS economics (80%+ gross margins) are under siege by compute-heavy AI features that drag margins down to 50-60%. We are witnessing a fundamental rewriting of the software business model, moving from “renting software” to “hiring AI labor.”

Core Analysis: The Pillars of the B2B SaaS Shakeout

1. The Shift to “Efficient Intensity” (Rule of X)

The “Rule of 40” (Growth % + Profit Margin % = 40) was the guiding star of the last decade. In 2026, it is merely the entry fee. The top quartile of companies are now measured by the “Rule of X” or “Weighted Rule of 40,” which places a significantly higher multiplier on growth—but only if that growth is efficient.

Investors have stopped rewarding “empty calories”—growth fueled by unsustainable marketing spend. The market has realized that in a high-interest environment, cash today (Free Cash Flow) combined with sustainable growth is the only metric that matters.

The New Valuation Scorecard – Rule of 40 vs. Rule of X (2026 Benchmarks)

| Metric | Standard Rule of 40 | The New “Rule of X” | Why the Shift? |

| Formula | Growth % + Profit % | (Growth % × 2) + FCF Margin % | Investors value growth 2x more than margin, but only if burn is low. |

| Median Score | ~31% | ~50% | The bar has been raised; average companies are failing the new test. |

| Top Decile | 48%+ | 80%+ | Elite performers are breaking away from the pack. |

| Valuation Impact | 6x – 7x Revenue Multiple | 12x – 15x Revenue Multiple | Efficiency acts as a multiplier on valuation. |

2. The AI Pricing Crisis: Beyond the Seat

The most disruptive trend of 2026 is the collapse of the per-seat billing model. For two decades, Salesforce and Microsoft taught the world to pay per user. But if an AI agent replaces three human SDRs (Sales Development Representatives), a seat-based model cannibalizes the vendor’s own revenue.

Data Snapshot: According to early 2026 benchmarks, seat-based pricing dropped from 45% (2024) to 22% of the market share. Companies sticking to pure seat-based models are seeing 40% lower gross margins and 2.3x higher churn. The winners are pivoting to hybrid pricing—a lower platform fee plus a “work done” metric (e.g., per ticket resolved, per lead scored, or per workflow completed).

Pricing Model Evolution (2024 vs. 2026)

| Pricing Model | 2024 Market Share | 2026 Market Share | The 2026 Reality |

| Per-Seat (User) | 45% | 22% | Declining: AI reduces headcount; vendors lose revenue if they stick to this. |

| Usage-Based | 30% | 35% | Steady: Aligns cost with consumption (tokens/credits), but can be unpredictable. |

| Outcome/Hybrid | 15% | 41% | Dominant: Customers pay for results (e.g., “per booked meeting”). High alignment. |

| Flat Rate | 10% | 2% | Dead: Unsustainable for vendors due to variable AI compute costs. |

3. Vertical SaaS vs. Horizontal Bloat

Horizontal SaaS (think generic CRMs or project management tools) is facing an existential crisis. These broad platforms are becoming “bloatware,” easily replicable by AI-generated code or large foundational models.

Conversely, Vertical SaaS (software for specific industries like construction, biotech, or legal) is thriving. These platforms own proprietary workflows and data sets that generalist AI models cannot easily hallucinate. They are “compound startups,” solving multiple problems for a specific persona, making them incredibly difficult to rip out.

Vertical vs. Horizontal SaaS Performance (2026)

| Metric | Vertical SaaS (Niche) | Horizontal SaaS (General) | Analysis |

| CAGR (Growth) | 16.3% | 11.2% | Niche markets are less saturated and harder for AI to disrupt. |

| Sales & Marketing Spend | 17% of ARR | 21% of ARR | Verticals have clearer targets, lowering Customer Acquisition Cost (CAC). |

| Retention (NRR) | 115%+ | < 100% | Specific workflows create “moats” that generic tools cannot cross. |

| M&A Probability | Low (Target for IPO) | High (Target for Roll-up) | Horizontal tools are being bought and consolidated by PE firms. |

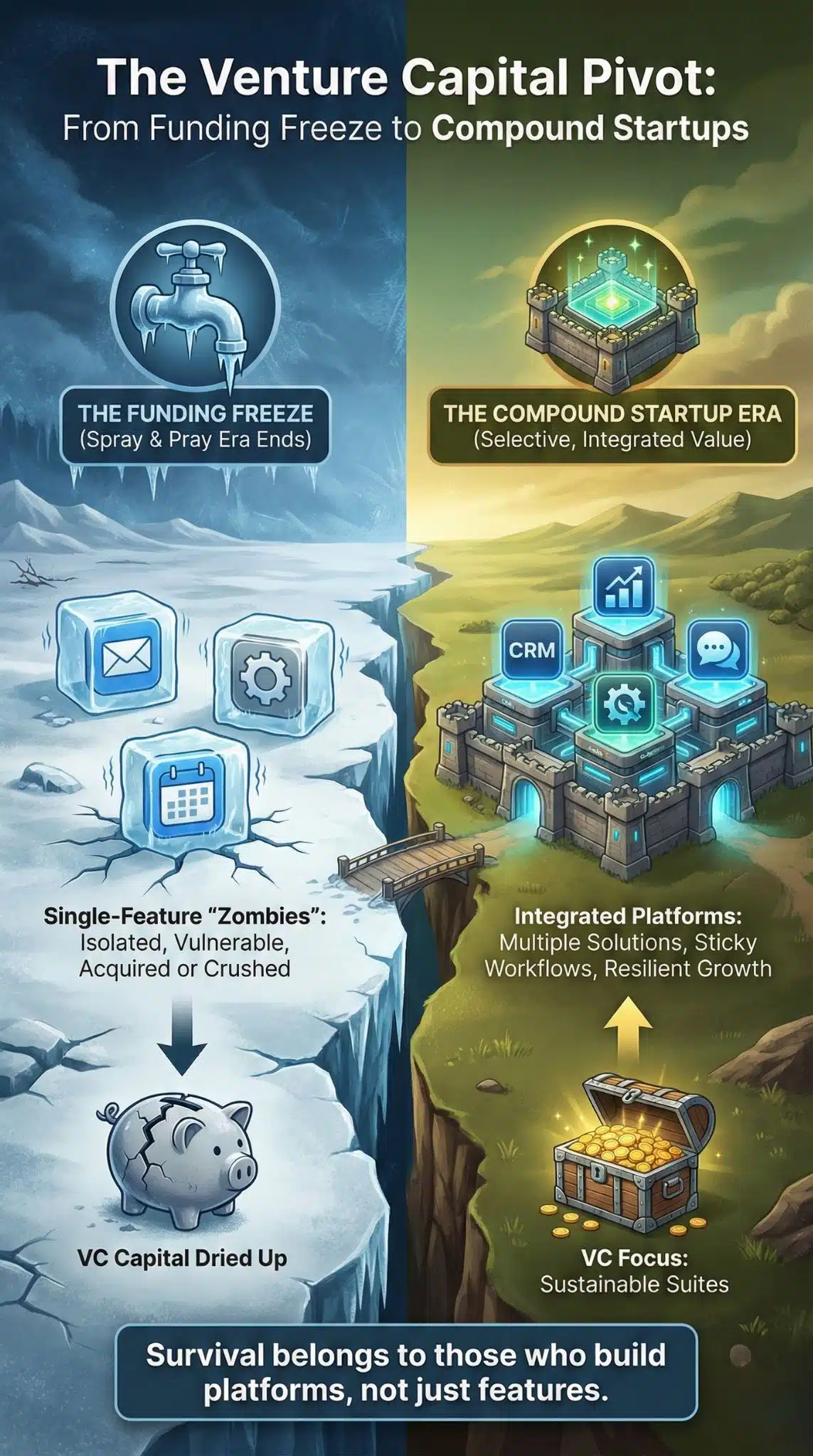

4. The Funding Freeze & The “Compound Startup”

The venture capital landscape has fundamentally changed. The “spray and pray” approach of 2021 is gone. In 2026, VCs are looking for “Compound Startups”—companies that build a suite of products from day one rather than a single point solution.

Single-feature products are being decimated by platform consolidation. If your startup only does “AI email writing,” you are a feature, not a company, and you will be acquired or crushed by Microsoft Copilot or Google Gemini.

5. M&A as the Primary Exit

With the IPO window still “selective” (open primarily for massive AI infrastructure plays), Mergers and Acquisitions (M&A) have become the default exit for the SaaS middle class. Private Equity (PE) firms are aggressively executing “buy-and-build” strategies, rolling up smaller, point-solution SaaS companies into larger platforms to achieve economies of scale and cross-sell opportunities.

Key 2026 PE Trends:

- Take-Private Deals: Public SaaS companies struggling with the AI transition are being bought out to be retooled away from quarterly scrutiny.

- The “Great Delisting”: Expect a wave of delistings as firms trade liquidity for the operational freedom to overhaul their pricing models.

Expert Perspectives

The industry is divided on the long-term impact of these shifts.

- The VC View: “Growth doesn’t always mean burn,” notes a recent analysis from Bessemer Venture Partners. They argue that “Shooting Stars”—startups that grow steadily (3x, 3x, 2x) with healthy margins—are far more resilient than the “Supernovas” that burn $125M to make $40M.

- The Founder View: Many founders feel trapped. Shifting from a seat-based model to usage-based pricing is technically complex and risky. As one CEO of a mid-sized CRM put it, “It’s like changing the engine of a plane while flying. If we get the metering wrong, we destroy trust. If we stay per-seat, we destroy our future.”

- The Counter-Argument: Some analysts warn that the swing toward efficiency is stifling innovation. By obsessing over the Rule of 40/X, companies may be under-investing in R&D, leaving them vulnerable to the next wave of disruptive AI agents that don’t care about profit margins yet.

Future Outlook: What Happens in Late 2026?

As we look toward the second half of 2026, three major trends will define the “What Next”:

- The “Agentic” Economy: We will move beyond “Copilots” (assistants) to “Agents” (autonomous workers). This will force the final death of seat-based pricing. The standard contract will look more like a labor contract (“Hire our AI Agent for $20k/year”) than a software subscription.

- Margin Recovery via SLMs: SaaS companies will master “Small Language Models” (SLMs). Instead of querying expensive models like GPT-5 for every task, companies will use specialized, cheaper models to restore their gross margins back toward the 75% range.

- The Rise of the “Micro-Unicorn”: We will see the first $1B valuation company with fewer than 20 employees, powered entirely by agentic workflows and automated GTM strategies.

Final Words

The SaaS shakeout is painful but necessary. It is purging the market of excess and forcing a return to business fundamentals. The companies that survive 2026 will be leaner, smarter, and priced for value delivered, not just access granted.