The United Kingdom’s transition to a carbon-neutral economy has entered a high-velocity phase in 2026, transitioning from high-level legislative targets to a tangible industrial and domestic reality. With the Seventh Carbon Budget now established and the National Wealth Fund actively deploying billions into “frontier” technologies, the strategic focus has shifted toward building the physical infrastructure—from offshore wind grids to carbon capture clusters—that will sustain the country through the 2030s.

How We Selected Our 12 Essential Facts About UK Net Zero 2050

To identify the most critical developments for this year, we analyzed the latest legislative updates from the Climate Change Committee (CCC) and the operational milestones of new state-led energy bodies. Our selection prioritizes structural shifts that directly impact investors, homeowners, and industrial leaders over the coming decade.

-

Legislative Maturity: We focused on the legally binding constraints of the new carbon budget.

-

Capital Mobilization: We examined the specific mandates of the National Wealth Fund and Great British Energy.

-

Technological Readiness: We included the transition points for domestic heating and international transport.

The following table provides a snapshot of the primary regulatory and financial pillars governing the UK’s Net Zero pathway in 2026.

| Strategy Pillar | 2026 Status | Core Objective |

| Seventh Carbon Budget | Set June 30, 2026 | Legally bind 2038–2042 emissions |

| Clean Power Mission | 2030 Implementation | 100% clean electricity grid |

| National Wealth Fund | £4bn Annual Deploy | De-risk green industrial clusters |

| Hydrogen Heating | Decision Expected | Determine future of domestic gas grid |

12 Essential Facts: UK Net Zero 2050 Strategy 2026

Success in the 2026 environment requires a deep understanding of how the government’s “Mission-led” approach is reshaping energy markets. These 12 facts highlight the critical components of the UK’s updated decarbonisation roadmap.

1. The Seventh Carbon Budget (CB7) Ceiling

In June 2026, the UK government legally codified the Seventh Carbon Budget, setting a strict emissions cap of 535 MtCO2e for the period 2038–2042. This budget is unique because it moves beyond the “easy wins” of renewable energy and requires the first significant reductions from hard-to-abate sectors like heavy industry and aviation. It represents a massive 87% reduction in emissions by 2040 relative to 1990 levels.

Best for: Corporate strategists and long-term asset managers needing regulatory certainty.

Why We Chose It: It is the primary legal “North Star” that will govern UK policy for the next two decades.

Things to consider: Failing to meet these budgets can lead to judicial reviews and forced policy corrections.

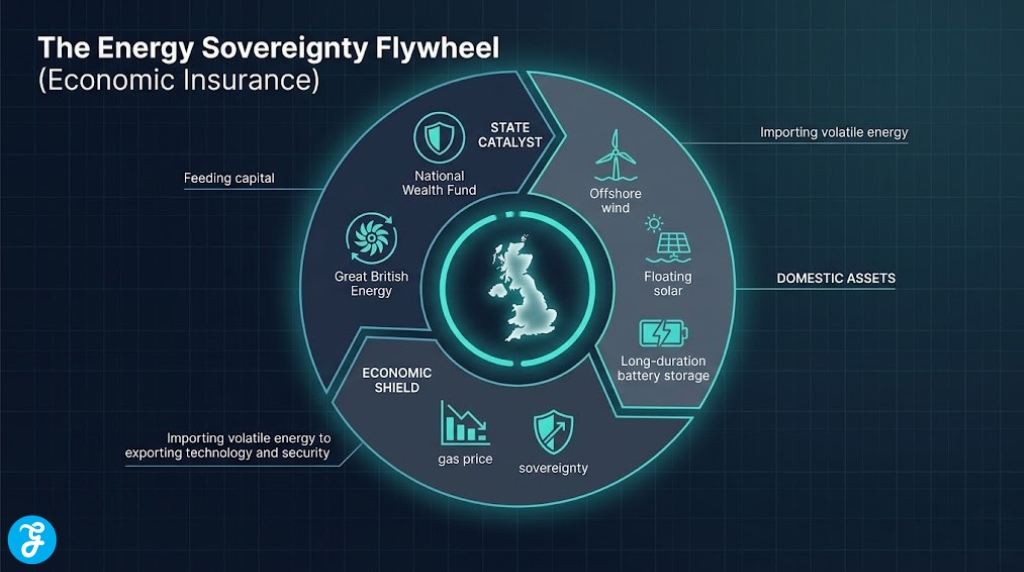

2. Great British Energy (GBE) as a Co-Investor

Fully operationalized in 2025, GBE is no longer just a concept; in 2026, it is actively deploying its £8.3 billion capitalization. Unlike a traditional utility, GBE acts as a lead investor or partner in offshore wind and tidal projects, specifically targeting technologies that are too “early-stage” for private banks. Its presence has already helped de-risk several floating offshore wind projects in the North Sea.

Best for: Clean energy developers seeking a strategic state-partner for high-risk projects.

Why We Chose It: It marks the return of the state as an active participant in the energy market.

Things to consider: GBE is headquartered in Scotland, focusing heavily on regional industrial development.

3. The 2030 “Clean Power” Acceleration

The UK has accelerated its target for a 100% clean electricity system to 2030, five years earlier than the previous 2035 goal. In 2026, this has triggered a massive overhaul of the planning system to fast-track grid connections for wind and solar. The National Energy System Operator (NESO) is now utilizing a “Clean Power Action Plan” to prioritize “pace over perfection” in infrastructure delivery.

Best for: Tech firms and data centers requiring massive, guaranteed green power supplies.

Why We Chose It: It is the foundational mission that enables the decarbonisation of all other sectors.

Things to consider: This target requires nearly doubling the current rate of offshore wind installation.

4. National Wealth Fund’s £4–5bn Annual Mandate

The National Wealth Fund (NWF) has officially entered its first full year of strategic deployment in 2026, aiming to invest between £4 billion and £5 billion annually through 2030. The fund’s priority sectors include green steel, battery manufacturing (gigafactories), and port upgrades. By providing equity and debt finance, the NWF aims to “crowd in” up to three times its value in private investment.

Best for: Industrial manufacturers looking to build large-scale decarbonisation facilities.

Why We Chose It: It provides the “patient capital” required for the UK’s industrial strategy.

Things to consider: The NWF specifically targets “frontier” industries that are critical for long-term domestic security.

5. Renewable Energy’s 7-Month Dominance Streak

As of April 2026, the UK has recorded seven consecutive months where wind and solar have outpaced gas as the primary source of electricity generation. This shift has been driven by the record-breaking CfD Allocation Round 7 (AR7) and a surge in solar deployment. Carbon intensity has dropped significantly, often dipping below 100 gCO2/kWh during peak wind periods.

Best for: Businesses looking to highlight their use of a cleaner national grid in sustainability reports.

Why We Chose It: It proves the operational feasibility of a renewable-led energy system.

Things to consider: Gas still plays a critical “balancing” role during low-wind winter months.

6. The 2026 “Hydrogen-Ready” Boiler Proposal

The government is currently finalizing a mandate that would require all new domestic boilers installed from late 2026 to be “hydrogen-ready.” While a final decision on hydrogen in the national gas grid isn’t expected until the end of the year, this rule ensures that the heating infrastructure is future-proofed. It prevents a “lock-in” of fossil fuel technology while the market decides between hydrogen and heat pumps.

Best for: Homeowners and property developers planning heating system upgrades.

Why We Chose It: It is a “low-regret” infrastructure decision that impacts millions of households.

Things to consider: A “hydrogen-ready” boiler still burns natural gas until the grid is actually converted.

7. Reinstated 2030 Ban on New ICE Vehicles

In a major policy reversal, the UK has reinstated the 2030 ban on the sale of new petrol and diesel cars (previously pushed to 2035). By 2026, the Zero Emission Vehicle (ZEV) mandate has become the dominant force in the UK auto market, requiring a significant percentage of every manufacturer’s fleet to be electric. This has drastically increased the availability of affordable EV models in the used car market.

Best for: Fleet managers and commuters looking to time their next vehicle purchase.

Why We Chose It: It restores the long-term certainty needed for the national charging rollout.

Things to consider: Hybrid vehicles may still be sold until 2035 if they meet specific efficiency standards.

8. Adoption of UK Sustainability Reporting Standards (SRS)

February 2026 saw the formal publication of the UK Sustainability Reporting Standards (UK SRS), which are based on the global ISSB (S1 and S2) framework. This means that large UK companies must now disclose their climate-related risks and their Scope 3 emissions using a standard that is internationally comparable. This has significantly reduced “greenwashing” by providing a transparent, data-driven baseline.

Best for: ESG compliance officers and institutional investors managing portfolio risk.

Why We Chose It: It brings financial-grade rigor to climate reporting.

Things to consider: While initially focused on listed firms, these standards are expected to filter down to large private companies by 2027.

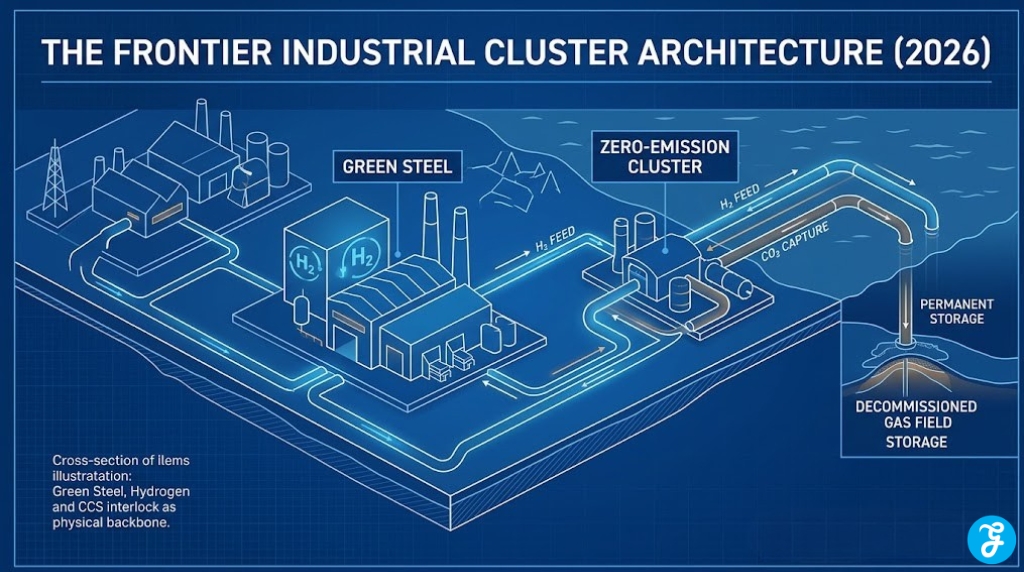

9. Carbon Capture and Storage (CCS) Cluster Construction

The UK’s flagship CCS clusters, including HyNet and the East Coast Cluster, have moved from planning into physical construction in 2026. Backed by a £20 billion government commitment, these clusters will capture CO2 from industrial sites and store it in depleted gas fields under the North Sea. This infrastructure is essential for the “Net” in Net Zero, allowing heavy industry to continue operating.

Best for: Chemical and cement manufacturers that cannot easily electrify their processes.

Why We Chose It: It is a vital component for maintaining the UK’s industrial base while meeting climate goals.

Things to consider: These clusters are often the focal points for the National Wealth Fund’s latest investments.

10. Inclusion of International Aviation and Shipping (IAS)

In a move for greater transparency, the Seventh Carbon Budget now formally includes the UK’s share of international aviation and shipping emissions. Previously, these were treated as “out of scope” for national targets. This change has put immediate pressure on the UK aviation sector to accelerate the deployment of Sustainable Aviation Fuels (SAF) and zero-emission flight technologies.

Best for: Logistics and travel companies navigating the updated carbon pricing landscape.

Why We Chose It: It ensures the UK’s climate targets are genuinely comprehensive.

Things to consider: This inclusion will likely lead to higher carbon costs for long-haul shipping and flight operators.

11. The Biodiversity Net Gain (BNG) Mandate for Energy

Major Net Zero infrastructure projects (like wind farms and grid lines) must now demonstrate a 10% Biodiversity Net Gain (BNG) as of May 2026. This ensures that the green transition does not come at the cost of local nature. Developers are now required to use sophisticated ecological mapping to prove that their project leaves the local ecosystem in a better state than before.

Best for: Landowners and infrastructure developers managing large-scale green projects.

Why We Chose It: It prevents the “green vs. green” conflict between climate and nature goals.

Things to consider: This has created a secondary market for “biodiversity units” that developers can purchase for off-site mitigation.

12. Net Zero as “Economic Insurance”

A landmark CCC report released in early 2026 has reframed Net Zero as an economic insurance policy. The report demonstrates that the total cost of reaching the 2050 target is less than the projected cost of a single major fossil fuel price shock similar to the 2022 energy crisis. This data-driven realization has shifted the narrative from “costly sacrifice” to “essential energy security.”

Best for: Policy makers and business leaders justifying transition costs to stakeholders.

Why We Chose It: It provides the strongest economic argument for maintaining the current pace of investment.

Things to consider: The UK currently saves roughly £7 million per day in gas purchases due to new wind and solar capacity.

An Overview Of the UK’s Net Zero 2050 Framework

The UK’s strategy is now built on a foundation of “Mission-led” pillars that combine state intervention with strict market regulations. The following comparison highlights how these tools interact in 2026.

| Strategy Pillar | Lead Body | Strategic Function |

| Clean Power 2030 | NESO | Rapid grid and renewables rollout |

| Industrial De-risking | National Wealth Fund | Capital for frontier tech and ports |

| Market Transparency | UK SRS (ISSB) | Standardized climate disclosure |

| Binding Pathways | Carbon Budget 7 | Legally capped emissions through 2042 |

Our Top 3 Picks and Why?

-

The Seventh Carbon Budget: This is our top pick because it provides the ultimate legal and regulatory certainty for the 2040s. It ensures that the transition remains a statutory requirement regardless of political shifts.

-

The National Wealth Fund: We chose this for its role in industrial de-risking. By 2026, the NWF is the primary engine allowing the UK to build its own green supply chains for batteries and steel.

-

The Clean Power 2030 Mission: This is essential because it sets a high-velocity pace for the entire energy system. It forces planning and grid reforms that were previously stalled for a decade.

How to Align with the UK Net Zero 2050 Strategy 2026?

Adapting to the 2026 roadmap requires a shift from “voluntary” sustainability toward “mandatory” compliance and strategic capital alignment. Use the following framework to evaluate your position in the current market.

The Selection Framework

-

Audit Your Disclosure Compliance: Ensure your sustainability reporting aligns with the new UK SRS (ISSB) standards by your 2026 year-end.

-

Monitor Infrastructure Hubs: If you are an industrial firm, align your footprint with the CCS or Hydrogen clusters receiving NWF support.

-

Evaluate Heating Timelines: If you are replacing commercial or domestic boilers, review the 2026 “hydrogen-ready” mandates before making a purchase.

-

Check Your Supply Chain: With the focus shifting to Scope 3, you must ensure your suppliers are also on a verified Net Zero pathway.

The following matrix helps you identify your primary strategic focus based on your economic role.

| Role | Primary Focus | Recommended Action |

| Homeowner | Heating & Transport | Switch to heat pumps before 2026 subsidies expire; plan for EV switch by 2028. |

| Business Leader | SRS Compliance | Transition from TCFD to UK SRS reporting standards immediately. |

| Infrastructure Dev | Grid Connectivity | Partner with NESO to secure grid access under the 2030 Clean Power Mission. |

| Industrialist | De-risking Finance | Engage with the National Wealth Fund for co-investment in green manufacturing. |

The Final Checklist

-

Have you reviewed the specific 2038–2042 limits set in the Seventh Carbon Budget?

-

Is your company preparing for the transition from TCFD to ISSB-based UK SRS reporting?

-

Have you checked the “Clean Power 2030” implementation plan for regional grid updates?

-

Are your new heating installations compliant with the late-2026 “hydrogen-ready” proposals?

-

Have you assessed your project’s 10% Biodiversity Net Gain requirement for May 2026?

Securing Britain’s Energy Sovereignty

As we move through 2026, the UK’s Net Zero strategy has matured into a comprehensive industrial plan. The shift toward publicly owned energy through GBE and the aggressive de-risking provided by the National Wealth Fund are building a system that is designed for energy security as much as it is for environmental protection. While the technical challenges of the Seventh Carbon Budget are significant, the regulatory and financial framework is now in place to ensure that the UK remains at the forefront of the global green economy.

Frequently Asked Questions About UK Net Zero 2050 Strategy 2026

Is the UK actually on track for 2050?

Answer: In 2026, the Climate Change Committee considers the target achievable, but only if the 2030 Clean Power Mission is met. The success of the current “acceleration” phase is critical to staying on the statutory pathway.

Will I be forced to remove my gas boiler in 2026?

Answer: No. The 2026 proposal only applies to the installation of new boilers, requiring them to be hydrogen-ready. There is currently no mandate for homeowners to remove working natural gas boilers.

What is the National Wealth Fund’s role in Net Zero?

Answer: The NWF provides debt, equity, and guarantees to large-scale green projects that private banks consider too risky. It specifically focuses on “frontier” industries like green steel and carbon capture.

How does the 2030 ICE ban affect used cars?

Answer: The 2030 ban only applies to the sale of new petrol and diesel cars. You will still be able to buy, sell, and drive used internal combustion engine vehicles well into the 2040s.

What happens if a company fails to report under UK SRS?

Answer: In 2026, regulators are consulting on making these standards mandatory for listed firms. Non-compliance could lead to financial penalties, legal challenges from shareholders, and significant reputational damage in the ESG investment market.