Imagine paying taxes on every penny your investments earn, year after year. It stings, right? As an investor, you work hard to grow your money, but Uncle Sam often takes a big bite out of those gains. This common headache leaves many folks frustrated, wondering if there’s a smarter way to keep more in their pockets. Think of it like trying to fill a leaky bucket; no matter how much you pour in, some always slips away.

Tax-Advantaged Accounts change that game, with one key fact showing Americans saved over $300 billion in taxes through them last year alone. This post guides you through the basics, from 401(k)s to HSAs, and shares tips to pick and max out the best ones for your life.

You’ll learn simple steps to slash taxes and boost your wealth. Ready to save big?

Understanding Tax-Advantaged Accounts

Tax-advantaged accounts act like smart tools for your money. They help you save on taxes while building wealth. Think of them as special buckets where your investments grow with less tax drag.

People use them for retirement savings, college costs, or health expenses. These accounts cut your tax bill through deductions or tax-free growth. Investors love them because they boost long-term savings. Take a traditional IRA, for example; you make pretax contributions that lower your taxable income now.

Folks often mix up tax-deferred and tax-exempt options. Tax-deferred means you pay taxes later, like in 401(k) plans. Tax-exempt lets earnings grow tax-free, as in Roth IRAs. Health savings accounts (HSAs) offer triple tax benefits: deductions on contributions, tax-free growth, and tax-free withdrawals for medical bills.

Savings plans like 529s focus on college savings with tax perks. Pick ones that fit your financial planning goals. Diversify across types to maximize tax benefits and secure your future.

Mechanics of Tax-Advantaged Accounts

Ever feel like taxes nibble away at your hard-earned cash, like a sneaky squirrel raiding a bird feeder? These accounts fight back by either postponing the tax bite until later or dodging it completely on growth, giving your investments room to sprint ahead.

Understanding Tax-Deferred Accounts

Tax-deferred accounts let you grow your retirement savings without paying taxes right away. You put money in before taxes, so contributions lower your taxable income now. Investments inside these accounts build up over time, and taxes hit only when you take money out later.

Think of it like planting a seed in fertile soil; the growth happens quietly until harvest time. Traditional IRAs and 401(k) plans fit this mold, offering tax deductions on pretax contributions. Savers love how these accounts promote long-term savings through deferred growth.

People often pick tax-deferred options for their tax benefits on investments. Your money compounds without annual capital gains taxes, dragging it down. Eligibility depends on income and job status, but many qualify for these retirement accounts.

Imagine chatting with a friend who says, “Hey, I slashed my tax bill by maxing out my 401(k).” Contribution limits change yearly, as the $23,000 cap for 401(k) plans in 2024. Health savings accounts sometimes work this way too, blending tax advantages with medical expenses. Diversify across these to boost wealth accumulation in your financial planning.

Exploring Tax-Exempt Accounts

Tax-exempt accounts act like a shield for your savings, keeping Uncle Sam away from your growth and withdrawals. Imagine planting a seed that sprouts into a money tree, tax-free. These accounts let you pay taxes upfront on contributions, then watch investments build without capital gains taxes dragging them down.

Roth IRAs shine here, offering tax-free withdrawals in retirement if you follow the rules. Folks, it’s like getting a free pass on future taxes, perfect for long-term financial planning.

Health savings accounts, or HSAs, join the party too, with triple tax benefits: pretax contributions, tax-free growth, and tax-free pulls for medical expenses. Picture stashing cash for health costs while your balance swells untouched by taxes.

College savings plans, such as 529s, deliver tax-exempt earnings when used for school bills, easing the burden on families. Investors love how these boost wealth accumulation without the usual tax hits.

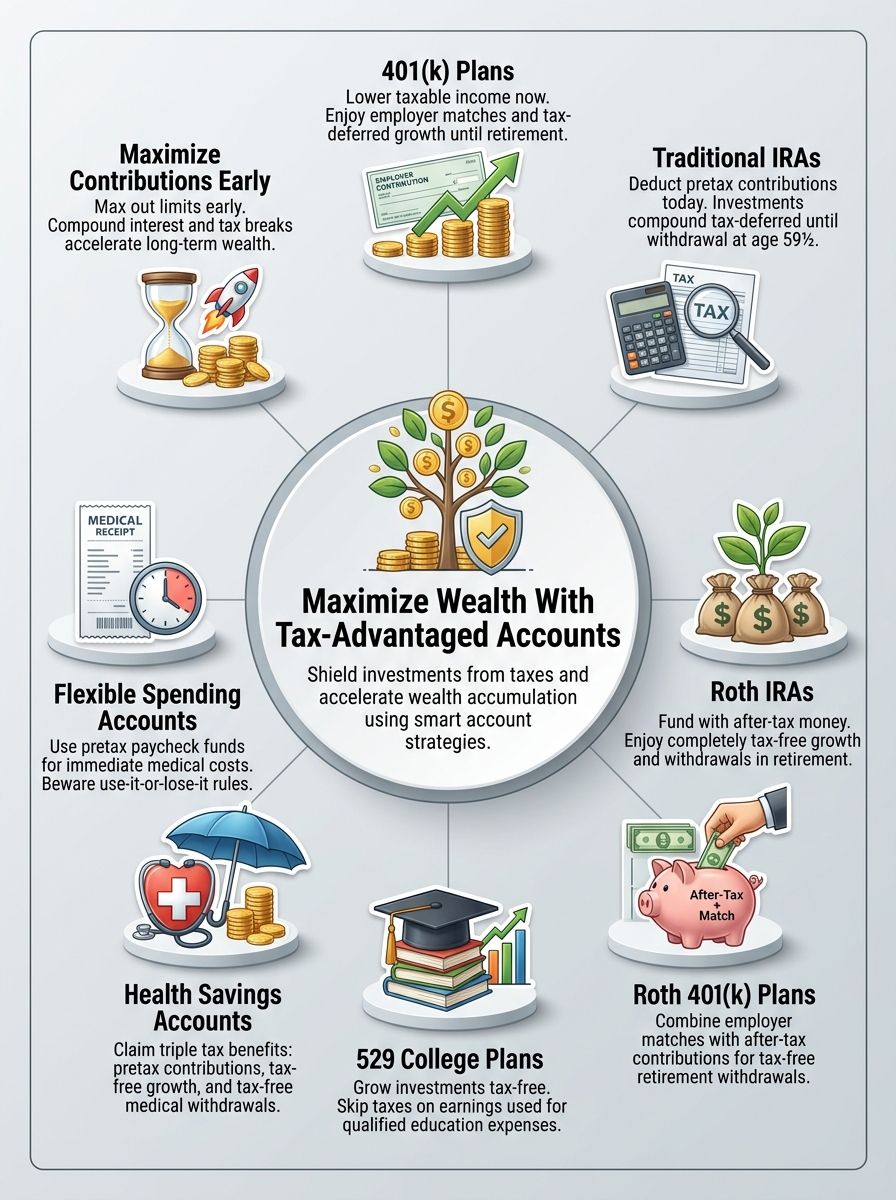

Types of Tax-Advantaged Accounts

You know, picking the right account can feel like finding the perfect pair of shoes, one that fits your life just right and saves you money on taxes along the way. Let’s chat about some popular options that investors love, and see which might spark your interest in growing your nest egg.

Benefits of 401(k) Plans

Employers offer 401(k) plans as solid retirement accounts. You make pretax contributions straight from your paycheck. This lowers your taxable income right away. Investments grow tax-deferred until you withdraw them in retirement.

Many companies match a part of what you put in, like free money for your savings plans. Picture your boss adding to your nest egg; it boosts wealth accumulation fast. For 2023, you can contribute up to $22,500 if under 50, or $30,000 if 50 or older.

These tax benefits help with long-term financial planning. People love how 401(k)s fit into investment strategies. They let you pick stocks, bonds, or funds for diversified growth. Withdrawals after age 59½ avoid penalties, keeping more cash in your pocket.

Families use them alongside other accounts for broader tax deductions. John, a reader like you, shared his story: he maxed his plan and saw his balance double in a decade thanks to compound interest. Tax-free growth on matches feels like a win against Uncle Sam.

A 401(k) match is the closest thing to free money in investing, says financial expert Suze Orman.

Advantages of Traditional IRAs

While 401(k) plans shine through employer perks, Traditional IRAs step in as a flexible choice for your retirement savings. You make contributions with pretax dollars, which lowers your taxable income right away.

Think of it like planting seeds in fertile soil; they grow without tax bites until harvest time. For 2023, you can add up to $6,500, or $7,500 if you’re 50 or older, boosting your tax deductions. Earnings compound tax-deferred, a quiet powerhouse for wealth accumulation.

Anyone with earned income qualifies, no boss required, so you control your financial planning. Withdraw funds after 59½ without penalties, though taxes apply then. Picture stashing cash in a tax-shielded vault; it builds steadily for future needs.

Mix this with other investment accounts, and you diversify your savings plans. HSAs pair well, too, but Traditional IRAs focus on long-term retirement goals, offering solid tax benefits for smart investors.

Features of Roth IRAs

Roth IRAs offer tax-free growth on your investments. You fund them with after-tax contributions. This means you pay taxes now, but qualified withdrawals come out tax-free in retirement.

People love this for long-term savings plans. Imagine planting a seed that grows without the taxman taking a bite later. These accounts suit folks under certain income limits. For 2023, single filers can contribute up to $6,500 if their income stays below $153,000.

Married couples filing jointly get a $228,000 limit. Roth IRAs skip required minimum distributions during your lifetime. You pass them on more easily to heirs, too.

Flexibility shines in Roth IRAs for retirement accounts. Pull out your original contributions anytime without penalties or taxes. Earnings need five years and age 59½ for tax-free status.

Health savings blend in if you roll over, but stick to the rules. Investors build wealth accumulation here with stocks or bonds. Tax benefits boost your financial planning. Many choose Roth for the expected higher taxes later. Picture dodging capital gains hits on big growth. These plans promote smart investment strategies.

Insights into Roth 401(k) Plans

Many employers offer Roth 401(k) plans as part of retirement savings. You make contributions with after-tax dollars, so no tax deductions up front. Investments grow tax-free, and qualified withdrawals come out tax-free too, if you follow the rules.

Think of it like planting a seed that sprouts money without Uncle Sam taking a bite later. These plans suit folks expecting higher tax brackets in retirement.

Contribution limits hit $22,500 in 2023 for those under 50, with $7,500 extra for catch-up if you’re older. Employers often match a portion, boosting your wealth accumulation. Healthier financial planning happens when you mix this with other accounts. Folks love the flexibility for long-term growth, especially with tax-free withdrawals after age 59½ and five years in the plan.

Overview of 529 College Savings Plans

Parents, listen up. You want to save for your kid’s college without taxes eating away at your money. Enter 529 college savings plans. These state-run savings plans let you grow your investments tax-free.

Withdraw the money for qualified education costs, and you skip taxes on earnings. Think tuition, books, even room and board. States offer them, and some give tax deductions on contributions.

Picture stashing cash in a piggy bank that multiplies without Uncle Sam taking a cut. Anyone can open one, not just parents. Grandparents often chip in too. No age limits apply, so start early for compound growth.

Contribution rules vary by state, but you can put in up to $18,000 a year per person without gift taxes. Use these for college savings in your financial planning. They beat regular accounts for tax benefits on education expenses.

Utilizing Health Savings Accounts (HSAs)

Shifting from saving for college with 529 plans, let’s talk about another smart way to handle expenses, like those pesky medical bills, through health savings accounts, or HSAs. These accounts let you set aside pretax contributions to cover health costs, and they pack a punch with tax benefits that boost your financial planning.

You put money in before taxes, watch it grow tax-free, and pull it out without taxes for qualified medical expenses, like doctor visits or prescriptions. Imagine stashing cash that works harder for you, dodging taxes at every turn, much like a secret weapon in your savings plans arsenal.

Investors love HSAs because they double as retirement accounts after age 65, letting you use funds for anything without penalties, though taxes apply on non-medical withdrawals then.

Eligibility ties to having a high-deductible health plan, so check that first to access these tax-advantaged accounts. Contribution limits change yearly, say up to $3,850 for individuals or $7,750 for families in 2023, plus catch-up contributions if you’re over 55.

Folks often max them out to build wealth accumulation over time, turning routine health expenses into savvy investment strategies. Envision this: you contribute now, invest the money in stocks or funds, and let compound growth do its magic, all while slashing your tax deductions.

HSAs offer flexibility, too, rolling over unused funds year after year, unlike some other accounts that force you to spend or lose them.

Maximizing Flexible Spending Accounts (FSAs)

While HSAs offer long-term savings power for medical costs, FSAs step in as a nimble sidekick for handling those same expenses with pretax contributions right now. You set aside money from your paycheck before taxes hit, slashing your taxable income and letting you pay for doctor visits, prescriptions, or even Band-Aids without Uncle Sam taking a cut.

Imagine, it’s like getting a discount on health bills that adds up fast; many folks save hundreds each year by maxing out.

FSAs shine for predictable costs, but watch that use-it-or-lose-it rule; folks often forfeit unused funds at year’s end, so plan smart. Employers might allow a grace period or small carryover, up to $640 for 2024, giving you a buffer to avoid waste.

Contribute up to $3,200 annually, and pair it with other tax-advantaged accounts for broader financial planning; think of it as your secret weapon against rising healthcare expenses, turning everyday outflows into savvy savings plays.

Key Benefits of Tax-Advantaged Accounts

Imagine your money growing like a snowball rolling downhill, picking up speed without the taxman taking a bite each year. These accounts pack a punch for your wallet, turning everyday savings into a powerhouse for your future dreams, so keep reading to see how they fit your life.

Enhance Tax Savings on Contributions

You put money into tax-advantaged accounts, and you cut your taxes right away. Think of it like getting a discount on your contributions. For example, a traditional IRA lets you deduct pretax contributions from your income.

This lowers your tax bill now. Retirement accounts like 401(k) plans work the same way. Employers match some funds, boosting your savings. Imagine your boss chipping in, “Hey, I’ll add to that pot for you.” Tax deductions make every dollar count more.

Contributions to Roth IRAs use after-tax money, but you skip taxes on withdrawals later. Health savings accounts (HSAs) offer triple tax benefits: pretax contributions, tax-free growth, and tax-free pulls for medical expenses.

College savings in 529 plans grow without taxes hitting earnings. Investments inside these accounts build wealth faster. Picture your money growing like a well-fed plant, safe from tax weeds. Financial planning gets easier with these tools.

Secure Tax-Free or Deferred Growth

Tax benefits shine bright in tax-advantaged accounts, like retirement savings plans or health savings accounts. Visualize this: your investments grow without Uncle Sam taking a bite each year.

In tax-deferred accounts, such as traditional IRAs or 401(k) plans, taxes wait until you withdraw funds. That delay lets your money compound faster, building wealth over time. Roth IRAs and Roth 401(k) plans offer tax-free growth, where qualified withdrawals come out clean, no taxes due. Imagine stashing pretax contributions now, watching them balloon through smart investment strategies.

Savings plans like 529 college savings accounts provide tax-free earnings for education expenses, easing the load on your wallet. Health savings accounts (HSAs) triple-dip with tax deductions on contributions, tax-free growth, and tax-free withdrawals for medical costs.

These features turn everyday savings into powerful tools for financial planning. Diversify across account types to lock in those gains. Such perks promote long-term savings, setting you up for a brighter future.

Promote Long-Term Savings

Tax-advantaged accounts act like a trusty sidekick in your financial journey, encouraging you to stash away money for the long haul. They reward patience with tax breaks on growth, turning small contributions into hefty nest eggs over time.

Imagine: you sock away pretax dollars in a 401(k) plan, and compound interest works its magic without Uncle Sam taking a cut each year. Investors love how these retirement accounts build wealth accumulation steadily, much like planting a seed that grows into a mighty oak.

Smart savers use Roth IRAs for tax-free withdrawals down the road, making it easier to commit to long-term goals like a comfy retirement. Health savings accounts let you set aside funds for future medical expenses, growing tax-free and promoting disciplined saving habits.

Diversify with 529 college savings plans to cover education costs years ahead, easing the burden on your wallet later. These investment strategies turn everyday contributions into powerful tools for financial planning, helping you stay the course without the drag of immediate taxes.

How to Choose the Right Tax-Advantaged Account

Picking the perfect tax-advantaged account starts with your dreams, like retiring on a beach or funding a kid’s college adventure. Match those goals to options that save you money, and you’ll laugh all the way to the bank.

Aligning with Your Financial Goals

Match your tax-advantaged accounts to your big dreams, like saving for retirement or college. Imagine: you aim for a cozy retirement nest egg. Grab a 401(k) or IRA for those tax benefits on contributions and growth.

These retirement accounts boost your investments over time. Feel that relief? No more tax worries eating into your savings plans.

Short-term goals matter too, folks. Eye health expenses? An HSA offers triple tax perks: pretax contributions, tax-free growth, and tax-free withdrawals for medical bills. Or stash cash in a 529 for college savings; watch it grow without capital gains taxes hitting hard. Mix accounts to fit your financial planning puzzle, and build wealth that sticks.

Understanding Contribution Limits

Contribution limits keep your tax-advantaged accounts in check, like guardrails on a winding road.

| Account Type | Key Limits for 2026 | Catch-Up Details | Quick Tips |

|---|---|---|---|

| 401(k) Plans | You can contribute up to $23,000 per year. Employers often match part of that. | Add $7,500 if you’re 50 or older. That boosts your nest egg fast. | Push for the max to grab free money from your boss. Imagine it as a bonus you earn by saving. |

| Traditional IRAs | The limit sits at $7,000 for most folks. Income affects deductions. | Over 50? Toss in an extra $1,000. It compounds over time. | Check your earnings first. This account fits if you want tax breaks now. |

| Roth IRAs | Same $7,000 cap as traditional. Phase-outs start at $146,000 for singles. | An extra $1,000 for those 50-plus. Growth stays tax-free forever. | Earn too much? Backdoor contributions might work. Talk to a pro about that trick. |

| Roth 401(k) Plans | Matches 401(k) at $23,000. No income limits here. | $7,500 more if 50 or up. Withdrawals come tax-free in retirement. | Pick this for future tax wins. It’s like planting seeds that grow without weeds. |

| 529 College Savings Plans | No federal limit, but states cap lifetime totals around $235,000 to $550,000. Gifts up to $18,000 per year avoid taxes. | No age-based extras. Focus on education costs. | Start small for your kids. Watch it grow tax-free for school bills. |

| Health Savings Accounts (HSAs) | $4,150 for individuals, $8,300 for families. Need high-deductible health plans. | Age 55? Add $1,000. Triple tax advantages shine here. | Use it for medical needs. Let leftovers invest like a retirement fund. |

| Flexible Spending Accounts (FSAs) | Up to $3,200 per year. Funds must be used by year-end. | No catch-ups. Employer sets the rules. | Plan your spending wisely. It’s pre-tax money for health or dependent care. |

Assessing Eligibility Requirements

Eligibility rules differ for each tax-advantaged account, so let’s break them down simply. Employers offer 401(k) plans to their workers, and you join if your job qualifies. Traditional IRAs let anyone with earned income contribute, but you stop at age 72 for required distributions.

Roth IRAs come with income caps; singles earning over $144,000 in 2023 face limits on contributions. Roth 401(k) plans follow similar employer rules, yet they skip income restrictions for high earners.

Think about 529 college savings plans next; anyone can open these for education expenses, no age or income barriers. Health savings accounts (HSAs) require a high-deductible health plan, and you max out at $3,850 for individuals in 2023.

Flexible spending accounts (FSAs) are tied to your job, with employers setting the terms for pretax contributions on medical costs. Match these to your situation, and you boost retirement savings or tax benefits without a hitch.

Strategies for Maximizing Tax-Advantaged Accounts

Kick off your investments early to let compound interest work its magic, max out contributions to grab every tax break, and mix up account types for a balanced ride—stick around for the full scoop on turning these moves into your financial superpower.

Emphasize Early Contributions for Optimal Growth

Start your contributions early in tax-advantaged accounts, folks. Time acts like a secret sauce for your investments. Imagine this: you toss in money now, and compound growth kicks in over decades.

A 25-year-old puts $5,000 yearly into a Roth IRA. By 65, that could balloon to over $1 million, thanks to an average 7% returns. Delaying until 35? You might see half that amount. Early moves build serious wealth accumulation.

Folks love how pretax contributions in 401(k) plans grow tax-deferred. You dodge taxes now, watch savings multiply. Imagine chatting with your future self, “Hey, thanks for starting young!” Retirement savings thrive on this strategy.

Mix in HSAs for health expenses, or 529 plans for college savings. Your financial planning gets a boost, simple as that.

Ensure Full Benefits through Adequate Contributions

Max out your contributions to grab every tax benefit available. Imagine you put money into a 401(k) plan up to the limit, and boom, you slash your taxable income right away. Employers often match a chunk of what you add, like free cash, boosting your retirement savings.

Hit that full match, say 6% of your salary, and watch your investments grow faster. Tax deductions kick in strongly with pretax contributions, easing your bill now.

Spread contributions across accounts for bigger wins. Start with a Roth IRA with after-tax money, then enjoy tax-free withdrawals later. Health savings accounts let you sock away pretax dollars for medical expenses, turning everyday costs into smart financial planning.

Aim for the max, folks, like $3,850 for individuals in HSAs this year, to build wealth without Uncle Sam taking a big bite. Mix in 529 college savings plans, and you shield education funds from taxes, too.

Diversify Your Portfolio Across Different Account Types

Once you’ve nailed down those adequate contributions to reap full benefits, think about spreading your investments wide. Diversify your portfolio across different tax-advantaged accounts, like mixing a 401(k) with a Roth IRA and an HSA.

This approach acts like a safety net, protecting your retirement savings from big tax hits down the road. Picture your financial planning as a balanced meal; you wouldn’t eat just one food group. Blend traditional IRAs for pretax contributions with Roth options for tax-free withdrawals.

Add in 529 college savings plans for education expenses or health savings accounts for medical costs. Such strategies boost wealth accumulation, cut capital gains taxes, and align with your long-term investment strategies.

The Bottom Line

Tax-advantaged accounts boost your retirement savings and investments. They cut tax bills on contributions and offer tax-free growth. Imagine you stash money in a 401(k) plan or traditional IRA, and watch it grow without Uncle Sam taking a bite right away.

Investors love these for building wealth over time. Health savings accounts handle medical expenses with tax deductions, while 529 college savings plans cover education costs tax-free. Explore financial planning with these tools, and you secure a brighter future. Roth IRAs let earnings grow tax-free for qualified withdrawals. Mix in flexible spending accounts to pay pretax for health needs.

Smart folks max out limits each year, turning small steps into big gains. Tax benefits like these make saving feel like a win, every single time.

FAQs on Tax-Advantaged Accounts

1. What exactly are tax-advantaged accounts, and why do they matter to every investor?

Hey, picture this: tax-advantaged accounts act like a secret vault for your money, shielding it from hefty taxes while it grows. Investors love them because they let your savings work harder, you know, like compounding interest on steroids. Think of classics like the 401(k) or IRA; they cut your tax bill now or later, making retirement feel less like a distant dream.

2. How does a 401(k) help with my taxes as an investor?

A 401(k) lets you stash pre-tax dollars from your paycheck, lowering your taxable income right away. It grows tax-free until you pull it out in retirement.

3. What’s the big deal with a Roth IRA for smart investors?

Unlike traditional IRAs, a Roth IRA takes after-tax contributions, but then your money grows and is withdrawn tax-free, forever. It’s like planting a money tree that bears fruit without the IRS picking any. Perfect if you expect higher taxes down the road, my friend.

4. Can health savings accounts count as tax-advantaged for investors, too?

Yes, an HSA offers triple tax perks: contributions go in pre-tax, earnings grow tax-free, and medical withdrawals stay tax-free.