Deciding where to allocate your hard-earned savings is one of the most consequential financial choices for Canadians this year. As inflation and shifting tax brackets alter the economic landscape, the debate between the Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA) has become increasingly nuanced.

How We Selected Our 5 Best RRSP vs TFSA 2025 Facts

To curate this list, we analysed the 2025 Canada Revenue Agency (CRA) contribution limits, current marginal tax rates across provinces, and long-term fiscal projections regarding Old Age Security (OAS) clawbacks. Our selection was filtered based on three primary metrics: the immediate impact on annual tax returns, the flexibility of asset liquidation, and the preservation of government benefits during retirement.

The 5 Most Essential RRSP vs TFSA 2025 Facts for Canadian Investors

Understanding the structural differences between these accounts is the first step toward building a resilient financial future. Each account serves a distinct purpose, and the “best” choice often depends on your current income versus your expected income in retirement.

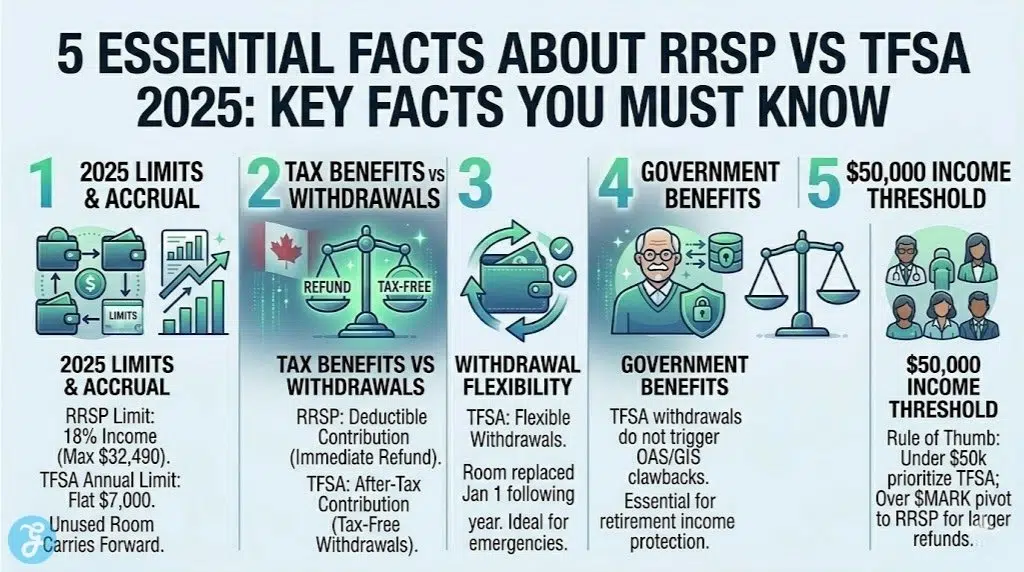

1. 2025 Contribution Limits and Room Accrual

For the 2025 tax year, the CRA has set specific caps that dictate how much “room” you have to grow your wealth. The RRSP limit is calculated as 18% of your previous year’s earned income, up to a maximum of $32,490. In contrast, the TFSA annual limit is a flat $7,000, regardless of your income level.

Best for: High-income earners looking to maximise their total annual savings volume.

Why We Chose It:

-

It defines the physical boundary of your tax-advantaged saving space.

-

It highlights the significant difference in “room” available for those with high earned income.

-

It reminds investors that unused room from previous years carries forward indefinitely for both accounts.

Things to consider: If you have a workplace pension (RPP), your RRSP room will be reduced by a “pension adjustment” on your T4.

2. Immediate Tax Relief vs. Long-Term Tax-Free Withdrawals

The fundamental divide between these accounts lies in the timing of the tax benefit. RRSP contributions are “pre-tax,” meaning they reduce your taxable income today and often trigger a significant tax refund. TFSAs are “post-tax” accounts; you get no immediate refund, but every dollar earned and withdrawn is completely tax-free.

Best for: Investors in the top tax brackets who expect to be in a lower bracket during retirement.

Why We Chose It:

-

It is the primary engine for tax-efficient wealth accumulation.

-

It illustrates the trade-off between a “cheaper” investment today (RRSP) and “cleaner” income tomorrow (TFSA).

-

It helps investors understand the impact on their current year’s cash flow.

Things to consider: Withdrawing from an RRSP early triggers immediate withholding tax and permanently destroys that contribution room.

3. Withdrawal Flexibility and Re-contribution Rights

One of the most misunderstood aspects of the RRSP vs TFSA 2025 debate is what happens after you take money out. TFSA withdrawals are incredibly flexible; any amount you withdraw is added back to your contribution room on January 1st of the following year. RRSP room, once used and withdrawn, is gone forever.

Best for: Emergency funds, short-term goals, or those with fluctuating income.

Why We Chose It:

-

It provides a safety net for investors who might need their capital before retirement.

-

It highlights the “recyclable” nature of TFSA room.

-

It prevents the permanent loss of tax-sheltered space during unexpected life events.

Things to consider: Withdrawing from a TFSA in December allows you to re-contribute just a few weeks later in January.

4. Avoiding Government Benefit Clawbacks in Retirement

In 2025, retirement planning is as much about what you keep as what you earn. Income from an RRSP (which becomes a RRIF) counts as taxable income and can trigger a “clawback” of Old Age Security (OAS) benefits if your income exceeds certain thresholds. TFSA withdrawals are invisible to these calculations.

Best for: Retirees or near-retirees aiming to maintain their full government entitlements.

Why We Chose It:

-

It protects the “bottom line” of your retirement income.

-

It identifies a hidden cost of RRSP-only strategies for middle-to-high earners.

-

It showcases the TFSA as a strategic tool for managing your “on-paper” income.

Things to consider: Strategic TFSA use can help you stay below the Guaranteed Income Supplement (GIS) income limits as well.

5. The Optimal $50,000 Income Threshold for Allocation

Financial planners often use a $50,000 annual income as the “pivot point” for advice. If you earn less than this amount, the immediate tax deduction of an RRSP is relatively small, making the TFSA’s tax-free growth more valuable. Once your income climbs significantly above this mark, the RRSP refund becomes much more impactful.

Best for: Young professionals and middle-income earners deciding where to put their first dollar.

Why We Chose It:

-

It provides a simple, actionable rule of thumb for account prioritisation.

-

It prevents lower-income earners from “wasting” RRSP room when their tax rate is low.

-

It aligns your savings strategy with your current marginal tax bracket.

Things to consider: If you expect your income to rise rapidly in the future, it may be wise to save your RRSP room for those higher-income years.

An Overview Of RRSP vs TFSA 2025 and Account Efficiencies

Comparing the mechanical advantages of these two accounts requires looking at how they treat your money at different stages of life. While the RRSP acts as a “tax-deferred” vehicle, the TFSA is a “tax-paid” vehicle that offers superior agility.

Overview Comparison Table

The table below outlines the key differences you need to know for the 2025 fiscal year.

| Feature | RRSP (2025) | TFSA (2025) |

| Annual Limit | 18% of income (Max $32,490) | $7,000 |

| Tax on Contribution | Fully Deductible (Refund) | None (After-tax dollars) |

| Tax on Withdrawal | Taxed as Ordinary Income | 100% Tax-Free |

| Room Replacement | No (Lost Forever) | Yes (Following Year) |

| Retirement Impact | Can trigger OAS clawbacks | No impact on benefits |

Our Top 3 Picks and Why?

Of the points discussed, Withdrawal Flexibility, Tax Refund vs. Tax-Free Growth, and the $50,000 Income Threshold are the most critical. These three pillars allow you to tailor your savings to your current lifestyle while ensuring you don’t accidentally overpay the government or lose your ability to access your own money when you need it most.

Buyer’s Guide: How to Choose the Right RRSP vs TFSA 2025 Strategy by Yourself?

Developing a personal savings framework requires an honest assessment of your current career stage and your long-term retirement goals. Use the logic below to determine your starting point.

The Selection Framework:

-

Career Trajectory: Are you at your peak earning years or just starting? Peak earners should lean toward RRSPs.

-

Goal Horizon: Is this money for a house in 3 years or a beach in 30? Short-term goals belong in a TFSA.

-

Employer Matching: Always prioritise an RRSP if your employer offers a matching program—this is essentially a 100% immediate return on your investment.

Decision Matrix (Table):

| Choose RRSP if… | Choose TFSA if… |

| Your current income is over $100,000. | Your current income is under $50,000. |

| You have an employer-matching plan. | You need an emergency fund or a “down payment” fund. |

| You want to use the Home Buyers’ Plan (HBP). | You want tax-free passive income in retirement. |

The Final Checklist: 5-point Checklist Before Choosing Your Account

-

Have you confirmed your exact contribution room on your last CRA Notice of Assessment?

-

Are you currently in a higher tax bracket than you expect to be in retirement?

-

Do you have a high-interest debt that should be paid off before you start saving?

-

Are you planning to use the money for a first-home purchase (HBP) or lifelong learning (LLP)?

-

Have you accounted for provincial tax variations that might affect your total refund?

Maximising Your Canadian Wealth in 2026

The decision between an RRSP and a TFSA is rarely “all or nothing.” For most Canadians, the ideal strategy involves a balanced approach that uses the RRSP to lower current taxes and the TFSA to provide a tax-free cushion for the future. By staying informed about the 2025 limits and rules, you ensure that every dollar you save is working as hard as possible toward your ultimate financial independence.