As the Irish financial landscape enters mid-2026, the battle for the “digital generation” has moved beyond simple smartphone apps into a complex era of integrated financial ecosystems. While neobanks like Revolut and N26 once held a monopoly on seamless user experiences, Ireland’s credit unions have undergone a radical transformation. By leveraging new legislation and centralized fintech partnerships, these community-focused institutions are now offering the speed of a neobank with the trust and physical presence of a traditional lender.

How We Selected Our 7 Best Irish Credit Union Digital Generation Strategies 2026

To identify the most effective ways credit unions are closing the gap with neobanks this year, we analyzed market share data, the latest 2026 Q1 financial reports from the Irish League of Credit Unions (ILCU), and consumer sentiment surveys. Our criteria focused on features that directly address the pain points of Gen Z and Millennial users, such as instant payments and sustainable lending.

-

Digital Accessibility: The availability of mobile-first features like biometric login and digital wallet integration (Apple/Google Pay).

-

Speed of Service: The transition from manual “committee-based” lending to automated, in-app loan approvals.

-

Service Breadth: The ability to offer “big bank” products like mortgages and business loans at scale.

-

Competitive Pricing: Transparency in fee structures compared to the “freemium” models of digital-only banks.

The following metrics highlight the significant shift in credit union capabilities as of March 2026.

| Metric | 2021 Status | 2026 Status |

| Current Accounts | Limited (Selected CUs) | 80+ CUs (280+ Branches) |

| Digital Wallet Support | Experimental | Industry Standard |

| Mortgage Portfolio | €250 Million | €1 Billion (Projected Q2) |

| P2P Payments | Manual / Slow | Instant (Zippay Integration) |

The 7 Smartest Ways Irish Credit Unions Compete with Neobanks 2026

The current era of Irish credit unions is defined by a “digital-first, human-always” philosophy that leverages the 2023 Amendment Act to its full potential.

1. Integration into the Zippay Instant Payment Network

In early 2026, the Irish banking sector launched Zippay, a domestic account-to-account instant payment service designed to rival Revolut’s P2P features. While initially a “Pillar Bank” initiative, credit unions are now actively integrating into this Nexi-powered infrastructure. This allows members to send and split payments instantaneously using only a mobile number, effectively neutralizing one of the neobanks’ biggest competitive advantages.

Best for: Young users who want the “Revolut-style” speed of splitting dinner bills without leaving their primary credit union app.

Why We Chose It:

-

It eliminates the “top-up” friction required by neobanks, as money moves directly between IBANs.

-

It leverages a secure, domestic infrastructure that many users find more trustworthy than offshore fintechs.

-

It provides 24/7/365 instant liquidity for small-scale retail transfers.

Things to consider: Participation varies by individual credit union, so members should check if their specific branch has finalized the Nexi/Zippay onboarding.

2. Nationwide Member Referral (The “Section 26” Advantage)

Under Section 26 of the Credit Union (Amendment) Act 2023, credit unions in 2026 are now operating as a cohesive national network through a referral system. If a small, local credit union does not offer a specific digital product—like a mortgage or a full current account—they can now refer the member to a larger “receiving” credit union. This ensures that no member has to switch to a neobank simply because their local branch lacks a specific digital service.

Best for: Members in rural areas who want a personal local relationship but need access to high-tech urban banking products.

Why We Chose It:

-

It prevents “member churn” to neobanks by keeping the user within the credit union ecosystem.

-

It allows smaller branches to remain specialized while still offering a full suite of modern financial tools.

-

It fosters a spirit of collaboration that neobanks, as individual corporate entities, cannot replicate.

Things to consider: The referred member is only deemed a member of the second credit union for the specific service provided, keeping their primary loyalty local.

3. The Rise of “Greenify” and Ethical Lending Portfolios

The digital generation is increasingly motivated by ESG (Environmental, Social, and Governance) factors, and credit unions have responded with the “Greenify” transport and home loan suite. In 2026, these digital-native loan products offer preferential rates for EVs and retrofitting, with the entire application process handled via document upload in the app. This links the credit union’s “not-for-profit” status with the climate-conscious values of younger borrowers.

Best for: Environmentally conscious Gen Z and Millennials looking for lower-interest loans to fund sustainable lifestyle changes.

Why We Chose It:

-

It offers a “social dividend” that neobanks, focused on shareholder profit, often lack.

-

It provides specialized expertise in local SEAI grants that digital-only banks cannot offer.

-

It creates a “virtuous cycle” where local savings fund local environmental improvements.

Things to consider: These loans often require proof of purchase or energy certificates, which can be uploaded directly via the mobile app’s secure messaging feature.

4. “One-Touch” App-Based Mortgage Approvals

Reaching a historic €1 billion mortgage book in early 2026, credit unions have digitized the once-tedious home loan process. Using the 2026 versions of their mobile apps, members can now use Face ID to access their “Mortgage Hub,” upload payslips, and receive a preliminary “Decision in Principle” within 24 hours. By offering competitive fixed and variable rates that often undercut “legacy” banks and match neobank lending products, they are becoming a serious force in the housing market.

Best for: First-time buyers who want the efficiency of a digital application but the security of a “bricks-and-mortar” institution to visit if things go wrong.

Why We Chose It:

-

It combines the speed of neobank lending with the long-term stability of a regulated credit institution.

-

It uses automated “decisioning” engines to provide instant feedback on loan eligibility.

-

It specifically targets the “switcher” market for people tired of high rates at commercial banks.

Things to consider: While the digital application is fast, credit unions still maintain a “common sense” approach to underwriting that can be more flexible than neobank algorithms.

5. Biometric-First Security and PSD2 Compliance

The 2026 suite of credit union apps has fully embraced biometric security, moving away from the “8-digit PIN” era into a seamless Face ID and Touch ID environment. These apps are fully compliant with the latest PSD2 (and emerging PSD3) standards, allowing for “Open Banking” where members can see their other bank balances (like Revolut or AIB) from within the credit union dashboard. This “aggregator” view makes the credit union app the central hub for a user’s entire financial life.

Best for: Tech-savvy users who demand high security without the friction of remembering multiple passwords or carrying card readers.

Why We Chose It:

-

It levels the playing field with neobanks in terms of “app-snappiness” and user interface design.

-

It provides a secure environment for 24/7 account management and payee setup.

-

It includes built-in “One-Time Passcode” (OTP) generation for secure online shopping with the credit union debit card.

Things to consider: Users must ensure their mobile number is updated with the branch to receive the mandatory validation texts for initial app setup.

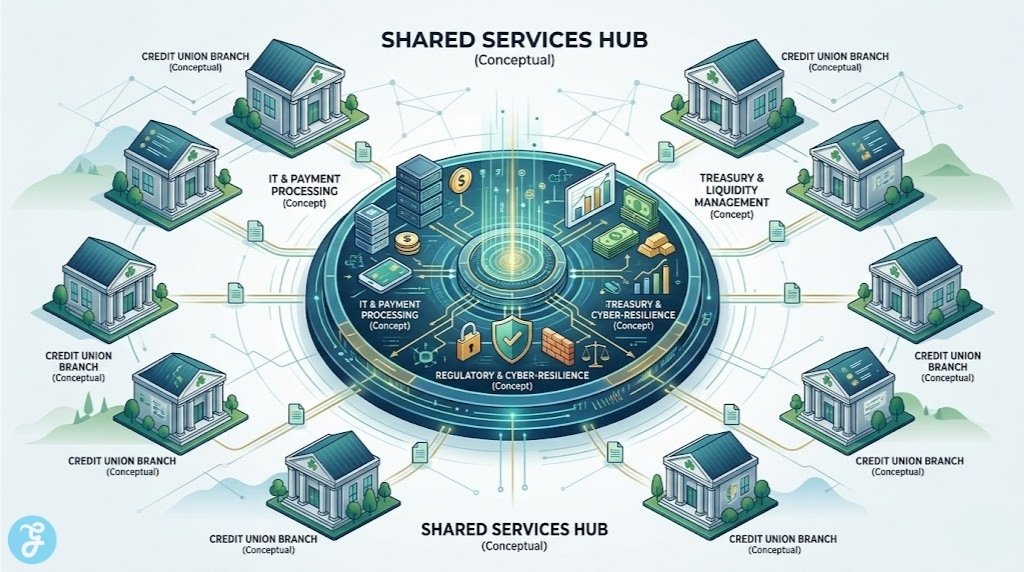

6. The Collaborative “Corporate Credit Union” Infrastructure

A major development in 2026 is the progress toward a “Corporate Credit Union“—a central hub designed to support shared services. By centralizing IT, treasury, and payment management, individual credit unions can now benefit from the economies of scale previously reserved for large neobanks. This backend transformation allows a small town credit union to offer a mobile app and debit card experience that feels as sophisticated as a multi-billion dollar fintech.

Best for: Ensuring that the digital experience remains high-quality and consistent regardless of the size of the local credit union.

Why We Chose It:

-

It reduces the “per-member” cost of technology, allowing CUs to maintain lower fees than many premium neobank tiers.

-

It provides a robust framework for cyber-resilience and operational stability.

-

It allows for the rapid rollout of new features, like Zippay, across the entire sector simultaneously.

Things to consider: This is a “behind-the-scenes” shift, but it is the engine that makes the front-end digital experience possible.

7. Human-Centred Digital Support (The 24/7 Hybrid)

While neobanks are notorious for “bot-only” customer support, Irish credit unions in 2026 have perfected a hybrid model. The app provides 24/7 automated support for basic tasks, but also features a “Call Back” or “Secure Message” button that connects the member to a real person in their local community. For the digital generation who has experienced the frustration of being “locked out” of a neobank account with no one to talk to, this human safety net is a major selling point.

Best for: Users who have been “burned” by the lack of customer service at digital-only banks and want a local point of contact.

Why We Chose It:

-

It solves the “account frozen” nightmare by providing a physical office where the member can show their ID in person.

-

It maintains the “community first” ethos while using digital tools to make that human connection more efficient.

-

It offers a level of empathy and personalized advice that an AI chatbot cannot replicate.

Things to consider: The hybrid model is most effective during branch hours, though 24/7 support for lost or stolen cards remains a standard feature.

An Overview Of the Irish Credit Union Digital Generation vs Neobank Market

The gap between community lending and high-tech fintech has narrowed significantly, with each offering distinct advantages depending on the user’s life stage.

Overview Comparison Table

The following comparison outlines the key differences in how these two financial models serve the Irish market in mid-2026.

| Feature | Irish Credit Unions (2026) | Neobanks (Revolut/N26) |

| Instant Payments | Yes (via Zippay integration) | Yes (In-network instant) |

| Physical Presence | 280+ Locations (Human Support) | None (Digital Only) |

| Lending Limits | High (Mortgages/Business) | Moderate (Personal/Credit Cards) |

| Ownership Model | Member-Owned (Not-for-Profit) | Venture/Shareholder-Owned |

| Ethical Impact | High (€8m Community Funding) | Low (Focus on Scale/Profit) |

| Account Fees | Low/Transparent | Freemium (High for Premium) |

Our Top 3 Picks and Why?

Of the strategies listed, Zippay Integration, Section 26 Referrals, and App-Based Mortgages are the most transformative. Zippay finally gives credit unions the “cool factor” of instant transfers. The referral system turns hundreds of independent branches into a powerful national bank. Finally, the move into mortgages proves that credit unions are no longer just for “small loans,” making them a lifetime financial partner for the digital generation.

How to Choose the Right Irish Credit Union Digital Generation Support by Yourself?

Not all credit unions have reached the same level of digital maturity, so it is important to audit your local branch before committing.

The Selection Framework:

-

Check for Digital Wallet Support: Ensure the branch supports Apple Pay and Google Pay if you prefer a phone-only wallet.

-

Verify Current Account Status: Look for the “Mastercard” logo on their website, which indicates they offer a full, modern current account.

-

Test the App UX: Many CUs offer a “demo” or screenshots of their new app; look for Face ID and Touch ID compatibility.

-

Inquire about Zippay: Ask if the branch is live on the Zippay P2P network for instant mobile transfers.

Decision Matrix:

The matrix below helps you decide which model fits your current financial priorities.

| Choose a Credit Union if… | Choose a Neobank if… |

| You want a mortgage or large business loan. | You primarily need a travel card for currency exchange. |

| You value local community reinvestment (ESG). | You want to trade crypto or stocks in a single app. |

| You want a human to talk to if your card is lost. | You want the absolute lowest “base” fee for simple tasks. |

The Final Checklist

-

Is my local credit union part of the 80+ branches offering the Full Current Account?

-

Does the mobile app allow for Digital Document Uploads for loan applications?

-

Can I use Apple Pay or Google Pay with my credit union debit card today?

-

Is the branch part of the Zippay network for splitting bills with friends?

-

Have I reviewed the 2026 Community Impact Report to see where my interest payments go?

Bridging the Divide: The Hybrid Future of Irish Banking

The narrative that credit unions are “behind the times” has been officially debunked by the reality of 2026. By merging the legislative power of the 2023 Amendment Act with an aggressive fintech roadmap, Irish credit unions have created a hybrid model that neobanks cannot easily copy. They have become “fintechs with a heart,” offering the digital generation a way to bank at the speed of light while keeping their money rooted in their local community. As neobanks begin to introduce more fees and struggle with human customer service, the credit union’s “member-first” digital transformation is looking like the smartest bet for the future of Irish finance.