Artificial intelligence is completely changing how we work. A few years ago, it was just a popular buzzword thrown around in boardrooms. Today, it sits at the absolute core of British finance, retail, and daily operations. Companies are rushing to deploy these powerful tools to save time, reduce human error, and make more money. But you cannot simply plug an open-source language model into your customer database and hope for the best.

Regulators are watching every move very closely. Understanding the FCA guidelines on generative AI for UK businesses is now a top priority for company directors across the country. The Financial Conduct Authority takes a firm but highly flexible approach. They desperately want to encourage technological innovation in London and beyond. At the exact same time, they demand total safety and transparency for the end consumer. We spent time looking at how real companies are managing this delicate balancing act. The facts show a massive shift in how businesses handle risk, compliance, and growth.

| AI Landscape Element | Current Status in 2026 |

| Overall Adoption | Rapidly scaling across all financial sectors |

| Regulatory Approach | Principles-based and outcomes-focused |

| Main Business Goal | Operational efficiency and cost reduction |

| Primary Challenge | Managing third-party vendor risks |

1: 75% of UK Financial Firms Are Already Using AI

The numbers speak for themselves when you look at current market data. Most financial firms in the UK have completely moved past the initial testing and sandbox phases. They use artificial intelligence daily to run their core business processes. If a company is not using these tools right now, they are actively falling behind their competitors and losing market share. Adoption rates jumped massively over the last three years, surprising even the most optimistic tech analysts.

Banks and insurance companies lead the pack because they handle massive volumes of paperwork. They use advanced algorithms to sort through giant piles of data faster than any human team ever could. This is not just about replacing simple tasks anymore. It is about fundamentally rewiring how a financial institution operates from the ground up.

| Metric | Data Point |

| Financial Firms Using AI | 75% |

| Firms Planning to Use AI Soon | 10% |

| Leading Sectors | Insurance and International Banking |

| Main Internal Use Cases | IT, Operations, Retail Banking |

The Data Behind the Surge

Recent reports from the Bank of England paint a very clear picture of this technological shift. Three out of four financial businesses now rely heavily on machine learning models. They use it to detect credit card fraud in milliseconds. They use it to price complex insurance premiums based on thousands of variables. They use it to manage overwhelming customer service requests during peak hours. This is a huge leap from just a few years ago when only about half of firms used AI for basic analytics.

The speed of this change is staggering and forces regulators to pay close attention. Companies saw the sheer potential of large language models and invested heavily to secure their future. Now, these tools are simply part of the normal daily software stack for employees. Workers expect to have smart digital assistants to help them draft sensitive emails, write complex code, or summarize long compliance documents.

2: The FCA Has Rejected AI-Specific Red Tape

You might naturally think the government would panic and write hundreds of new laws just for artificial intelligence. That is exactly what did not happen here in the UK. The FCA looked at their massive existing rulebook and decided it was already strong enough to handle the challenge. They specifically chose not to create a brand new, highly restrictive set of rules just for generative models. Instead, they actively apply existing regulatory standards to this new technology.

This means companies do not have to waste time learning a completely new compliance language from scratch. They just have to map their AI tools to the rules they already follow. This prevents the industry from drowning in unnecessary paperwork while still protecting the public.

| Regulatory Framework | Core Purpose Regarding AI |

| Consumer Duty | Ensures AI products provide fair value to customers |

| SM&CR | Makes senior managers personally accountable for AI |

| Data Protection (ICO) | Protects consumer data fed into AI models |

| Operational Resilience | Ensures firms can survive AI vendor outages |

A Principles-Based Approach

The authority strictly focuses on final outcomes rather than the specific technology used. They do not care if a human or a computer makes a terrible mistake. A mistake is a mistake, and the firm must answer for it. The Consumer Duty rules clearly state that businesses must support their customers and offer fair value. If an AI chatbot gives a retail investor bad financial advice, the company is entirely responsible for the financial damage. The Senior Managers and Certification Regime plays a massive role in this regulatory strategy.

Under these specific rules, a named human executive must take ultimate responsibility for the AI systems. If an algorithm illegally discriminates against a minority customer, the FCA will hold that specific executive personally accountable. This harsh reality forces companies to be extremely careful about testing their models extensively before launching them to the public.

3: Foundation Models Make Up 17% of AI Use Cases

Generative AI is no longer treated as a fun, small experiment for the IT department. These massive foundation models now represent a huge and growing chunk of all AI activity in the business world. We are talking about the highly advanced systems that can write, code, analyze, and reason almost exactly like a highly educated person. They are rapidly moving out of the back office and into every single corner of the corporate structure.

Companies use them to read complex financial histories and write personalized investment summaries. This represents a major shift in how the UK economy operates. Businesses are moving away from simple prediction tools and fully embracing cognitive automation.

| AI Type | Percentage of Use Cases | Primary Function |

| Traditional Machine Learning | 83% | Predictive analytics, sorting, fraud detection |

| Foundation Models (Generative) | 17% | Text creation, summarization, complex coding |

The Shift Toward Complex Machine Learning

This seventeen percent figure is highly significant for the future of work. It shows a definitive move from basic robotic automation to real, thinking cognitive assistance. Legal teams use foundation models to scan massive merger contracts for hidden errors and liabilities. Human resources departments use them to instantly draft company policies that comply with new employment laws. But with this incredible complexity comes a massive amount of hidden risk.

The FCA expects companies to fully understand exactly how these models reach their conclusions. You cannot just use a tool because it looks magical and saves time. If a generative model hallucinates and makes up a fake law to justify a denied loan, the business takes the full blame. Companies have to build strict testing frameworks to catch these algorithmic hallucinations before they ever reach a paying client.

4: Third-Party AI Dependency is the New Systemic Risk

Building a good language model from scratch costs billions of pounds and requires massive computing power. Most normal businesses absolutely cannot afford that kind of investment. So, they rent the technology from massive American tech companies through cloud subscriptions. This creates a deeply hidden and terrifying danger for the UK economy.

If every single major bank relies on the exact same three tech giants for their AI, what happens if one of them breaks down? Regulators are incredibly worried about this single point of failure. It is no longer just about one bank failing. It is about the entire financial system grinding to a halt because a server farm in California lost power.

| Risk Factor | Description |

| Concentration Risk | Too many banks using the exact same AI provider |

| Outage Impact | An AI server crash halting UK financial operations |

| Data Security | Sensitive client info leaking through third-party models |

| Vendor Lock-in | Difficulty switching AI providers due to integrated systems |

The Danger of Outsourcing to Big Tech

The Bank of England and the FCA view this concentration as a major, urgent threat to the national economy. Imagine a scenario where five major UK banks use the exact same external AI vendor for their real-time fraud detection. If that specific vendor suffers a sophisticated cyberattack, all five banks are completely vulnerable at exactly the same time. Millions of accounts could be compromised instantly.

To meet the FCA guidelines on generative AI for UK businesses, firms have to legally prove they can survive a massive AI blackout. They must aggressively stress-test their operational resilience systems. They need expensive backup plans and redundant systems. If the AI goes down completely, they need to know exactly how to switch back to human workers without crashing their entire daily operation.

5: Tangible ROI is Finally Here for Early Adopters

The initial media hype is finally turning into hard, measurable cash for smart companies. For a long time, companies spent millions on AI pilot programs without seeing any real financial return. That era is officially over. The companies that jumped in early and set up good, safe governance structures are making significantly more money.

They are doing things much faster and noticeably cheaper than their slower rivals. Employees are spending less time on incredibly boring administrative tasks and more time on actual, high-value problem-solving. This proves that artificial intelligence is a true business multiplier when deployed correctly.

| ROI Indicator | Percentage of Firms Reporting Benefit |

| Increased Overall Productivity | 87% |

| Direct Profit Increases | 48% |

| Profit Uplifts of 11% or More | 22% |

| Reduced Operational Costs | 65% |

The Profitability Factor

Recent industry survey data shows that almost nine out of ten companies using AI see a massive boost in worker productivity. Even more impressively, half of them are seeing actual, measurable profit increases tied directly to their AI software investments. When you deploy generative AI correctly, it gives you a massive, sometimes unfair competitive advantage. You can serve frustrated customers infinitely faster.

You can process complex insurance claims in minutes instead of weeks. However, the FCA is very quick to remind everyone that chasing profits cannot ever hurt the consumer. Pushing for ruthless efficiency is great for the bottom line, but treating the customer fairly is a strict legal requirement. Businesses must prove their cost-cutting algorithms do not accidentally penalize vulnerable people.

6: The Consumer Trust Gap is Widening

Regular people are getting very nervous about all of this. While bank executives celebrate their shiny new AI tools and cost savings, regular consumers are deeply worried about their data privacy and their hard-earned money. Many people simply do not trust a faceless computer program to make important financial decisions for them.

They find the incredible speed of this technology deeply unsettling and opaque. This creates a massive, structural problem for businesses that rely heavily on consumer trust to survive. If the public revolts against AI banking, the technology becomes a liability rather than an asset.

| Consumer Sentiment | Percentage |

| High Anxiety About Financial AI | 50% |

| Zero Trust in Generative AI Models | 33% |

| Prefer Human Interaction for Banking | 72% |

| Want Clear Labeling of AI Content | 89% |

Education Must Match Innovation

This growing gap in public trust is a very serious compliance issue for every firm. The Consumer Duty legally requires firms to communicate clearly and honestly with the public. If you use a secret algorithm to decide if a young family gets a mortgage, you have to be able to explain that math to them in plain English. Consumers absolutely need to know when they are talking to a bot and when they are talking to a real human being.

If a customer feels tricked or manipulated by a smart AI system, they will immediately complain to the Financial Ombudsman. Businesses must spend exactly as much time and money educating their customers as they do building their complex algorithms. Total transparency is the only way to close this dangerous trust gap.

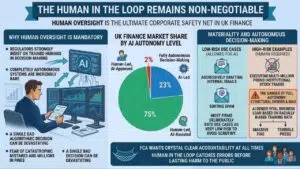

7: The Human in the Loop Remains Non-Negotiable

We are definitely not living in a science fiction movie just yet. Artificial intelligence absolutely does not run the company on its own while the humans sleep. Regulators strongly insist that trained humans stay deeply involved in the decision-making process. Completely autonomous, unsupervised AI systems are incredibly rare in the UK financial sector right now.

Businesses are simply too terrified of making a catastrophic regulatory mistake to let the computer take the wheel entirely. They know that a single bad algorithmic decision could lead to millions in fines. Therefore, human oversight acts as the ultimate corporate safety net.

| AI Autonomy Level | Current UK Market Share |

| Human-Led, AI-Assisted | 75% |

| AI-Led, Human-Approved | 23% |

| Fully Autonomous Decision-Making | 2% |

Materiality and Autonomous Decision-Making

Currently, only about two percent of AI applications in UK finance run without a human double-checking the final work. Most firms deliberately rate their AI use cases as very low risk to avoid regulatory scrutiny. They use it to aggressively draft internal emails or sort spam, not to execute multi-million pound institutional stock trades autonomously. This extreme caution aligns perfectly with what the FCA wants to see from the market.

They want crystal clear human accountability at all times. If an autonomous AI system denies a vital business loan based on racially biased training data, the company gets a massive fine and terrible press. Keeping a smart human in the loop is the absolute best way to catch these structural errors before they cause real, lasting harm to the public. It is a mandatory safety net.

8: The UK Strategy Drastically Differs from the EU AI Act

If you run a financial business with offices in both London and Paris, you have a massive headache right now. The European Union recently passed a huge, incredibly strict law to aggressively control artificial intelligence. The UK government deliberately went in the exact opposite direction. The British government desperately wants to attract global tech companies to London, so they chose a much lighter, highly flexible regulatory approach.

This severe difference creates a deeply confusing legal landscape for international companies trying to operate across borders. They have to build entirely different compliance systems depending on which side of the English Channel they are standing on.

| Feature | UK Approach | EU AI Act Approach |

| Legislative Style | Principles-based, sector-specific | Prescriptive, universal regulation |

| Risk Categorization | Flexible, outcome-focused | Rigid risk tiers |

| Regulator | Existing bodies | New centralized AI offices |

| Focus | Innovation and economic growth | Strict compliance and safety documentation |

Innovation Over Prescriptive Categorization

The European Union strictly categorizes every single AI system by risk level. If a system is legally deemed high risk, the company must fill out absolute mountains of paperwork before they can even turn it on. Some controversial systems are banned completely across Europe. The UK framework is vastly different because it is based on simple, flexible principles like transparency and fairness. Regulators apply these broad principles to their own specific sectors as they see fit.

This allows British tech companies to move much faster than their European rivals. They can freely experiment with brand new generative models without waiting six months for a government approval stamp. But they still carry the heavy burden of proving their systems are completely safe for the end user.

9: SMEs Are Democratizing AI Adoption

Generative AI is absolutely not a luxury item reserved just for massive multinational banks anymore. Small businesses are aggressively jumping on board every single day. A local high street accounting firm or an independent mortgage broker can now easily access the exact same powerful language models as a global investment bank.

They do not have to build it themselves; they just pay a small monthly subscription fee to a cloud provider. This completely levels the playing field and allows small firms to punch way above their weight. They can process documents and handle customer queries with the speed of a massive corporation.

| Business Size | AI Adoption Rate | Primary AI Access Method |

| Large Enterprises | 85%+ | Enterprise APIs, Custom deployments |

| Medium Enterprises | 60% | Embedded software features, APIs |

| Small Businesses | 40% | Off-the-shelf software, SaaS tools |

Beyond the Banking Giants

Nearly forty percent of small and medium businesses in the UK actively use smart AI tools today. They definitely do not hire expensive machine learning engineers or data scientists. They just buy basic office software that already has artificial intelligence secretly built into it. This presents a very unique and difficult challenge for national regulators. Small firm owners often do not even realize they are technically using artificial intelligence.

If a small financial advisor uses a smart software plugin to quickly summarize a client portfolio, they are actively deploying AI. The FCA strongly expects even the smallest, one-person firms to deeply understand the technology they rely on and to vigorously protect their clients’ private data. Ignorance of the software is not a valid legal defense.

10: The FCA is Already Preparing for 2030 and Agentic AI

The underlying technology keeps moving at a blistering pace, and the regulators are desperately trying to look ahead to the future. They fully know that today’s impressive text chatbots will look incredibly primitive in just a few short years. The next massive wave hitting the market is agentic AI.

These are highly advanced systems that can make long-term plans and execute complex tasks over several days without ever asking a human for help. The FCA is already heavily studying exactly how this will fundamentally change the global economy. They are preparing the rules today for the software that will exist tomorrow.

| Future Tech Trend | Regulatory Concern |

| Agentic AI | Lack of direct human control over complex workflows |

| Big Tech Dominance | Tech giants pushing out traditional financial firms |

| Hyper-Personalization | Pricing models that unfairly target vulnerable people |

| Deepfakes in Fraud | Advanced voice and video cloning bypassing security |

The Mills Review and Future Readiness

The FCA is aggressively conducting deep market reviews to prepare for the reality of the year 2030. They urgently want to know what happens when autonomous AI agents start actively negotiating financial contracts with other AI agents in milliseconds. Will traditional high street banks lose all their market power to giant, faceless tech platforms? Businesses absolutely need to build internal compliance systems that can adapt to these wild future scenarios.

The core rules of fairness might not change, but the way regulators enforce them certainly will. A rigid, old-fashioned compliance checklist will fail completely. Companies desperately need a flexible, highly educated governance culture that deeply understands how this technology works.

Why This Matters for the Future of UK Business?

You simply cannot ignore this massive technological shift and hope it goes away. The forward-thinking companies that figure out how to safely deploy these tools will completely dominate their respective markets over the next decade. Those stubborn firms that ignore the technology or fail to govern it properly will simply disappear into bankruptcy. It really is that simple and brutal. This is an adapt or die moment for the British economy.

| Business Action | Expected Outcome |

| Ignore AI completely | Loss of competitive edge, higher operational costs |

| Deploy AI recklessly | Massive regulatory fines, loss of consumer trust |

| Strategic deployment | Sustainable growth, high ROI, regulator approval |

Striking the Balance Between Growth and Compliance

This entire conversation brings us right back to the core operational issue facing directors. Deeply understanding the FCA guidelines on generative AI for UK businesses is the only safe and profitable way forward. You have to aggressively push for operational efficiency while keeping an incredibly tight grip on risk management protocols. You must ensure consumer data is locked down and totally safe from hackers. You must mathematically ensure your models are fair and unbiased.

Smart firms view the regulator as a helpful partner, not a hostile enemy to be avoided. The FCA’s principles-based approach actually gives you the incredible freedom to innovate rapidly. As long as you maintain clear human oversight and always prioritize the customer, this technology will be the best thing to ever happen to your business.

Final Thoughts

The rapid, unstoppable rise of artificial intelligence is undeniably the biggest structural shift the British corporate world has seen in a generation. Adopting these advanced tools is absolutely no longer a fun luxury; it is a basic, fundamental requirement for staying relevant in the modern economy. However, as we have seen through the data, deploying this technology safely requires incredibly careful planning and a deep, unwavering respect for consumer rights. By closely following the FCA guidelines on generative AI for UK businesses, you actively protect your firm from severe financial fines and devastating reputational damage.

More importantly, you build a highly sustainable foundation for long-term, explosive growth. The technology will continue to advance rapidly, moving toward fully autonomous agents in the coming years. Keep a smart human in the loop at all times, prioritize data security above everything else, and always put the customer’s best financial interests first.