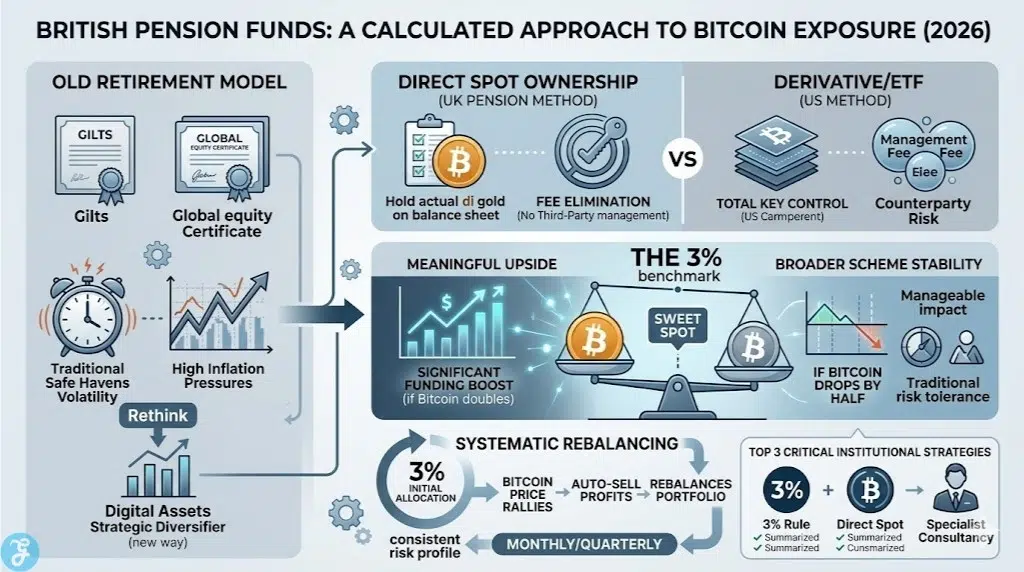

The British retirement landscape is shifting toward digital assets as traditional safe havens face new economic pressures. For decades, pension trustees in the United Kingdom focused exclusively on gilts and global equities, but the high volatility of the current market has forced a rethink.

We are seeing a historic move where defined benefit schemes are now integrating Bitcoin as a strategic diversifier rather than a speculative bet. This transition represents a major milestone in the journey toward the institutionalization of crypto assets across the country.

How We Selected Our 7 Best Bitcoin Exposure Strategies

To determine the most impactful ways British pension funds are approaching the digital market, we analyzed the latest regulatory filings and consultancy reports from early 2026.

We filtered our selection based on three core criteria. First, we prioritized strategies that have already been implemented by active UK pension trusts. Second, we evaluated the level of regulatory compliance with the Financial Conduct Authority and the Pension Regulator. Third, we looked at the long term risk management frameworks used by specialist investment consultants to protect member benefits.

The Top 7 Trends in British pension Bitcoin exposure

Understanding how these conservative institutions are moving into the crypto space reveals a very calculated and cautious approach. Here are the seven most surprising facts about how British pension funds are managing their digital allocations today.

1. Direct Asset Ownership Over ETF Wrappers

While many American funds prefer exchange traded funds, the pioneering British pension funds have chosen to hold Bitcoin directly. This approach involves owning the underlying asset on their own balance sheet rather than holding a derivative or a share in a fund. By doing this, trustees eliminate the management fees associated with large fund providers. It also allows the pension scheme to maintain total control over the private keys through specialized institutional custody providers.

Best Feature/For:

-

Large defined benefit schemes with long investment horizons

Why We Chose It:

-

Eliminates recurring annual management fees from third party fund issuers

-

Reduces counterparty risk by holding the actual digital commodity

-

Provides greater transparency for annual auditing and reporting requirements

Things to consider:

-

Requires a much higher level of technical due diligence on custody partners

Moving from the method of ownership, we must also consider the specific size of these initial allocations.

2. The Emergence of the Three Percent Benchmark

Institutional investors in the UK are coalescing around a very specific initial allocation size of three percent. This number is seen as the “sweet spot” where the asset can provide meaningful upside without jeopardizing the stability of the broader portfolio. If Bitcoin doubles in value, a three percent position adds a significant boost to the total scheme funding level. However, if the price drops by half, the impact on the overall pension pot remains manageable within traditional risk tolerances.

Best Feature/For:

-

Risk averse trustees looking for asymmetric growth opportunities

Why We Chose It:

-

Balances high potential returns with strict capital preservation goals

-

Limits the overall portfolio volatility increase to just a few percentage points

-

Provides a clear framework for rebalancing and taking profits systematically

Things to consider:

-

Small allocations still require the same level of legal and regulatory oversight

Beyond the size of the trade, the motivation for these investments has shifted toward a hedge against inflation.

3. Bitcoin as a Gilt Alternative for Monetary Hedging

The historic volatility of UK government bonds, known as gilts, has led trustees to look for non sovereign alternatives. Many consultants now argue that Bitcoin serves as a modern version of gold that sits entirely outside the traditional banking system. Because it has a fixed supply of twenty one million coins, it is being used to protect against the long term debasement of the British Pound. This marks a radical departure from the old view that government bonds were the only truly risk free assets.

Best Feature/For:

-

Schemes concerned about long term currency devaluation and sovereign debt

Why We Chose It:

-

Offers a hard cap on supply that central banks cannot manipulate

-

Functions as a store of value that is independent of UK fiscal policy

-

Diversifies the portfolio away from heavy reliance on the bond market

Things to consider:

-

Short term price swings can still be much more aggressive than bond movements

The implementation of these strategies relies on a new breed of specialized investment consultants.

4. The Rise of Specialist Bitcoin Pension Consultants

Traditional investment firms were slow to embrace crypto, leading to the rise of specialized boutique advisers like Cartwright. These firms provide the deep technical training and due diligence frameworks that pension trustees need to feel comfortable. They handle everything from choosing a regulated exchange to setting up multi signature custody arrangements. This specialized support has been the primary catalyst for the first wave of UK pension fund entries into the market.

Best Feature/For:

-

Trustee boards that lack internal expertise in digital asset management

Why We Chose It:

-

Provides independent due diligence that satisfies fiduciary duties

-

Educates trustees on the difference between speculation and strategic allocation

-

Manages the complex relationship between crypto exchanges and traditional banks

Things to consider:

-

Boutique advisory fees can be higher than standard consultancy rates

Regulatory clarity has also played a massive role in making these investments possible for retail and institutional savers alike.

5. Inclusion in Tax Advantaged Pension Wrappers

As of late 2025 and early 2026, the UK government has officially allowed cryptoasset exchange traded notes to be held in registered pension schemes. This means that individual savers can now gain exposure through their Self-Sourced Account or other personal pension vehicles. These products are now treated with the same tax advantages as traditional stocks and shares within a pension pot. This regulatory green light has removed the final legal hurdles for millions of UK workers looking to diversify their retirement savings.

Best Feature/For:

-

Individual savers and small business owners with self managed pensions

Why We Chose It:

-

Simplifies the tax reporting process for digital asset gains

-

Allows for compounding growth within a tax free or tax deferred environment

-

Standardizes the regulatory oversight through the Financial Conduct Authority

Things to consider:

-

Not all pension providers have updated their platforms to support these new assets

One of the most surprising technical details is how these funds handle the timing of their trades.

6. Profit Trimming and Systematic Rebalancing

British pension funds are not “holding forever” in the way many retail investors do. Instead, they use strict rebalancing frameworks that automatically sell a portion of the Bitcoin position when it hits a certain percentage of the total portfolio. If the three percent allocation grows to five percent because of a price rally, the trustee automatically sells the excess to buy more traditional assets. This mechanical approach removes the emotional stress of trading and ensures that the fund lock in gains during market peaks.

Best Feature/For:

-

Maintaining a consistent risk profile over a multi year period

Why We Chose It:

-

Forces the fund to sell high and buy low on a consistent basis

-

Prevents the digital asset from becoming an outsized risk to the scheme

-

Provides a predictable stream of cash that can be used for member payouts

Things to consider:

-

Excessive rebalancing can lead to higher transaction costs over time

Finally, we are seeing a surprising level of collaboration between pension funds and renewable energy projects.

7. Integration with Tokenized Renewable Infrastructure

In 2026, some of the most innovative UK master trusts are exploring how to combine Bitcoin exposure with green energy investments. Through tokenized renewable asset coalitions, pension funds are looking at using blockchain technology to fund wind and solar projects. This allows them to meet their ESG goals while utilizing the same digital infrastructure used for their Bitcoin holdings. It creates a virtuous cycle where digital finance helps fund the physical transition to a net zero economy.

Best Feature/For:

-

Master trusts focused on meeting strict environmental and social governance goals

Why We Chose It:

-

Connects digital innovation with tangible real world infrastructure

-

Lowers the operational complexity of investing in private energy markets

-

Enhances liquidity for assets that are traditionally difficult to sell

Things to consider:

-

Tokenization of physical assets is still an emerging and complex field

To see how these different trends and strategies compare, let us look at the high level data across the industry.

An Overview Of 7 British pension Bitcoin exposure Trends

The shift toward digital assets in the UK pension sector is driven by a mix of technological curiosity and economic necessity. We have summarized the landscape to show how these different moving parts work together.

Overview Comparison Table

Below is a breakdown of the key metrics and strategies currently defining the British retirement market for Bitcoin.

| Strategy Component | Primary Goal | Target Group | Estimated Allocation |

| Direct Spot Allocation | Fee reduction and control | Defined Benefit Trusts | 1% to 3% |

| Crypto ETN Inclusion | Tax efficiency and ease | Individual Pension Savers | Varies |

| Systematic Rebalancing | Volatility management | Institutional Trustees | Monthly/Quarterly |

| Specialized Consultancy | Fiduciary compliance | Small to Mid Size Funds | Project Based |

| Renewable Tokenization | ESG and infrastructure | Large Master Trusts | Emerging |

While all of these trends are significant, a few specific strategies are clearly leading the way for the rest of the industry.

Our Top 3 Picks and Why?

After reviewing the current market activity, we have identified the three most important trends for the future of British pensions.

-

The Three Percent Allocation Rule: This takes our top spot because it provides a realistic and safe blueprint for thousands of other conservative funds to follow without blowing up their risk profiles.

-

Direct Asset Ownership: We rank this second as it sets a higher standard for security and fee transparency compared to the fund products used in the United States.

-

Specialist Bitcoin Consultancy: This is our third pick because the move into crypto is impossible for traditional trusts without the “hand holding” provided by these new expert firms.

Now that we have looked at the institutional side, you need to understand how to evaluate these options for your own retirement planning.

Buyer’s Guide: How to Choose the Right British pension Bitcoin exposure by Yourself?

If you are looking to add digital assets to your own UK pension, you need to be extremely careful about the providers and products you choose. The market is full of different options that carry very different levels of risk and cost.

Here is the core selection framework you should use when evaluating your options:

-

Regulatory Status: Only use platforms and products that are explicitly registered with the Financial Conduct Authority for crypto activities.

-

Fee Structure: Compare the total cost of ownership, including trading spreads, custody fees, and the annual management charge of the pension provider.

-

Security Model: Look for providers that use institutional grade “cold storage” and offer multi factor authentication for all account changes.

-

Liquidity Access: Ensure you can sell your holdings and move back into cash or traditional assets within a single business day.

To make this decision process easier, we have created a matrix to help you match your needs to the right pension setup.

Below is a decision matrix to help you choose the best path for your personal retirement strategy.

| Choose this strategy… | If your primary retirement situation is… |

| Choose a SIPPs Provider with ETNs if… | You want a hands off approach using familiar stock market instruments. |

| Choose a Specialist Crypto Pension if… | You want to hold the actual Bitcoin and have direct control over your keys. |

| Choose a Balanced Master Trust if… | You want a professional manager to handle the rebalancing and risk for you. |

| Choose an ESG Focused Fund if… | You want your digital exposure to be offset by investments in green energy. |

Before you make any changes to your long term savings, you should go through this final preparation list.

The Final Checklist:

-

Review your existing pension trust deed to see if digital assets are already a permitted investment.

-

Compare the management fees of at least three different FCA registered pension providers.

-

Calculate how a three percent allocation would change your total portfolio volatility.

-

Consult with a qualified financial adviser who has specific experience in the UK crypto regime.

-

Document your investment rationale to ensure you are not acting on short term market hype.

Modernizing the British Retirement Model

The integration of Bitcoin into the UK pension system is a clear sign that digital assets have reached a new level of maturity. By moving away from pure speculation and toward disciplined portfolio construction, British funds are showing the rest of the world how to modernize a conservative industry. Whether you are a trustee for a large scheme or an individual saver, staying informed about these institutional trends is the best way to secure your financial future in 2026.