The 2025 tax season marked a historic shift in American green energy policy, characterized by the unexpected sunsetting of several long-standing incentives. While the original Inflation Reduction Act (IRA) was intended to last until 2032, the legislative landscape shifted dramatically in mid-2025, leaving many taxpayers confused about what was actually claimable on their current 2026 filings.

How We Selected Our 7 Insights on US EV Tax Credit 2025 Eligibility

To provide the most accurate guidance for the current filing period, we reviewed the final 2025 IRS Form 8936 instructions and the specific termination clauses introduced by the One Big Beautiful Bill (OBBB) Act. Our selection focuses on the “hidden” technicalities that determined whether a purchase actually qualified during that chaotic transition period.

-

Legislative Timing: We prioritized the impact of the September 30, 2025, early termination date.

-

Compliance Rigor: We analyzed the “Foreign Entity of Concern” (FEOC) rules that disqualified several popular models overnight.

-

Financial Risk: We looked at the specific income “clawback” provisions that surprised many high-earning filers.

The following criteria were essential in determining which 2025 rules had the most significant impact on taxpayer eligibility.

| Eligibility Factor | Priority Level | Strategic Impact |

| Acquisition Date | High | Determines if the Sept 30 cutoff applies |

| FEOC Sourcing | High | Disqualifies vehicles with prohibited minerals |

| MSRP Caps | Medium | Limits eligibility based on vehicle type |

| AGI Thresholds | Medium | Restricts credit based on buyer income |

7 Essential Facts: US EV Tax Credit 2025 Eligibility

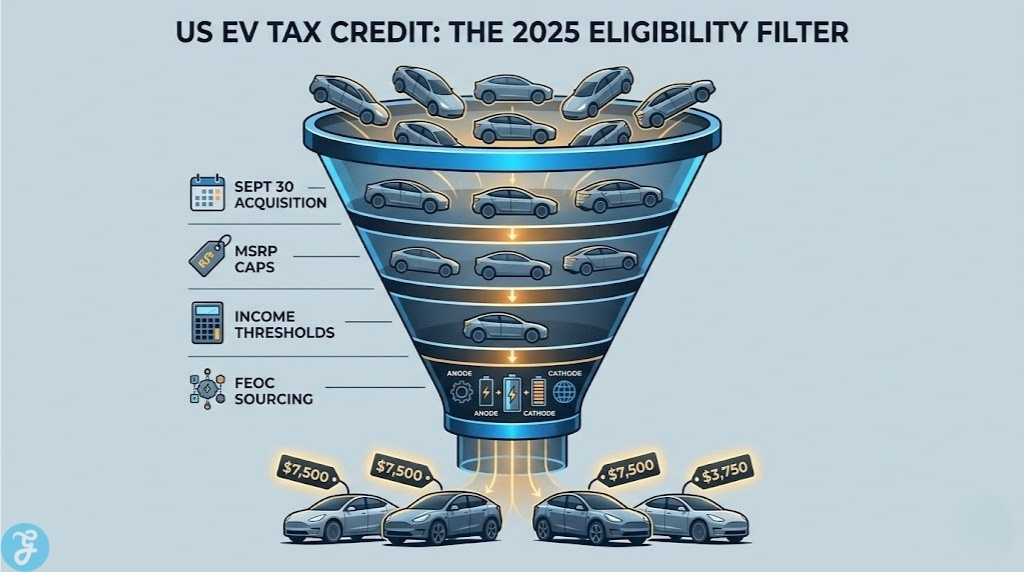

Navigating the 2025 rules requires looking beyond the basic $7,500 headline. These seven insights explain the technical hurdles that defined the final year of the original federal EV incentive program.

1. The September 30 “Hard Cutoff”

Most taxpayers assumed the 2025 credit would run until the end of the calendar year, but the OBBB Act effectively ended the program for any vehicle acquired after September 30, 2025. This three-month “lost window” caused a massive surge in Q3 sales and left many October buyers without the expected federal support. For eligibility purposes, the date you took title is the only date the IRS recognizes.

Best for: Filers who purchased their vehicles in late summer or early autumn of 2025.

Why We Chose It: This is the most significant legislative change that overrode the original 2032 expiration date.

Things to consider: If you purchased in October 2025, you are generally ineligible for the federal credit, regardless of the vehicle’s manufacturing.

2. The “Acquisition” vs. “Delivery” Loophole

A common point of confusion is the difference between when you signed for the car and when it arrived in your driveway. Eligibility for the 2025 credit was tied to the “acquisition” date, defined as having a binding written contract and having made a payment. If you signed a binding contract on September 28 but didn’t receive the car until November, you are still eligible for the credit under the 2025 rules.

Best for: Buyers who faced long dealership wait times or manufacturing delays.

Why We Chose It: It provided a vital safety net for consumers who committed to an EV before the surprise legislative sunset.

Things to consider: You must be able to produce the binding purchase agreement if audited, as the delivery date on the VIN report may raise a red flag.

3. The 60% Mineral Sourcing Jump

In 2025, the percentage of critical minerals required to be extracted or processed in the US (or free-trade partners) jumped from 50% to 60%. This was a “stealth” disqualifier for several vehicles that were eligible in 2024 but failed to update their supply chains in time for the 2025 tax year. This halved the available credit for many popular models, dropping them from $7,500 to $3,750.

Best for: New EV buyers who only received half of the expected tax credit at the point of sale.

Why We Chose It: It explains the technical reason why many “all-American” cars suddenly lost half their credit value in 2025.

Things to consider: Check your specific VIN on the Department of Energy’s 2025 list to see which half of the credit your vehicle qualified for.

4. The Foreign Entity of Concern (FEOC) Lockdown

As of January 2025, any vehicle containing battery components manufactured or assembled by a “Foreign Entity of Concern” (primarily China, Russia, Iran, or North Korea) became instantly ineligible for any portion of the credit. This rule was applied with zero “grace period,” meaning several models that were eligible on December 31, 2024, became ineligible on January 1, 2025, due to their graphite or electrolyte sourcing.

Best for: Consumers who were surprised to find certain low-cost EVs excluded from the program.

Why We Chose It: It was the primary driver for the removal of several high-volume EVs from the eligibility list.

Things to consider: This rule specifically targeted the battery’s chemical components, not just the final assembly of the cells.

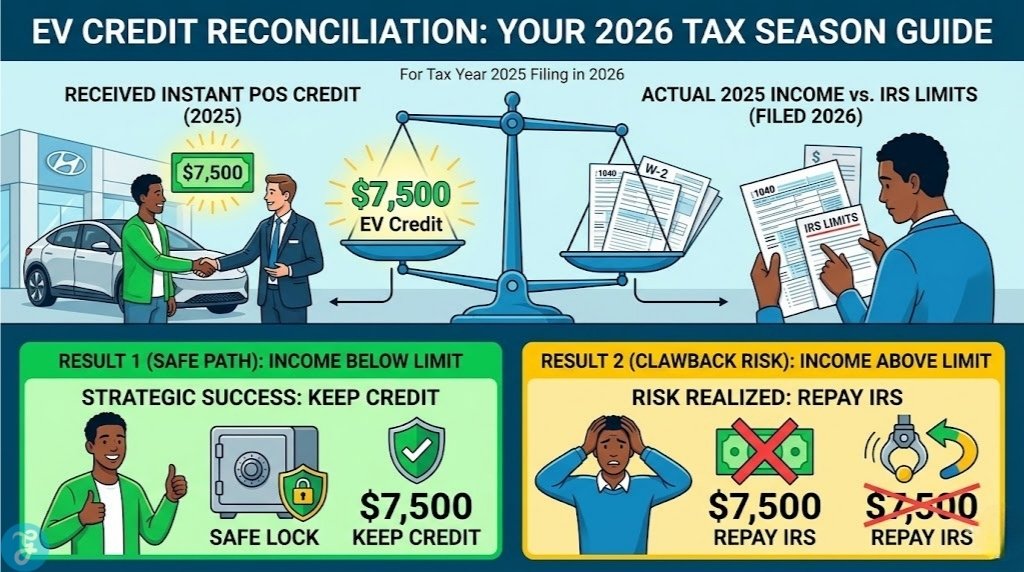

5. The “Instant Credit” Repayment Risk

The 2025 tax year allowed buyers to transfer their credit to the dealer for an instant $7,500 discount. However, many people don’t know that if your 2025 Modified Adjusted Gross Income (MAGI) exceeded the limits ($300k joint, $150k single), you must now pay that money back to the IRS on your current tax return. The “point of sale” rebate was an advance on a credit you hadn’t technically earned yet.

Best for: High-earning individuals whose 2025 income was higher than their 2024 income.

Why We Chose It: It is a major “tax trap” for the 2026 filing season that many people are only discovering now.

Things to consider: You are allowed to use your 2024 income to qualify if it was lower than your 2025 income, providing a one-year buffer.

6. The Used EV “First Transfer” Rule

The $4,000 used EV credit has a strict “one-time-only” rule: a vehicle can only qualify for the credit once in its lifetime. If a used EV was sold in 2023 or 2024 and the buyer claimed the credit, any subsequent buyer in 2025 was automatically ineligible, even if the car met the $25,000 price cap. Many 2025 buyers were denied the credit at the dealership because the VIN history showed a prior credit claim.

Best for: Second-hand EV buyers who found a great deal under the $25,000 threshold.

Why We Chose It: It is a hidden disqualifier that is not visible on a standard window sticker.

Things to consider: Always ask for a “Time-of-Sale Report” from the dealer, which confirms if the VIN is still credit-eligible.

7. The Charging Infrastructure Credit Extension

While the EV vehicle credits were sunsetted early, the 30C charging infrastructure credit was actually extended through June 30, 2026. This means that even if you bought your EV after the September 30 cutoff, you might still be eligible for a 30% credit (up to $1,000) on the installation of your home charger. This remains one of the few active federal incentives for current EV owners.

Best for: New EV owners who installed a home charging station in late 2025 or early 2026.

Why We Chose It: It provides a “silver lining” for those who missed the vehicle credit but still invested in home infrastructure.

Things to consider: This credit is only available if your home is located in a “non-urban” or “low-income” census tract as defined by the IRS.

An Overview Of US EV Tax Credit 2025 Eligibility Tiers

Understanding your eligibility requires a look at how the different 2025 credits interacted with the legislative deadlines. The following comparison highlights the varying sunset dates and caps.

| Credit Type | Max Value | MSRP Cap | Sunset Date |

| New EV Credit | $7,500 | $55k (Sedan) / $80k (SUV) | Sept 30, 2025 |

| Used EV Credit | $4,000 | $25,000 | Sept 30, 2025 |

| Lease “Loophole” | $7,500 | None | Sept 30, 2025 |

| Charger Credit | $1,000 | N/A | June 30, 2026 |

Our Top 3 Picks and Why?

-

The Binding Contract Exception: This was the most important protection for consumers in 2025. Without this “acquisition” rule, thousands of buyers who ordered cars in early 2025 would have lost thousands of dollars due to shipping delays outside of their control.

-

The Instant POS Transfer: This changed the EV market from a “tax season” incentive to a “shopping season” incentive. By making the $7,500 a down payment rather than a tax refund, it lowered the barrier to entry for middle-class families significantly.

-

The 30C Charging Credit: We chose this because it is the “survivor” of the 2025 legislative shift. For those filing their taxes right now in 2026, it is often the only credit they can still claim if they missed the vehicle purchase window.

How to Verify Your US EV Tax Credit 2025 Eligibility Today?

If you are preparing your 2025 tax return right now, you need to verify your eligibility based on the final rules. Use the following framework to ensure your claim is valid before you file Form 8936.

The Selection Framework

-

Verify the Acquisition Date: Ensure your purchase agreement was signed on or before September 30, 2025.

-

Confirm the VIN Status: Use the IRS “Clean Vehicle” lookup tool to ensure your specific model didn’t lose eligibility due to the 2025 FEOC rules.

-

Audit Your 2024/2025 Income: Compare your MAGI for both years; if either is below the threshold, you qualify.

-

Check Your Used EV History: If you bought a used EV, verify with the dealer that it was the “first transfer” to an individual after August 2022.

The following matrix helps you determine if you should claim the credit or if you might be at risk of a clawback.

| Situation | Eligibility Status | Action Required |

| Bought New EV Aug 2025 | Likely Eligible | File Form 8936 to reconcile. |

| Bought New EV Oct 2025 | Ineligible | Do not claim; look for state-level credits. |

| Took POS Credit, Income $200k | Eligible (if Single) | No repayment needed. |

| Took POS Credit, Income $400k | Ineligible | Repay the $7,500 on your 2025 return. |

The Final Checklist

-

Did you receive a “Time-of-Sale” report from your dealer at the time of purchase?

-

Is your vehicle’s final assembly location in North America?

-

Does the sales price of your used EV ($25,000 cap) include dealer fees?

-

Have you confirmed your home’s census tract eligibility for the charger credit?

-

Are you filing Form 8936 even if you already received the credit at the dealership?

Closing the Chapter on Federal EV Incentives

The 2025 tax year represented the end of an era for aggressive federal EV subsidies. With the early termination of these programs on September 30, the focus has shifted toward state-level incentives and manufacturer-driven discounts. While the federal landscape is now more restrictive, those who navigated the 2025 eligibility rules successfully were able to secure some of the last major tax-funded savings for the transition to electric mobility.

Frequently Asked Questions About US EV Tax Credit 2025 Eligibility

Can I still get the $7,500 credit in 2026?

Answer: Generally, no. The federal Clean Vehicle Credit ended for vehicles acquired after September 30, 2025. Some commercial or “clean energy” credits may still apply for business fleets, but the standard consumer credit is currently unavailable for new purchases.

What if I leased my EV in 2025?

Answer: Leased vehicles were eligible for the $7,500 credit via the “Commercial” loophole, but this also sunsetted on September 30, 2025. If your lease started after that date, the credit usually wasn’t passed down to you in the form of lower payments.

Do I have to pay back the credit if I sell the car?

Answer: No. As long as you purchased the vehicle for your own use and not for resale, you are not required to repay the credit if you decide to sell the car later in 2026.

How do I find my home’s “Census Tract” for the charger credit?

Answer: You can use the IRS-provided mapping tool or enter your address into the Federal Financial Institutions Examination Council (FFIEC) website to find your GEOID and cross-reference it with the list of eligible “non-urban” or “low-income” zones.

Is the MSRP cap based on the base price or the final price?

Answer: The MSRP cap ($55k for cars, $80k for SUVs/Trucks) is based on the Manufacturer’s Suggested Retail Price including options, but excluding destination charges and taxes.