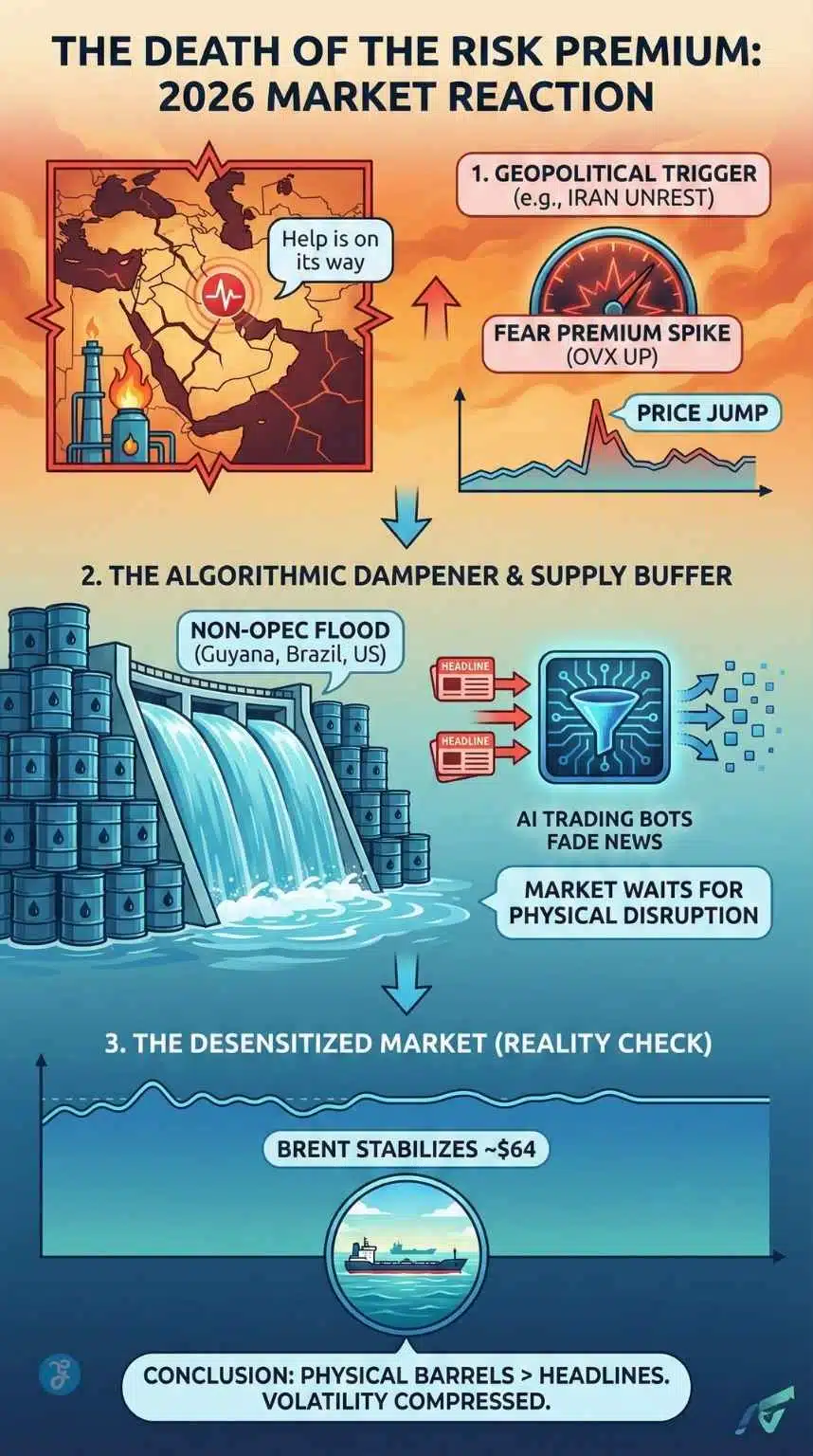

Oil Prices Forecast 2026, the global energy market has signaled a decisive shift in how it processes geopolitical risk, with crude benchmarks retreating sharply despite ongoing instability in the Middle East. Brent Crude has stabilized near $64 per barrel, while West Texas Intermediate (WTI) hovers around $59, marking a swift unraveling of the “war premium” that briefly flared earlier this month.

The immediate catalyst for this bearish turn is the grim restoration of order in Tehran following weeks of civil unrest. However, a deeper analysis reveals a more structural transformation: the emergence of a “Desensitized Energy Market.” In this new paradigm, traders, aided by algorithmic execution, are increasingly shrugging off headline risks, from regime changes in Venezuela to bizarre trade disputes over Greenland, in favor of cold, hard supply fundamentals.

This analysis dissects the current market apathy, the structural supply glut cushioning prices, and the “unconventional” risks that could define the remainder of 2026.

The “Fear Premium” Evaporates: Market Reaction Analysis

The reaction to the de-escalation in Iran has been clinical and immediate. Just a week ago, speculative buying pushed Brent toward $67 on the back of President Trump’s “Help is on its way” rhetoric and footage of burning government buildings in Tehran. Today, those gains have evaporated.

The “Boy Who Cried Wolf” Dynamic

The swift sell-off underscores a critical lesson for 2026: The market now demands physical disruption before pricing in risk.

- Volatility Compression: Despite the high stakes, Iran produces roughly 3.2 million barrels per day (bpd), and implied volatility metrics (OVX) barely spiked.

- Algorithmic Dampeners: High-frequency trading algorithms are now programmed to “fade” geopolitical headlines almost instantly. Instead of panic-buying on news of a missile strike or a protest, these bots scan satellite data for actual tanker stoppages. When none are detected, they short the rally.

- The Result: A market that feels “numb” to danger. As John Evans of PVM Oil Associates noted in a recent client note, “The market is locked in a stalemate between perceptions of oversupply and a thickening layer of geopolitical risk that it simply refuses to price in.”

Key Stat: Brent Crude dropped 4.5% in 48 hours once reports confirmed that Iran’s security forces had regained control of key export terminals at Kharg Island.

The Iran Situation: A Brutal “Calm”

The stabilization of oil prices is built on a grim reality. The “calm” that traders are celebrating is the result of a violent crackdown that has reportedly left thousands dead, but the oil infrastructure intact.

- The Unrest: What began as protests against currency devaluation and the removal of fuel subsidies quickly morphed into a call for regime change. For a brief window (Jan 12-15), the market feared a repeat of the 1979 revolution, which removed millions of barrels from the global market.

- The Resolution: By January 19, Tehran declared the “sedition” over. State media footage showed the resumption of normal operations at the Abadan refinery.

- The US Pivot: Crucially, the White House walked back its aggressive posture. After signaling potential support for the protesters, the administration pivoted to a “wait and see” approach, effectively removing the immediate threat of a U.S. naval blockade or airstrikes on nuclear facilities.

Market Takeaway: The “Regime Stability = Lower Prices” correlation remains the market’s guiding star, regardless of the humanitarian cost.

Structural Realities: The “Supply Glut” Buffer

Why is the market so confident in ignoring these risks? The answer lies in the massive “Supply Buffer” built up by non-OPEC producers. The Oil Prices Forecast 2026 is heavily weighted by a physical wall of crude that makes the Middle East less relevant than it was a decade ago.

The Non-OPEC Flood

While the headlines focus on the Middle East, the barrels are coming from the Atlantic Basin.

- Guyana’s Meteoric Rise: The tiny South American nation is the star of 2026. With the Uaru project now ramping up, Guyana’s total output is crossing the 1.1 million bpd threshold. This high-quality, low-sulfur crude is flooding into European and Asian markets, directly competing with OPEC grades.

- Brazil’s Offshore Boom: New FPSO vessels in the pre-salt fields have pushed Brazil’s production to nearly 3.8 million bpd, adding another layer of security to global supply.

- USA Permian Basin: Despite a lower rig count, efficiency gains (longer laterals, AI-driven fracking) have kept U.S. production steady at a record 13.6 million bpd.

OPEC+ Pauses the Cuts

Facing this deluge, OPEC+ has opted for a “production pause” for Q1 2026 rather than deeper cuts. The cartel acknowledges that ceding more market share to Guyana and the U.S. is a losing strategy.

- The Strategy: OPEC is betting that demand will catch up in late 2026.

- The Reality: The International Energy Agency (IEA) currently forecasts a 3.8 million bpd surplus capacity globally. This “spare capacity” acts as a massive shock absorber. Even if Iran went offline tomorrow, the market believes Saudi Arabia and the UAE could plug the gap within weeks.

The “Fiscal Pain” Threshold: How Long Can OPEC Bleed?

While consumers celebrate falling prices at the pump, the “Desensitized Market” is creating a fiscal nightmare for OPEC+ nations. The critical metric to watch in Q1 2026 is the “Fiscal Breakeven Price”, the price per barrel needed for a country to balance its government budget.

- Saudi Arabia’s Dilemma: Despite its massive reserves, Riyadh requires oil at approximately $78-$80 per barrel to fund its ambitious “Vision 2030” giga-projects like NEOM. With Brent trading at $64, the Kingdom is effectively burning through its foreign currency reserves to keep the lights on.

- The Russian Reality: Moscow has adjusted its budget for a longer war economy, but at $60/barrel, its oil revenue barely covers domestic spending, let alone military expansion.

- The Breaking Point: This creates a dangerous game of chicken. The market is currently “desensitized,” but if prices dip below $60 for a sustained quarter, we should expect a desperate, and potentially chaotic, response from the cartel. This could range from surprise unilateral cuts to aggressive diplomatic pressure on non-compliant members like Iraq. The current calm is expensive, and OPEC cannot afford it forever.

The Fiscal Pain Index: OPEC+ Fiscal Breakeven vs. Current Reality [Jan 2026]

It shows exactly why OPEC+ cannot afford to let the “desensitized” market continue for too long; most members are losing money at current prices.

| Country | Fiscal Breakeven Price* ($/bbl) | Current Brent Price ($/bbl) | Fiscal Status |

| Saudi Arabia | $78.00 – $80.00 | $64.15 | Deep Deficit: Vision 2030 projects at risk. |

| Russia | $72.00 – $75.00 | $64.15 | Deficit: The war economy budget is strained. |

| Iraq | $85.00+ | $64.15 | Critical: Public sector salary crisis looming. |

| UAE | $60.00 – $65.00 | $64.15 | Balanced: The only major member currently safe. |

| Iran | $300.00+ (Sanctioned) | ~$55.00 (Discounted) | Crisis: Selling at deep discounts to China. |

Note: Fiscal Breakeven Price is the price per barrel required for the country to balance its government budget.

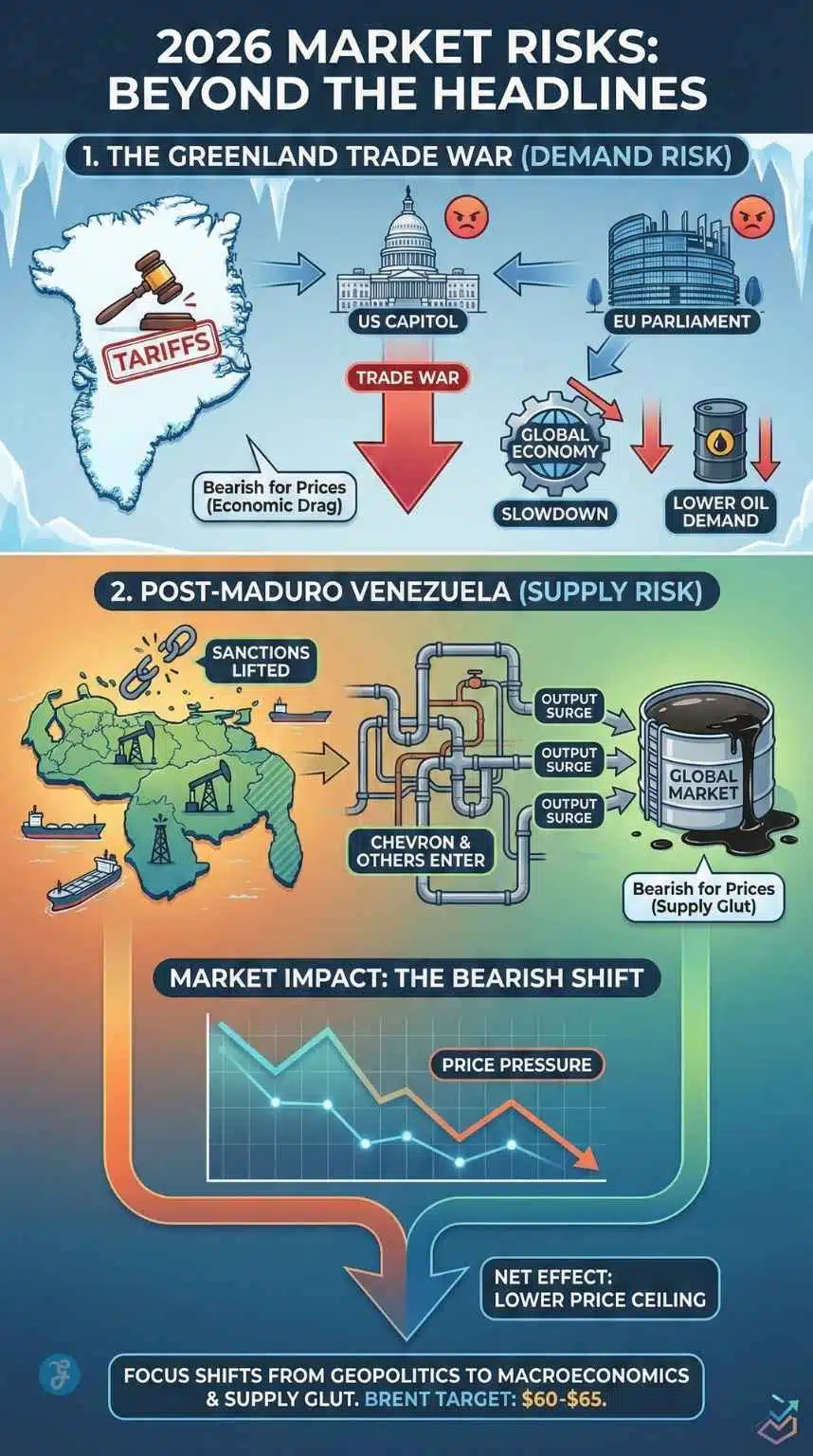

Beyond Iran: The New “Unconventional” Risks

In a “desensitized” market, standard risks (war in the Middle East) are ignored. However, traders are keeping a wary eye on two “unconventional” flashpoints that threaten the mechanics of trade rather than just the supply.

A. The Greenland Standoff: Demand Destruction Risk

In one of the most surreal geopolitical turns of 2026, the diplomatic row between the U.S. and the EU over Greenland has become a legitimate market mover.

- The Context: President Trump’s renewed offer to purchase Greenland was rejected by Denmark and the EU, leading to threats of punitive U.S. tariffs on European autos and wind turbines.

- The Oil Angle: This is a Bearish Risk. If a transatlantic trade war erupts, it would crush economic growth in the Eurozone, effectively killing oil demand. While war in Iran is bullish (supply fear), a trade war over Greenland is bearish (demand fear).

- Status: Traders are shorting oil every time the “Greenland Tariff” rhetoric heats up.

B. Post-Maduro Venezuela: The Chaotic Re-entry

Following the ouster of Nicolás Maduro on January 13, Venezuela is open for business, but it’s a mess.

- The Chevron Effect: The U.S. has moved swiftly to license Chevron and other Western majors to rehabilitate Venezuela’s dilapidated fields.

- The Impact: In the short term, this is chaotic. Traditional flows to China (repayment for debt) are being diverted to U.S. Gulf Coast refineries. While this promises more supply in 2027, the immediate effect is logistical gridlock. However, the market views this as “net bearish” for the long term, adding yet another source of supply to an oversupplied world.

The “Drill, Baby, Crash” Paradox

The White House finds itself in a paradoxical position in 2026. President Trump’s “Drill, Baby, Drill” mandate has been wildly successful in boosting production to record highs (13.6M bpd), but this very success is crashing the price.

- The Double-Edged Sword: Low prices are great for the President’s approval ratings (low gas prices), but they are disastrous for the US oil donors who supported his campaign.

- The Tariff Threat: Watch for a potential pivot. If prices fall too low (threatening US oil jobs), the administration might paradoxically consider supporting prices, perhaps by enforcing stricter sanctions on Iranian or Venezuelan exports to artificially tighten the market. The “Desensitized Market” might force the most free-market President to intervene to save domestic producers.

Macroeconomic Headwinds: The Demand Equation

The final nail in the coffin for the “Risk Premium” is the lackluster demand picture, particularly from the world’s engine room.

- China’s Slowdown: Beijing’s economic data for January 2026 has been underwhelming. Manufacturing PMI remains in contraction territory, and the expected post-stimulus boom hasn’t materialized. As the world’s largest oil importer, China’s weakness puts a hard “ceiling” on prices.

- The Cold Snap Wildcard: The only immediate “Bullish” factor is the weather. Meteorologists are predicting a Polar Vortex event for late January across North America and Northern Europe.

- Forecast: This could trigger a short-term spike in demand for heating oil and natural gas, potentially drawing down inventories. However, traders view this as a temporary weather event, not a structural shift.

Market Winners & Losers: The Investment Implications

A sustained period of $60 oil creates distinct economic beneficiaries and casualties. For investors and corporate strategists, the 2026 playbook is shifting:

The Winners (Deflationary Plays)

- Airlines & Logistics: Carriers like Delta and DHL are seeing their highest operational costs, fuel, plummet. Expect revised earnings guidance to the upside for the transport sector in Q1.

- Net Importers (India & Japan): For economies like India, which imports over 80% of its crude, this price drop is a massive stimulus, reducing the import bill and cooling domestic inflation. The Indian Rupee (INR) and Japanese Yen (JPY) may strengthen against the dollar as a result.

The Losers (High-Cost Producers)

- US Shale Independents: While majors like ExxonMobil can survive at $40, smaller, highly leveraged shale drillers in the Permian Basin need $55-$60 just to service debt. A dip below $55 could trigger a wave of consolidation or bankruptcies in the American energy patch.

- The “Green Premium”: Ironically, cheap oil is a headwind for the renewable transition. When fossil fuels are cheap, the immediate economic incentive for heavy industries to switch to green hydrogen or biofuels diminishes, potentially slowing the pace of decarbonization projects in the short term.

2026 Market Impact Matrix: Winners & Losers in the $60 Oil Environment

It is great for skimming and allows investors to quickly identify which sectors to watch.

| Sector / Entity | Impact | Rationale |

| Global Airlines | Bullish | Jet fuel costs (30% of expenses) drop significantly; margins expand. |

| Net Importers (India/Japan) | Bullish | Lower import bills reduce inflation and strengthen national currencies (INR/JPY). |

| US Shale (Independents) | Bearish | Small drillers in the Permian need ~$55 to break even; bankruptcies likely below $50. |

| Green Energy / Renewables | Bearish | Cheap fossil fuels reduce the immediate economic incentive for industrial decarbonization. |

| Logistics (FedEx/DHL) | Bullish | Reduced diesel surcharges boost shipping volumes and consumer demand. |

Strategic Outlook for Q1 2026

- Price Target: Expect Brent to trade in a tight range of $60 – $65.

- Upside Risk: A physical closure of the Strait of Hormuz (Probability: Low).

- Downside Risk: Escalation of U.S.-EU trade tariffs over Greenland or worse-than-expected China data (Probability: Moderate).

In this environment, the smart money is ignoring the “War Headlines” and watching the “Trade Headlines.”

Final Thought: The Death of the Risk Premium?

The events of January 2026 have confirmed a hypothesis that has been building for years: The Geopolitical Risk Premium is effectively dead.

Unless a conflict physically stops a tanker, closes a pipeline, or destroys a refinery, the algorithm-driven, oversupplied market will not sustain a price rally. The “Desensitized Market” is a creature of abundance; there is simply too much oil in the world for fear to take hold.