Taxes hit hard every year, don’t they? You work all day, save what you can, and then boom, a big chunk goes to the IRS. It’s frustrating when your tax bill feels like a thief in the night, stealing your peace of mind. Imagine if you could fight back without breaking any rules. That’s the dream for folks staring at their paychecks, wondering where the money went.

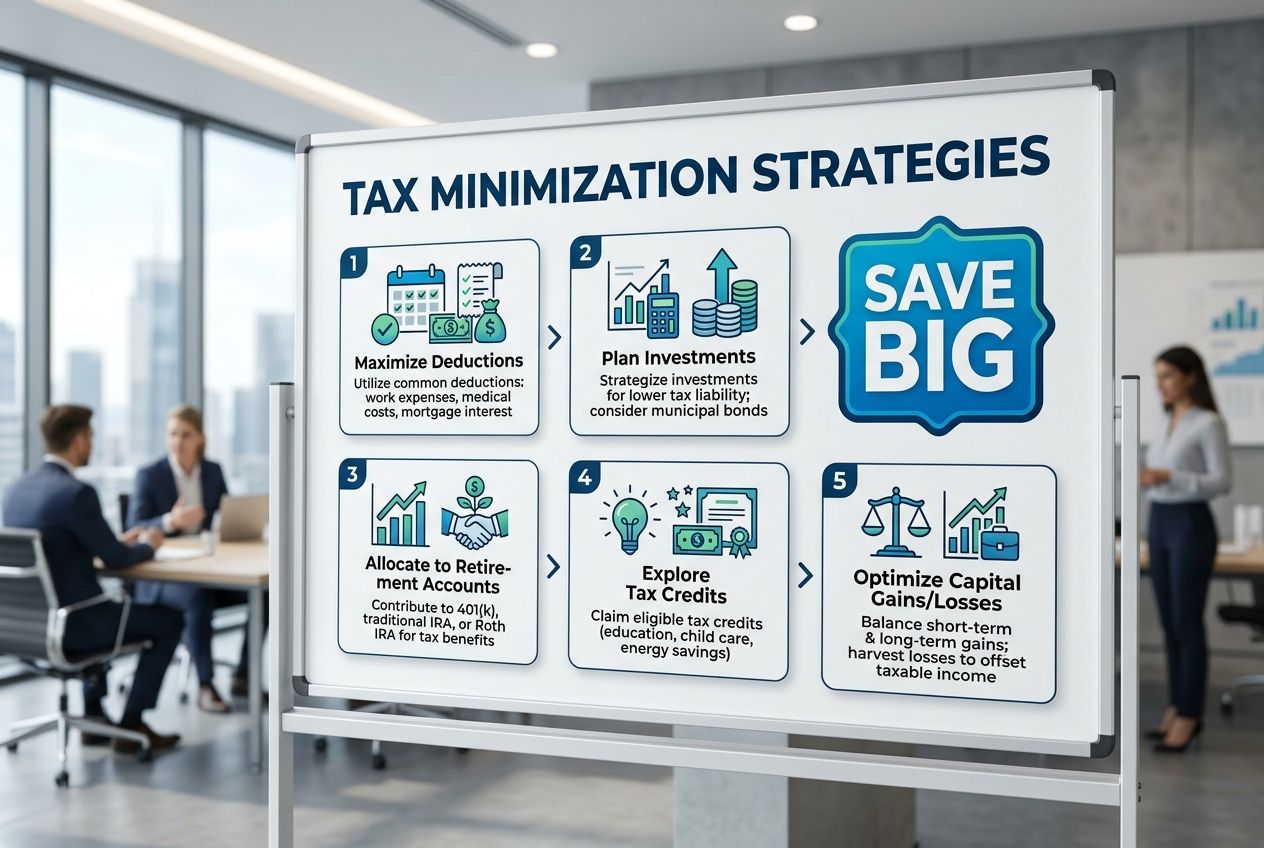

One key fact stands out: the average American overpays taxes by hundreds of dollars each year due to missed deductions. This post explores Tax Minimization Strategies that keep more cash in your pocket, from boosting retirement savings to smart charitable moves.

We’ll walk you through simple steps that anyone can follow. Ready to save big?

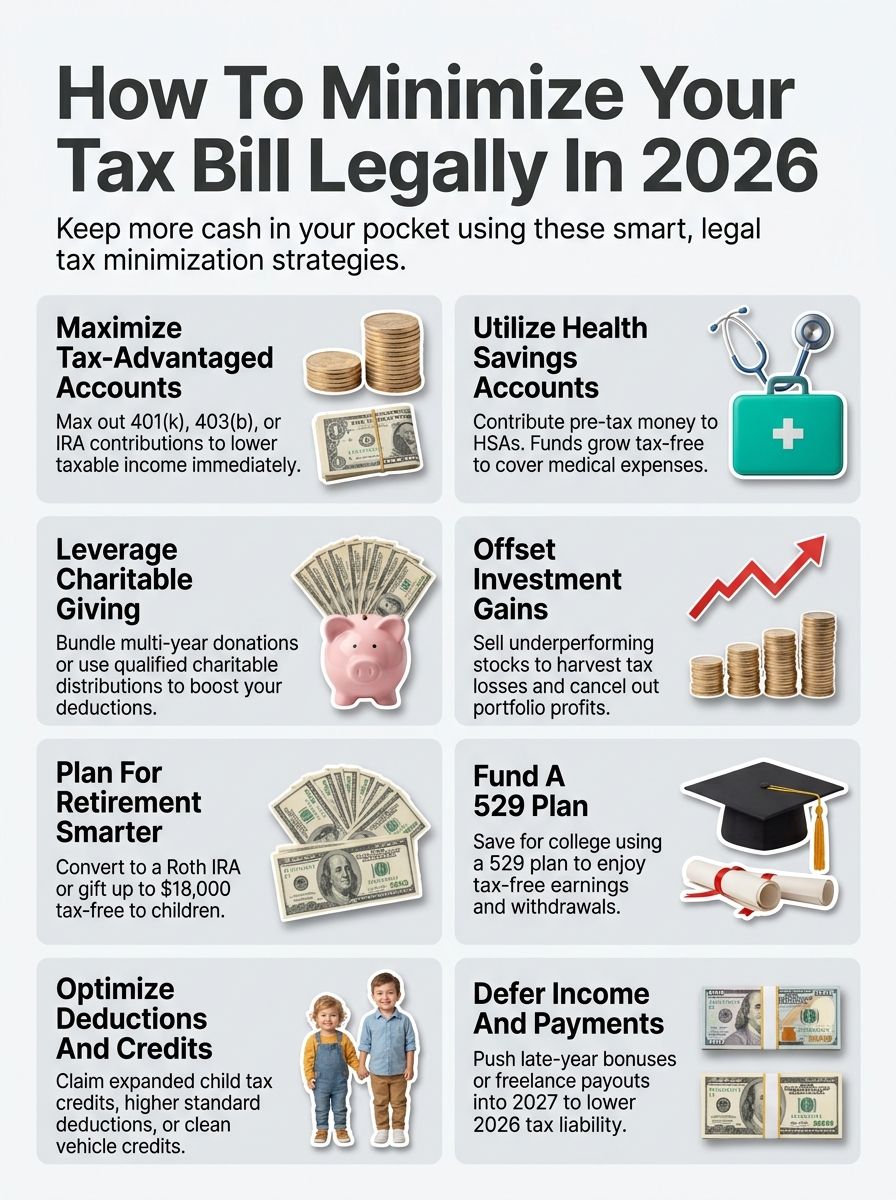

Maximize Tax-Advantaged Accounts

Put your money to work in accounts that slash taxes, like stuffing cash into a 401(k) or IRA before the year ends. Imagine your savings growing tax-free, giving you a real edge come filing time, so dig into these options now.

Contribute to 401(k), 403(b), or Traditional IRA

You want to cut your tax bill in 2026, so start with retirement contributions. Put money into a 401(k) or 403(b) through your job. These plans lower your taxable income right away.

For example, stash up to $23,000 in a 401(k) if you’re under 50. That move gives you big tax deductions. Or pick a Traditional IRA for similar perks. You can add up to $7,000 if you’re under 50.

This tax strategy boosts your savings and shrinks your tax liability. Hey, it’s like planting seeds for a richer future while dodging taxes now.

Many folks overlook how these accounts supercharge tax planning. They let you defer taxes on earnings until you pull the money out. Imagine your investments growing tax-free for years.

That means more cash in retirement. Plus, some employers match your 401(k) contributions. Free money, anyone? Use this for a smart financial strategy and income tax savings. It fits right into fiscal responsibility.

The secret to building wealth is to start saving early and let compound interest work its magic. – A wise investor

Utilize a Health Savings Account (HSA)

Think about your health costs as a sneaky tax trap, folks. Open a Health Savings Account, or HSA, if you have a high-deductible health plan. You put money in before taxes, which cuts your tax bill right away.

That cash grows tax-free over time. Spend it on doctor visits, meds, or even eyeglasses, and skip taxes on those withdrawals too. Families can sock away up to $8,300 in 2026, while singles hit $4,150.

Folks over 55 add an extra $1,000. This tax strategy feels like finding money in an old coat pocket, easing your tax liability without much fuss.

People often overlook how HSAs double as retirement boosters. Save what you don’t spend, and after 65, pull funds for anything without penalties, just like a traditional IRA. Pair this with smart tax planning to maximize savings.

Imagine dodging taxes on medical bills that pile up; it’s a real win for fiscal responsibility. Now, let’s talk about ways to leverage charitable giving opportunities.

Leverage Charitable Giving Opportunities

You know that warm, fuzzy feeling from helping others? It turns out, giving to charity can slash your tax bill too, like killing two birds with one stone, if you play your cards right.

Imagine donating in ways that boost your deductions without dipping into your pocket extra, and hey, who wouldn’t want to feel like a hero while keeping more cash?

Make qualified charitable distributions (QCDs)

Folks over age 70 and a half can slash their tax liability with qualified charitable distributions. Imagine: you send money straight from your traditional IRA to a charity you love.

That counts as your required minimum distribution. Best part? It skips your taxable income altogether. In 2026, aim for up to $105,000 per person, thanks to inflation adjustments. This tax strategy feels like a win-win, supporting causes while dodging extra taxes.

Talk about smart charitable giving. You avoid the hit on adjusted gross income, which opens doors to other tax deductions. Couples can double up if both qualify. Just pick eligible charities, like your local food bank or alma mater. Keep records tight for tax compliance. Now, bundle those multi-year deductions into one year for even bigger tax savings.

Bundle multi-year deductions into one year

You know that feeling when you stack all your firewood in one spot to build a bigger fire? Bundling multi-year deductions works like that for your tax bill. Group big expenses, such as charitable giving or medical costs, into a single tax year.

This boosts your itemized deductions above the standard deduction, slashing your tax liability. People often double up on donations, say, giving two years’ worth in December 2026. Tax strategies like this optimize your tax planning without breaking rules.

Picture a savvy saver who pays property taxes early and bunches medical bills. They claim hefty tax deductions in one go, then switch to the standard deduction next year. This approach cuts income tax smartly, especially for families eyeing tax credits.

Use it with retirement contributions to enhance savings. Charitable giving shines here, turning generosity into real tax savings.

Offset Investment Gains

Investment gains can pile up fast, and nobody wants Uncle Sam taking a big bite. Sell off some underperforming stocks to cancel out those profits, or shift assets around like a pro chess player, keeping more cash in your pocket—stick around for the full playbook.

Use tax-loss harvesting strategies

You spot a stock that tanked this year, right? Sell it to lock in that loss. This move offsets your capital gains from winners in your portfolio. Tax-loss harvesting cuts your tax bill by reducing taxable income.

Imagine turning a market dip into a silver lining, like finding money in an old coat pocket. Folks often use this in taxable accounts, not IRAs. Aim to sell before year-end for the best impact.

Pair those losses with gains to wipe out tax liability on profits. Excess losses? Deduct up to $3,000 against ordinary income. Carry over the rest to future years. This tax strategy boosts your savings without breaking rules.

Think of it as a smart shuffle in your investment deck, keeping more cash in your wallet. Consult a pro to avoid wash-sale pitfalls, where you can’t buy back the same stock too soon.

Rebalance your portfolio strategically

Rebalance your portfolio to cut tax liability, folks. Think of it like shuffling cards in a game where you win by keeping more cash. Move high-growth stocks into tax-advantaged spots, such as Roth IRAs, to shield gains from Uncle Sam.

Asset location matters here, so park bonds in taxable accounts for lower hits. This tax strategy boosts savings without breaking rules.

I get it, juggling investments feels like herding cats sometimes. Start small, review your mix yearly, and sell off losers to offset winners. Tax optimization shines when you align assets smartly, reducing your total tax bill in 2026.

Gifting shares to family can defer taxes too, turning potential pains into gains. Keep it simple, and watch those tax savings add up.

Plan for Retirement

Think about your golden years, folks, like planting seeds today for a shady tree tomorrow. You can shift funds from a traditional IRA to a Roth version, paying taxes now to dodge bigger bites later, or gift cash to your kids’ accounts, turning family love into smart tax moves that keep more money in your pocket.

Consider converting a Traditional IRA to a Roth IRA

You might convert your Traditional IRA to a Roth IRA as a smart tax strategy. This move lets you pay taxes now on the converted amount, but future withdrawals come tax-free. Imagine dodging a bigger tax bill later when rates climb.

For 2026, plan this during a low-income year to cut your tax liability. Retirement contributions like this build long-term tax savings. Talk to a tax pro first; they spot the best timing.

Folks often overlook how Roth conversions fit into comprehensive tax planning. Shift funds bit by bit over years to stay in lower brackets. Think of it as planting seeds for a tax-free harvest in retirement.

This approach offsets income tax hits and boosts fiscal responsibility. Use it with other moves, like asset location, for max impact on your tax bill.

Help your children with their retirement through gifting

Parents, you can boost your kids’ future savings with smart gifts that cut your tax bill. Give up to $18,000 per child in 2026 without triggering gift taxes; that’s the annual exclusion limit.

This money goes straight into their Roth IRA, building tax-free growth over time. Imagine handing them a nest egg that grows like a well-tended garden, all while you trim your own tax liability through gifting strategies.

Kids under 50 can sock away up to $7,000 in a Roth IRA yearly, and your gifts make that possible even if they lack earned income from jobs. Use this tax planning move to shift assets efficiently, dodging higher estate taxes later.

Think of it as passing the baton in a relay race, setting them up for retirement wins while you claim those sweet tax savings.

Explore Education Savings Options

Saving for college feels like a smart move, right, especially when it cuts your taxes. Put cash into a 529 plan, grow it tax-free, and pull funds for school without the IRS bite.

Fund a 529 education savings plan

Fund a 529 education savings plan to slash your tax bill with smart tax strategies. You put money into this account for college costs, and earnings grow tax-free. Withdrawals stay tax-free too, as long as you use them for qualified education expenses like tuition or books.

Many states offer tax deductions or tax credits on contributions, boosting your tax savings right away. Imagine stashing cash for your kid’s future while trimming your income tax liability today; it’s like hitting two birds with one stone.

Families love this for long-term tax planning, especially with rising college prices. This approach fits neatly into your total financial strategy for fiscal responsibility. Now, let’s tackle how to efficiently manage healthcare costs.

Efficiently Manage Healthcare Costs

Healthcare bills hit hard, like a surprise punch in the wallet. Fight back and cut your taxes. Claim deductions for medical expenses that top 7.5% of your adjusted gross income. Think doctor visits, prescriptions, and even some travel to get care.

You rack up savings there. Contribute to a flexible spending account, too. Set aside pre-tax cash for health needs. Pay for copays and contacts without the tax bite. It’s a smart play, almost like free money for your aches and pains. Stick around for tips on optimizing deductions and credits next.

Take advantage of medical tax deductions

You face high medical bills this year, right? Deduct those costs on your taxes if they top 7.5% of your adjusted gross income. Think doctor visits, surgeries, or even mileage to appointments.

Folks often overlook this tax deduction, like a hidden gem in your tax planning toolkit. Track every receipt, from prescriptions to dental work, and slash your tax bill legally. Imagine turning that hefty hospital bill into a smart tax strategy that puts money back in your pocket.

Pair this with other moves, such as bunching expenses into one year for bigger savings. Families with ongoing health needs see real wins here, cutting tax liability without breaking a sweat.

Use apps to log costs easily, and consult a pro to maximize these tax deductions. This approach fits right into your total financial strategy, keeping things simple and effective for 2026.

Contribute to flexible spending accounts (FSAs)

Flexible spending accounts let you set aside pre-tax dollars for healthcare costs. You contribute money from your paycheck before taxes hit. This cuts your tax bill right away. Think of it as paying for doctor visits or prescriptions with money that skips the taxman.

Many employers offer these plans, and you can use the funds for things like copays or eyeglasses. Just plan wisely, because unused money often vanishes at year’s end, like a pumpkin after Halloween.

Aim to estimate your needs accurately to avoid losing out. These accounts work well for families facing routine medical bills. They boost your tax savings by lowering your taxable income. Pair them with other tax strategies for even bigger wins. Now, let’s optimize deductions and credits.

Optimize Deductions and Credits

Hey, friend, chase down those fresh deductions for 2026. Grab the expanded ones that fit your life. Snap up every tax credit you qualify for, like a smart shopper at a sale. These moves shrink your tax hit big time. Got an appetite for extra ways to save? Keep flipping through this guide.

Claim new or expanded deductions

You know that feeling when you spot a bargain at the store and grab it quickly? That’s like claiming new or expanded tax deductions in 2026, a smart tax strategy to cut your tax bill.

The standard deduction jumps to $15,000 for single filers and $30,000 for married couples filing jointly, up from last year. Itemized deductions get a boost too, with higher limits on mortgage interest and state taxes. Homeowners, listen up, you can deduct up to $1 million in mortgage debt now, a real game-changer for big loans.

Business owners face fresh chances with expanded deductions for electric vehicles and green energy upgrades. Imagine you buy a qualifying EV and slash $7,500 off your tax liability through the clean vehicle tax credit.

Families benefit from pumped-up child tax credits, now worth up to $2,000 per kid, easing your income tax load. Pair these with charitable giving or retirement contributions, and you optimize your tax planning like a pro.

Stay on top of tax compliance by tracking receipts; it pays off big time.

Take full advantage of available tax credits

After claiming those new or expanded deductions to lower your taxable income, shift your focus to tax credits, which can slash your tax bill even more by reducing what you owe dollar for dollar. Tax credits act like a direct discount on your tax liability, so grab every one that fits your life.

Families, listen up, the Child Tax Credit offers up to $2,000 per qualifying kid under 17 in 2026, a real game-changer for cutting costs. If you earn a modest income, the Earned Income Tax Credit could boost your refund by thousands, depending on your family size and income.

Homeowners might snag the Residential Clean Energy Credit for solar panels, knocking off 30% of installation costs. Electric vehicle fans, check the Clean Vehicle Credit for up to $7,500 on a new plug-in car.

These tax strategies turn everyday choices into smart tax savings, easing your financial load without breaking rules.

Defer Income and Payments

Kick that bonus or freelance payout into 2027 if you can swing it, and bam, you slash your 2026 taxes like a pro dodging a curveball. Craving extra ways to keep more cash in your pocket? Stick around for the wrap-up.

Strategically delay payouts to the following tax year

You can push some income into 2027 to cut your 2026 tax bill. Think about it like holding off on cashing a check until after New Year’s. Self-employed folks, invoice clients late in December so payments hit next year.

Employees might ask bosses to delay year-end bonuses. This tax strategy defers tax liability, giving you more cash now. It works best if you expect lower income taxes next year.

Pair this with other moves for bigger tax savings. Retirees, hold off on extra IRA withdrawals until January. Business owners, time equipment sales wisely. Use this in your tax planning to optimize income tax. Just chat with a pro to stay in tax compliance. Imagine dodging a hefty bill, like sidestepping a puddle after rain.

Wrapping Up

Tax strategies can save you big in 2026, folks. Imagine: you get into retirement contributions, and suddenly your tax bill shrinks like ice in summer heat. Folks often overlook charitable giving as a smart move, but it packs a punch for cutting tax liability.

Income tax optimization feels like a puzzle, but you fit the pieces with ease. Standard deduction might seem basic, yet pairing it with tax planning turns the tide. Gosh, imagine gifting to your kids’ funds, it boosts their future while trimming your tax bill.

Asset location matters too; place investments wisely, and watch tax savings grow. Budgeting strategies tie it all together, making legal loopholes work for you without a hitch. Stay sharp on tax compliance, and you’ll sleep easy knowing your financial strategy stands strong.

FAQs on Tax Minimization Strategies

1. What’s the best way to cut my tax bill legally in 2026?

Hey, think of it like finding hidden treasure in your everyday spending; max out contributions to retirement accounts, like a 401(k) or IRA, to lower your taxable income right away. That move can save you big bucks, and it’s all above board.

2. How do tax deductions help minimize taxes next year?

Tax deductions act like a shield against Uncle Sam’s grab; claim things like home office expenses or medical costs if you qualify. Just keep good records, you know, to avoid any headaches with the IRS. It adds up fast.

3. Can charitable donations reduce my 2026 tax bill?

Absolutely, giving to charity is like killing two birds with one stone; it helps others and shrinks your taxes. Donate cash or goods to qualified groups, and deduct the value from your income; remember, the more you give, the less you owe, but stay within the rules.

4. What about tax credits for lowering my bill in 2026?

Tax credits are straight-up money savers, not just reductions. Grab ones for energy-efficient home upgrades or education costs; they cut your bill dollar for dollar.