You’re self-employed, and tax season hits like a surprise bill you forgot about. You work hard as a freelancer or independent contractor, chasing clients and building your business. But then taxes sneak up, and you scramble to figure out what you owe. It’s stressful, right? Imagine pouring your energy into your passion, only to lose sleep over numbers that don’t add up.

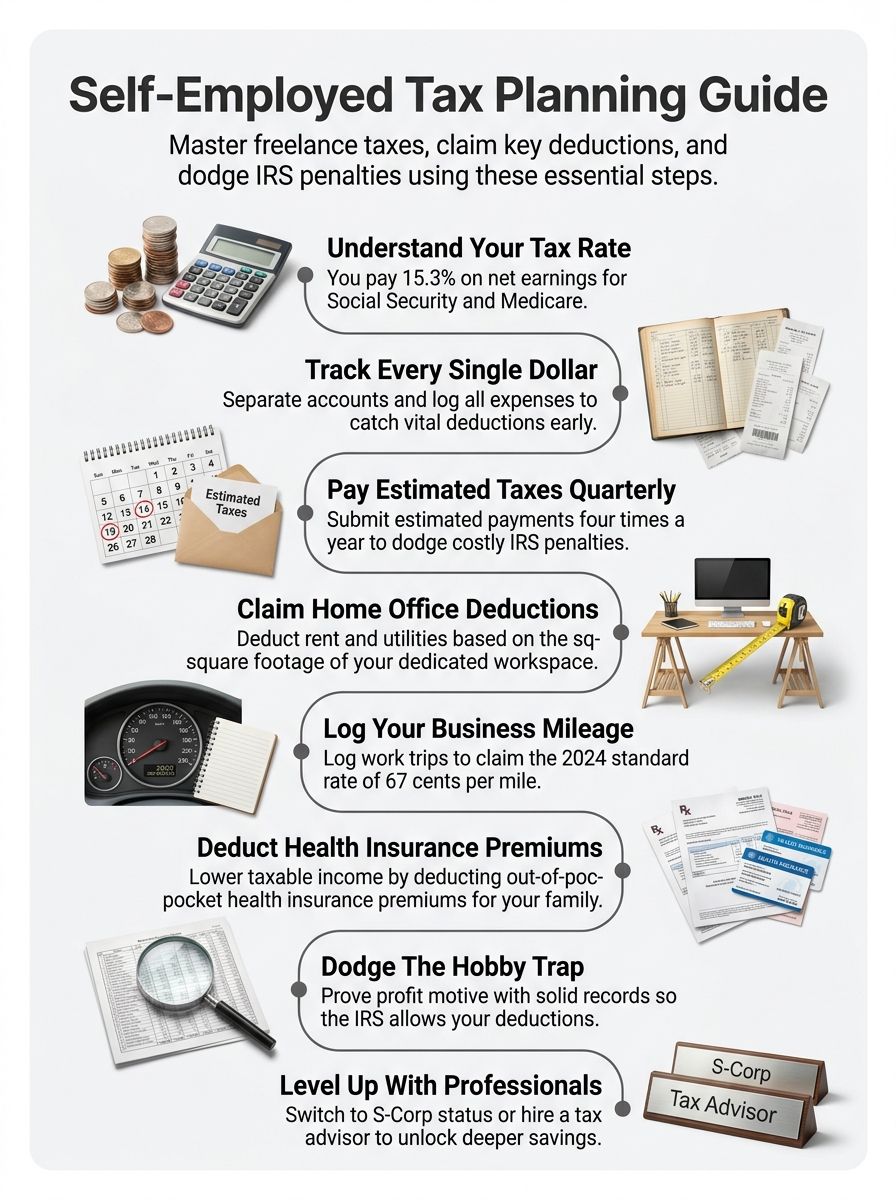

Many folks in your shoes face big tax hits because they skip planning ahead. Did you know self-employed people pay about 15.3 percent in self-employment taxes on their net earnings? That’s a chunk of cash. This guide breaks down Self-Employed Tax Planning in easy steps.

We’ll cover tracking expenses, claiming deductions like home office costs, and making quarterly payments on time. You’ll learn to dodge common pitfalls and even explore smart strategies like S-Corp status.

Understanding Self-Employment Taxes

Self-employment tax hits you hard, like a surprise bill at the end of a fun night out, covering both your share and the employer’s portion of Social Security and Medicare. Here’s the deal: employees split that load with their bosses, but you fly solo, so grasp these basics to dodge nasty surprises and keep your cash flowing smoothly.

What is the self-employment tax?

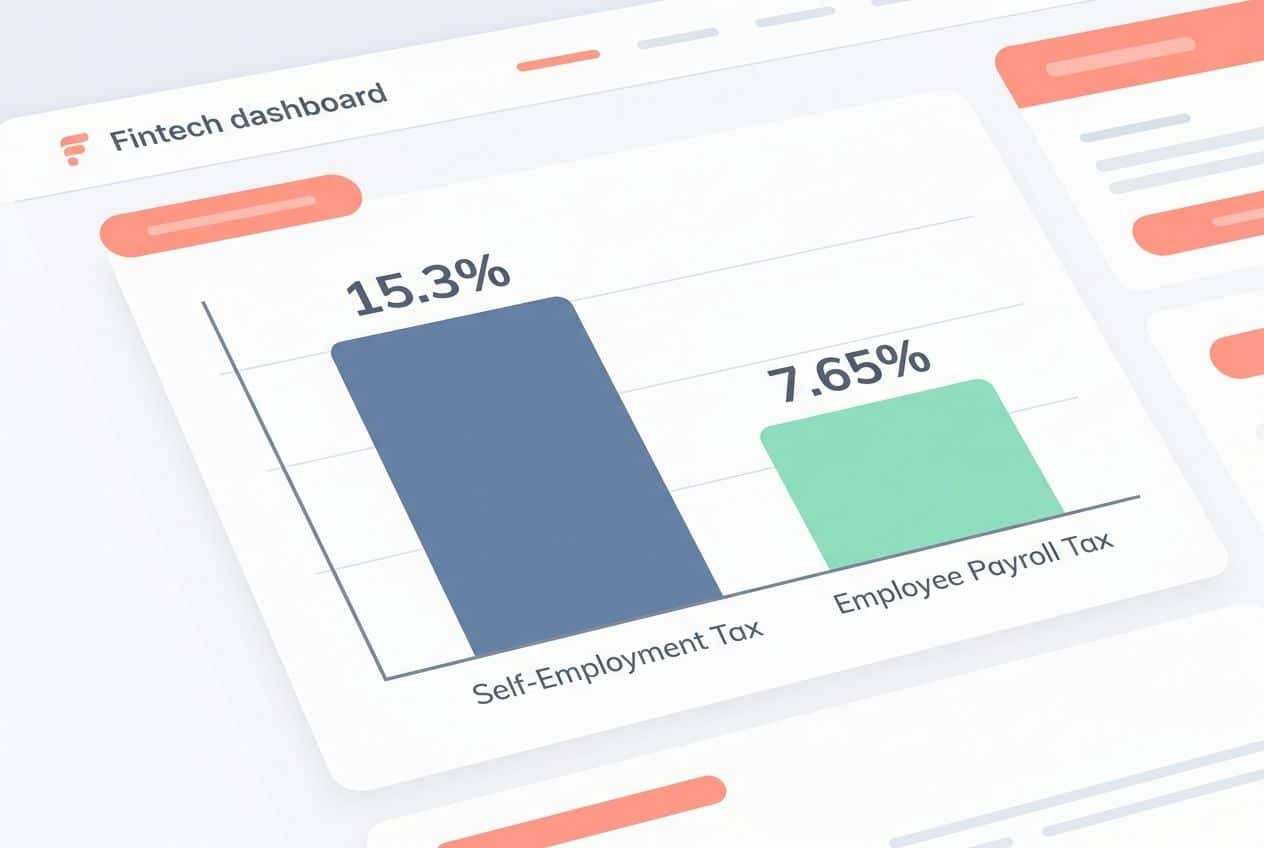

If you’re self-employed, you pay self-employment tax on your net earnings. This tax covers Social Security and Medicare, at a rate of 15.3 percent. Employees split this cost with their bosses, but you handle the full amount as a freelancer or independent contractor.

Think of it like funding your own safety net for retirement and health needs. Half of this tax counts as a deduction on your income tax return, easing the bite a bit.

Self-employment tax is basically the self-employed version of FICA taxes, says IRS guidelines, helping you grasp its role in your financial planning.

You calculate it using Schedule C on your tax return, based on business income minus expenses. This ties into estimated taxes, so track cash flow well to avoid surprises. Many folks deduct costs like health insurance premiums to lower their tax obligations.

Stay on top of record keeping; it makes tax strategies smoother for your self-employment journey.

Key differences between the self-employment tax and the employee payroll tax

Self-employment tax hits differently than the payroll taxes employees face, and grasping these gaps can save you headaches come tax time.

| Aspect | Self-Employment Tax | Employee Payroll Tax |

|---|---|---|

| The rate you pay | You cover the full 15.3% on net earnings, which splits into 12.4% for Social Security and 2.9% for Medicare. | You pay just 7.65%, with your boss matching that amount to hit the total 15.3%. |

| Who foots the bill | You act as both worker and boss, so you shoulder the whole load, like carrying a backpack full of bricks solo. | Your employer splits the cost, easing your share, much like a friend helping lug that heavy load. |

| Payment style | Quarterly estimates fall on you, no automatic withholding, so plan ahead or face penalties. | Taxes get withheld from each paycheck, keeping things steady without extra effort from you. |

| Deduction perks | Deduct half your self-employment tax from adjusted gross income, lightening the blow a bit. | No such deduction exists, since your employer already covers their half. |

| Income threshold | Social Security portion caps at $168,600 for 2024, but Medicare has no limit; it keeps going. | Same caps apply, yet your share stays at half the rate throughout. |

With these differences clear, shift gears to building a solid tax plan that fits your freelance life.

Setting Up a Tax Plan

3. Setting Up a Tax Plan: Picture yourself as a solo captain steering your freelance ship through choppy financial waters, where a solid tax plan acts like your trusty compass. Grab a notebook or app right now, jot down your projected earnings, and log those daily expenses to dodge nasty surprises come April.

Importance of estimating your income accurately

Estimating your income correctly keeps your tax planning on track as a self-employed worker. You avoid big surprises come tax return time. Imagine you’re freelancing and think you’ll earn $50,000, but you pull in $70,000.

That mismatch messes up your estimated taxes and cash flow. Get it accurate to set aside enough for income tax and self-employment tax. Use last year’s Schedule C as a guide, or track monthly earnings closely.

Folks often underestimate ups and downs in freelance work. Stay ahead by reviewing business expenses and retirement plan contributions regularly. This way, you nail those quarterly payments without stress.

Talk to an accounting support buddy if numbers feel tricky. Smart estimating turns tax obligations into a smooth ride, not a headache.

Good tax planning starts with knowing your numbers cold, says tax expert Jane Doe.

Tracking income and expenses efficiently

Once you’ve nailed down accurate income estimates, keeping tabs on your actual earnings and spending becomes your secret weapon for smooth tax planning.

This habit saves you headaches at tax time. It also boosts your cash flow by spotting deductions early.

- Grab a simple app or spreadsheet to log every dollar coming in and going out, like QuickBooks or even Google Sheets for starters; think of it as your financial diary that catches those freelance payments and business expenses before they slip through the cracks.

- Separate your personal and business bank accounts right away to avoid mixing up that coffee run with legit accounting support needs; this move keeps your records clean and makes pulling data for your tax return a breeze.

- Snap photos of receipts on your phone the moment you get them, turning potential paper clutter into digital gold for claiming deductions on things like equipment or travel.

- Review your tracking system monthly, not just quarterly, to tweak your estimated taxes and dodge surprises; imagine catching a big expense early, like health insurance premiums, and adjusting your cash flow on the spot.

- Use categories in your logs for common self-employment items, such as mileage for independent contractors or supplies for freelancers, so you can easily tally up totals for Schedule C without scrambling later.

- Set reminders on your calendar for logging entries weekly, treating it like a quick coffee break that pays off in retirement planning by maximizing those tax strategies.

- Consult free online tools from the IRS for guidance on record keeping, helping you align your habits with tax obligations and avoid audits from sloppy income tax tracking.

- Share anecdotes with fellow self-employed folks in online forums to pick up tips on efficient methods, like how one freelancer turned expense tracking into a game that improved their financial planning.

Quarterly Tax Payments

Picture yourself sailing through the year without a massive tax bill sneaking up like a storm at sea; that’s the magic of quarterly payments if you’re self-employed. Dive right in with us to master this, and keep your finances steady as she goes.

How to calculate your quarterly estimated tax payments

Self-employed folks often dread tax time, but smart planning makes it easier. You handle your own estimated taxes, so let’s break down how to calculate those quarterly payments.

- Figure out your expected adjusted gross income for the year, and subtract any deductions or credits you qualify for to get your taxable income. Use last year’s tax return as a guide, or estimate based on current freelance gigs and business expenses. For example, if you run a graphic design business, tally up client payments minus costs like software subscriptions.

- Apply the self-employment tax rate of 15.3 percent to your net earnings, which covers Social Security and Medicare. Split that into 12.4 percent for Social Security on earnings up to $168,600 in 2024, and 2.9 percent for Medicare with no cap. Add in your income tax rate based on IRS brackets, say 22 percent if your taxable income hits around $100,000.

- Divide your total estimated tax by four to get each quarterly amount, but adjust for uneven cash flow in freelancing. If summer brings big projects, bump up that quarter’s payment. Tools like QuickBooks help track this without headaches.

- Use IRS Form 1040-ES to crunch the numbers officially, or try the IRS online withholding estimator for quick checks. Plug in your Schedule C details from last year, and it spits out estimates. Many independent contractors swear by this to avoid underpayment penalties.

- Check for safe harbor rules to skip penalties, like paying at least 90 percent of this year’s tax or 100 percent of last year’s total. If your adjusted gross income topped $150,000 last year, aim for 110 percent instead. This keeps the IRS off your back and supports steady financial planning.

- Factor in state taxes if your area requires them, on top of federal ones. California freelancers, for instance, add about 9 percent more. Combine everything for accurate quarterly figures, and set reminders for deadlines to maintain good record-keeping.

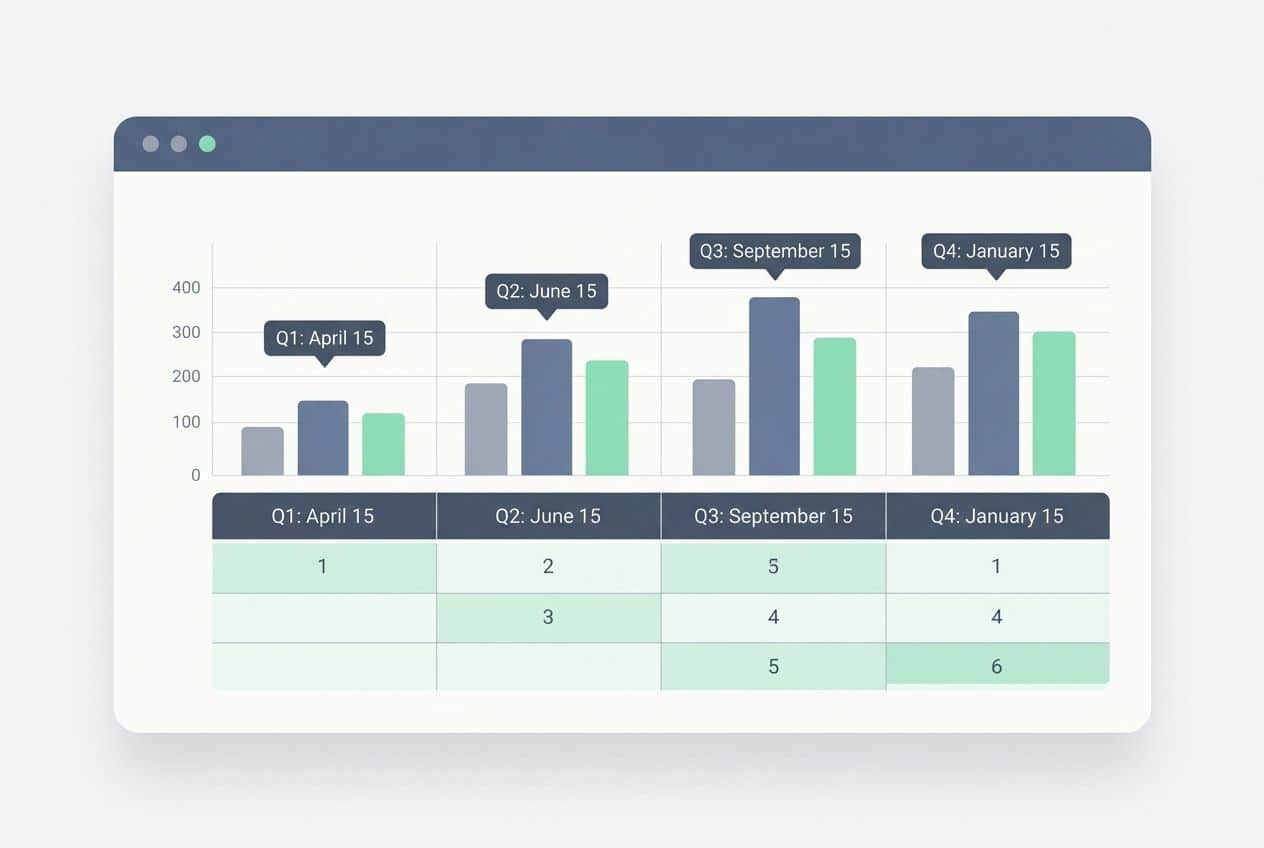

Deadlines for quarterly payments

You face specific deadlines for quarterly tax payments as a self-employed person, so mark your calendar to stay on track.

| Quarter | Deadline | What You Need to Know |

|---|---|---|

| First quarter (January to March) | April 15 | Pay this one right after tax season kicks off, folks; miss it, and penalties add up like unwanted junk mail. |

| Second quarter (April to May) | June 15 | Summer vibes hit, but don’t let beach dreams distract you; get this in to keep the IRS off your back. |

| Third quarter (June to August) | September 15 | Back-to-school time reminds you to handle this; think of it as homework that saves you money in fines. |

| Fourth quarter (September to December) | January 15 of the next year | The new year starts with this deadline; pay up early to avoid that nagging feeling, like forgetting your keys. |

With those dates locked in, explore key tax deductions for the self-employed next.

Key Tax Deductions for the Self-Employed

As a self-employed hustler, you juggle a lot, and smart deductions act like your secret weapon against hefty tax bills. Picture slashing your taxes with everyday business perks, and stick around to uncover how these gems work in your favor.

Claiming the home office deduction

Self-employed folks often turn their homes into workspaces, and that’s where the home office deduction shines. This tax deduction lets you subtract part of your home costs from your income tax.

You qualify if you use a specific area just for business, like a spare room or corner desk. Measure that space, then figure out its share of your whole home. Deduct things like rent, utilities, or mortgage interest based on that percentage.

Track business expenses here to keep your records straight. Freelancers and independent contractors love this perk, as it cuts down on tax obligations.

Pick between two ways to claim it for your tax return. The simple method gives you $5 per square foot, up to 300 square feet. Or go with actual costs for a bigger break if you have high bills.

Keep good records of your setup and use, in case the IRS asks. This deduction boosts your cash flow by lowering what you owe. Many self-employed people pair it with retirement planning to save even more. Stay on top of Schedule C when you file.

Health insurance premiums can eat into your cash flow as a freelancer or independent contractor. You deduct them directly from your income tax, which lowers your tax obligations without itemizing.

Imagine you’re running your own show, and this deduction acts like a safety net for your wallet. Claim premiums for yourself, your spouse, and dependents, as long as you paid them out of pocket.

The IRS lets you take this on Schedule 1 of your tax return, making it a smart move in your tax planning arsenal.

This tax deduction covers plans like marketplace insurance or private policies, but skip it if you qualify for an employer’s plan through a spouse. Track those payments with solid record keeping, folks; it ties right into managing business expenses.

Imagine dodging extra income tax hits by treating health coverage as a legit self-employment perk. Pair it with retirement planning for even bigger savings down the line.

Tracking business mileage and travel expenses

After sorting out those health insurance premiums as a solid tax deduction, you can shift gears to another money-saver for self-employed folks. Track your business mileage and travel expenses correctly, and you’ll cut your tax bill big time.

Business trips add up fast in your freelance life. They count as key tax deductions if you log them well.

- Choose your method for claiming mileage: go with the standard rate or actual costs. The IRS sets the standard mileage rate at 67 cents per mile for 2024, up from 65.5 cents in 2023. This rate covers gas, repairs, and wear on your car for business use. Pick this if you hate math; it simplifies your tax return. Or, tally actual expenses like fuel and maintenance for a bigger deduction sometimes. Track every detail to back up your Schedule C form.

- Keep a detailed mileage log to prove your claims. Note the date, purpose, starting point, ending spot, and miles for each business drive. Apps like MileIQ or QuickBooks Self-Employed make this easy with automatic tracking. Skip personal errands in your records; mix-ups lead to audits. Solid logs protect your cash flow and slash income tax owed.

- Deduct travel expenses beyond just mileage for out-of-town work. Cover airfare, hotels, and meals at 50% if they tie to your independent contractor gigs. Say you fly to a client meeting in another state; log receipts for the flight and lodging as business expenses. Use tools like Expensify to scan and organize everything. This boosts your deductions and supports smart financial planning.

- Watch for home-to-office drives that don’t qualify. Trips from your home office to a job site count, but commuting to a regular workplace might not. Picture a freelancer driving to a coffee shop for a quick client chat; that mileage is deductible if it’s business. Check IRS rules to avoid the hobby trap on your tax return. Accurate tracking ensures you claim every legit deduction without hassle.

- Factor in parking fees and tolls as part of travel costs. Add these to your mileage log for a fuller picture of expenses. For example, if you pay $20 to park at a networking event, deduct it fully. This small stuff piles up over the year in your accounting. Pair it with retirement planning deductions for even better tax strategies.

Deducting costs for equipment and supplies

Self-employed folks, you get to claim tax deductions for equipment and supplies that keep your business running. Think of computers, office chairs, or even paper clips, as long as they tie to your work.

Track those business expenses with receipts, and list them on Schedule C of your tax return. This cuts your income tax bill, freeing up cash flow for more fun stuff, like that retirement plan you’ve eyed.

Imagine: You buy a new printer for client invoices, no sweat, deduct the full cost if it’s under $2,500, or spread it out over years for bigger items. Freelancers and independent contractors, mix in some accounting support to sort these out right.

Avoid mixing personal buys, though; the IRS watches that. Deduct health gear too, if it fits your gig, boosting those self-employment tax strategies.

Advanced Tax Strategies

6. Advanced Tax Strategies: Hey, if you’re ready to level up your tax game like a pro chess player timing their moves, think about shifting income and expenses around the calendar, chatting with a tax whiz for insider tips, or even switching to an S-Corp setup to slash those self-employment taxes—stick around for the full scoop on making these work for you.

Plan income and expenses with timing in mind

Smart tax planning for self-employed folks often hinges on timing your income and expenses just right. Shift big purchases to the end of the year, and you might boost your business expenses deduction on your Schedule C form.

Delay invoicing clients until January, if cash flow allows, to push taxable income into the next tax return period. This move can lower your current income tax bill, especially if you expect a higher tax bracket soon.

Picture a freelance graphic designer who times equipment buys for December. She deducts those costs right away, shrinking her self-employment tax obligations. Independent contractors, listen up, small tweaks like this keep your financial planning sharp and reduce surprises during tax season.

Track everything with solid record keeping, and you’ll sail through tax strategies without the headache.

Consider engaging a tax professional

Timing your income and expenses smartly keeps cash flow steady, but sometimes you need expert eyes on the details. Think about hiring a tax professional for your self-employment journey.

These pros handle complex tax strategies, like maximizing deductions on your Schedule C. They spot overlooked business expenses, from accounting support to retirement planning. Imagine chatting with someone who turns tax headaches into smooth sailing, saving you money and stress.

Freelancers and independent contractors often juggle tax obligations alone, yet a tax advisor brings fresh ideas. They guide you through income tax rules, ensuring accurate estimated taxes.

Imagine a quick consult reveals ways to boost your financial planning. With their help, track cash flow better and avoid costly slips in record keeping. Engaging one feels like having a trusted sidekick in the tax return game.

Assess the advantages of S-Corporation status

Switch to S-Corporation status if you run your own business as a freelance or independent contractor. This setup lets profits pass through to your personal tax return, avoiding corporate income tax.

You pay yourself a reasonable salary, subject to income tax and self-employment tax. Remaining profits come as distributions, free from self-employment tax. Imagine slicing your tax bill like a pie, keeping more for cash flow. Self-employed folks often save big on taxes this way.

S-Corporations boost retirement planning, too. Contribute more to a retirement plan, like a SEP-IRA, based on your salary. This cuts your taxable income through deductions. Handle accounting with care to meet IRS rules on Schedule C or similar forms.

Weigh costs, like filing extra paperwork for your tax return. Many see better financial planning in general, dodging high estimated taxes. Talk to a pro about fitting this into your tax strategies.

Avoiding Common Tax Mistakes

Self-employed life feels like juggling chainsaws, and one wrong move with taxes can slice into your profits, so steer clear of blurring lines between hobbies and real business to keep the IRS off your back.

Picture mixing up a family dinner expense as a client meeting, that slip-up lands you in hot water, but smart habits like double-checking records turn those risks into smooth sailing for your wallet.

The IRS hobby trap

Fall into the IRS hobby trap, and you lose big on tax deductions. This rule hits when the IRS sees your freelance gig as a hobby, not a real business. They check if you aim for profit.

Run your self-employment like a side hustle without tracking income tax properly, and deductions vanish. Picture pouring cash into supplies, only to claim zero on your tax return. Ouch, right? Focus on the profit motive to dodge this pit.

Show consistent efforts, like keeping solid records of business expenses and cash flow. Many folks trip here by mixing personal fun with work. Say you love photography and sell a few prints, but the IRS questions your intent. They look at factors like time spent and financial planning.

Claim Schedule C deductions only if you treat it as true self-employment. Laugh it off as a pastime, and estimated taxes bite harder. Stay sharp, document everything, and prove you’re in it to win.

Misclassifying personal and business expenses

Self-employed folks often mix up personal and business expenses, leading to big tax headaches. Spot this mistake early to keep your tax return clean and avoid IRS audits.

- You deduct business expenses on Schedule C, but personal ones don’t count, so label them right to claim valid tax deductions.

- Imagine grabbing lunch with a client; that meal qualifies as a business expense if you discuss work, yet a family dinner out won’t fly as a deduction.

- Track mileage for freelance gigs carefully; use a log to show trips for client meetings, not your daily commute, to support your tax planning.

- Health club fees sound like self-employment perks, but the IRS sees them as personal unless your job demands peak fitness, like a trainer.

- Home internet bills split between work and streaming shows; allocate only the business portion to avoid misclassifying and messing up your income tax.

- Buying a new laptop for your independent contractor tasks counts fully, but adding personal software turns part of it into a non-deductible expense.

- Gifts to clients boost relationships and qualify for deductions up to $25 per person, while presents for friends stay personal and off your tax return.

- Cell phone costs get deducted based on business use percentage; estimate it honestly to steer clear of cash flow issues from audits.

- Office supplies like paper and pens deduct easily from your freelancing setup, but school supplies for kids belong in personal spending.

- Travel expenses for a conference are deductible if tied to your self-employment, yet a vacation disguised as a business trip raises red flags with the IRS.

- Accounting software aids in sorting expenses; invest in it to prevent errors and strengthen your general tax strategies.

- Retirement plan contributions are deducted as business expenses when you set them up properly, unlike personal savings, which don’t help your tax obligations.

Considering Professional Tax Assistance

Taxes can twist you up like a pretzel when you’re flying solo in business, right? Grab a tax advisor to spot those hidden deductions, or try user-friendly software that keeps your books straight and stress low—dive deeper for the full scoop.

Benefits of working with a tax advisor

Working with a tax advisor brings real peace of mind for self-employed folks like you. They spot deductions you might miss, such as those for home offices or business expenses. Imagine you chat about your freelance gigs, and they crunch the numbers to lower your income tax bill.

Advisors handle Schedule C forms with ease, keeping your tax return on point. You save hours that you can pour back into your work. Plus, they guide you on retirement plans, boosting your long-term cash flow.

Advisors excel at estimated taxes, helping you avoid nasty surprises from the IRS. They review your records, suggest smart tax strategies, and track your income with precision. Imagine dodging penalties by nailing those quarterly payments.

Self-employment taxes feel less scary with their support. They offer accounting tips specific to independent contractors. You gain confidence in your financial planning, focusing more on growing your business.

Tools and software for self-employed tax planning

Tools simplify tax planning for self-employed folks like you. They keep your cash flow smooth and help with deductions without the headache.

- QuickBooks Self-Employed tracks income and expenses for freelancers, categorizing them automatically to make Schedule C filing a breeze, and it even estimates quarterly taxes to avoid surprises.

- TurboTax Self-Employed guides independent contractors through tax returns with step-by-step questions, spotting deductions like business expenses and home office setups you might miss on your own.

- FreshBooks handles accounting support by invoicing clients and logging mileage, which boosts your cash flow management and supports retirement planning through easy expense reports.

- Wave offers free tools for tracking business expenses and generating reports, perfect for small self-employment gigs where you need to monitor income tax obligations without extra costs.

- TaxAct provides affordable software for estimated tax calculations, helping you plan ahead for deadlines and integrate retirement plan contributions into your general financial planning.

- H&R Block software focuses on tax strategies for self-employed users, with features that deduct health insurance premiums and equipment costs, turning complex tax obligations into manageable tasks.

With these options in your toolkit, shift gears to some final thoughts on wrapping up your tax planning journey.

Final Thoughts

You’ve tackled self-employment taxes, from grasping those quarterly payments to snagging key deductions like home office perks and mileage tracking. These steps keep things simple and smart, saving you time and cash without the headaches.

What if you started estimating your income today, or jotted down those expenses right now? Smart tax planning boosts your bottom line, dodging IRS pitfalls and fueling your freelance dreams.

Check out tools like QuickBooks or chat with a pro for extra help, and kick off your plan with confidence, because you’ve got this.

FAQs on Self-Employed Tax Planning

1. Hey, what’s the first step in tax planning if I’m self-employed?

Start by tracking all your business costs, like supplies and travel. This helps you spot deductions that cut your bill. Think of it as finding hidden treasure in your receipts.

2. Do I need to pay taxes every quarter as a freelancer?

Yes, send in estimated payments four times a year to avoid penalties. It’s like paying rent on time, keeps the IRS happy.

3. What deductions can I claim for my home office?

You can deduct part of your rent or utilities if you use a space just for work. Picture your desk as a mini business zone, and claim costs tied to it; just keep good records.

4. How does saving for retirement help with my taxes?

Set up a solo 401(k) or SEP IRA to lower your taxable income. It’s a smart move, like planting seeds for a future harvest, and you get tax breaks now.