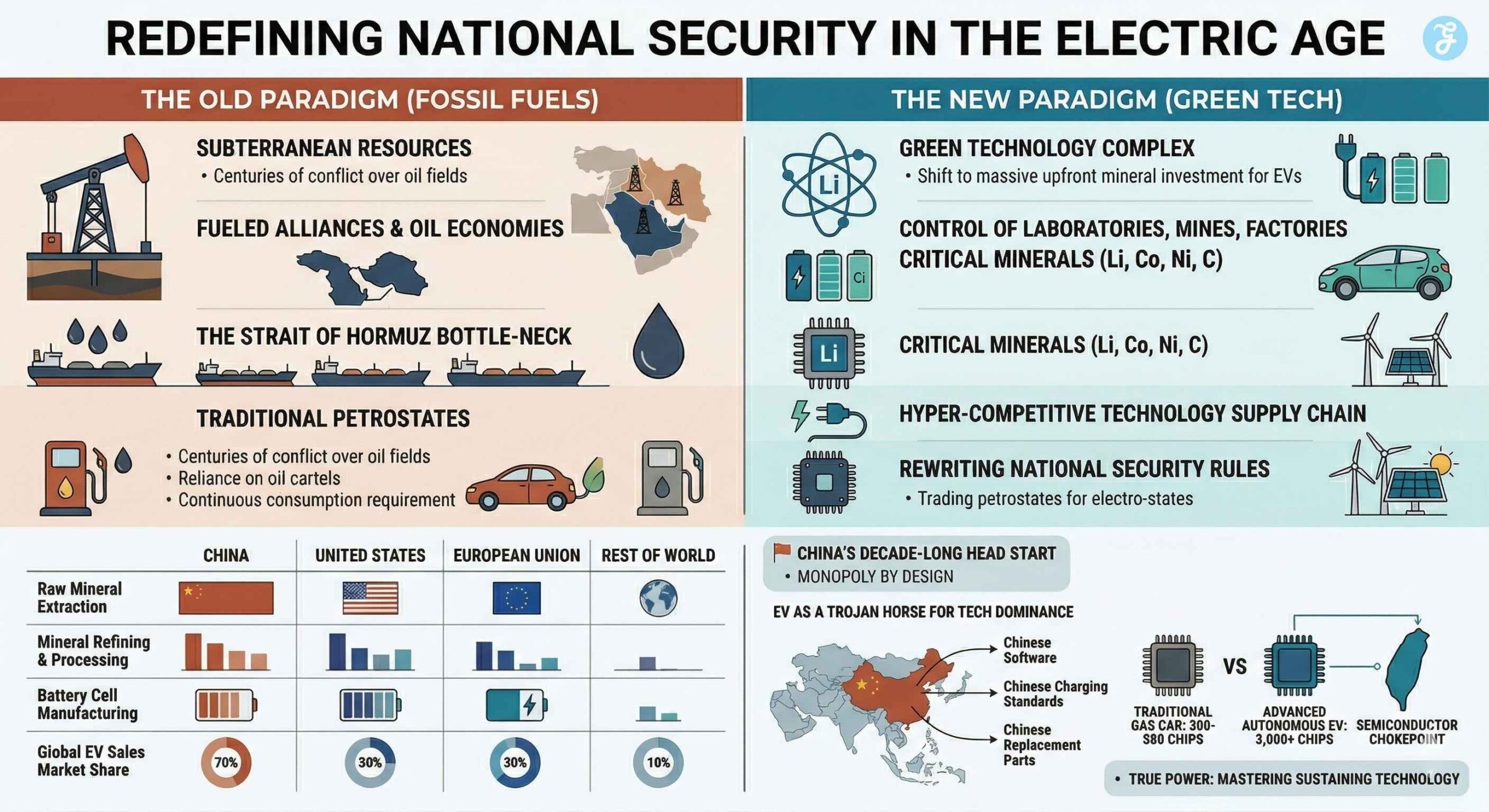

We are officially in the thick of a Green Tech Cold War, a high-stakes geopolitical standoff where the ammunition is not artillery, but lithium, cobalt, and semiconductor chips. As the world rapidly transitions from gasoline-powered vehicles to electric mobility, the very foundation of global power is shifting beneath our feet. For a century, nations fought over the Middle Eastern oil fields that fueled our economies and dictated international alliances.

Today, that scramble has been replaced by a desperate race to control the complex technologies and critical minerals that power modern electric vehicles (EVs). This shift is undeniably necessary to combat climate change, but it introduces terrifying new vulnerabilities.

We are trading our reliance on traditional petrostates for a deep dependence on a highly concentrated, hyper-competitive technology supply chain, fundamentally rewriting the rules of national security in the 21st century.

Redefining National Security in the Electric Age

To understand the modern geopolitical landscape, we must first recognize that the transition to electric vehicles has permanently altered the definition of global supremacy. Power is moving away from subterranean fossil fuels and toward the laboratories, mines, and factories developing green technology. This is no longer merely an ecological imperative; it is the ultimate strategic battleground of our time.

The Illusion of Energy Independence

For decades, Western political rhetoric has championed green energy as the ultimate path to “energy independence.” The logic seemed sound: if we harvest the sun, wind, and power our cars with electricity generated at home, we no longer need to bow to the whims of oil cartels. However, this is a dangerous illusion.

Transitioning to green tech does not erase global dependencies; it merely relocates them. A gas-powered car requires oil, which is continuously consumed and must be constantly replenished. An EV, conversely, is a massive upfront investment of critical minerals. While you do not need to “refill” a battery with lithium every week, the sheer volume of raw materials required to build a national fleet of EVs creates a severe, front-loaded supply chain dependency.

Instead of worrying about tankers passing through the Strait of Hormuz, national security advisors are now losing sleep over graphite mining operations in Africa, lithium brine extraction in South America, and nickel processing in Indonesia. We are trading petrostates for electro-states.

The nations that sit on these vast mineral reserves, and more importantly, the nations that possess the infrastructure to refine them into usable battery components, now hold the keys to the global economy.

China’s Decade-Long Head Start: Monopoly by Design

The narrative of this new era is dominated by an undisputed heavyweight. Beijing did not just participate in the green transition; it systematically engineered a monopoly over its foundational elements while the rest of the world was still debating the viability of electric cars.

Owning the Supply Chain from Mine to Motor

China’s dominance is not accidental; it is the result of a coordinated, state-sponsored industrial strategy executed over more than fifteen years. While Western legacy automakers were focused on squeezing the last drops of efficiency out of internal combustion engines, China was quietly buying up mineral rights across the globe and building massive refining infrastructure at home.

By January 2026, CATL’s global market share surged to 45.2%, while BYD held 13.8%. Together, just two Chinese companies control 59% of the entire global EV battery market. When factoring in other Chinese manufacturers (like CALB, Gotion, and Eve Energy), Chinese enterprises now control over 70% of total global EV battery installations, up from roughly 50% in 2021.

To illustrate the sheer scale of this dominance, consider the current distribution of the EV supply chain across major global players.

Estimated Global Control of the EV Supply Chain:

| Supply Chain Stage | China | United States | European Union | Rest of World |

| Raw Mineral Extraction | 15% | 5% | 2% | 78% |

| Mineral Refining & Processing | 70% – 85% | 10% | 5% | 10% |

| Battery Cell Manufacturing | 75% | 10% | 8% | 7% |

| Global EV Sales Market Share | 60% | 12% | 18% | 10% |

This table reveals the most critical bottleneck: refining. Even if the United States or Europe secures raw lithium from allied nations in South America or Australia, those minerals almost always have to be shipped to China to be processed into battery-grade materials before they can be used in a factory.

Chinese capital and technical expertise, particularly from companies like the Tsingshan Holding Group, have been the primary drivers behind Indonesia’s massive surge in high-pressure acid leaching (HPAL) nickel processing. Because these facilities are crucial for producing battery-grade nickel, counting Indonesia’s output as entirely independent from China is a statistical illusion. The geopolitical control extends far beyond the geographic borders.

The EV as a Trojan Horse for Tech Dominance

Transitioning from hardware to global strategy, the EV has become Beijing’s most potent geopolitical tool. Because their domestic market is heavily saturated and subsidized by the state, Chinese automakers, led by giants like BYD, have achieved economies of scale that Western manufacturers simply cannot match.

They are producing high-quality, ultra-affordable EVs and flooding the global market. But this is not just about selling cars; it is about expanding geopolitical influence. China is actively investing in EV infrastructure, charging networks, and local manufacturing plants across Southeast Asia, Latin America, and the Middle East.

By providing the affordable green technology that the Global South desperately needs to modernize, Beijing is cementing long-term trade partnerships and pulling these developing regions deeper into its economic orbit. The affordable Chinese EV acts as a Trojan Horse, establishing reliance on Chinese software, Chinese charging standards, and Chinese replacement parts for decades to come.

The Western Counter-Offensive: Tariffs, Subsidies, and Desperation

Having awakened to the reality of China’s dominance, the West has adopted a fiercely reactionary posture. The US and Europe face a brutal paradox: they urgently need cheap electric vehicles to meet their ambitious climate targets, but importing those cheap vehicles from their biggest geopolitical rival will destroy their domestic automotive industries.

Washington’s Fortress Economy and the IRA

The United States has opted for a strategy of economic isolationism, attempting to brute-force a domestic supply chain into existence. The cornerstone of this strategy is the Inflation Reduction Act (IRA), a piece of legislation that relies heavily on protectionist policies to separate the American automotive market from Chinese influence.

The IRA offers massive tax credits to consumers who buy EVs, but only if those vehicles, and the batteries inside them, are assembled in North America using minerals sourced from the US or its free-trade allies. It is a legislative fortress designed to starve Chinese companies of American consumer dollars while artificially incubating a local battery industry.

However, this “Fortress Economy” approach is incredibly expensive and slow. Building new mines and refineries in the US takes years, largely due to stringent environmental regulations and local opposition. Washington is discovering that you cannot simply legislate a multi-billion-dollar, highly technical supply chain into existence overnight.

Europe’s Existential Auto Crisis

Across the Atlantic, the European dilemma is even more acute. The automotive industry is the undisputed crown jewel of the European economy, particularly in Germany. Millions of high-paying jobs rely on the manufacturing of internal combustion engine vehicles.

As the EU mandates a shift to zero-emission vehicles by the 2030s, European automakers find themselves completely outpaced by the cost-efficiency of Chinese imports. To prevent their auto industry from being hollowed out, the EU has weaponized trade policy, slapping aggressive tariffs on Chinese-made EVs.

This creates a severe friction point. European consumers, battered by inflation, want affordable electric cars. By blocking cheap imports through tariffs, the EU is essentially forcing its citizens to pay a premium for green tech, potentially slowing down domestic EV adoption and jeopardizing the continent’s own climate goals in the name of economic self-preservation.

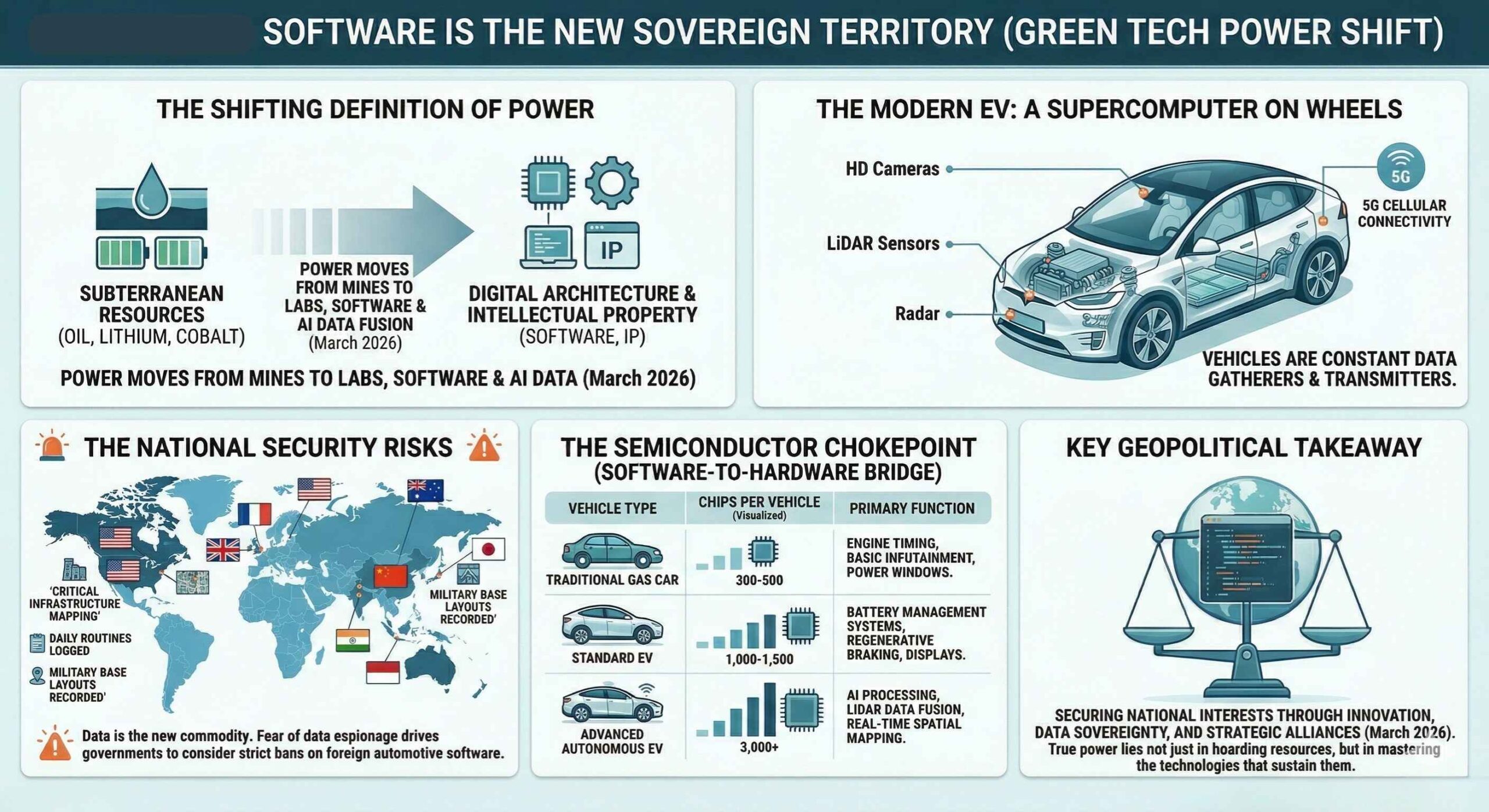

Software is the New Sovereign Territory

The discourse surrounding the Green Tech Cold War often fixates on physical resources, mines, gigafactories, and batteries. However, the true battleground of this era lies in the digital architecture and intellectual property that operate these vehicles.

Autonomous Driving and Data Espionage

We must stop thinking of the modern electric vehicle as a car; it is, in reality, a supercomputer on wheels. Today’s EVs are equipped with dozens of high-definition cameras, LiDAR sensors, radar, and constant cellular connectivity. They map their surroundings with pinpoint accuracy to enable autonomous driving features.

This raises monumental national security alarms. If millions of foreign-manufactured vehicles are driving on domestic streets, they are actively gathering terabytes of data: mapping critical infrastructure, logging daily routines, and recording the layout of military bases or government facilities.

In a world where data is the most valuable commodity, the nation that controls the software inside the vehicle controls an unprecedented intelligence-gathering network. The fear of data espionage is driving governments to consider strict bans on foreign automotive software, pushing the global market toward a fragmented, heavily regulated tech ecosystem.

The Semiconductor Chokepoint

Connecting the software to the hardware is the semiconductor industry, which represents the most fragile and highly contested chokepoint in the green tech revolution. Without microchips, an EV is just a heavy piece of metal.

The transition to electric and autonomous driving requires an exponential increase in processing power. To understand the gravity of this bottleneck, we can compare the computing requirements of different vehicle generations.

The Silicon Shift: Estimated Semiconductor Requirements

| Vehicle Type | Average Number of Chips per Vehicle | Primary Function of Chips |

| Traditional Gas-Powered Car | 300 – 500 | Engine timing, basic infotainment, and power windows. |

| Standard Electric Vehicle | 1,000 – 1,500 | Battery management systems, regenerative braking, and displays. |

| Advanced Autonomous EV | 3,000+ | AI processing, LiDAR data fusion, and real-time spatial mapping. |

This immense reliance on semiconductors ties the automotive industry’s fate directly to Taiwan, which manufactures the vast majority of the world’s advanced chips. The geopolitical tension surrounding the Taiwan Strait is not just a regional dispute; it is an existential threat to the global automotive supply chain.

A disruption in chip manufacturing would immediately halt the production of green technology worldwide, proving that technological supply chains are far more brittle than the oil pipelines of the past.

Winning the Climate War While Surviving the Tech Cold War

As the rhetoric escalates and trade barriers rise, the global community must find a way to navigate this precarious new world order without sacrificing the planet in the process. The friction between national security and climate survival is the defining challenge of our generation.

The True Cost of Decoupling

The harsh reality is that a complete decoupling of Western and Eastern supply chains is likely impossible, and attempting it will inflict massive economic collateral damage. Strict isolationism and endless tariff wars artificially inflate the cost of green technology.

If Western nations refuse to leverage existing, highly efficient Asian supply chains, the global transition to sustainable energy will become too expensive for the average consumer and too slow to avert environmental catastrophe. We cannot afford to let protectionism derail the climate timeline.

The atmosphere does not care where a battery was manufactured; it only cares about the reduction of carbon emissions.

Forging a Pragmatic Path Forward

To survive the Green Tech Cold War, Western policymakers must abandon the zero-sum mentality and embrace a more pragmatic, localized strategy. Instead of trying to replicate China’s dominance in raw mineral refining, a race they have already lost, the US and Europe should focus their capital on next-generation innovation.

This means investing heavily in solid-state battery technology, which promises higher density and safety without the same reliance on rare earth metals. It means establishing aggressive, closed-loop battery recycling industries to extract valuable minerals from old EVs, turning domestic scrapyards into the “mines” of the future. It also requires forging strategic, mutually beneficial partnerships with mineral-rich emerging markets in Africa and South America, offering them technology transfers and local manufacturing opportunities rather than just extracting their resources.

Finally: Steering Toward a New Global Balance

The shift to electric vehicles is the defining geopolitical chessboard of our time. While the race for critical minerals and semiconductor dominance presents unprecedented national security challenges, we cannot let the Green Tech Cold War derail our climate goals. Western nations must pivot from defensive protectionism to proactive innovation, focusing on next-generation battery technology and robust domestic recycling networks.

Securing our global future requires recognizing that true power in the 21st century lies not in hoarding physical resources, but in mastering the technology that sustains them. The road ahead is undeniably complex, but with strategic foresight and pragmatic diplomacy, we can win both the climate war and the technological race.