The Australian financial landscape in 2026 continues to favor those who utilize sophisticated structures to manage their wealth. A discretionary trust remains the most popular vehicle for families looking to protect assets while optimizing their annual tax obligations. While the Australian Taxation Office has increased its oversight, the core benefits of these structures remain incredibly powerful for those who understand how to deploy them.

How We Selected Our 5 Best Trust Strategies

To determine the most effective approaches for modern wealth management, we evaluated the current legal landscape and common financial bottlenecks facing Australians today.

We filtered these strategies based on three core criteria. First, we looked at absolute compliance with current ATO directives to ensure safety. Second, we measured the potential for long term tax reduction across a family unit. Third, we prioritized methods that offer dual benefits in both wealth accumulation and legal liability shielding.

The Top 5 Ways To Use Family Trusts for Legal Tax Planning This Year

Understanding the specific mechanics of a trust is the first step toward effective long term wealth management. Below is our breakdown of the most powerful strategies available to Australian taxpayers right now.

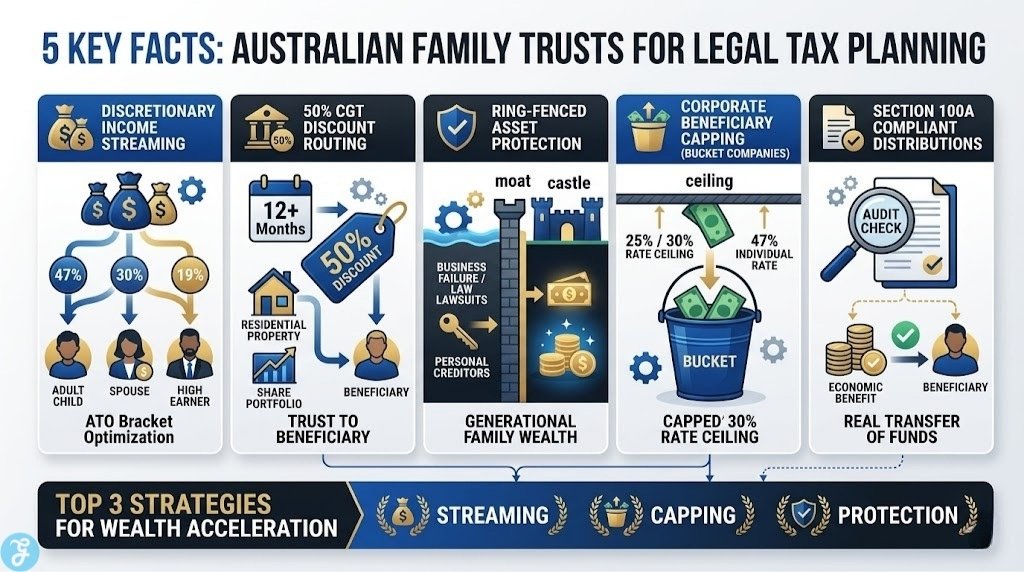

1. Discretionary Income Streaming

The most significant advantage of a discretionary trust is the ability to choose how income is distributed each year. This process is known as income streaming and it allows the trustee to allocate profits to family members who are in lower tax brackets. If a high income earner is already in the 47 percent top tax bracket, the trust can instead distribute investment income to a spouse or an adult child with a lower personal income. This strategy ensures that the family unit pays the lowest possible amount of tax on its collective earnings.

Best Feature/For:

-

Families with a mix of high and low income earners

Why We Chose It:

-

Provides immediate and legally compliant tax reduction

-

Maximizes the amount of cash retained within the family unit for reinvestment

Things to consider:

-

Requires precise annual trustee resolutions completed before June 30

To build on annual tax savings, we must also look at how trusts handle the sale of major assets.

2. The 50 Percent CGT Discount Routing

When an individual holds an investment for more than twelve months, they typically qualify for a significant reduction in their taxable gain upon sale. A major structural benefit is that a trust can pass this 50 percent Capital Gains Tax discount directly through to the individual beneficiaries. Unlike a company structure which is ineligible for this specific discount, a trust allows the gain to remain discounted when it reaches the taxpayer. This makes it an ideal vehicle for holding high growth assets like residential property or diversified share portfolios.

Best Feature/For:

-

Long term investors holding high yield property or equities

Why We Chose It:

-

Halves the assessable tax burden on major liquidity events

-

Outperforms standard corporate structures for holding appreciating assets

Things to consider:

-

Assets must be held by the trust for a minimum of 12 months to qualify

Beyond just tax, it is vital to understand how these structures defend the wealth you accumulate.

3. Ring Fenced Asset Protection

Tax planning is most effective when it is combined with robust asset protection to defend the principal capital. Because a beneficiary does not personally own the underlying assets held within a trust, those assets are generally shielded from personal creditors or legal claims. In the event that a family member faces a professional negligence claim or a business failure, the capital within the trust remains legally insulated. This decoupling of ownership is a cornerstone of professional wealth strategy in Australia.

Best Feature/For:

-

Business owners, company directors, and high risk medical professionals

Why We Chose It:

-

Separates personal financial liability from generational family wealth

-

Ensures tax effective reinvestment strategies are not derailed by lawsuits

Things to consider:

-

The protection can be pierced if the trust is found to be a sham setup

When all family members are earning high incomes, a different routing strategy is required.

4. Corporate Beneficiary Capping (Bucket Companies)

There are instances where every individual in a family is already earning a high income and pushing money to them is tax inefficient. In these cases, many Australians use a corporate beneficiary which is commonly referred to as a bucket company. The trustee distributes trust profits to this company where the tax rate is permanently capped at the corporate level of 25 or 30 percent. This allows the family to keep more capital within a controlled environment for future investment activities instead of losing 47 percent to the ATO.

Best Feature/For:

-

High net worth families maxing out their individual tax brackets

Why We Chose It:

-

Places a hard ceiling on the maximum tax rate paid on trust profits

-

Creates a private internal bank for the family to fund future ventures

Things to consider:

-

Requires strict Division 7A loan agreements if the trust wants to use the company cash

Finally, none of these strategies matter if they do not hold up under regulatory scrutiny.

5. Section 100A Compliant Distributions

The benefits of a trust are only available to those who maintain strict legal and accounting compliance in the modern era. The Australian Taxation Office is currently heavily focused on Section 100A which prevents artificial tax avoidance schemes and reimbursement agreements. A valid distribution must involve a real transfer of benefit to the beneficiary rather than just using them as a paper tax shield. Accurate documentation is mandatory to ensure that the setup is not invalidated during an audit.

Best Feature/For:

-

Anyone actively distributing trust income to adult children or extended family

Why We Chose It:

-

Essential for surviving an ATO audit

-

Defines the boundary between legal tax planning and illegal tax evasion

Things to consider:

-

Beneficiaries must actually receive the economic benefit of the funds distributed to them

With the individual strategies defined, let us look at how they compare holistically.

An Overview Of 5 Family Trusts for Legal Tax Planning Strategies

To help you visualize how these strategies interact, we have compiled a matrix detailing their primary mechanisms.

Overview Comparison Table

Below is a direct comparison of the five strategies based on their primary function and target user base.

| Strategy Name | Primary Function | Ideal Target User | Setup Complexity |

| Discretionary Income Streaming | Annual tax bracket optimization | Families with varied incomes | Low |

| CGT Discount Routing | Minimizing tax on asset sales | Property and share investors | Low |

| Asset Protection | Shielding capital from litigation | Business owners and directors | Medium |

| Bucket Companies | Capping maximum tax rates | High net worth family groups | High |

| Section 100A Compliance | Audit survival and legality | All trust operators | High |

Understanding all options is important, but a few stand out above the rest.

Our Top 3 Picks and Why?

While all five strategies are vital for a holistic financial plan, three specific implementations provide the highest immediate value.

-

Discretionary Income Streaming: We rank this first because it provides the most immediate, year over year cash flow benefit for the average Australian family by legally manipulating tax brackets.

-

Corporate Beneficiary Capping: This takes the second spot as it is the ultimate wealth acceleration tool for high earners, allowing them to reinvest capital at a 25 percent tax rate instead of 47 percent.

-

Ring Fenced Asset Protection: This is our third top pick because tax savings are useless if you lose the underlying asset to a lawsuit. It provides the necessary defensive moat for the first two offensive strategies.

Now that we have reviewed the top picks, you need to know how to apply them to your specific situation.

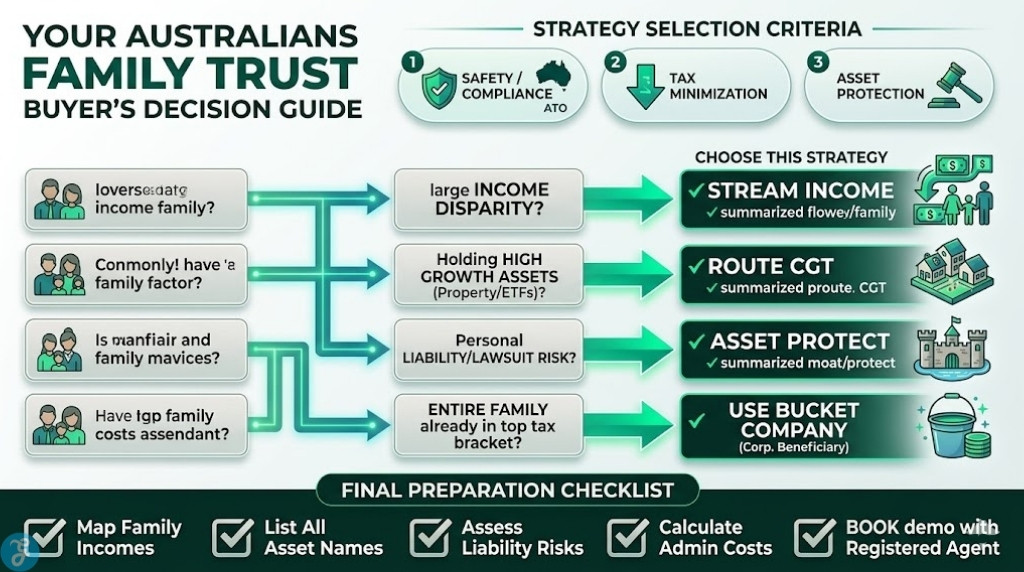

Buyer’s Guide: How to Choose the Right Family Trusts for Legal Tax Planning by Yourself?

Selecting the right strategy depends entirely on your current phase of wealth creation and your family dynamics.

Here is the core selection framework you should use to evaluate your needs:

-

Income Disparity: Assess the gap between the highest and lowest earners in your family to see if streaming is viable.

-

Asset Type: Determine if you are holding cash flowing businesses or high growth capital assets.

-

Risk Profile: Evaluate your personal exposure to lawsuits, bankruptcy, or professional negligence claims.

-

Administrative Tolerance: Consider how much accounting and legal paperwork you are willing to manage annually.

To make this easier, we have built a matrix to guide your structural choices.

Below is a decision matrix to help you match your situation with the correct trust strategy.

| Choose this strategy… | If your primary financial situation is… |

| Choose Income Streaming if… | You earn 190k+ and your spouse or adult children earn under 45k. |

| Choose CGT Routing if… | You plan to buy and hold property or ETFs for decades before selling. |

| Choose Asset Protection if… | You own a risky business or operate in a highly litigious profession. |

| Choose a Bucket Company if… | Your entire family is already paying the top marginal tax rate. |

Before you meet with an accountant, make sure you have everything prepared.

The Final Checklist:

-

Map out the estimated annual income of every adult in your immediate family.

-

List all assets currently held in your personal name versus corporate names.

-

Assess your current and future professional liability risks.

-

Calculate the administrative costs of running a trust and a potential bucket company.

-

Book a consultation with a registered tax agent to draft a compliant trust deed.

Securing Your Financial Future With A Trust

Family trusts offer unparalleled flexibility for income distribution and asset protection in the Australian market. By understanding the mechanisms of income streaming, corporate beneficiaries, and strict compliance, you can legally optimize your tax position. You should review your specific financial goals with a qualified professional before the end of the financial year to ensure your structures are optimized for 2026.