You earn big bucks, but does your money work as hard as you do? Many high earners face this puzzle. They pull in six figures or more, yet watch wealth slip away. Taxes bite hard. Bad investments flop. Life throws curveballs like job changes or family needs. It’s like chasing a leaky bucket; the cash flows in, but it drips out fast. No wonder stress builds up. Imagine a friend who scored a huge bonus, only to blow it on fancy toys without a plan.

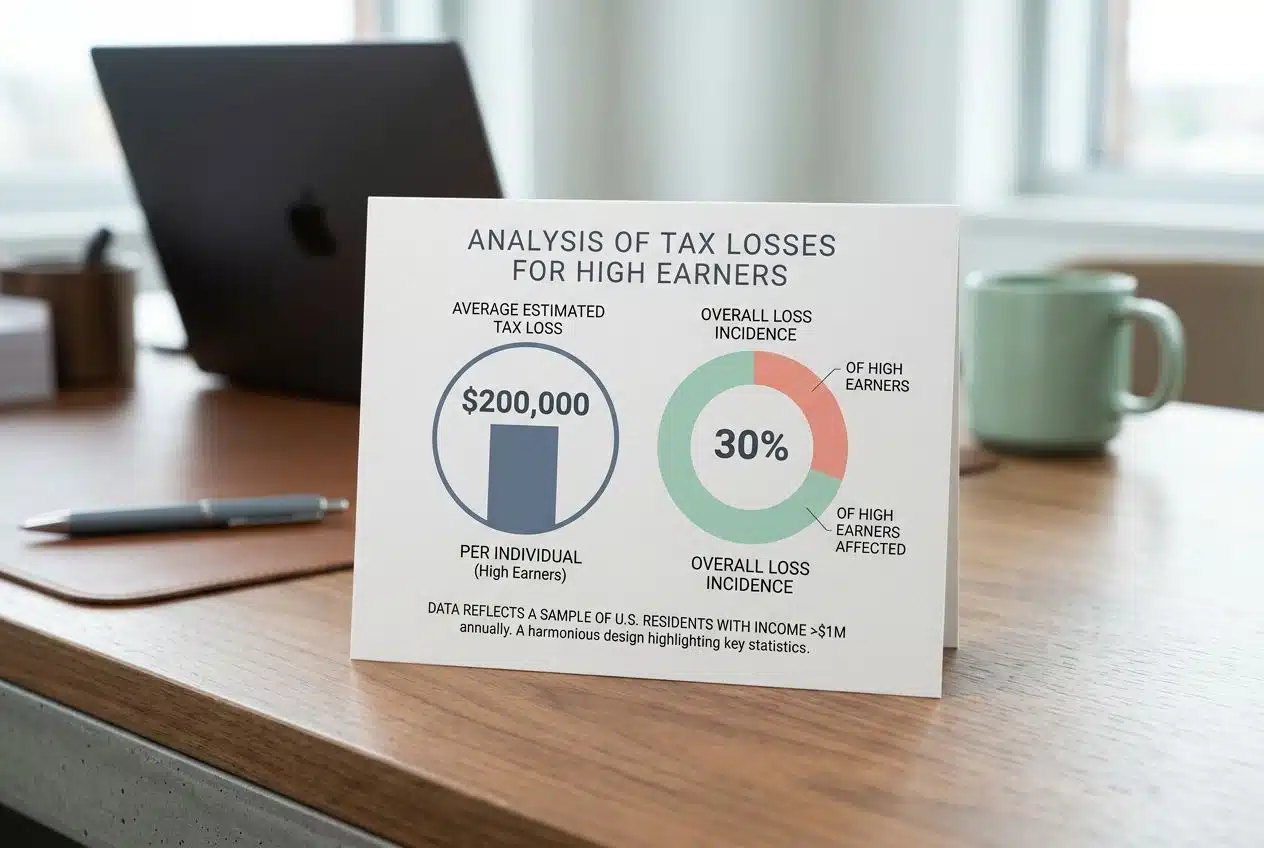

Sound familiar? Did you know that folks with incomes over $200,000 often lose 30% or more to taxes without smart moves? This fact hits home for many. Our blog explores the best Wealth Management Strategies for high earners.

We break them down step by step, with tips to build, protect, and grow your fortune. From goal setting to tax tricks, you’ll get tools that fit your busy life. Stick around. You’ll thank yourself later.

What is Wealth Management?

Wealth management acts as your money’s best friend, handling everything from investments to taxes with a sharp eye on growth. Curious about how it stands apart from regular financial advice?

Definition and Importance

High earners often juggle high incomes, yet managing that money can feel like herding cats. Wealth management steps in as a smart way to handle your finances. It covers financial planning, investment strategies, and tax efficiency all in one go.

Imagine it’s like having a skilled captain steer your ship through stormy seas, keeping your assets safe. This approach helps high-net-worth individuals grow and protect their money over time.

Folks with hefty paychecks need it most, since simple savings won’t cut it. Estate planning fits in here, too, making sure your legacy lasts. Diversification plays a key role, spreading risks across different investments.

Retirement planning gets a boost, setting you up for those golden years. Asset allocation keeps everything balanced, like a well-mixed cocktail.

Think about John, a tech exec pulling in $500,000 a year, who ignored wealth management at first. He lost big in one bad stock pick. Now, with proper strategies, he sleeps easily knowing his portfolio management shields him.

High-income earners face unique challenges, like lifestyle inflation creeping up. Wealth preservation becomes vital, guarding against market dips. Risk management acts as your safety net, catching falls before they hurt.

Tax optimization saves you thousands, legally trimming what you owe. Income diversification adds extra streams, like side gigs or rentals. Portfolio rebalancing keeps things fresh, adjusting as needed. High net worth folks, you deserve this peace; it turns stress into confidence.

Key Differences Between Wealth Managers and Financial Managers

You know, sorting out wealth managers from financial managers can feel like comparing apples to oranges, but it boils down to their focus and services.

| Aspect | Wealth Managers | Financial Managers |

|---|---|---|

| Client Focus | They target high-net-worth folks, often with millions in assets. | They serve a wider crowd, from everyday savers to mid-level investors. |

| Services Offered | They provide full-spectrum advice, like estate planning, tax strategies, and even lifestyle perks. | They stick to basics, such as budgeting, retirement plans, and simple investments. |

| Approach Style | They craft custom plans, acting like a personal finance quarterback for the wealthy. | They offer standard guidance, more like a coach for general money goals. |

| Fee Structure | They charge based on assets under management, sometimes with performance bonuses. | They use flat fees or hourly rates, keeping things straightforward and affordable. |

| Expertise Level | They dive deep into complex issues, including trusts and international investments. | They handle everyday finances, focusing on debt reduction and basic savings. |

With those distinctions in mind, let’s move on to the strategic necessities that high earners really need.

Strategic Wealth Management Necessities for High Earners

High-income earners face distinct challenges in wealth management. They often deal with complex tax situations and high lifestyle demands. Financial planning becomes key to handling these issues.

Think of it like steering a big ship through rough waters; you need strong tools to stay on course. Investment strategies must focus on diversification to spread risk. Tax efficiency helps keep more money in your pocket.

Estate planning protects your legacy for future generations. High-net-worth individuals benefit from retirement planning that matches their earnings. Asset allocation plays a big role in balancing growth and safety.

Income diversification guards against job loss or market dips. Avoid lifestyle inflation, that sneaky habit of spending more as you earn more. Portfolio management keeps everything in check with regular tweaks.

People with high incomes need strong risk management to shield their assets. They should prioritize wealth preservation amid market ups and downs. A retirement strategy involves smart saving and investing early.

Use goal-based investing to target specific dreams, like buying a vacation home. Professional advice from wealth managers guides these choices. Family offices offer customized support for the ultra-wealthy.

Online tools make tracking easier, but a personal touch matters. High earners juggle multiple income streams, so coordination is vital. Empathy comes in here; building wealth can feel overwhelming, but small steps lead to big wins. A dash of humor: don’t let your money work harder than you do, or it might run away!

The rich invest in time, the poor invest in money. – Warren Buffett

Foundational Principles of Effective Wealth Management

Picture your wealth as a sturdy house, you build it with smart planning to chase dreams, shield it from storms to keep assets safe, and nurture it to grow riches over time. Life throws curveballs like job shifts or family surprises, so tweak your money moves to stay on track, and watch your fortune thrive.

Planning, Protecting, and Prospering

High earners often build wealth through smart steps. Start with planning. Set your goals for retirement or buying a home. Use financial planning to map out income and expenses. Think of it like charting a course on a treasure map, avoiding pitfalls along the way.

Diversify your assets to spread risk. Asset allocation matters here. High-net-worth individuals succeed by aligning plans with their lifestyle.

Protecting your wealth comes next. Guard against market drops or unexpected events. Risk management keeps your portfolio safe. Consider tax efficiency to minimize what you owe. Estate planning ensures your legacy passes smoothly to loved ones.

Prospering builds on this base. Grow your investments with strategies like goal-based investing. Retirement planning helps you thrive long-term. Wealth preservation turns earnings into lasting security.

Adapting Financial Strategies to Life’s Changes

Life throws curveballs at everyone, and your financial plan must flex with them. Imagine landing a big promotion, that boosts your income but also spikes your taxes. You adjust your tax efficiency strategies right away to keep more cash in your pocket.

Or picture starting a family, and suddenly estate planning jumps to the top of your list. Smart high-income earners tweak their wealth management approach, matching it to these shifts.

Diversification helps too, spreading investments across assets to weather market storms. Stay proactive, and your portfolio management stays strong through ups and downs.

Job loss hits hard, yet it opens doors to rethink retirement planning. Dust off your financial planning blueprint, cut back on lifestyle inflation to protect your nest egg. A friend once ignored market dips, lost big, but learned to rebalance his asset allocation fast.

You can do the same, incorporating risk management to safeguard wealth preservation. Chat with advisors about income diversification; it cushions blows from career changes. Keep adapting, your investment strategies evolve with life’s twists, building lasting security.

8 Essential Wealth Management Strategies for High Earners

High earners often juggle big bucks and bigger dreams, so smart moves can turn your cash flow into a lasting empire. Imagine, like a captain steering through stormy seas, these tactics keep your wealth on course, ready to explore them.

1. Establish Clear Financial Goals

Set clear financial goals to steer your wealth management journey. Picture your future like a roadmap, where you mark spots for buying a dream home or funding kids’ college. High earners often juggle big dreams, so start by listing short-term wins, like building an emergency fund, and long-term aims, such as retirement planning.

This step fuels your financial planning and keeps investment strategies on track.

Make goals specific and measurable to avoid vague wishes. For instance, aim to save $500,000 for estate planning in five years, not just “get rich.” Tie them to tax efficiency by factoring in deductions, and blend in diversification to protect against market dips.

Chat with a spouse or advisor about these targets; it sparks ideas and builds commitment. This approach turns high-income earners into masters of their wealth preservation.

2. Develop a Comprehensive Financial Plan

High earners like you often juggle high incomes with even bigger dreams. A solid financial plan acts as your roadmap to turn those dreams into reality.

- Assess your current financial situation, including income, expenses, assets, and debts, to build a strong foundation for your wealth management journey. Visualize it: you’re the captain of a ship, and without knowing your exact position, you can’t chart a course to Treasure Island. High-income earners, think about tracking your net worth annually; it helps spot leaks in your budget, like that sneaky lifestyle inflation creeping in.

- Set specific, measurable goals for short-term wins and long-term visions, such as buying a vacation home or funding kids’ college. You know the saying, “A goal without a plan is just a wish,” right? Tie these to your retirement strategy, maybe aiming for $5 million in assets by age 60, and watch how it motivates you to push harder.

- Build an emergency fund covering six to twelve months of living expenses, stashed in a high-yield savings account. Life throws curveballs, folks, like a sudden job shift or market dip. For high-net-worth individuals, this buffer prevents dipping into investments during tough times, keeping your portfolio management on track.

- Diversify income streams beyond your main job, perhaps through real estate or side ventures, to combat risks from job loss. Imagine your income as a basket of eggs; don’t put them all in one spot. High earners often add rental properties or dividend stocks, boosting financial planning and reducing reliance on a single paycheck.

- Incorporate tax efficiency by using accounts like 401(k)s or IRAs to minimize what Uncle Sam takes. Taxes can eat into your wealth like termites in a wooden house. Consult strategies such as Roth conversions, which high-income earners use to pay taxes now at lower rates, preserving more for estate planning later.

- Plan for retirement by calculating needs based on lifestyle and expected lifespan, adjusting for inflation. You deserve to kick back without worries, don’t you? Factor in Social Security, pensions, and investments; many high-net-worth folks target 4% withdrawal rates to make savings last.

- Address risk management with insurance for health, life, and disability, protecting your assets from unforeseen events. Think of insurance as your financial shield in a storm. High earners, you might need umbrella policies for extra coverage, ensuring wealth preservation even if lawsuits come knocking.

- Include estate planning elements, like wills and trusts, to pass on your legacy smoothly. Nobody wants family feuds over inheritance, after all. Designate beneficiaries on accounts, and for high-income earners, consider charitable trusts to cut taxes while doing good.

- Review your plan yearly or after big life changes, like marriage or a new baby, to keep it aligned with your evolving world. Flexibility is key, my friend; a stale plan gathers dust. Adjust asset allocation as needed, ensuring your investment strategies stay sharp and effective.

3. Diversify Your Investment Portfolio

Diversification acts as your safety net in the investment world. Spread your money across stocks, bonds, real estate, and even commodities. This approach cuts risk if one area tanks.

Think of it like not putting all your eggs in one basket, a classic idiom that saves high-income earners from big losses. Asset allocation plays a key role here, balancing growth with stability. Mix in some international investments too, for that extra layer of protection against local market dips.

Picture a friend who only bet on tech stocks, then watched them crash. Ouch, right? Avoid that trap by building a varied portfolio. Include index funds for broad exposure, or add alternative assets like gold.

Tax efficiency comes into play when you diversify smartly, shielding more of your wealth. Portfolio management keeps things in check, adjusting as markets shift. High net worth individuals often thrive this way, turning potential pitfalls into steady gains.

4. Incorporate Tax-Efficient Strategies

High earners often pay big taxes on their income and investments. You can cut those taxes with smart moves. Think of tax efficiency as a shield for your wealth. Use accounts like 401(k)s or IRAs to defer taxes.

Put money in municipal bonds; they offer tax-free interest. High-income earners save thousands this way each year. Harvest tax losses by selling underperforming stocks to offset gains. This keeps more cash in your pocket.

Charity giving boosts tax breaks, too. Donate appreciated assets instead of cash; skip capital gains taxes. Roth conversions shift funds for tax-free growth later. These steps fit into your comprehensive financial planning.

Tax optimization protects your retirement strategy from unnecessary hits. Now, let’s talk about how to plan for estate and legacy considerations.

5. Plan for Estate and Legacy Considerations

After optimizing your taxes through smart strategies, shift your focus to estate planning, which secures your legacy for future generations. Imagine you’ve built a solid fortune, but without a plan, it could vanish in probate fees or family disputes.

High-net-worth individuals often use wills and trusts to pass on assets smoothly. They avoid common pitfalls like outdated documents that lead to hefty estate taxes. Think of it as planting a family tree that bears fruit long after you’re gone, protecting your hard-earned wealth.

Estate planning goes beyond paperwork; it involves open talks with loved ones about your wishes. Use tools like living trusts to dodge court hassles and ensure privacy. For high-income earners, this means factoring in charitable giving to cut taxes while building a meaningful legacy.

Diversify your approach by naming beneficiaries on accounts, which speeds up transfers. Stay proactive, update plans as life changes, and watch your wealth preservation efforts pay off in peace of mind for everyone involved.

6. Leverage Goal-Based Investing

Goal-based investing ties your money moves to specific life targets, like buying a dream home or funding kids’ college. You set clear aims first, then pick investments that match those dreams.

This approach beats random stock picks; it keeps you focused and motivated. Imagine aiming for retirement at 55, so you pour funds into growth stocks and bonds that align with that timeline. High-income earners often use this strategy to dodge lifestyle inflation, ensuring every dollar works toward real wins.

Picture your portfolio as a roadmap, not just a pile of assets. You assign buckets for short-term needs, like a family vacation, and long-term ones, such as estate planning. Diversify across asset allocation to cut risks, while weaving in tax efficiency for bigger gains.

One client I know targeted early retirement; he leveraged robo-advisors to track progress, adjusting as markets shifted. This method builds wealth preservation, turning high earnings into lasting security without the guesswork.

7. Regularly Review and Rebalance Your Portfolio

High earners like you know that markets shift fast. Regular reviews keep your portfolio on track for wealth preservation.

- Check your investments quarterly to spot any drift from your asset allocation goals. You might find stocks have surged, throwing off your balance. Adjust by selling some winners and buying underperformers. This step in portfolio management cuts risks and boosts returns over time. Think of it as tuning a car engine; skip it, and you risk a breakdown during tough economic rides.

- Use tools like online platforms for quick portfolio scans. They show real-time data on diversification and performance. Spot issues early, say if bonds lag behind inflation. Rebalance then to match your risk tolerance. High net worth individuals often see better outcomes this way, avoiding emotional decisions in volatile times.

- Factor in life changes, like a new job or family addition, during reviews. These can alter your retirement planning needs. Update your strategy to include tax efficiency tweaks. For example, shift assets to minimize capital gains hits. It’s like recalibrating a compass; stay pointed to long-term wealth goals.

- Track fees and costs eating into your returns. High-income earners sometimes overlook these in busy lives. Review statements to cut unnecessary expenses. Rebalance to low-cost index funds for better efficiency. Picture your portfolio as a garden; weed out the drags to let investments flourish.

- Compare your portfolio against benchmarks, such as the S&P 500. This reveals if your investment strategies underperform. Make data-driven shifts, perhaps adding international assets for more diversification. Estate planning ties in here too; ensure allocations support legacy goals without big tax burdens.

- Involve a professional advisor for deeper insights during rebalancing. They spot blind spots you might miss. Discuss income diversification to hedge against job loss risks. This collaborative approach builds peace of mind, turning complex portfolio management into a smoother ride.

- Set reminders for annual thorough reviews beyond quarterly checks. Analyze trends in risk management and market shifts. Adjust for things like lifestyle inflation creeping up. High earners often benefit from this habit, preserving wealth through ups and downs.

8. Seek Professional Financial Advice

Wealth managers bring sharp skills to your financial planning. They spot risks you might miss in investment strategies. Imagine a trusted advisor helps with tax efficiency and asset allocation.

You gain from their know-how on portfolio management. Pros often save you money in the long run. Think of it as having a co-pilot for your wealth journey.

Many high-income earners turn to experts for estate planning and retirement strategy. These advisors customize plans to fit your life. They handle diversification and risk management with ease. Chat with one, and watch your wealth preservation soar. You deserve that edge in building a secure future.

Tools and Resources for Wealth Management

Picture your wealth as a garden that needs the right tools to thrive, and you’ll find options that fit like a glove. Online platforms simplify tracking your assets, robo-advisors handle investments with smart algorithms, and family offices offer personalized service for those big portfolios—dive deeper to pick what suits you best.

Online Financial Planning Platforms

High earners often turn to online financial planning platforms for easy access to smart tools.

| Platform Type | Key Features | Why It Helps You |

|---|---|---|

| Budget trackers like Mint | They link your accounts, track spending, and set budgets automatically. | You spot leaks in your cash flow fast, like finding money hidden in couch cushions. |

| Investment apps such as Betterment | They offer automated portfolios, tax-loss harvesting, and goal setting. | Your money grows without daily hassle, giving you more time for golf swings. |

| Full-service sites like Personal Capital | They provide dashboards for net worth, retirement planners, and advisor chats. | You see your big picture clearly, avoiding surprises that sting like a bee. |

| Goal-oriented tools from Vanguard | They include calculators for savings, debt payoff, and emergency funds. | You build wealth step by step, turning dreams into reality without the sweat. |

| Free resources on Fidelity’s site | They deliver market insights, webinars, and portfolio analyzers. | You learn as you go, boosting confidence like a trusted friend at your side. |

Robo-Advisors and Automated Tools

Robo-advisors and automated tools simplify wealth management for busy high earners like you, offering smart tech to handle investments without the hassle.

| Tool Type | Key Features | Benefits for High Earners | Popular Examples |

|---|---|---|---|

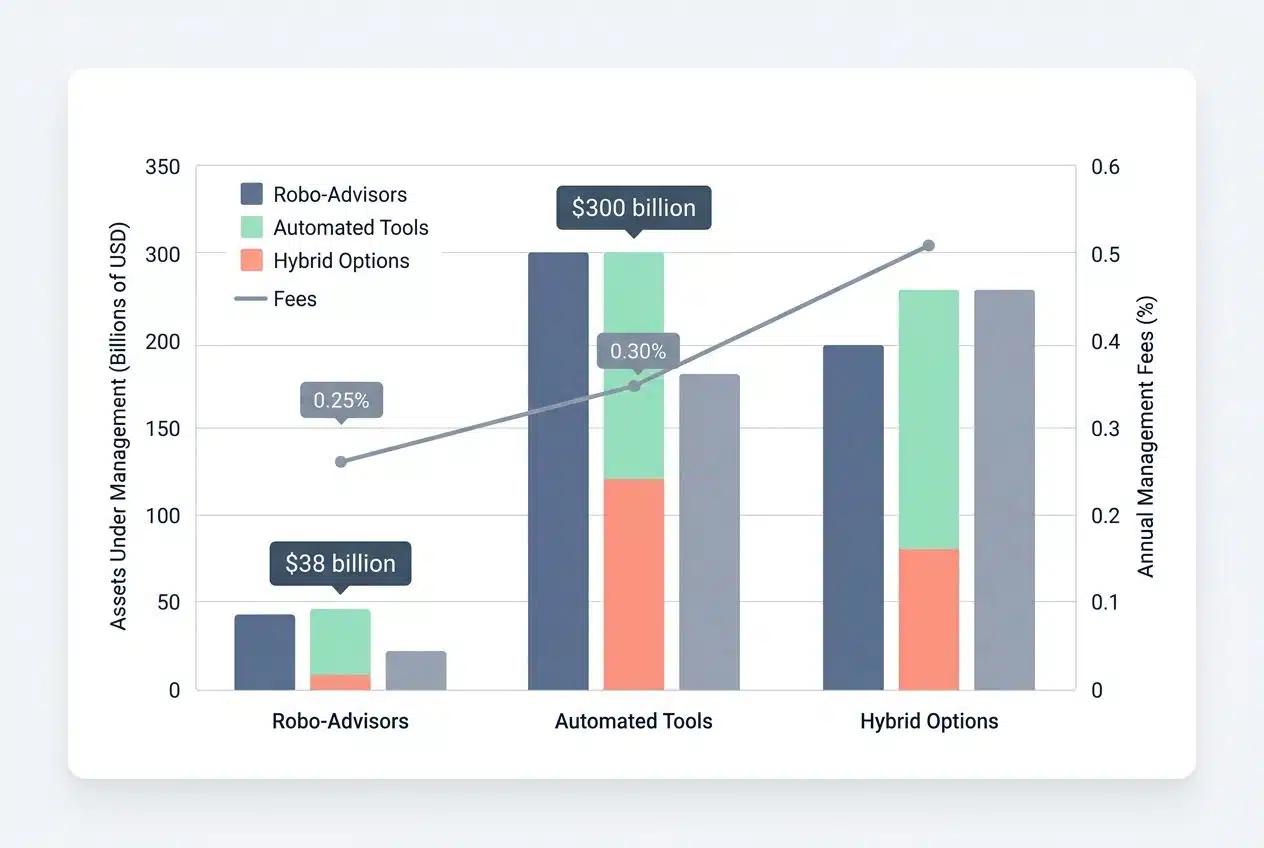

| Robo-Advisors | These platforms use algorithms to build and manage your portfolio, based on your risk tolerance and goals. They automate rebalancing and tax-loss harvesting. | You get low-cost advice, often under 0.25% in fees, saving time while growing wealth efficiently. Imagine sipping coffee as your money works harder. | Betterment handles over $38 billion in assets as of 2023. Wealthfront manages $50 billion, focusing on tech-savvy users. |

| Automated Tools | Apps and software track expenses, forecast cash flow, and suggest optimizations. They integrate with bank accounts for real-time insights. | High earners cut taxes and spot opportunities fast, like a personal finance sidekick whispering smart moves. No more guesswork in volatile markets. | Personal Capital tracks $25 billion in assets, offering free tools. Mint by Intuit monitors budgets for millions since 2006. |

| Hybrid Options | Combine robo-tech with human advisors for custom tweaks. Vanguard’s version blends automation with expert calls. | You enjoy tech efficiency plus empathy for complex needs, like planning a big estate. It’s like having a robot butler with a heart. | Vanguard Personal Advisor Services oversees $300 billion, charging just 0.30% for balances over $5 million. |

Family Offices and Private Banking

Family offices serve high-net-worth individuals with custom services. They handle everything from investment strategies to estate planning. Think of them as a one-stop shop for your wealth needs.

High-income earners often use them to protect assets and grow wealth. Private banking offers similar perks through big banks. These include special loans and tax efficiency advice. Both options focus on wealth preservation and risk management.

Imagine a team that knows your financial story inside out. They help with asset allocation and retirement planning. Many high earners pick family offices for that personal touch. Private banking suits those who want bank backing. Explore what fits your life. Now, consider factors to think about when choosing a wealth manager.

Factors to Consider When Choosing a Wealth Manager

Picking a wealth manager feels like choosing a trusted co-pilot for your financial journey, so weigh their track record, fees, and client vibes carefully to avoid turbulence down the road. Craving deeper insights? Explore the rest of this guide!

Credentials and Expertise

Credentials matter a lot in wealth management for high-net-worth individuals. Look for certifications like CFP or CFA, which show deep knowledge in financial planning and investment strategies.

These pros handle complex tax efficiency and estate planning with skill. Imagine hiring a pilot without a license; you want someone proven to steer your portfolio management right. High-income earners often pick experts with years of experience in asset allocation and risk management.

Expertise goes beyond just papers on the wall. Seek advisors who specialize in retirement planning and wealth preservation for folks like you. They should understand income diversification to fight lifestyle inflation.

Chat with them about real cases they’ve tackled; this reveals their grasp on diversification and portfolio management. Empathy helps too, as they guide you through tough spots with a touch of humor to ease the stress.

Fee Structures and Costs

Once you’ve checked a wealth manager’s credentials and expertise, turn your attention to their fee structures and costs, because these directly impact your wealth preservation. Managers often charge in different ways. Some use a flat fee for services. Others take a percentage of your assets under management, typically around 1% per year for high-net-worth individuals.

You might see hourly rates too, especially for specific advice on financial planning or tax efficiency. Watch out for hidden costs, like transaction fees or expense ratios in your investment strategies. Think of it like shopping for a car; you don’t just look at the sticker price, you check the total cost of ownership.

Compare options to find what fits your retirement planning and estate planning needs. Fee-only advisors avoid commissions, which can reduce conflicts of interest. In contrast, commission-based ones earn from products they sell, potentially skewing their portfolio management advice.

High-income earners, you deserve transparency here. Ask for a clear breakdown upfront. This step helps with asset allocation and risk management, keeping more money in your pocket over time. A funny thing happens when fees eat into returns; it’s like a slow leak in your wealth boat, so patch it early.

Reputation and Client Reviews

Reputation matters a lot in wealth management. High-income earners like you need a wealth manager with a solid track record. Check online reviews from past clients. They share real stories about service quality.

Look for patterns in feedback on sites like Google or Yelp. Positive comments often highlight strong financial planning and tax efficiency. Negative ones might flag poor communication or high fees. Think of it as reading restaurant reviews before a big dinner; you want to avoid a bad experience.

Client reviews reveal the true picture of a wealth manager’s skills in areas like estate planning and portfolio management. Talk to current clients if you can. Ask about their experiences with asset allocation and retirement planning.

A good reputation builds trust, much like a reliable old friend. High-net-worth individuals often share anecdotes in forums. Use these insights to spot red flags early. This step helps you pick someone who truly gets your investment strategies and wealth preservation needs.

Benefits of Effective Wealth Management

Think of your finances as a well-oiled machine, humming along without a hitch, shielding you from life’s curveballs and building a fortress around your hard-earned cash. You lock in that steady security, keep your legacy thriving across years, and kick back with real calm, knowing your moves pay off big time—stick around to see how these perks unfold in your world.

Increased Financial Security

High earners often face big risks with their money. Wealth management steps in like a sturdy shield. It guards your assets against market dips and surprise costs. Imagine dodging a financial storm because you planned ahead.

You build a safety net through smart asset allocation and risk management. This approach keeps your wealth steady, even in tough times.

Picture your finances as a well-oiled machine. Effective strategies boost your security by mixing diversification with tax efficiency. High-net-worth individuals sleep better at night.

They know their retirement planning and estate planning are solid. You gain control over income diversification, avoiding lifestyle inflation pitfalls. Professional advice turns worries into wins.

Long-Term Wealth Preservation

With increased financial security in place, you set the stage for long-term wealth preservation, keeping your assets safe across generations. Think of it like planting a sturdy oak tree that withstands storms, year after year.

Wealth preservation guards your hard-earned money against inflation, market dips, and unexpected life twists. You focus on strategies like estate planning and asset allocation to shield your fortune.

Diversify investments, folks, to spread risk and maintain growth. Imagine your portfolio as a balanced meal, with stocks, bonds, and real estate providing nutrition for the future.

High-income earners often use tax efficiency to minimize losses and boost legacy goals. Retirement planning plays a key role here, ensuring funds last through golden years. Portfolio management helps you adjust as needs change, like tweaking a sailboat’s course in shifting winds.

Seek ways to combat lifestyle inflation, that sneaky thief eroding savings. Income diversification adds another layer, creating multiple streams to flow steadily. This approach delivers peace, knowing your wealth endures for family and causes you cherish.

Greater Peace of Mind

Effective wealth management frees you from constant money worries. Imagine sleeping soundly, knowing your financial planning covers emergencies and dreams alike. High-income earners often face stress from volatile markets, but solid investment strategies build a safety net.

You gain confidence, like a captain steering through calm seas. Tax efficiency plays a big role here, cutting unnecessary losses that eat at your peace. Estate planning ensures your loved ones stay secure, with no surprises down the road.

Envision diversification in your portfolio management, acting as a shield against risks. Retirement planning turns distant goals into reachable milestones, easing daily pressures. Wealth preservation becomes second nature, letting you enjoy life more.

High net worth individuals report less anxiety with these tools in place. Asset allocation keeps things balanced, so you focus on what matters most. This approach delivers true calm, day in and day out.

The Closing Thoughts

You take charge of your wealth, and that’s a smart move for high-income earners. Imagine this: you build a strong financial plan, mix in smart investment strategies, and add a dash of tax efficiency.

Estate planning fits right in, like the cherry on top. High-net-worth folks often juggle asset allocation with retirement planning. They focus on wealth preservation and risk management, too.

Diversification keeps things steady, you know? Portfolio management helps you sleep better at night. Think about income diversification to beat lifestyle inflation. High earners, you deserve that peace from solid strategies. Chat with pros for personalized advice, and watch your future brighten.

FAQs on Wealth Management Strategies

1. What top strategies help high earners manage wealth?

High earners, you know, often dive into smart investing like a kid in a candy store; spread your bets across stocks, real estate, and bonds to keep risks low and growth steady.

2. How does tax planning fit into wealth management for the rich?

Picture taxes as that sneaky thief in the night. Smart high earners dodge big hits by using deductions and retirement accounts. It keeps more cash in your pocket for the long haul.

3. Why bother with estate planning as a high earner?

Estate planning acts like a safety net for your fortune. It makes sure your loved ones get what you want without a mess. Plus, it cuts down on those hefty taxes that could eat up your legacy.

4. Can diversification really boost wealth for top earners?

Yes, diversification spreads your eggs in many baskets, dodging big losses if one market tanks.