Imagine this: You’re an expat, sipping coffee in a cozy café abroad, but tax worries keep nagging at you. You wonder if your U.S. citizenship means you owe taxes on every penny earned overseas. Many folks face this mess, juggling tax residency rules from their home country and the new one. It feels like walking a tightrope, right? Double taxation risks pop up, and reporting foreign accounts adds to the stress.

No wonder expat tax compliance turns into a headache for so many.

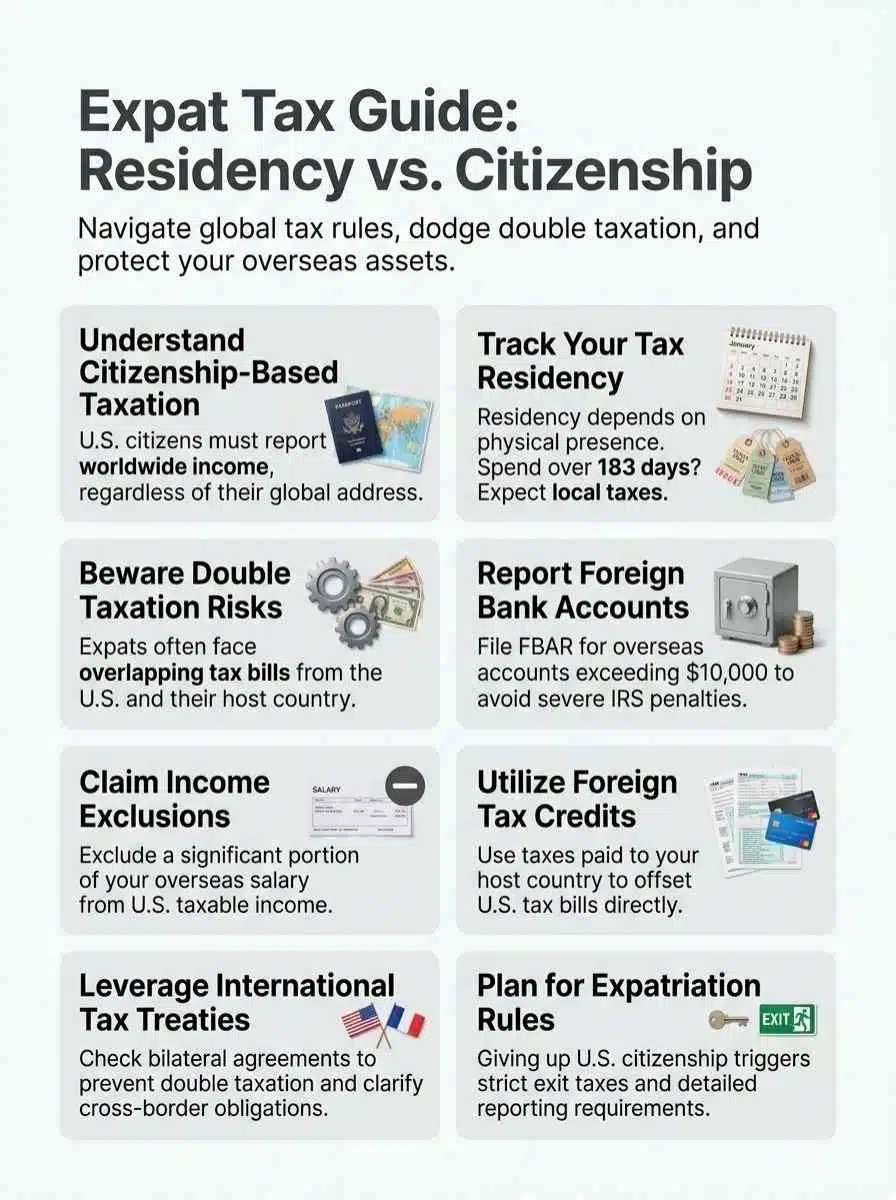

Only three countries tax based on citizenship, no matter where you live: the United States, Hungary, and Eritrea. This setup hits U.S. citizens hard, as they report worldwide income to the Internal Revenue Service.

Explaining tax obligations, foreign earned income exclusion, and foreign tax credit strategies. You’ll learn to dodge pitfalls like FBAR filings and tax treaties.

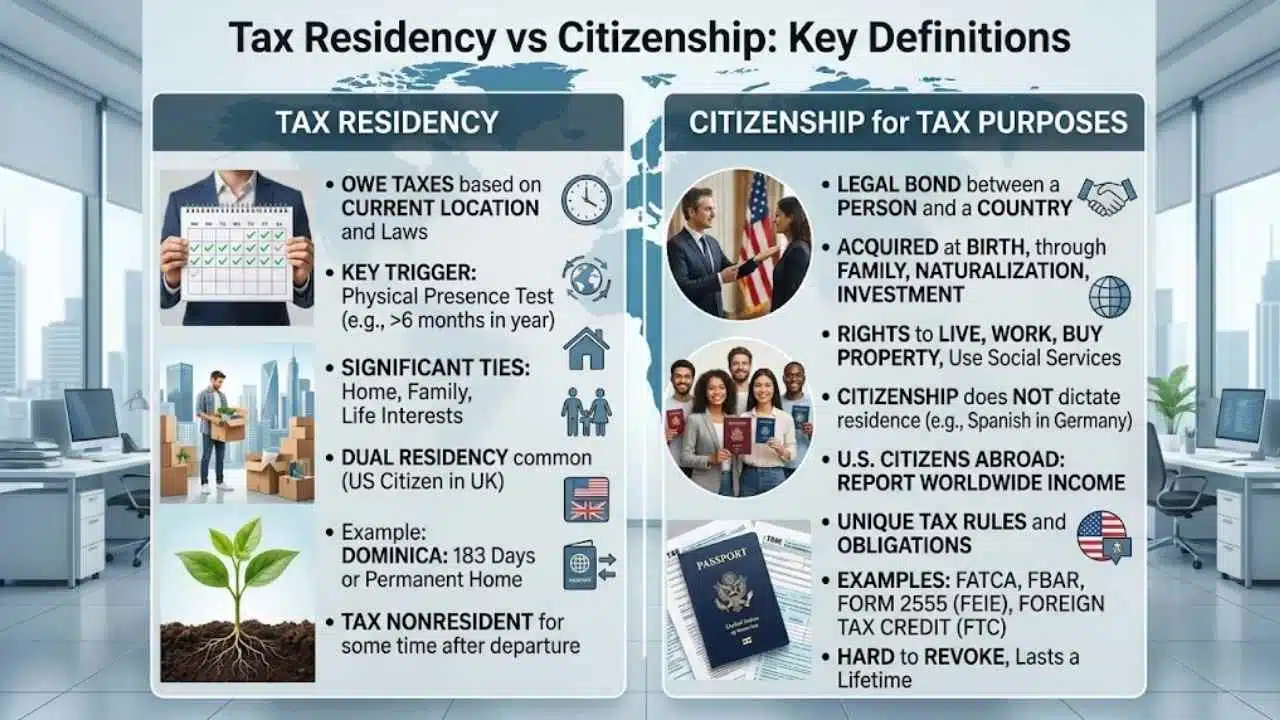

Tax Residency vs Citizenship: Key Definitions

Ever wonder why some folks pay taxes based on where they plant their feet, while others get hit no matter where they roam? Tax residency kicks in through rules like the physical presence test, tying your obligations to days spent in a country, but citizenship-based taxation, think U.S. citizens living abroad, demands you report worldwide income regardless of your address.

What is Tax Residency?

Tax residency means you owe taxes in a country based on its laws. Countries set rules for this status. You might qualify if you spend six months or more there in a year. Or, if your main life interests, like home and family, sit in that place, even with less time spent.

Picture a U.S. citizen who moves to the UK and stays over six months; both nations could claim taxes on worldwide income. Dual tax residency happens often, so one person faces rules from two spots at once.

In the Commonwealth of Dominica, you gain this status with at least 183 days of physical presence in the tax year. Set up a permanent home and live there, or hold residency from the year before or after.

Some places keep taxing non-resident citizens for a bit after they leave, say six months to a year. Residency-based taxation focuses on where you live now, not your passport. Think of it like roots in soil; your tax obligations grow from daily life ties.

Green card holders or accidental Americans deal with this mix. Use the physical presence test to check your tax status. Living abroad as a nonresident alien changes how you file a tax return.

Tools like Form 1040 help sort it out.

What is Citizenship for Tax Purposes?

Citizenship acts as a legal bond between you and a country. This status gives you the right to stay there without fear of deportation in most cases. You gain it at birth, through family ties, by naturalizing, or via citizenship by investment programs.

Naturalization demands legal entry, a stay permit, and living there for a set time. US citizens, for instance, face unique tax rules tied to this status. Citizenship lets you live and work in the nation, buy property, use social services like schools and health care, and get a passport.

It lasts a lifetime and stays hard to take away. Picture a Spanish citizen who packs up and heads to Germany for a job; their citizenship stays put, but residence shifts.

Citizenship does not dictate residence; for example, a Spanish citizen may reside and work in Germany. – Key insight from tax experts at Greenback Expat Tax Services.

This setup affects US expat tax obligations, including reporting foreign financial accounts under the Foreign Account Tax Compliance Act. You might file Form 2555 for the foreign earned income exclusion (FEIE) or use the foreign tax credit (FTC) to ease burdens.

Countries like Canada, the United Kingdom, France, and Germany have their own twists on this. US citizens abroad often deal with FBAR requirements for foreign bank account reports.

Tax treaties help, but you need to grasp host country laws to avoid penalties. Think of it as juggling two sets of rules, one from home and one from your new spot.

Key Differences Between Tax Residency and Citizenship-Based Taxation

You know, living abroad as a U.S. citizen means Uncle Sam still wants a piece of your global earnings, no matter where you hang your hat. Switch that to residency rules in most countries, and they only tax what you make locally, easing up on those FBAR reports for foreign accounts.

Basis of Tax Liability

Tax liability hits you based on where you live or your passport. Most countries tax people who reside there, no matter their citizenship. They focus on your days in the country and local earnings.

For example, you move to Spain, and Spain taxes your income from jobs there. Simple as that. But citizenship throws a curveball. Only three countries do this: the United States, Hungary, and Eritrea.

They tax citizens on worldwide income, regardless of residency status. U.S. citizens abroad must file U.S. income tax returns, even from a beach in Thailand. This stems from the Internal Revenue Code, pushing U.S. expat tax obligations far and wide.

Countries might rethink this setup, thanks to pandemic-fueled economic woes.

Expats, listen up, this basis shapes your wallet big time. Residency taxation keeps things local, like tying tax to your address. Citizenship-based taxation, though, follows you everywhere.

U.S. citizenship means reporting global income on federal tax returns. Miss it, and tax penalties loom. Tools like Publication 54 and Publication 519 guide you through U.S. expat tax rules.

Think of it as a tax shadow that sticks, no escape without planning. Tax strategies, such as understanding tax treaties, help lighten the load. Stay sharp to avoid double hits on your earnings.

Global vs. Local Income Reporting

Let’s talk about how global and local income reporting differ, like comparing a world tour to a neighborhood stroll, and why it matters for you as an expat.

| Aspect | Global Income Reporting | Local Income Reporting |

|---|---|---|

| Main Idea | U.S. tax residents pay taxes on worldwide income, no matter where they live. Think of it as your earnings following you everywhere, like a loyal shadow. | Non-resident aliens pay taxes only on U.S.-connected income and U.S. source passive income, often at lower rates. It’s like taxing just the fruit from one tree in your yard. |

| Who It Applies To | Dual citizens must file U.S. tax returns, even with income only from another country. Picture a U.S. passport that keeps knocking on your door for reports. | People without U.S. residency focus on local U.S. sources. They skip the global chase and stick to what’s nearby. |

| Capital Gains Example | Residents report all capital gains worldwide. Every profit counts, from stocks in Tokyo to bonds in Berlin. | Non-resident aliens avoid taxes on most capital gains, except those from U.S. real property. Sell a house in Miami? That bites, but foreign assets slide by. |

| Double Taxation Angle | Expats risk taxes in two places on the same money. The U.S. and New Zealand tax treaty steps in to cut that double hit for cross-border earners. | Local focus means fewer overlaps. You pay once on U.S. bits, and home country handles the rest, keeping things simple. |

| Real-Life Twist | Imagine earning big in Europe as a U.S. citizen; Uncle Sam wants details on every euro. It feels like reporting to a far-off boss who never forgets. | A visitor sells art in New York; taxes hit only that sale. No need to spill about income back home, like keeping your diary private. |

How Does Citizenship-Based Taxation Work?

Uncle Sam keeps tabs on your global earnings if you hold US citizenship, taxing you wherever you roam. Expats file Form 1040 each year, and don’t forget FBAR for those overseas bank accounts over $10,000.

U.S. Citizenship Tax Rules

U.S. citizens face tax rules that stand out, folks. The system taxes worldwide income, no matter where you live. This setup started over a century ago. It applies to citizens, permanent residents like green card holders, and those who pass the substantial presence test.

They all count as U.S. tax residents. Non-resident citizens must file federal tax returns on global earnings. No flat tax rate exists here. They share the same duties as folks back home.

Think of it like a global net that catches every dollar, earned anywhere. Tax filing stays key for US citizenship, even abroad. Tools like Form 8833 help report treaty positions. Form 3520 covers foreign trusts and gifts.

Expatriation rules hit hard if you give up citizenship. A net worth of at least $2 million triggers them at the time you leave. An average annual net income tax over $136,000 in the past five years does too, with yearly tweaks.

You must prove compliance with U.S. tax laws for those five years before. Skip that, and rules apply anyway, no thresholds needed. Estate tax and gift tax factor in during planning.

FBAR reports foreign bank accounts. Use tax planning to stay compliant. Publication 17 guides you through basics.

Tax Filing Obligations for U.S. Expats

Americans abroad often juggle tax duties from multiple countries. You might feel like a juggler in a circus, keeping all those balls in the air without dropping one.

- Dual citizens face a tough spot, as they must file U.S. tax returns even if they earn all their income in another country. Imagine: you live in France, sip coffee by the Eiffel Tower, but Uncle Sam still wants his share. This rule stems from citizenship-based taxation, where the U.S. claims taxes on your worldwide income, no matter where you park your feet. Expats, listen up, this means reporting everything, from your Paris salary to that side gig in Provence. Fail to do so, and penalties pile up like unread mail.

- Expats must watch out for double taxation risks, where you pay taxes to both the U.S. and your host country on the same income. Americans living abroad may owe taxes to both the U.S. and the foreign country where their income is earned, creating a financial headache that feels like a bad hangover. To dodge this, look into tools like the Foreign Tax Credit (FTC) or tax treaties, but first, grasp how the U.S. taxes residents on worldwide income and imposes estate tax on worldwide assets, prompting some to consider expatriation as an escape hatch.

- Filing Form 8854 becomes crucial if you decide to expatriate, as this notifies the IRS of your status and cuts ties with U.S. tax obligations. Expatriates must file Form 8854 to notify the IRS of their expatriation status, or else they stay hooked to U.S. rules. Imagine sailing away from tax burdens, only to realize you forgot to untie the rope. Failure to file Form 8854 or submitting an incomplete form results in a $10,000 penalty, a steep price that hits like a surprise bill. Dual citizens, take note, this form helps you break free, but skip it, and individuals who do not file Form 8854 remain subject to U.S. tax laws even after expatriation.

- Reporting foreign accounts and assets adds another layer for U.S. expats, especially with forms like FBAR (Foreign Bank Account Report) and FinCEN Form 114. You need to disclose overseas bank accounts if they exceed certain thresholds, or face hefty fines that sting worse than a bee. The U.S. demands this to track potential tax fraud or identity theft, so use tools like EFTPS for payments and consider a CPA for guidance. Folks like Mike Wallace or Allen Pfeister from Titan Wealth International might offer insights, but always check Circular 230 for professional standards.

- Tax filing obligations include annual returns, often using Form 1040-X for amendments or Form 4868 for a tax extension. Streamlined procedures help if you’re behind, allowing you to catch up without massive penalties, like a second chance in a game. Expats, grab your EIN (Employer ID Number) if needed, and don’t forget child tax credit or earned income credit (EITC) if eligible. Services like TFX can simplify this, but watch for identity protection with an IP PIN to avoid identity theft.

- Compliance with both systems demands planning, such as understanding host country tax laws while filing U.S. forms like W-9 or W-4 for withholding. The substantial presence test determines residency, but for citizens, it’s worldwide anyway. Tools like Google Analytics or Hotjar might track your online tax prep, but focus on essentials: Form W-7 for ITIN, Form 941 for employers, or Form 4506-T for transcripts. Social media like YouTube or Facebook can provide tips, but secure sites with HTTPS and Cloudflare keep your data safe.

How Does Residency-Based Taxation Work?

Most countries tax you based on where you live, not your passport. They use rules like the Substantial Presence Test to decide if you’re a resident, and then you report income earned there, plus handle forms like Form W-9 for any U.S. ties.

Substantial Presence Test

The U.S. uses the Substantial Presence Test to figure out if someone counts as a tax resident. This test looks at days you spend in the country. You meet it if you stay at least 31 days in the current year, and your total days over three years add up to 183 or more.

Count all days this year, one-third from last year, and one-sixth from two years ago. Green card holders face expatriation rules, but only after eight years as permanent residents in the last 15.

Imagine packing your bags for a new adventure abroad, yet Uncle Sam still wants his share based on those calendar marks.

Non-green card holders who pass this test might slip into an alternate tax setup. That happens if they lived in the U.S. for three straight years, or hit 183 days each year in that span.

Some folks file Form W-9 to report income, while others use Form 2848 for help with reps. Think of it like a game of tag, where days tag you as resident. Countries sometimes tax citizens who leave for six months to a year, keeping things uncomplicated with tools like the Electronic Federal Tax Payment System.

Expats, you juggle this to avoid surprises, maybe even grabbing an Identity Protection PIN for safety.

Tax Obligations Based on Residency

Tax residency shapes your obligations in ways that can surprise you, especially if you’re living abroad. Let’s break down what this means for your wallet, with clear steps to keep things uncomplicated.

- Countries use residency rules to tax income earned within their borders, so you report local earnings based on where you live most of the year. Think of it like a game of musical chairs, you pay where you sit longest. For instance, the substantial presence test counts your days in a country; rack up 183 days or more, and bam, you’re a tax resident there. This hits expats hard if they bounce between spots, forcing them to track every trip like a detective on a case. Income tax treaties between the U.S. and other nations can help reduce or eliminate double taxation, acting as a peace treaty for your finances.

- Green card holders face U.S. tax on worldwide income as residents, even if they jet off abroad. You file using forms like Form W-4 to adjust withholdings at your job, or Form W-2 to report wages. Imagine you’re sipping coffee in Paris, but Uncle Sam still wants his cut from your global gigs. For long-term residents, expatriation notification requires filing Form I-407, which terminates lawful permanent resident status, a big move if you’re done with U.S. ties. Miss this, and taxes chase you like a bad ex.

- Non-resident aliens dodge U.S. tax on foreign income, but they pay on U.S.-sourced stuff, keeping it simple. They are only subject to gift tax on U.S. situs tangible property, and intangible property is exempt from gift tax, so gifting stocks abroad stays tax-free. All individuals, including U.S. citizens, green card holders, and non-resident aliens, can make annual tax-free gifts of $12,000 to different recipients, like handing out cookies at a party without the IRS crashing in. This rule eases family transfers, no strings attached.

- Estate taxes apply differently based on residency; non-resident aliens are subject to U.S. estate tax only on U.S. situs assets, with a $60,000 exemption. Imagine leaving behind a house in Florida, that gets taxed, but your overseas bank account slips by untouched. Residents, though, report everything worldwide, so plan ahead to avoid a hefty bill for your heirs. Use tools like Form 9465 for installment agreements if payments pile up, turning a mountain into manageable steps.

- Residency ties into reporting foreign accounts, but non-residents skip a lot of that hassle. You might think of it as a lighter backpack on your tax hike. Still, everyone benefits from tax uncomplicated strategies, like claiming credits through treaties. Expats, chat with a pro about your setup; one wrong move, and you’re juggling forms like a circus act gone wild.

Challenges Expats Face Under Citizenship-Based Taxation

Living abroad as a U.S. citizen, you still owe taxes on your worldwide income, which can feel like carrying a heavy backpack everywhere you go. Plus, you must report foreign bank accounts through FBAR forms, and missing that step might lead to steep penalties that sting like a bee.

Double Taxation Risks

Americans abroad often face taxes from the U.S. and the country where they earn income. You might end up paying twice on the same money, like getting hit with a double whammy. Double tax residency happens too, so you count as a resident in more than one place at once.

Check the double taxation agreement between countries to sort out your obligations. It acts like a referee in a messy game.

Eritrea slaps a flat 2% tax on its citizens overseas, called the diaspora tax. Critics blast its collection tactics, full of extortion and threats. The United Nations Security Council called them out for that.

Imagine dodging one tax bill, only to face another with teeth. You deal with these risks as an expat, staying sharp to protect your wallet.

Reporting Foreign Accounts and Assets

Expats often sweat over reporting foreign accounts and assets, feeling like they’re juggling hot coals while blindfolded. You face strict U.S. rules that demand full disclosure, or else penalties hit hard.

- U.S. citizens living abroad must report worldwide income on federal tax returns, just like residents back home, with no flat tax rate to simplify things; this setup creates a maze of paperwork that keeps you on your toes, especially when foreign banks get involved.

- File Form 8854 every year for 10 years after expatriation, spilling details on your income, assets, and liabilities; view this as the IRS peeking into your wallet annually, making sure nothing slips through the cracks.

- Watch out for broad definitions in the alternate tax system, which tags U.S. source income like capital gains from American stocks or earnings from Controlled Foreign Corporations (CFCs); one expat I know compared it to a fishing net that catches every little minnow, including gains from deals made up to five years before you left.

- Skip capital loss carryover as an expat, and stick to deducting only expenses tied straight to your earned income; this rule bites when markets dip, leaving you without that safety net others enjoy.

- Grab Form 1040-C, known as the United States Departing Alien Income Tax Return or Sailing Permit, to prove you owe no U.S. taxes before heading out; think of it as your golden ticket to avoid last-minute hassles at the airport.

Strategies to Avoid Double Taxation

Hey, expat friend, imagine your hard-earned cash getting taxed in two countries, like a bad dream where the bill just doubles. You can fight back with tools such as income exclusions, credits for taxes paid abroad, and agreements between nations that keep things fair, so keep reading to grab these lifesavers.

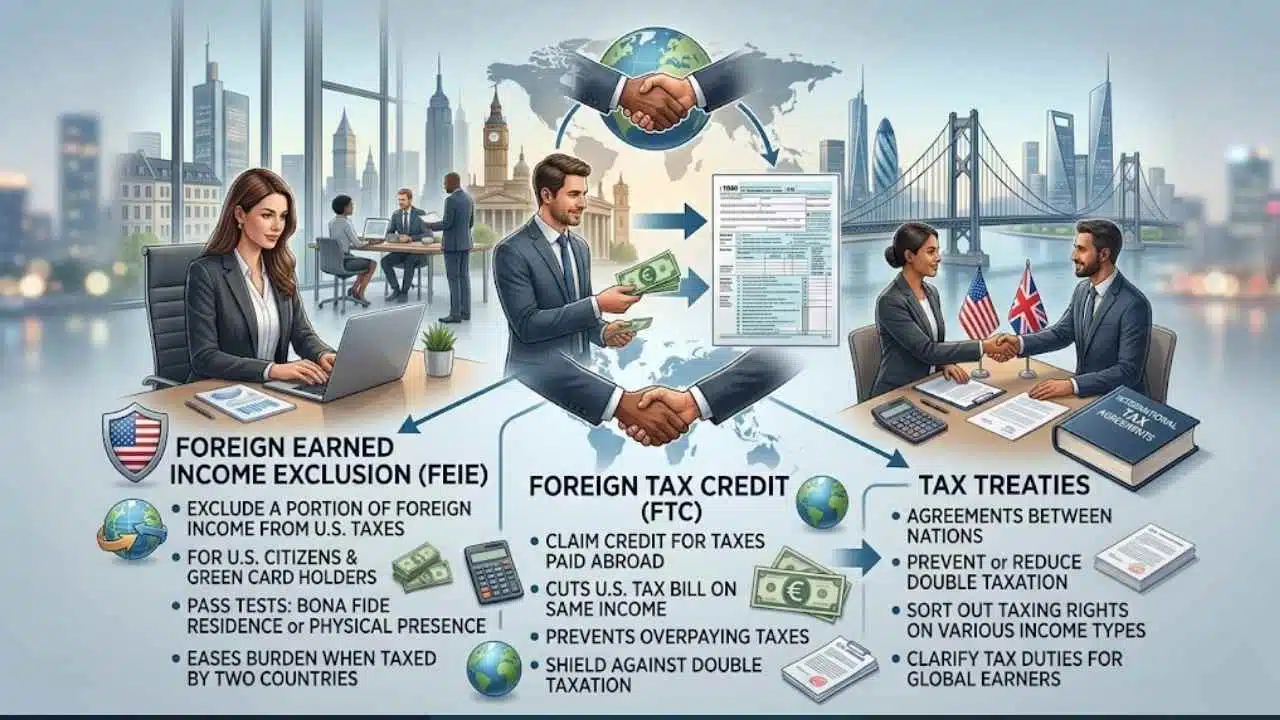

Foreign Earned Income Exclusion (FEIE)

Americans living abroad often turn to the Foreign Earned Income Exclusion, or FEIE, as a lifesaver against double taxation. This tool lets you exclude a chunk of your foreign-earned income from U.S. taxes, easing the burden when countries pull you in two directions.

Imagine working hard overseas, only to face tax bills from Uncle Sam and your new home; FEIE steps in like a trusty shield. U.S. citizens and green card holders qualify if they pass tests, such as the bona fide residence test or the physical presence test.

These checks confirm your life abroad feels genuine, not just a quick trip.

Expats love how FEIE reduces U.S. taxable income earned overseas, keeping more money in your pocket. For example, you earn a salary in Europe, and FEIE knocks off a set amount before the IRS takes a bite.

You must meet specific requirements to grab this benefit, proving your ties to the foreign country through residence or time spent there. This exclusion helps dodge the trap of paying taxes twice on the same earnings, making life smoother for those chasing dreams across borders.

Foreign Tax Credit (FTC)

U.S. citizens and residents abroad often face taxes from two countries. They pay taxes on income earned overseas. The Foreign Tax Credit helps here. It lets you claim a credit for foreign taxes paid.

This credit cuts your U.S. tax bill on that same income. Imagine earning money in France, and paying taxes there. You then use those payments to lower what you owe Uncle Sam. FTC shines when foreign taxes exceed U.S. rates on the income.

You apply it directly against U.S. taxes for income taxed abroad. Expats, you avoid overpaying this way. Think of it as a shield against double dips into your wallet. Claim it on your tax return, and keep records handy.

This tool keeps things fair for global earners.

Tax Treaties

Income tax treaties exist between the U.S. and many other nations. These agreements help cut or wipe out double taxation. You earn money abroad, and these pacts step in like a fair referee.

They sort out who taxes what. Take the deal between the U.S. and New Zealand, for example. It stops double hits on income from both spots. Folks with cash flowing across borders find relief here.

Check the double taxation agreement for your countries. This move clarifies your tax duties. You avoid nasty surprises that way. Governments sign these to keep things smooth. Expats, you gain peace of mind.

Picture dodging a tax storm with a solid umbrella. These treaties make global living easier.

What Expats Need to Consider Before Moving Abroad

Picture yourself landing in a fresh spot abroad, only to face a maze of local income tax rules that catch you off guard. Plan ahead for juggling taxes from your home and host nations, like mapping out a road trip to dodge potholes, so you stay compliant and stress-free.

Understanding Host Country Tax Laws

Expats often overlook local rules, and that can lead to big surprises. Take India, for example. They rolled out a tax residency law that hits non-resident Indians hard. If you live in places like the UAE, Saudi Arabia, Bahrain, Oman, Brunei, Kuwait, the Maldives, Monaco, or Qatar, and skip paying income tax there, India steps in and taxes you.

Ouch, right? This rule skips folks with foreign citizenship, so many chase dual citizenship to shield their cash. Imagine an Indian expat in Dubai, dodging taxes twice by grabbing a second passport.

Smart move, if you ask me.

Now, shift gears to the Caribbean. Dominica offers tax residency if you stay there at least 183 days in a year, set up a lasting home and live in it, or held residency the year before or after.

The region kicked off citizenship by investment in St. Kitts and Nevis. You invest at least $125,000 in their government fund, pass security checks, and boom, citizenship. These spots draw expats for low taxes, like a warm hug from the sun.

Chat with locals or advisors; they spill real stories on fitting in without tax headaches.

Planning for Compliance with Dual Tax Systems

You deal with dual tax systems as a U.S. expat living abroad. Smart planning keeps you compliant and avoids nasty surprises.

- Know that dual tax residency hits many expats, so you can count as a tax resident in two countries at once, like the U.S. and your new home, which means facing rules from both sides.

- U.S. citizens and green card holders pay taxes on worldwide income no matter where they live, so track every dollar earned globally to meet IRS demands.

- Non-resident aliens face taxes only on U.S.-connected income and certain passive sources at lower rates, but you switch back to worldwide taxation if you return to the U.S. within 10 years and stay over 30 days.

- File Form 8854 each year for 10 years after expatriating, and list your income, assets, and debts in detail to prove you follow the rules.

- Spend more than 30 days in the U.S. during those 10 years after proper expatriation, and you trigger U.S. income tax on worldwide earnings again, like a boomerang that pulls you back in.

- Capital gains escape U.S. taxes for non-resident aliens unless they tie to U.S. real estate, so plan asset sales around your status to dodge extra hits.

- Expatriates who return within 10 years and linger past 30 days lose their break from worldwide income taxes, forcing a full reset on obligations.

Final Thoughts

Expats, you’ve seen how tax residency hinges on where you live and work, while citizenship taxation, like in the U.S., follows you worldwide no matter where you roam. Those strategies, from claiming the Foreign Earned Income Exclusion to using the Foreign Tax Credit and tapping tax treaties, keep things simple and cut down on double taxation headaches.

Picture dodging extra bills that could sink your overseas dreams; these tools make a real difference in staying compliant and saving cash. Check out American Citizens Abroad for more tips, or read up on the Residence-Based Taxation for Americans Abroad Act to push for fairer rules.

So gear up, plan smart, and turn those tax woes into smooth sailing abroad.

FAQs

1. What’s the big difference between tax residency and citizenship for expats?

Tax residency means where you pay taxes based on where you live and work, like planting roots in a new spot; citizenship is your legal tie to a country, more like your family tree that doesn’t move easily. Imagine you’re a bird nesting in different trees, but your original flock stays the same. That setup can save you headaches if you plan it right.

2. How does tax residency impact my taxes as an expat?

It decides which country taxes your income, often based on days you spend there. Switch it up, and you might dodge double taxation, like slipping through a loophole in a game.

3. Can I keep my citizenship but change my tax residency?

Yes, you can shift your tax home without touching your passport. Many expats do this by moving abroad for over half the year. It’s like changing your address but keeping your old phone number.

4. What pitfalls should expats watch for with dual citizenship and tax residency?

Dual citizenship can complicate taxes if residencies overlap, leading to extra paperwork. Picture juggling two balls that sometimes collide. Always check treaties between countries to avoid surprises.