Buying your first home in New Zealand is an exciting step, but it can also feel overwhelming. The high cost of purchasing a property, especially in larger cities like Auckland or Wellington, can be a barrier for many would-be homeowners.

Fortunately, the New Zealand government offers several tax relief options designed to make homeownership more accessible to first-time buyers.

These relief options include grants, loans, tax deductions, and exemptions that can ease the financial burden of buying a home. Understanding and utilizing these tax relief opportunities can significantly reduce the amount you need to save for a deposit, lower your mortgage repayments, and even provide ongoing financial support.

In this comprehensive guide, we’ll explore 8 Tax Relief Options for First-Time Homebuyers in New Zealand, providing you with practical details and advice on how to make the most of these opportunities.

What Qualifies as a First-Time Homebuyer in New Zealand?

Before you dive into the tax relief options, it’s crucial to understand what qualifies someone as a first-time homebuyer in New Zealand. This designation opens the door to various financial relief programs, including grants, loans, and tax incentives. Here are the basic criteria that you must meet to be eligible:

- No previous property ownership: This includes land, homes, or any form of residential property in New Zealand or overseas.

- Primary residence intent: You must intend to live in the property as your primary residence. If you plan to rent out the property, you will not qualify for most tax relief options.

- Age and citizenship status: You must be at least 18 years old and a New Zealand citizen or permanent resident.

For some programs, the government may also assess factors like household income or the value of the property you’re buying. So, it’s essential to familiarize yourself with specific eligibility requirements for each tax relief option.

1. First Home Grant (FHG)

The First Home Grant (FHG) is one of the most popular and widely accessible forms of financial assistance for first-time homebuyers. This program is designed to provide you with a cash grant to help with the deposit when buying your first home.

Overview of the First Home Grant

The First Home Grant is a government-backed cash grant that you don’t have to pay back. It’s designed to assist with the purchase of both new and existing homes. The amount you can receive is determined by where you plan to buy and whether you are purchasing a new or existing home.

| Region | Grant for New Homes | Grant for Existing Homes |

| Auckland | $10,000 | $5,000 |

| Wellington | $10,000 | $5,000 |

| Christchurch | $10,000 | $5,000 |

| Rural Areas | $10,000 | $5,000 |

Eligibility Requirements

To be eligible for the First Home Grant, you must meet the following criteria:

- Age: You must be at least 18 years old.

- Income: Your income must be within specific limits set by the government. For example, the maximum income for a single person is $95,000, while for a couple it’s $150,000.

- Deposit: The First Home Grant is typically combined with other initiatives like the First Home Loan to help reduce the upfront deposit required.

Benefits of the First Home Grant

- Immediate Financial Assistance: The grant offers significant immediate support, reducing the financial pressure of saving for a deposit.

- No Repayment Required: Unlike loans, the First Home Grant doesn’t require repayment, so it’s a non-debt solution to help you enter the property market.

2. First Home Loan (FHL)

The First Home Loan (FHL) provides a low-interest mortgage option to help first-time buyers who are struggling to save a large deposit. This government initiative, in partnership with banks, makes it easier to secure a home loan with a smaller upfront deposit.

Overview of the First Home Loan

The First Home Loan offers first-time buyers the ability to purchase a property with just a 5% deposit instead of the usual 20%. The government guarantees a portion of the loan, which reduces the risk for the lender.

| Deposit Required | Interest Rates | Maximum Loan Amount |

| 5% | Market-Competitive | Varies by region |

Eligibility for First Home Loan

To qualify for the First Home Loan, you must meet the following criteria:

- Income limits: Your household income must fall within a specified range. For example, a single person must earn no more than $95,000, while a couple’s combined income can be up to $150,000.

- Property price caps: The value of the home you wish to purchase must fall within specific price limits, depending on the region.

How It Works

- The 5% deposit makes it easier for first-time buyers to enter the market without waiting years to save.

- The government’s loan guarantee lowers the lender’s risk, making it more likely that you will be approved for the loan.

Differences Between First Home Loan and First Home Grant

The First Home Loan is essentially a mortgage with a government guarantee, while the First Home Grant is a direct cash grant. The two programs can be used together for maximum benefit.

3. KiwiSaver HomeStart Grant

The KiwiSaver HomeStart Grant is a significant benefit for New Zealanders who have been contributing to their KiwiSaver accounts and are now looking to use their savings to purchase their first home. KiwiSaver is a voluntary savings scheme for retirement, but it also doubles as a powerful tool for first-time homebuyers.

Overview of KiwiSaver HomeStart Grant

If you’ve been contributing to your KiwiSaver account for at least three years, you could be eligible for a HomeStart Grant. The grant can be up to $10,000 for a new home and $5,000 for an existing home.

| Home Type | Grant Amount | Maximum Available |

| New Home | $10,000 | $10,000 |

| Existing Home | $5,000 | $5,000 |

Eligibility for KiwiSaver HomeStart Grant

- KiwiSaver contributions: You must have been contributing to your KiwiSaver account for at least three years.

- Income limits: There are income caps, which vary by region and the size of your household.

- Property price limits: There are also price caps on the homes you can purchase with the grant, depending on the region.

How to Use Your KiwiSaver for Buying Your First Home

The HomeStart Grant can be used alongside other first-time buyer programs, such as the First Home Grant. You can also use your KiwiSaver balance to contribute towards your deposit, giving you more purchasing power.

Key Benefits

- Additional Savings: KiwiSaver can help you build a substantial deposit over time, and the HomeStart Grant provides a boost.

- Government Contributions: The government’s contribution to your KiwiSaver savings means that you don’t need to rely entirely on personal savings to fund your home deposit.

4. Property Tax Relief for First-Time Homebuyers

While property taxes can often feel like an unavoidable cost, first-time homebuyers in New Zealand have access to some property tax relief options. These are designed to reduce the cost of homeownership, particularly in relation to local property taxes and rates.

What is Property Tax Relief?

Property tax relief includes reductions or exemptions on local council rates, which are taxes that fund local government services. These rates can often be a significant financial burden for new homeowners.

Key Forms of Property Tax Relief

- Council Rates Exemptions: Some councils offer first-time buyers exemptions or reductions in council rates for the first few years of homeownership.

- New Builds and Property Taxes: For new builds, you may qualify for a temporary exemption or reduction in local taxes.

How Property Tax Relief Can Save You Money

By reducing or exempting the amount you pay in council rates and other property taxes, first-time buyers can save significant amounts each year, easing the cost of owning a home.

| Council | Tax Relief Type | Details |

| Auckland | Reduced Rates | Applies to new buyers |

| Wellington | Full Exemption | Applies for 3 years |

| Christchurch | Partial Exemption | Varies by income |

5. Income Tax Deductions for Mortgage Interest

An often overlooked tax relief option for first-time homebuyers in New Zealand is the ability to claim income tax deductions on mortgage interest. This option can significantly reduce your overall tax burden, helping you save money in the long run.

Overview of Mortgage Interest Deductions

Mortgage interest deductions allow homeowners to deduct the interest paid on their mortgage from their taxable income. This deduction helps reduce your overall tax bill and can provide financial relief during the early years of homeownership when mortgage interest payments are typically higher.

| Mortgage Term | Interest Deduction Available | Tax Benefit |

| 5-Year Fixed | Interest paid on the loan | Reduces taxable income |

| 30-Year Fixed | Interest paid on the loan | Provides savings each year |

How Mortgage Interest Deductions Work

The key to benefiting from mortgage interest deductions is keeping accurate records of your mortgage payments. At the end of each financial year, you can claim the total amount of interest you’ve paid on your mortgage as a deduction. This means you will be taxed on a lower amount of income, potentially resulting in a tax refund or a reduced annual tax liability.

How Much Can You Save?

Your tax savings from mortgage interest deductions depend on your tax bracket and the amount of interest you pay on your mortgage. For example, if you are in the 30% tax bracket and pay $10,000 in mortgage interest annually, you could save around $3,000 in taxes.

Eligibility Requirements

- The property must be your primary residence, and you cannot claim deductions on mortgage interest for rental properties.

- Ensure that your mortgage lender provides detailed records of the interest paid on the loan throughout the year.

Example Case:

Sarah and Tom purchased their first home in Wellington. They took out a $400,000 mortgage at an interest rate of 5% for 30 years. Over the first year, they paid $20,000 in interest. If they are in the 33% tax bracket, they could save approximately $6,600 in taxes through mortgage interest deductions in their first year. This could be a game-changer for first-time buyers looking to reduce their overall homeownership costs.

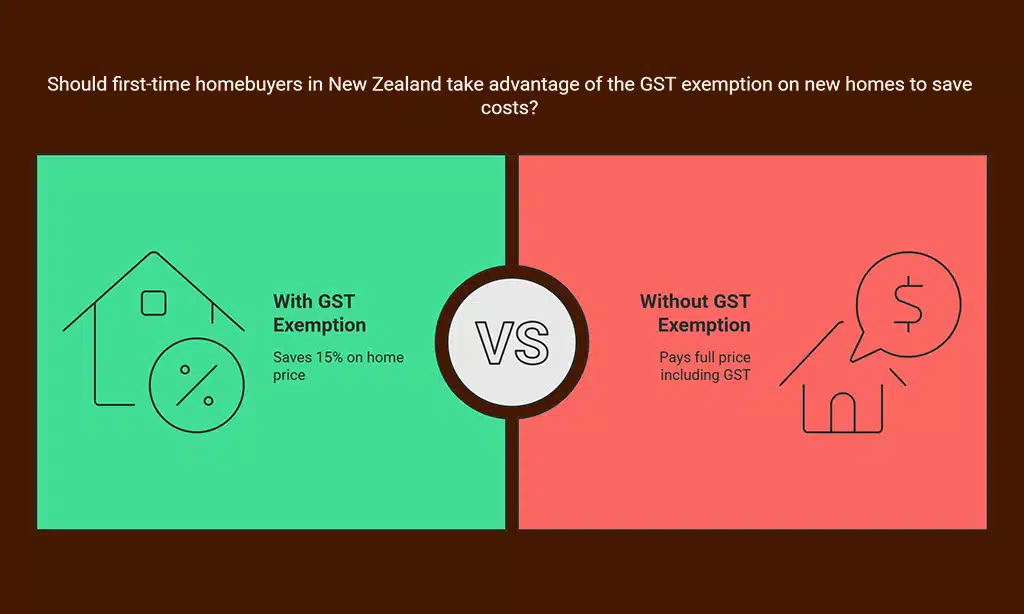

6. GST Exemption on New Homes

The Goods and Services Tax (GST) is a value-added tax applied to the sale of most goods and services in New Zealand, including the purchase of homes. However, first-time homebuyers can benefit from a GST exemption when purchasing newly built homes.

Overview of GST Exemption

When buying a newly built home in New Zealand, you may not be required to pay GST on the property. This exemption significantly reduces the total cost of buying a new home, providing financial relief for first-time buyers.

| Home Type | GST Exemption Available | Benefit to Buyers |

| New Homes | GST Exemption | Saves 15% on home price |

How the GST Exemption Works

New homes typically come with a 15% GST, which is included in the sale price. However, under New Zealand law, GST does not apply to new homes when they are sold to the end user (you, the buyer). This means that if you’re purchasing a newly built home, you can save up to 15% on the total sale price.

Practical Example

Imagine you’re purchasing a newly built home valued at $600,000. With GST included, the cost would be $690,000. With the GST exemption, you would pay the base price of $600,000, saving $90,000 in GST.

Eligibility for GST Exemption

- The home must be newly constructed and not previously owned.

- You must be buying the property as your primary residence and not for investment purposes.

Key Benefits of the GST Exemption

- Lower Purchase Price: The 15% savings on a new home can significantly reduce the upfront cost, making it easier for first-time buyers to enter the property market.

- Simpler Transaction: The exemption streamlines the process of buying a new home, ensuring you’re not burdened with additional paperwork or complex calculations.

7. Council Rates and Local Tax Relief Programs

Some local councils in New Zealand provide council rates relief or other financial incentives to first-time homebuyers. These local tax relief programs can significantly reduce the annual costs associated with homeownership, particularly during the first few years.

What are Council Rates and How Do They Impact Homebuyers?

Council rates are annual charges levied by local governments to fund essential services such as waste collection, road maintenance, and public amenities. These charges can add up quickly, especially in larger urban areas. First-time homebuyers, however, may qualify for reductions or exemptions from these council rates through specific local programs.

| Council Type | Rate Relief Available | Benefits |

| Auckland City | Reduced rates for 3 years | Lowers ongoing costs |

| Christchurch City | Rates reduction for 2 years | Offers significant savings |

| Wellington City | Full exemption for 1 year | Immediate relief |

How to Access Council Tax Relief

Each local council has different policies regarding council rates relief for first-time buyers. Typically, you will need to:

- Apply directly to your local council.

- Provide proof that you are a first-time homebuyer.

- Show evidence of your primary residence.

How Council Tax Relief Saves You Money

Council rates can range from $1,000 to $5,000 per year depending on the location and value of your property. By receiving a reduction or exemption, you could save hundreds or even thousands of dollars annually, easing the ongoing financial burden of homeownership.

Example:

John and Lucy recently purchased their first home in Christchurch. With council rates typically costing $2,500 per year, they were eligible for a two-year rates reduction through the local council’s first-time buyer program. As a result, they saved $5,000 during the first two years of ownership, money they could use to invest in home improvements or save for other expenses.

8. Capital Gains Tax Exemption for Primary Residences

In New Zealand, capital gains tax (CGT) does not generally apply to the sale of residential properties, particularly when the property is your primary residence. This tax relief is a significant benefit for homeowners and first-time buyers, as it ensures that any profit made from the sale of your primary home is tax-free.

What is Capital Gains Tax?

Capital gains tax is typically applied to the profit made from selling assets, such as property, that have increased in value. However, in New Zealand, there is no general capital gains tax on the sale of residential property, provided it’s your primary residence.

| Home Type | CGT Applicability | Exemption Criteria |

| Primary Residence | No Capital Gains Tax | Must live in the home |

| Investment Properties | Capital Gains Tax Applies | If sold within 10 years |

How the CGT Exemption Works

When you sell your home, any profit made on the sale is not subject to tax if the property has been your primary residence for the entire time you’ve owned it. This is a significant benefit for first-time homebuyers, as it means they can sell their home for a profit without worrying about paying a portion of the proceeds to the government.

How Much Can You Save with the CGT Exemption?

The potential savings from the CGT exemption can be substantial, especially if property values increase significantly over time. For example, if you purchase a home for $400,000 and later sell it for $600,000, the $200,000 profit would be tax-free.

Eligibility for CGT Exemption

- The property must have been your primary residence for the entire duration of ownership.

- If you own the property for more than 10 years and sell it, certain conditions may apply, and CGT may be triggered, but this is rare for most homebuyers.

Benefits of the CGT Exemption

- Tax-Free Profits: You can sell your home without worrying about taxes on your gains.

- Increased Financial Flexibility: The money you make from the sale of your home is yours to reinvest, whether in your next property or other financial ventures.

Wrap Up: Maximizing Tax Relief and Saving on Your First Home

Navigating the complexities of buying your first home can be challenging, but New Zealand offers a range of Tax Relief Options for First-Time Homebuyers to help make homeownership more affordable.

By understanding and utilizing these relief options, you can reduce your upfront costs, lower your ongoing expenses, and ultimately secure a property with less financial strain.

From the First Home Grant to KiwiSaver’s HomeStart Grant and First Home Loans, these programs are designed to ensure that first-time buyers have the tools and financial support they need to enter the housing market with confidence.

Remember to consult with financial advisors or tax professionals to ensure you’re making the most of these opportunities, and always stay informed about the latest updates to these programs to ensure you don’t miss out on any potential benefits.

By taking advantage of these tax relief options, you can pave the way to homeownership and enjoy the peace of mind that comes with owning your own home.