Imagine your hard-earned dollars shrinking, bit by bit, as prices for groceries, gas, and rent climb higher. You feel the pinch in your wallet every day, and it stings. This common struggle hits many folks, making them wonder why their money doesn’t stretch as far. That’s the sneaky side of inflation at work, eroding what you’ve built up over time.

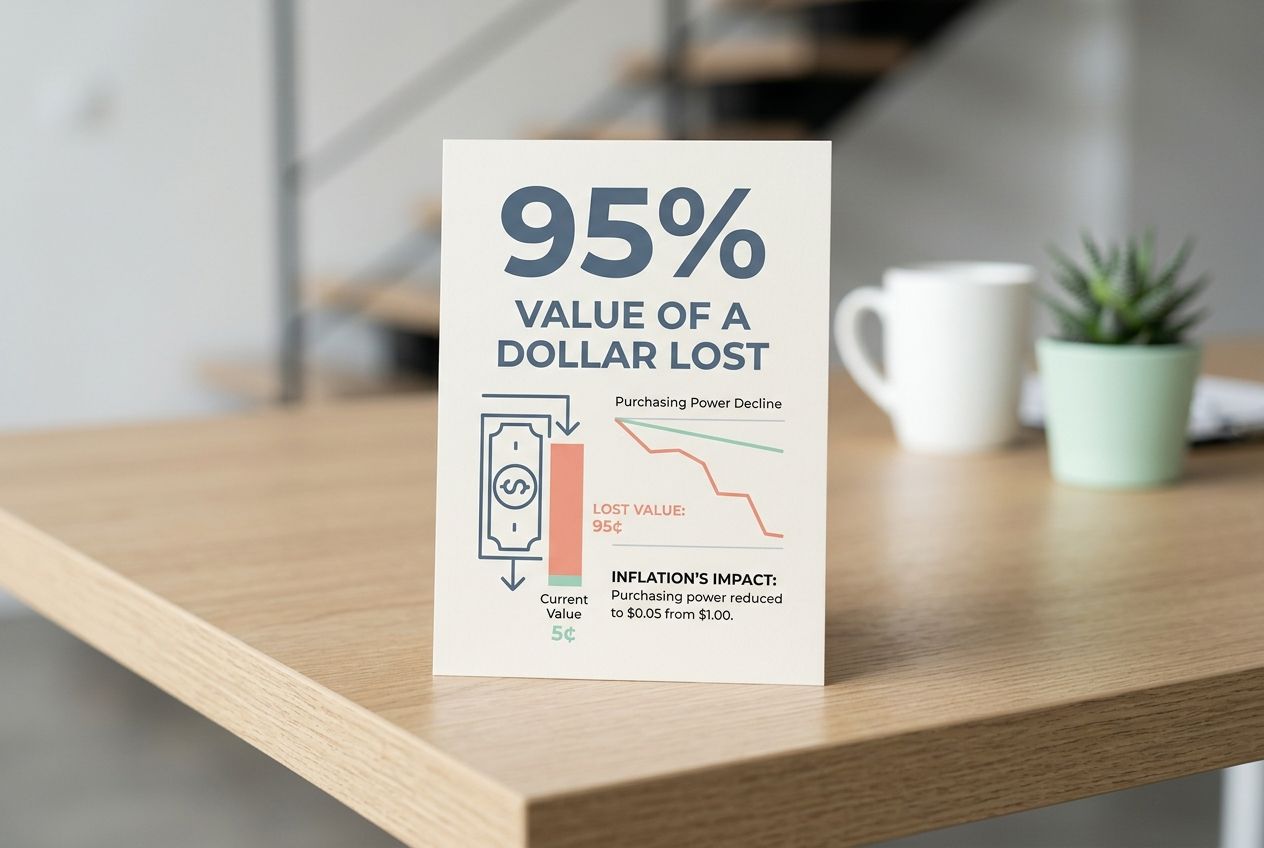

Did you know that over the last century, inflation has cut the value of a dollar by more than 95 percent? Ouch, right? We explore the Inflation Impact on Wealth here, showing you smart ways to fight back with tips on investments, savings tweaks, and more.

What Is Inflation?

You’ve just read the intro, so let’s jump right into the basics of inflation. Inflation happens when prices for goods and services rise over time. This rise cuts into your purchasing power.

Think of it like a slow leak in your wallet; money buys less as costs climb. Economists track the inflation rate to measure this change. A steady inflation rate signals economic stability, but high rates spark trouble.

People feel the pinch in everyday life, from groceries to gas. Savings lose value if they sit idle. Investments need smart tweaks to keep up.

Inflation is as violent as a mugger, as frightening as an armed robber and as deadly as a hit man. – Ronald Reagan

Cost of living jumps during inflation spikes. Your budget stretches thin without warning. Financial planning becomes key to fighting back. Debt can feel heavier as interest rates often follow suit.

Asset allocation helps shield your wealth. Economic impact hits everyone, yet some cope better than others. Stay alert to these shifts for better decisions.

How Inflation Affects Your Wealth

Imagine your hard-earned cash melting away, like an ice cube in summer sun, as prices climb and your buying power shrinks. You feel the pinch in savings, investments, and even that cozy home you own, so let’s explore smart ways to fight back and keep your wealth strong.

Erosion of Purchasing Power

Inflation sneaks up like a thief in the night, robbing your money of its strength. You earn a dollar today, but tomorrow it buys less bread or gas. This erosion hits your purchasing power hard, as the cost of living climbs.

Think about that cup of coffee you love; it costs more each year, yet your savings stay the same. People feel the pinch in everyday budgets, watching wealth shrink without warning. Inflation rates push prices up, forcing tough financial decisions on investments and spending.

Your cash holdings lose value fast during high inflation. Fixed savings accounts offer little fight back. Real assets, like property, sometimes hold up better, but not always. Stock market investments fluctuate with these economic shifts.

Diversify to guard against this wealth drain, or risk seeing your economic stability fade. Focus on smart asset allocation now, before the cost of living bites deeper into your plans.

Impact on Savings and Cash Holdings

You stash cash in a savings account, thinking it’s safe. But inflation chips away at its value, bit by bit. Your purchasing power drops as the cost of living climbs. Say the inflation rate hits 3 percent a year; that same dollar buys less bread, gas, or gadgets tomorrow.

People with lots of cash holdings feel this pinch hard during economic downturns. It forces smarter financial decisions to protect your wealth.

Folks often overlook how savings shrink in real terms. Inflation acts like a silent thief, stealing from your nest egg without you noticing right away. Shift focus to investments that beat inflation, like those tied to asset management.

Budget wisely, and watch your money work harder. This keeps your economic stability intact, even as prices rise.

Inflation is taxation without legislation. – Milton Friedman

Effects on Fixed Income Investments

Inflation hits fixed-income investments hard, like bonds or certificates of deposit. These assets promise steady returns, but rising prices eat away at their value. Say you buy a bond paying 3% interest.

If inflation jumps to 5%, your real return drops into the negative. That means your purchasing power shrinks over time. Investors see their wealth erode as the cost of living climbs faster than earnings from these holdings.

Picture inflation as a sneaky thief, stealing from your savings without you noticing at first. Fixed-income securities struggle in such times, since they lock in rates that don’t adjust quickly.

Focus on how this impacts your financial decisions; bonds might seem safe, but high inflation turns them into a losing bet for long-term wealth. Shift thoughts to asset allocation to counter this, keeping your investments ahead of economic downturns.

Influence on Real Assets like Property

Real assets like property can act as a shield against rising prices. Think of your home as a boat that floats higher when the tide of costs comes in. Property values often climb with the inflation rate, keeping pace with the cost of living.

This helps preserve your wealth, unlike cash, which loses buying power over time. Owners see rents go up, too, boosting income during economic shifts. But watch out, higher interest rates might make buying tougher for some. Stocks respond in their own way to these changes, so let’s look at the impact on stock market investments.

Impact on Stock Market Investments

Inflation hits stock market investments hard. It erodes purchasing power, making your returns buy less over time. Stocks often rise with inflation, as companies pass higher costs to customers.

Yet, rapid inflation spikes can scare investors, leading to market drops. Think of it like a roller coaster; the ride gets bumpy when prices soar. Your portfolio might grow in value, but inflation eats into real gains.

Focus on companies that thrive in tough times, like those in energy or consumer goods. They adjust prices fast and protect your wealth.

High inflation pushes interest rates up, which hurts stock prices. Growth stocks suffer most, as future earnings look weaker. Value stocks may hold up better. Diversify to manage this risk in your asset allocation.

Inflation affects economic stability, so watch the inflation rate closely for smart financial decisions. Now, examine how inflation shapes investment returns.

Inflation’s Influence on Investment Returns

Inflation sneaks up on your investments, chewing away at returns like a mouse in a cheese factory. Stocks might surge or stumble based on rising prices, while bonds often take a hit, so keep reading to spot the winners in this economic game.

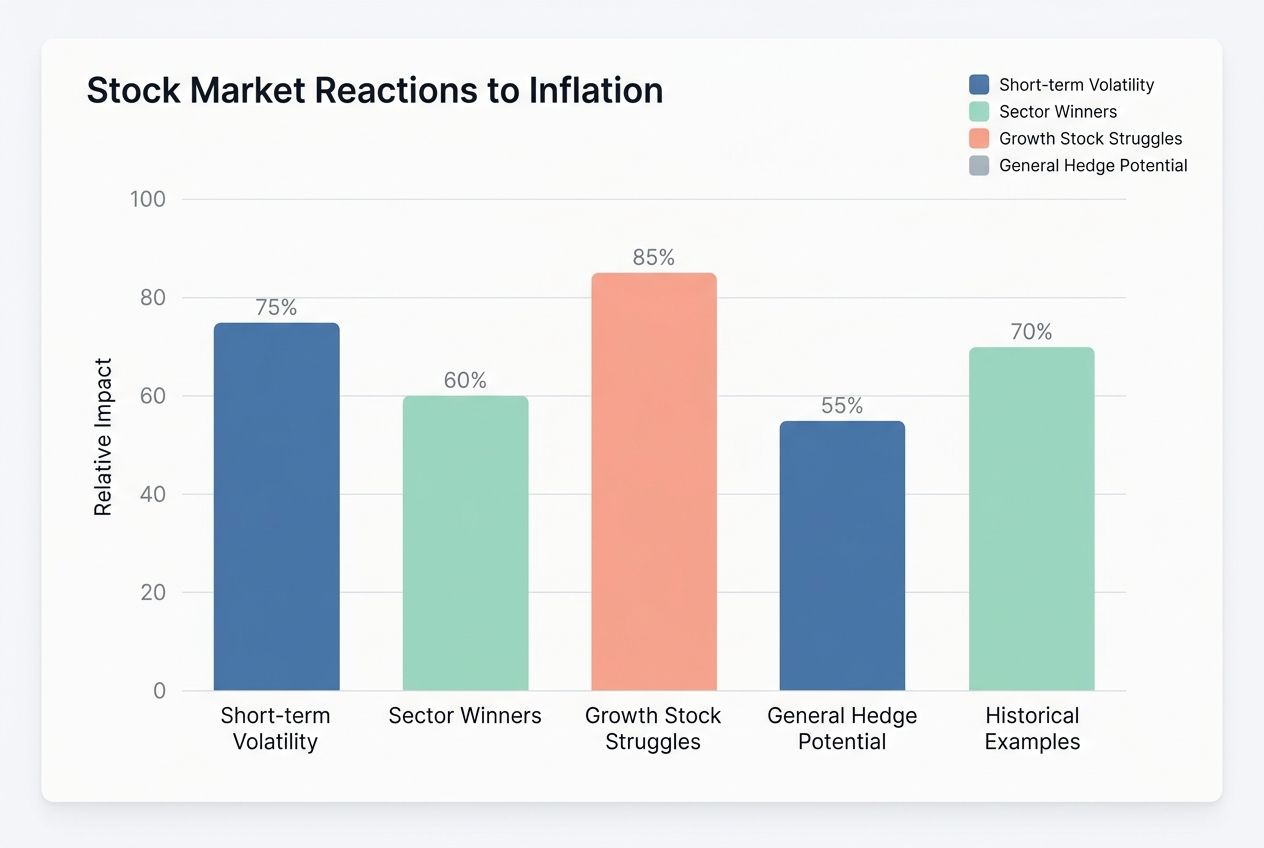

Stock Market Reactions to Inflation

You know how stocks can feel like a roller coaster during economic shifts, right? Let’s break down how the stock market reacts to inflation in this handy table.

| Reaction Type | What Happens | Why It Matters to You |

|---|---|---|

| Short-term Volatility | Stocks often drop sharply when inflation spikes, as companies face higher costs for materials and labor. | This hits your portfolio hard if you sell in a panic, so stay calm and think long-term. |

| Sector Winners | Energy and commodity stocks tend to soar, since their products rise in price with inflation. | Shift some investments here to cushion the blow, like betting on oil giants during a price surge. |

| Growth Stock Struggles | Tech and growth stocks suffer because future earnings look less valuable in high-inflation environments. | Watch out if your holdings lean heavily on startups; they might drag your returns down fast. |

| General Hedge Potential | Many stocks outpace inflation over time, especially those from firms that can pass costs to customers. | Build a mix that includes these resilient picks, turning inflation from foe to mere speed bump. |

| Historical Examples | Back in the 1970s, stocks lagged during rampant inflation, but bounced back strongly in the 1980s. | Learn from the past; it shows patience pays off when markets adjust to new realities. |

Bonds face their own battles in inflationary times, so let’s explore that next.

Bonds and Fixed-Income Securities in Inflationary Times

Inflation hits bonds hard, folks. These fixed-income securities promise set payments over time, but rising prices eat away at their real value. Your bond might pay $50 a year, yet that cash buys less as the cost of living rises.

Investors see their purchasing power shrink, making these assets less appealing during high inflation rates. Think of it like holding a leaky bucket; the water, or your wealth, drips out slowly.

Smart folks turn to options like Treasury Inflation-Protected Securities to fight back. These adjust with inflation, helping preserve your investments and savings. Bonds can still fit in a diverse portfolio, but watch interest rates closely since they often rise to combat inflation, pushing bond prices down. Real estate offers another angle on shielding your wealth from these economic shifts.

Real Estate Market Dynamics During Inflation

Real estate often shines as a solid player when prices climb everywhere else.

| Dynamic | Impact on Your Wealth |

|---|---|

| Property values rise. | You gain equity, like turning your home into a growing piggy bank, especially if you bought low in the 2000s. |

| Rents increase with costs. | Landlords collect more cash flow; think of it as your rental property keeping pace with grocery bills that jumped 10% in 2022. |

| Mortgage payments stay fixed. | Your debt shrinks in real terms, a bit like inflation eating away at what you owe, as seen in the 1970s when rates hit 18% but homeowners won out. |

| Construction slows due to higher material prices. | Supply drops, pushing home values up further; consider how lumber costs soared 300% in 2021, squeezing new builds. |

| Investors flock to tangible assets. | People like Warren Buffett tout real estate as an inflation fighter, with REITs returning 12% annually during high-inflation periods since 1990. |

| Interest rates spike to curb inflation. | Borrowing gets pricier, cooling the market short-term, yet long-term gains held strong in cities like New York during the 1980s recovery. |

Inflation and Wealth Inequality

Inflation sneaks in like a pickpocket at a crowded fair, robbing some folks while padding the pockets of others. It widens the chasm between haves and have-nots, you know, by shifting money from everyday workers to those with hefty investments.

People on fixed incomes watch their dollars shrink fast, as if melting like ice cream on a hot day, while asset owners see their stocks or homes balloon in value. Low earners get hit hardest, spending big chunks on rising food and rent prices that outpace their paychecks.

Middle-class families scramble to keep up, cutting corners where they can. Wealthy types, though? They ride the wave, their portfolios growing stronger against the tide. Imagine inflation as that unfair game where the rich get extra turns. Curious how this plays out in your life? Stick around for tips on shielding your cash.

Redistribution of Wealth

Think about how rising prices shift money around, like a sneaky game of musical chairs. High earners often protect their wealth with smart investments that beat the inflation rate, keeping their purchasing power strong.

Low-income folks, though, feel the pinch more, as their savings lose value fast and the cost of living soars. This gap widens wealth inequality, turning economic stability into a tougher climb for many.

Picture a family budgeting tight while big investors ride the wave of real assets like property. Debtors win big, too, since inflation erodes what they owe, easing their debt load. Savers on fixed incomes lose out, watching their nest eggs shrink.

Smart financial decisions, like tweaking asset allocation, help level the playing field and guard against this uneven economic impact.

Effects on Different Income Groups

This redistribution of wealth hits people in varied ways, depending on their income levels, and it often widens the gap between groups.

We see inflation play out differently across income brackets. Check this table for a clear breakdown.

| Income Group | Effects of Inflation |

|---|---|

| Low-Income Groups | You face the brunt. Essentials like food and rent spike fast. Wages lag behind. Savings erode quickly. Debt feels heavier. Picture scraping by on a fixed budget, only to watch costs soar. It squeezes your daily life hard. |

| Middle-Income Groups | Your situation mixes pain and gain. Mortgage payments might ease if rates adjust, but grocery bills bite. Investments in stocks could help, yet not always enough. You juggle rising expenses with modest asset growth. Feels like running in place sometimes, right? |

| High-Income Groups | You often come out ahead. Assets like real estate and stocks rise with inflation. Diversified portfolios protect wealth. Access to hedges, like gold, shields you. Borrowed money costs less in real terms. It’s like inflation acts as your silent ally, boosting net worth while others struggle. |

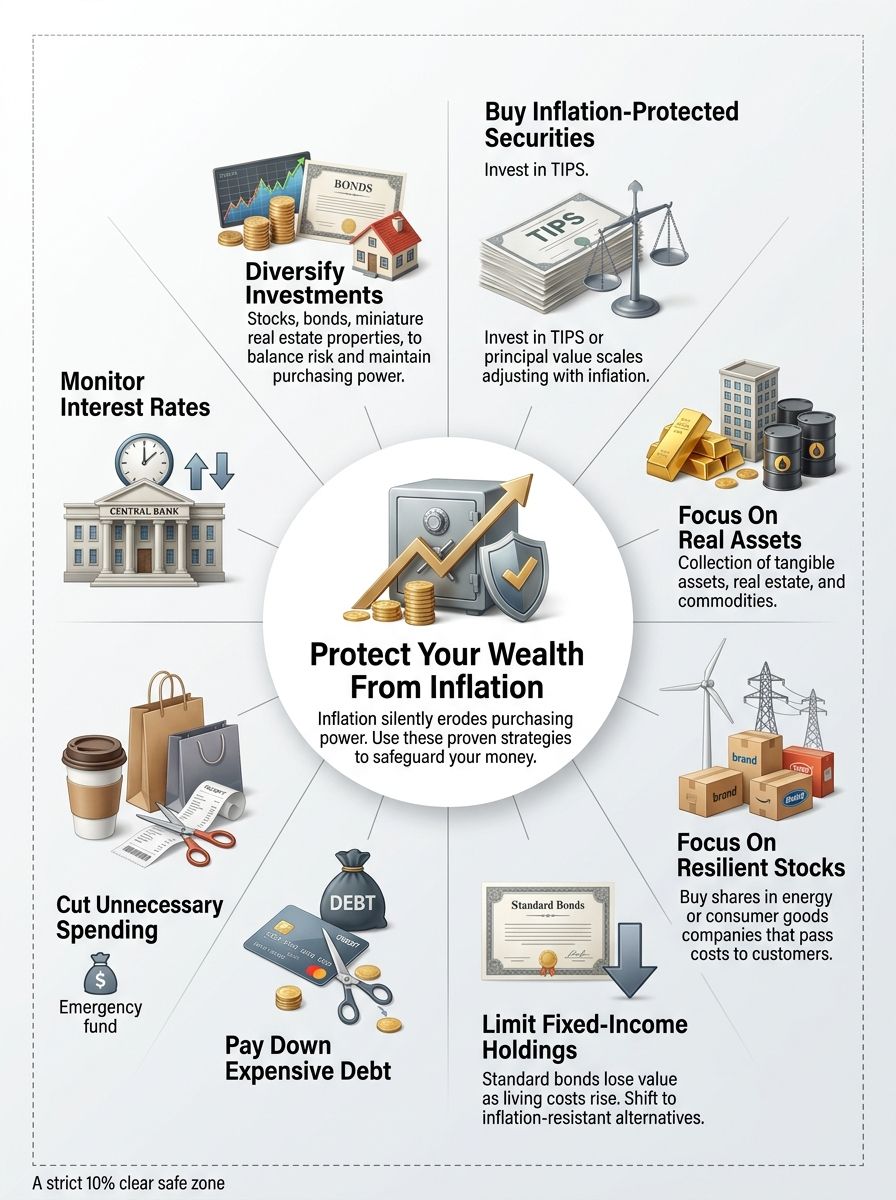

Strategies to Protect Your Wealth from Inflation

Inflation sneaks up like a thief in the night, robbing your money’s value, so arm yourself with smart moves that keep your finances strong and growing. Curious for the details? Dive deeper into this guide.

Diversify Your Investment Portfolio

Diversification shields your wealth from inflation’s bite. You spread risks across assets to maintain purchasing power.

- Mix stocks, bonds, and real estate in your portfolio; this approach counters how inflation erodes savings by letting growth in one area offset losses in another, like a safety net during economic downturns.

- Include commodities such as gold or oil; these often rise with the cost of living, preserving your investments when inflation rates climb, and cash holdings lose value.

- Add inflation-protected securities like TIPS; they adjust with inflation, supporting asset management and helping your budget weather financial decisions in tough times.

- Balance domestic and international assets; this guards against local economic impacts, ensuring your wealth stays stable even if one market faces high inflation.

- Reassess your mix yearly; adjust based on inflation trends to boost investment returns, much like tweaking a recipe to suit changing tastes and keep economic stability in check.

- Consider alternative options like cryptocurrencies or art; these can hedge against rising costs, adding fun layers to your financial planning while dodging debt pitfalls from inflation.

- Focus on dividend-paying stocks; they provide income that often outpaces inflation, aiding in budgeting and protecting your total wealth from erosion over time.

Invest in Inflation-Protected Securities

Inflation sneaks up like a thief in the night, stealing your purchasing power. Smart investors turn to inflation-protected securities to shield their wealth and keep investments growing.

- Treasury Inflation-Protected Securities, or TIPS, adjust with the inflation rate to protect your savings. These bonds from the U.S. Treasury boost their principal value based on the Consumer Price Index. Imagine your money growing as costs rise; that’s the magic here. For example, if inflation hits 3 percent, your TIPS investment rises by that amount, preserving your economic stability. Folks love them for a steady income during high-cost-of-living times. Just buy them through TreasuryDirect or a broker, and watch them counter the effects of economic downturn on your wealth.

- Series I Savings Bonds offer another solid choice for asset management against inflation. They combine a fixed interest rate with an inflation adjustment twice a year. Envision this: you lock in returns that beat rising prices, helping your budget stay intact. In 2022, these bonds hit rates over 9 percent due to high inflation, a real win for everyday savers. Limit your purchase to $10,000 per year electronically, but they beat regular savings accounts in inflationary periods. This keeps your financial planning strong without much risk.

- Consider inflation-linked bonds from other countries for broader diversification in your portfolio. These work like TIPS but tie to global inflation metrics, spreading your investments worldwide. Say inflation spikes in Europe; your bonds from there could rise, balancing U.S. economic impacts. Investors often mix them with stocks for better asset allocation. They help low-income groups fight wealth inequality by maintaining purchasing power. Always check fees and taxes to maximize returns.

- Real Return Funds pool inflation-protected assets into mutual funds or ETFs for easy access. These funds track inflation indexes, making them great for beginners facing financial decisions. Think of them as a basket that grows with the cost of living, protecting your complete wealth. For instance, the Vanguard Inflation-Protected Securities Fund has delivered solid performance amid rising inflation rates. They reduce the hit on fixed income from economic downturns. Start small to test the waters and build confidence.

- Corporate inflation-protected bonds add a private sector twist to your strategy. Companies issue these to hedge against inflation, often yielding more than government ones. Envision earning extra interest as prices climb, boosting your investment returns. During the 2021 inflation surge, some bonds outperformed traditional ones by 2 to 3 percent. They suit those with higher risk tolerance in their financial planning. Pair them with real assets like property for full protection.

Focus on Real Assets

Real assets act like a shield against inflation’s bite on your wealth. They help preserve purchasing power when the cost of living rises.

- Gold shines as a classic real asset during inflation spikes. You buy it to hedge against rising prices, since its value often climbs with inflation rates. See it as your financial lifeboat in stormy economic seas. For example, if inflation hits 5%, gold might jump 7%, keeping your investments ahead. This approach boosts asset management and supports financial planning for long-term economic stability.

- Real estate offers solid ground when inflation erodes savings. You invest in property because rents and home values typically rise with the cost of living. Owning an apartment generates more income each year as prices swell. This protects your wealth from economic downturns and aids in budgeting by providing steady returns. Smart asset allocation here means your portfolio stays strong amid high inflation.

- Commodities like oil or wheat serve as direct bets against inflation’s impact on investments. You trade them to capture price surges tied to supply demands. Ride the wave of global needs, where a 3% inflation bump could lift commodity values by 4%. This strategy diversifies your holdings and counters the effects on fixed income. Focus here enhances economic impact resistance for your general financial decisions.

- Artwork and collectibles add flair to inflation-proofing your wealth. You collect pieces that appreciate over time, outpacing inflation rates. Snag a vintage car that doubles in value while costs soar. This fun twist on asset management fights purchasing power loss. It fits into broader financial strategies, helping different income groups maintain stability during tough times.

- Timber and farmland provide growth you can touch amid inflation pressures. You own land that yields crops or wood, with values rising as demand grows. Trees mature into profit as the economy heats up. This real asset focus safeguards savings from erosion. It promotes wise budgeting and counters wealth inequality by offering tangible returns in volatile markets.

Adapt Your Spending and Saving Habits

Inflation sneaks up on you like a thief in the night, quietly chipping away at your purchasing power and cost of living. You can fight back by tweaking your spending and saving habits, turning the tide on your wealth during these economic twists.

- Cut back on non-essential buys to protect your savings from the rising inflation rate, think of it as trimming the fat from your budget, so you free up cash for smarter investments that beat economic downturns.

- Build an emergency fund that covers six months of expenses. This acts like a safety net, keeping your financial decisions steady when prices soar, and your wealth feels the pinch.

- Track your daily spending with a simple app or notebook, and you spot leaks in your budget fast, like finding hidden treasures, which boosts your asset management and guards against wealth erosion.

- Switch to cheaper alternatives for everyday items, for example, opt for store brands over name brands. This small shift preserves your purchasing power without sacrificing much in your cost of living.

- Increase your income streams through side gigs. Imagine turning a hobby into extra cash; it cushions your savings against inflation’s bite and supports better financial planning.

- Pay down high-interest debt quickly; debts grow like weeds in inflationary times, so you slash them to keep more money in your pocket for investments that grow your wealth.

- Review and adjust your budget monthly. Life throws curveballs, but this habit keeps your spending in check, ensuring economic stability amid rising costs.

- Save in high-yield accounts that outpace inflation, your money works harder for you, like a loyal friend, countering the impact on your general financial decisions.

- Plan meals and shop with a list to curb impulse buys; this strategy fights the cost-of-living creep, leaving room in your budget for real assets that shield your wealth.

- Educate yourself on inflation trends; knowledge is power, it empowers you to make savvy choices in savings and investments, dodging the traps of economic downturns.

The Role of Interest Rates in Inflation

Central banks raise interest rates to fight high inflation. They make borrowing cost more. People spend less money. Businesses slow down on loans for growth. Demand drops for goods and services.

Prices stop rising so fast. Think of interest rates as a brake pedal on a speeding car. Step on it, and the economy slows to a safer speed. This protects your purchasing power from eroding too quickly.

Savers earn more on their money in banks. Investors see shifts in stock market returns. Debt becomes pricier to carry, so folks pay off loans faster. Economic stability improves with these moves.

You feel the impact on your budget and savings. Picture a seesaw, where high rates tip the balance against runaway costs of living. Financial strategies include watching these rate changes closely.

Asset allocation adjusts to favor short-term bonds in such times. Low interest rates can spark inflation instead. Central banks cut rates to boost spending. Money flows freely into the economy. People buy more houses and cars. Businesses invest in new projects.

Supply struggles to keep up with demand. Prices climb as a result. Your wealth faces risks from this heated pace. Investments in real assets like property often shine here. Stocks might surge at first but falter later.

Consider how the Federal Reserve hiked rates in 2022 to tame inflation above 8 percent. That action cooled things down. You adapt by focusing on inflation-protected securities. Savings accounts yield better returns in high-rate eras.

Cost-of-living pressures ease over time. Economic impact hits different income groups unevenly. Stay alert to these signals for smart financial decisions. Debt management becomes crucial to avoid traps.

Final Thoughts

Inflation eats away at your money’s value, hits savings hard, and shakes up investments like stocks and real estate. You can fight back with smart moves, like diversifying your portfolio or picking inflation-protected bonds.

These steps keep things simple and work well for most people. Protect your wealth now, and watch it grow stronger against rising prices. Check out books on financial planning or talk to a money expert for more tips. Take charge today, your future self will thank you.

FAQs on Inflation Impact On Wealth

1. What is inflation, and how does it mess with my wealth?

Inflation is like a sneaky thief that steals your money’s power over time, making everything cost more. It shrinks what your dollars can buy, so your wealth feels the pinch. Think of it as your savings slowly melting like ice cream on a hot day.

2. How can I shield my savings from rising prices?

Invest in things that grow faster than inflation, like stocks or real estate. That way, your money keeps up with the climbing costs.

3. Does inflation hit my investments hard?

Yes, it can erode returns if your investments lag behind price hikes.

4. What quick steps can I take to fight inflation’s bite?

Start by tracking your spending to spot waste, then shift some cash into inflation-beating options like bonds or commodities. Talk to a financial buddy for tips tailored to you; remember, beating inflation is like training for a marathon, it takes steady effort. And hey, don’t panic, we’ve all been there, adjusting sails in this economic wind.