Imagine starting from zero, working hard every day, yet watching your efforts fade away when you pass on. Many folks face this tough spot, scraping by paycheck to paycheck, dreaming of a legacy that supports their kids and grandkids.

They worry about bills piling up, no safety net in sight, and wonder if real change is possible. Building generational wealth feels like chasing a rainbow sometimes, but hey, it’s within reach if you know the steps.

Did you know that families who plan ahead often pass down three times more assets than those who don’t? This blog breaks it down simply, from smart saving tricks to real estate wins, helping you create a solid plan that sticks. Stick around.

What Is Generational Wealth?

You’ve just dipped your toes into why building wealth from scratch feels like a big deal in our introduction. Now let’s get clear on the basics. Generational wealth means assets and money that pass from one family group to the next, creating lasting financial security.

Think of it like planting a tree that grows fruit for your kids and grandkids, not just for you. This includes real estate, stocks, businesses, and savings that build over time through smart investment strategies. Families with it often enjoy more freedom, like funding education or starting ventures without starting at zero.

Picture a family business handed down, or a home that stays in the family for decades; that’s generational wealth in action. It goes beyond cash in the bank. Wealth creation here focuses on longterm assets, like retirement accounts and passive income streams, that compound and grow.

With good financial planning and asset allocation, you set up a safety net against tough times. Risk management plays a key role too, helping avoid pitfalls that could wipe out gains. In short, it’s about turning today’s efforts into tomorrow’s financial foundation for your loved ones.

Why Building Generational Wealth Matters

Now that you grasp what generational wealth means, let’s explore its real impact on your life and family. Generational wealth acts like a sturdy bridge, connecting today’s hard work to tomorrow’s security.

Families with this kind of wealth often escape the cycle of living paycheck to paycheck. Think about it, your kids could start businesses or buy homes without crushing debt. Wealth building creates financial security that lasts, much like planting a tree whose shade benefits generations.

Studies show families with inherited assets face less stress from economic dips. They invest in education and health, leading to better outcomes. You build this through smart financial planning and long-term investing.

Imagine passing down a family business that grows over time. That stability feels like a warm blanket on a cold night, doesn’t it? Debt management plays a key role here, keeping your assets safe from unnecessary risks.

Generational wealth also empowers future generations to chase dreams without financial chains. Picture your grandchildren traveling the world or starting innovative ventures, all thanks to your estate planning.

This wealth reduces inequality gaps, as data from the Federal Reserve highlights how inherited money boosts homeownership rates by 20 percent. You foster entrepreneurship by teaching investment strategies early.

Asset allocation spreads risks, turning small savings into substantial retirement accounts. Families avoid common pitfalls, like sudden tax hits, with proper tax planning. Empathy kicks in when you realize not everyone starts on equal footing; building wealth from scratch levels that field.

A touch of humor: it’s like giving your heirs a head start in the marathon of life, minus the sore feet. Risk management ensures your efforts compound over decades, creating passive income streams. Involve the family in budgeting techniques to sustain this legacy.

Foundations of Generational Wealth

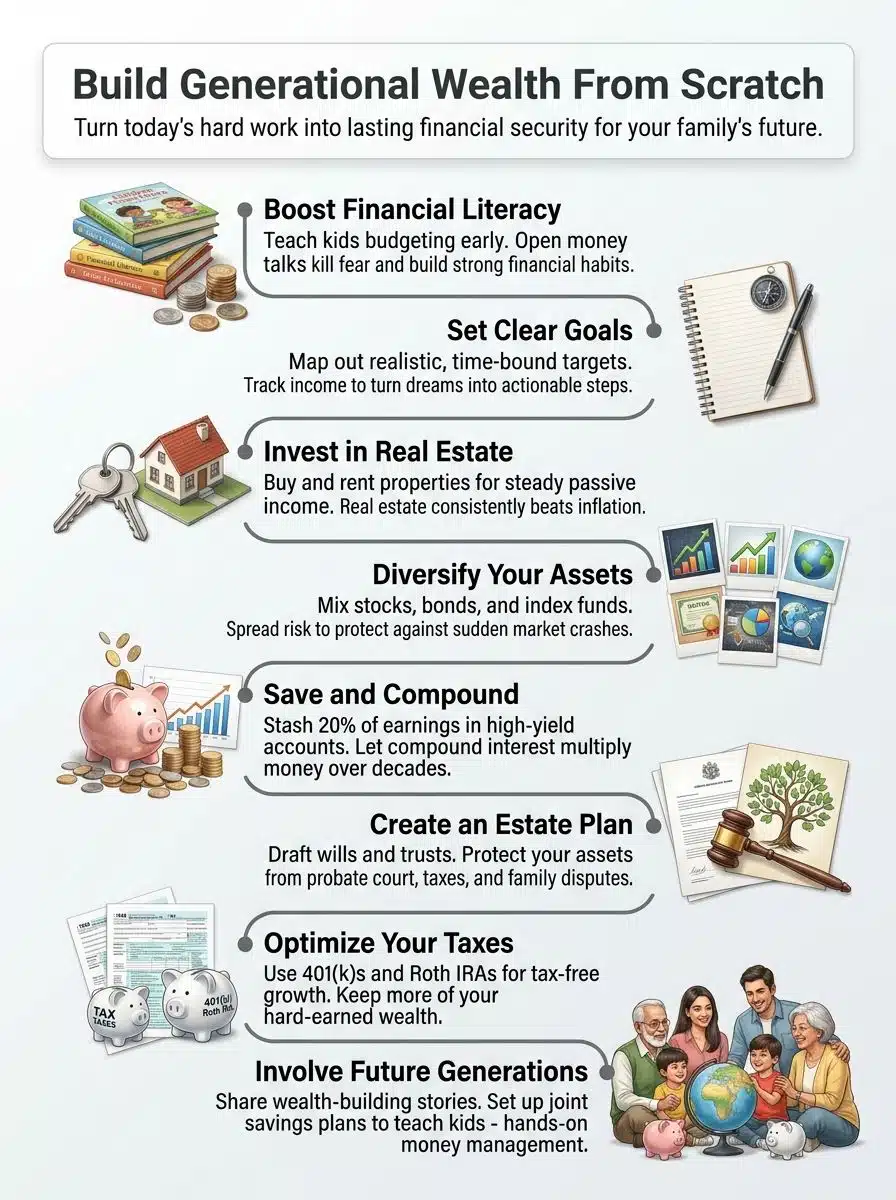

4. Foundations of Generational Wealth: Picture your family’s future as a sturdy house. You kick things off by grabbing financial smarts through education, nailing down sharp goals that everyone buys into, and sketching out a family plan that grows stronger each year.

Financial Literacy and Education

Financial literacy kicks off your path to wealth creation. You gain skills in budgeting techniques and debt reduction. Imagine this, like learning to drive before hitting the road; it keeps you from crashing your finances.

Families who teach kids about asset allocation early on see big wins. They build habits that last. Talk to your loved ones about money openly. Share stories from your own slips and triumphs. This sparks interest and cuts fear.

Education ties right into long-term planning. Explore books or online courses on investment strategies. Think of it as planting seeds for a family tree of financial security. Parents, show heirs how savings plans compound over time.

Use simple tools like apps for tracking expenses. Empathy helps here; everyone starts somewhere, right? Keep the chat light, maybe joke about that impulse buy you regret.

The more you learn, the more you earn. – Warren Buffett

Setting Clear Financial Goals

Clear goals act as your roadmap in wealth building. They keep you focused and motivated on the path to financial security.

- Start by assessing your current financial situation, like listing all debts and assets, to build a strong base for wealth creation. Picture yourself as a captain charting a course; without knowing your starting point, you might sail in circles. Use tools like budgeting apps to track income and expenses, ensuring every dollar works toward long-term planning.

- Define specific, measurable goals, such as saving $50,000 for a down payment on real estate in five years. This approach turns vague dreams into actionable steps, much like planting seeds that grow into a sturdy oak tree. Incorporate investment strategies here, aiming for milestones that align with retirement savings or passive income streams.

- Make your goals realistic and time-bound to avoid frustration and keep momentum high. For instance, if entrepreneurship excites you, set a target to launch a small family business within two years, factoring in risk assessment. Think of it as training for a marathon; you build endurance step by step, not in one giant leap.

- Involve your family in goal-setting discussions to foster unity and shared vision. Share stories around the dinner table about past financial wins or slips, turning it into a fun, empathetic chat. This builds financial literacy early, preparing heirs for wealth management and asset allocation down the line.

- Review and adjust goals regularly, say every six months, to adapt to life changes like job shifts or market dips. Life throws curveballs, so stay flexible, like a bamboo tree bending in the wind without breaking. Tie this to tax planning and debt reduction strategies to maximize your progress.

- Celebrate small victories along the way to keep spirits up and reinforce positive habits. Did you pay off a credit card? Treat the family to ice cream and chat about how it boosts your savings plan. Humor helps; joke that you’re turning pennies into a fortune, one high-five at a time.

With these goals in place, you can move on to creating a family financial plan.

Creating a Family Financial Plan

Building a family financial plan sets the stage for lasting wealth creation. This step turns dreams into actionable steps for financial security.

- Gather your family around the table to discuss everyone’s money goals, like saving for college or retirement accounts. Talk openly about incomes, expenses, and debts to spot areas for debt reduction. Use simple tools, like spreadsheets, to track everything. Imagine your plan as a roadmap that keeps everyone on track toward wealth management.

- Set specific, achievable targets for the short and long term, such as building an emergency fund within a year. Tie these to bigger aims, like real estate investing or starting a family business. Review progress quarterly and adjust as life changes. Think of it as planting seeds that grow into a sturdy tree of financial literacy for all.

- Include strategies for asset allocation to spread risks across stocks, bonds, and other investments. Explain why diversification matters, using examples like not putting all eggs in one basket. Teach heirs about risk management early to avoid common pitfalls. Picture your assets as a balanced diet that fuels long-term planning.

- Budget wisely by tracking monthly spending and cutting unnecessary costs, which boosts savings plans. Allocate funds for passive income sources, like dividend stocks. Share stories from families who turned small habits into big gains. It’s like training for a marathon, one step at a time, building endurance for wealth building.

- Factor in tax planning to minimize what you owe, perhaps through retirement savings or deductions. Consult experts for advice on optimizing returns. Use anecdotes from successful folks who saved thousands this way. View taxes as a puzzle you solve together for better financial planning.

- Plan for the unexpected with life insurance and emergency funds to protect your assets. Discuss scenarios, like job loss, to prepare everyone. This creates a safety net for entrepreneurship ventures. It’s akin to wearing a helmet while biking, smart and essential for long-term assets.

- Educate the whole family on investment strategies, starting with basic lessons on compounding. Use real examples, like how $100 invested young can grow massively. Make it fun with games or apps. Consider this the glue that holds your estate planning together for generations.

Strategies for Building Generational Wealth

You know that old saying, “Don’t put all your eggs in one basket”? Well, smart folks spread their money across real estate, stocks, and even a family business to watch it grow like a mighty oak over decades.

Imagine turning a small savings habit into a fortune through compounding, or flipping properties to create passive income streams that keep your kids’ kids smiling. Stick around, and we’ll break it down step by step.

Investing in Real Estate

Investing in real estate kicks off wealth-building like planting a money tree that grows for generations. You buy properties, fix them up, and rent them out for steady passive income.

Think about starting small, maybe with a duplex in your town, where tenants pay the mortgage while the value climbs. Real estate investing builds long-term assets that beat inflation, often appreciating 3 to 5 percent yearly based on market trends.

Families pass down these holdings, creating financial security that lasts. Diversify your approach to cut risks in this game. Mix rental homes with commercial spaces for better asset allocation. My neighbor, Joe, started with one condo in 2010; now his kids inherit a portfolio worth over $500,000.

Use tax planning perks, like deductions on repairs, to boost returns. This strategy fuels wealth creation, turning sweat equity into a family legacy without fancy tricks.

Diversifying Investments

Real estate gives you a solid start, but smart folks spread their bets to build real staying power. Think of your money like eggs in a basket; you don’t want them all in one spot if things go south.

Diversify investments by mixing stocks, bonds, and maybe some index funds. This approach cuts risk and boosts long-term assets. Picture a friend who lost big in one stock crash, but his buddy with a spread-out portfolio sailed through fine.

Spread out with asset allocation that fits your goals, like retirement accounts for steady growth. Add in some passive income streams, such as dividend stocks or ETFs. Families often thrive by blending real estate with these options for true financial security.

Talk to a pro about risk assessment to keep things balanced. Entrepreneurship can tie in too, turning side hustles into diverse wealth creators over time.

Starting and Growing a Family Business

Family businesses often kick off with a spark of passion, like turning your grandma’s secret cookie recipe into a local hit. You spot a need in the market, say, eco-friendly cleaning products, and jump in with both feet.

Start small; gather your loved ones around the kitchen table to brainstorm ideas. Assign roles based on strengths. Dad handles sales, while you manage the books. This builds wealth creation through hands-on entrepreneurship.

Keep costs low at first, bootstrap with savings to avoid heavy debt. As sales pick up, reinvest profits wisely. Think of it as planting a seed that grows into a sturdy oak, providing shade for generations.

Growth happens when you scale smartly, maybe expanding from online sales to a brick-and-mortar shop. Involve the kids early, teaching them budgeting techniques and risk management.

Share stories of setbacks, like that time a supplier flaked, to build resilience. Diversify offerings to create passive income streams, such as adding a subscription box service. Monitor finances closely, using simple tools for asset allocation.

Laughter helps too; joke about that failed product launch to keep spirits high. Now, let’s talk about saving and compounding over time.

Saving and Compounding Over Time

While a family business pumps fresh income into your pockets, true generational wealth blooms when you save smartly and let compounding work its magic. Start by stashing away at least 20% of your earnings each month in a high-yield savings account or retirement accounts like a 401(k).

Imagine your money as a snowball rolling downhill; it gathers size over time without much effort from you. Albert Einstein called compounding the eighth wonder of the world, and he nailed it, because $10,000 invested at 7% annual return grows to over $76,000 in 30 years.

This approach fits right into your financial planning and wealth management strategy. Pair saving with debt reduction to free up more cash for long-term investing. Cut high-interest debts first, like credit cards charging 20% or more, so your savings don’t fight against losses.

Diversify into stocks, bonds, or real estate investing for passive income that compounds steadily. Teach your kids these budgeting techniques early, turning them into savvy heirs who value financial literacy.

Picture a tree you plant today, its roots spread deep, providing shade for generations. Stick to this savings plan, and watch asset allocation build your financial security brick by brick.

Common Mistakes to Avoid When Building Generational Wealth

Hey, you hustle to create a lasting legacy for your family, but pitfalls like ignoring key plans or skipping money talks with your kids can wipe out everything you’ve built, so spot these errors early to keep your wealth rock solid. Craving tips on dodging them? Keep scrolling for the full scoop!

Failing to Create an Estate Plan

Failing to create an estate plan can derail your generational wealth dreams, like building a castle without a solid gate. You work hard to build assets, but without a plan, taxes and legal fees eat them up after you pass.

Estate planning protects your family’s future through wills, trusts, and clear instructions. Many folks skip this step, thinking it’s too complex or far off, yet it secures long-term assets and cuts down on family disputes.

Picture your kids fighting over inheritance; a good plan avoids that mess. Smart wealth management includes this key move to pass on riches smoothly.

People often ignore estate planning, leading to lost fortunes in probate court. Set up a will early to direct your assets where you want them. Use trusts for tax planning and to shield wealth from creditors.

This keeps your hard-earned money in the family for generations. Don’t let oversight rob your heirs of financial security. Now, let’s talk about the lack of financial education for heirs.

Lack of Financial Education for Heirs

Many heirs lose hard-earned wealth because they lack basic financial literacy. Imagine this: you build a fortune through smart investment strategies and long-term planning, only for your kids to squander it on poor choices.

They might not grasp asset allocation or debt reduction. Teach them early about budgeting techniques and risk management. Share stories from your own journey in wealth creation. Make it fun, like turning family dinners into quick lessons on passive income.

Empathy kicks in here; no one wants their legacy to vanish. Involve heirs in discussions about retirement savings and tax planning. Show them real examples of entrepreneurship or real estate investing.

This builds financial security for generations. Avoid this pitfall, and watch your family thrive with solid wealth management skills.

Mismanagement of Family Assets

Family assets can slip away fast if you don’t handle them right. Imagine your hard-earned money vanishes like sand through your fingers because of poor choices. People often chase quick wins in investments, ignoring solid asset allocation.

They forget about risk assessment, leading to big losses. Take real estate investing, for example, folks buy properties without a clear plan, then face debt management woes. A family business might crumble if no one tracks expenses well.

I get it, life’s busy, but skipping budgeting techniques hurts long-term planning. Talk to your loved ones about these pitfalls, share stories from friends who learned the hard way. Wealth management demands steady hands, not reckless moves.

Bad habits in asset management pass down, eroding financial security for kids and grandkids. Diversify, sure, but don’t spread too thin without research. I’ve seen folks ignore tax planning, only to pay hefty bills later.

Retirement accounts sit untouched, missing out on growth. Entrepreneurship sounds great, yet without risk management, it flops. Build habits now, like reviewing investments yearly.

Passive income streams help, but mismanage them, and poof, they’re gone. Empathy here, we all make mistakes, but we learn from them quickly.

Tools to Protect Generational Wealth

You’ve worked hard to stack up that family fortune, so don’t let taxes or surprises wipe it out, grab some smart shields like trusts to keep it locked down for your kids. Picture your wealth as a sturdy oak tree, and these strategies as the roots that hold it firm through any storm, ready to pass on the shade for generations.

Trusts and Estate Planning

Trusts act as smart tools in estate planning. They let you control how your assets pass to heirs. You set up a trust to hold property, like homes or stocks. A trustee manages it for your family’s benefit.

This setup avoids probate court hassles. Probate can eat up time and money. Families save on taxes, too, with proper tax planning. Think of trusts as a safety net for your wealth management goals.

Estate planning keeps your wishes clear after you’re gone. Draft a will to name who gets what. Add powers of attorney for health and finances. Life insurance fits in here, boosting financial security.

Involve a lawyer to tailor these steps. Your kids learn asset allocation early this way. Avoid surprises that erode longterm assets. Pass on wealth smoothly, like handing off a baton in a relay race.

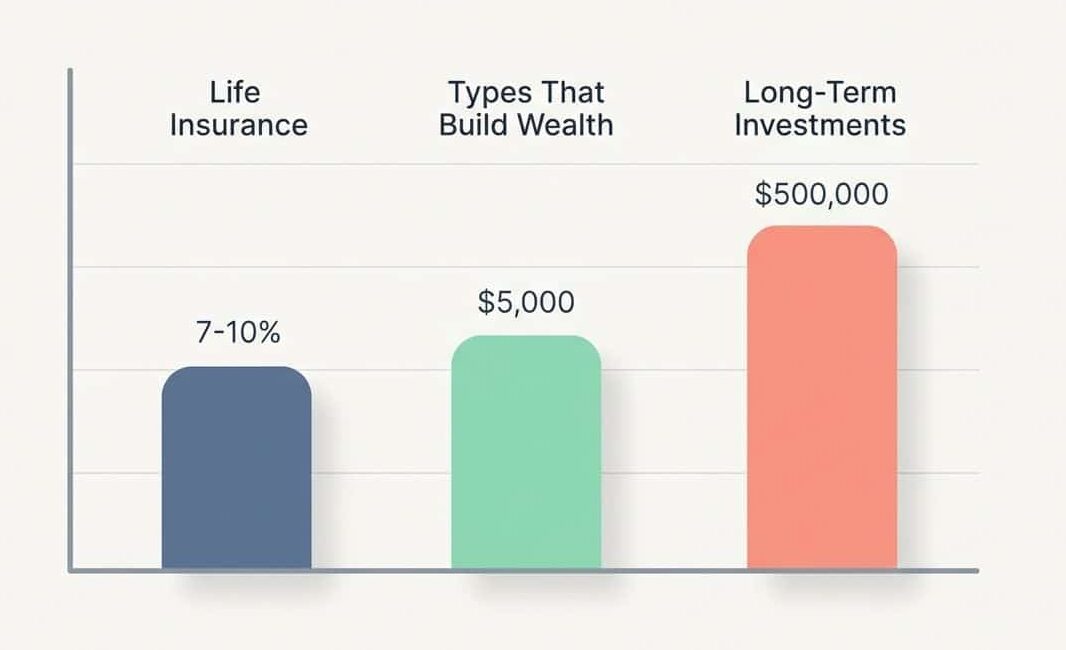

Life Insurance and Long-Term Investments

While trusts and estate planning lay the groundwork for safeguarding your assets, life insurance and long-term investments add powerful layers of protection and growth for your family’s future. Think of them as the dynamic duo that keeps your wealth engine running smoothly across generations.

| Aspect | Key Points |

|---|---|

| Why Life Insurance Fits In | Life insurance acts like a safety net. It pays out to your loved ones if you pass away. This cash helps cover debts, living costs, or even college tuition. Pick term life for affordable coverage during your working years, or whole life for lifelong protection with a savings component. You shield your family from financial shocks, keeping the wealth-building momentum alive. |

| Types That Build Wealth | Go for permanent policies like universal life. They build cash value over time, which you can borrow against tax-free. Imagine it as a piggy bank that grows while protecting your heirs. Variable policies tie into investments, potentially boosting returns, but watch the risks. Families often use these to fund estates or businesses without selling off assets. |

| Long-Term Investments Basics | Focus on stocks, bonds, and mutual funds for steady growth. Compound interest works magic here; start early, and small amounts balloon over decades. Picture planting a seed that turns into a mighty oak for your grandkids. Diversify to spread risk, like not putting all eggs in one basket. |

| Real-World Strategies | Invest in index funds for low-cost market exposure. They track the S&P 500, delivering average annual returns of around 7-10% historically. Add Roth IRAs for tax-free growth; contribute now, and your heirs withdraw without taxes. One family I know started with $5,000 yearly investments; by retirement, it hit over $500,000. You create a legacy that pays dividends, literally. |

| Combining Insurance and Investments | Link life insurance with investment accounts. Use policy proceeds to fuel retirement funds or trusts. This combo multiplies wealth; insurance covers gaps, while investments grow the pot. Families thrive when you plan this way, turning “what if” worries into “we’ve got this” confidence. Hey, it’s like giving your wealth a turbo boost. |

| Tips for Success | Review policies yearly; life changes fast. Work with advisors to match investments to your risk tolerance. Teach kids about these tools early, so they carry the torch. Avoid high fees that eat into gains. You build not just money, but security and stories for generations. |

Tax Optimization Strategies

Life insurance and long-term investments safeguard your assets, but smart tax moves amplify their power for lasting family security. Imagine you work hard to grow wealth, yet taxes can eat away at it like a silent thief in the night.

Tax optimization strategies help you fight back. Start with basic tax planning to lower what you owe each year. Use retirement accounts like 401(k)s or IRAs for tax breaks on contributions.

These tools let earnings compound without immediate tax hits, boosting long-term assets over decades. Deduct mortgage interest on real estate investments too, a simple way to cut your bill. Chat with a tax advisor about credits for education or energy-efficient home upgrades; they add up fast.

Shift focus to estate planning for bigger wins in wealth management. Set up trusts to pass assets with minimal estate taxes, keeping more for heirs. Consider gifting money annually within IRS limits to reduce your taxable estate over time.

Roth conversions turn traditional IRA funds into tax-free growth for future generations. Diversify with municipal bonds; their interest often skips federal taxes altogether. Manage capital gains by holding investments longer for lower rates.

Balance asset allocation to harvest losses that offset gains, a savvy risk management play. Teach kids these investment strategies early, so they build on your foundation without costly slip-ups.

The Role of Financial Literacy in Sustaining Wealth

Financial literacy acts as the backbone for keeping wealth alive across generations. Imagine your money as a garden; without knowing how to plant, water, and prune, weeds take over fast.

You learn budgeting techniques to control spending, and that stops leaks in your finances. Families with strong financial literacy spot smart investment strategies early. They build passive income streams, like rental properties or dividend stocks, that grow without constant effort.

Think of Warren Buffett, who started young and compounded his knowledge into billions. He teaches us that understanding asset allocation keeps risks low and rewards high. Parents pass this wisdom to kids, turning family talks into lessons on debt reduction.

Empathy kicks in here, folks, because life’s curveballs hit everyone, but knowledge helps you swing back strong. You sustain wealth by making informed choices every day. Picture a family business thriving because heirs grasp tax planning basics. They avoid pitfalls that drain assets, like hidden fees in retirement accounts.

Financial security comes from assessing risks before jumping in. Start with simple steps, such as tracking expenses in a savings plan. Entrepreneurship flourishes when you know how to manage cash flow.

Longterm planning turns small habits into big fortunes. Share stories around the dinner table about real estate investing wins and losses. That builds confidence in future leaders.

Wealth management becomes a team sport, where everyone contributes ideas on asset management. Humor aside, don’t let ignorance play the villain in your wealth story; knowledge flips the script.

How to Involve Future Generations in Wealth Planning

Involving your kids and grandkids in wealth planning keeps the family legacy strong and teaches them smart money habits early. You build a team effort that lasts, turning financial security into a shared adventure.

- Start family talks about money when kids hit their teens, sharing stories from your own wealth creation journey to spark interest in financial literacy and long-term planning.

- Teach budgeting techniques through fun games, like a pretend family business where everyone tracks expenses, which boosts their skills in debt management and asset allocation.

- Include heirs in investment strategy meetings, explaining simple choices like retirement accounts or real estate investing, so they grasp risk assessment without feeling overwhelmed.

- Set up joint savings plans for big goals, such as college funds, and watch compounding grow the pot, showing passive income in action with real numbers.

- Role-play estate planning scenarios, acting out what happens if assets get mismanaged, to highlight the need for trusts and tax planning in wealth management.

- Encourage entrepreneurship by helping them launch small ventures, tying it to family wealth-building, and celebrate wins with tales of famous business folks who started young.

- Share books or online courses on financial security, discussing key points together, which plant seeds for their own investment strategies down the line.

- Plan family retreats focused on long-term assets, like visiting properties or reviewing portfolios, mixing in humor about “money trees” that actually grow through smart choices.

- Foster open chats about debt reduction, using anecdotes from your life to show how avoiding bad loans leads to stronger financial planning for everyone.

Wrapping Up

You made it this far in your wealth-building journey, and that’s a big win. Think of generational wealth as a sturdy tree that grows stronger with each passing year. Plant those seeds now through smart financial planning and long-term investing.

Get your family on board with estate planning to keep assets safe. Cut down on debt management issues by focusing on asset allocation and risk management. Imagine passing down financial security like a treasured family recipe.

Stay consistent with your savings plan and watch passive income streams flow in. Talk to your loved ones about investment strategies and wealth management early. Share stories of entrepreneurship that built empires from nothing. Use tax planning to shield your hard-earned gains.

Building this legacy takes grit, but the payoff brings lasting joy. Envision your grandkids thriving thanks to your real estate investing moves. Keep financial literacy central to it all.

FAQs on Building Generational Wealth

1. What does generational wealth mean, and why should I care about building it from scratch?

Generational wealth is money and assets passed down through your family, like a sturdy oak tree that shades generations. It gives your kids a head start, avoiding the rat race you might have faced. Picture this: your grandkids thanking you for that college fund you started with pocket change.

2. How can I start building generational wealth with no money to my name?

Begin by saving small amounts consistently, like pennies in a jar that grow into a mountain. Invest in low-cost index funds or real estate to let your money work for you over time.

3. What key steps help in creating lasting wealth for my family?

Educate yourself on smart budgeting to cut unnecessary spending. Start a side business, perhaps selling handmade crafts online, to boost income. Always think long-term, passing on financial wisdom to your children like a treasured family recipe.

4. Are there common pitfalls to avoid when trying to build wealth from nothing?

Don’t chase get-rich-quick schemes; they’re like fool’s gold.